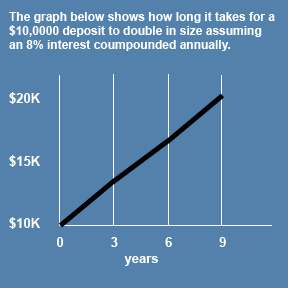

Meghna Khanna has just got her first job after graduation. She plans to work for a few years before going back to school to get a management degree. She likes spending, but is equally keen to save for her studies. Though her parents live comfortably, they are not wealthy enough to fully fund her education. Allocating a large sum towards higher studies will compromise their other goals, but they will help her as much as they can. Meghna is tempted to leave home and fend for herself now that she is employed. She likes her financial independence, but wants to be sure that she does not take wrong decisions when it comes to money matters. What should she do?

Meghna's key goal is to fund her higher education, but she must first ascertain whether her saving would be adequate to cover the cost. She should clock a conservative rate of return by using a bank deposit rate on her investments in which she will deploy her savings. For the balance amount, she can seek a bank loan. She should choose a management school that has a good placement record, so she can hope to repay the loan without any difficulty. Since her parents are willing to support her routine needs, Meghna should use this to increase her monthly savings. She should not move out on an impulse as it would significantly increase her expenses and reduce her ability to save. For her parents, this arrangement would seem a much better proposition compared with funding a large sum towards her higher education.

Since Meghna knows that she will need an education loan in the future, she should work on building a good relationship with her bank. She should ensure that she builds her deposits in one bank account and also have a clean record. She should avoid taking a credit card at this point of time and also not take personal loans. If she does take a loan, she should repay it on time and have a good credit record. Since the money that is not saved invariably ends up being spent, Meghna should begin a systematic investment plan that debits her account towards the chosen investment.

Tuesday 9 August 2011

Monday 8 August 2011

Stockmarket crisis: Q&A

As markets lose billions of pounds in value this week, Harry Wallop explains how the crisis came about and what it all means.

7:47AM BST 06 Aug 2011

Q. Why have stockmarkets fallen so heavily this week?

A. Markets falls when there are more sellers than buyers. Investors around the world have become increasingly nervous about where to put their money, amid fears of the global economy entering a fresh recession and the entire Eurozone area collapsing because of mounting Government debts in Italy and Spain. As a result many investors – both private and the institutions who invest our pension funds – have started to sell.

Q. So how serious is the risk of another global recession?

A. Ironically, many British companies, especially engineering firms, have reported stellar financial results this week, announcing to the London Stock Exchange that they have never enjoyed such good business on the back of a resurgence in global travel and trade.

America reported a better-than-expected improvement in unemployment on Friday.

But there are some signs that China, whose booming middle classes have helped keep global consumption above water, is starting to slightly slow down. And many economies such as Italy, America and Britain are barely moving forward. Families here, and around the world, reacted quite sensibly to the financial crisis of 2008 and started to pay off their own household debts and save a little bit of money.

While this was very sensible for individual families, it was disastrous for the economy – it meant people stopped spending, causing problems for the high street.

Q. And the Eurozone? Why is it in such poor shape?

But there are some signs that China, whose booming middle classes have helped keep global consumption above water, is starting to slightly slow down. And many economies such as Italy, America and Britain are barely moving forward. Families here, and around the world, reacted quite sensibly to the financial crisis of 2008 and started to pay off their own household debts and save a little bit of money.

While this was very sensible for individual families, it was disastrous for the economy – it meant people stopped spending, causing problems for the high street.

Q. And the Eurozone? Why is it in such poor shape?

A. It's all to do with debt. Governments in Europe have just too much debt and there is a real concern they cannot pay back their creditors.

Much of this problem has come about from the financial crisis of 2008, when governments around the world propped up the banking system – also saddled with too much debt – by transferring many of problematic loans from the private sector to the public sector. In Britain, this manifested itself in the taxpayer buying majority stakes in Lloyds Banking Group and RBS.

Many governments also reacted by pumping taxpayers' money into the economy. While this staved off a global depression, it merely delayed problems rather than solving them.

Last year, Ireland had to be given an emergency loan, so too Greece. Earlier this year Portugal and then Greece again had to be bailed out.

Now the spotlight has turned to Spain and Italy. Quite simply these countries are not earning enough – from tax receipts – to pay off its debts. And the two countries' debts together are an eye-watering £2 trillion.

Italy's debt stands at about 120 per cent of gross domestic product (GDP) – or in other words, a fifth more than the country's annual economic output – and is one of the highest in the world.

Q. Can't the European Central Bank step in?

A. In theory, yes, it could. But its special backup body, the European Financial Stability Facility has just €440bn (£382bn) of firepower, not enough to cover Italy and Spain's debts of £1 trillion, and though this figure is meant to increase not all countries have signed it off.

European countries are split as to whether they should pump more money or not. This sense of indecision from politicians is not helped by the fact many are on holiday this week.

Q. Why does it matter if Italy or Spain defaults?

A. Because the people who hold Spain or Italy's debts are indirectly millions of ordinary consumers around the world. That's because Governments raise money by selling bonds – in essence IOUs. These are bought by banks and institutional investors, on behalf of ordinary pension funds, on the understanding the government will pay an annual interest payment and return the full amount of the loan when the bond "matures", either after a few months or a few years.

If a Government defaults, it can't pay its bondholders. That's you and me.

http://www.telegraph.co.uk/finance/financialcrisis/8684246/Stockmarket-crisis-QandA.html

http://www.telegraph.co.uk/finance/financialcrisis/8684246/Stockmarket-crisis-QandA.html

Opportunities amid the carnage

Nathan Bell

August 8, 2011 - 12:00PMWarren Buffett famously said, 'be greedy when others are fearful'. That's easier said than done. With the market falling 10 per cent over the past week, 'being greedy' might be the last thing on your mind.

It shouldn't be.

Cast your mind back to March 2009. When everyone was panicking back then some of the best buying opportunities in years arose amongst the turmoil.

Advertisement: Story continues below

A flood of disappointing news has panicked investors but this sell-off is offering some equally good bargains.

The US is slipping back toward recession, Europe is following, aided by sovereign debt fears and there are genuine concerns that Chinese demand won't keep Australia's economy bubbling along.

The health of the global economy is at risk but this time, governments' ability to manage spiralling deficits and cut interest rates is greatly reduced.

While the problems are real - governments do need to rein in spending and the economy isn't recovering as hoped - in many cases share prices already reflect the bad news.

Over the past 18 months we've been advising investors to increase their cash holdings. Now is the time to deploy some of it (but not all; we may well get more opportunities down the track).

The question is where?

Avoidance strategy

Firstly, we're steering clear of the big four banks. If the economy really falters, they will be hit hard.

Better to focus on best-of-breed companies with excellent defensive qualities: stocks like CSL, QBE Insurance, Sonic Healthcare and Woolworths, all now attractively priced (although our recommendations on them differ).

For the more aggressive, less conservative investor, real value is starting to emerge in those sectors most exposed to financial markets. Macquarie Group, a very different business to what it was two years ago, currently yields 7.8 per cent after falling 21 per cent over the past fortnight.

Computershare (down 12 per cent over the past week) and some of the funds management businesses like Perpetual (down 45 per cent since October 2010) and Platinum Asset Management (down 10 per cent over the past two weeks) are also on our shopping list, as is News Corporation, already suffering from corporate scandal but plummeting a further 8 per cent over the past week.

Don't speculate

This is a challenging environment for all investors and, despite the abundance of opportunities, it's no time to be cavalier.

If you're a conservative investor, ignore speculative situations altogether. There is less reward and far more risk in buying cyclicals and speculative companies right now.

In contrast, best-of-breed companies, many of which sport attractive prices and have already found a place on our buy list, offer defensive qualities and a far gentler ride.

This is no time to be riding bareback but for the first time in a few years, I'm getting quite excited by the value on offer.

This article contains general investment advice only (under AFSL 282288).

Nathan Bell is research director of The Intelligent Investor.

For more Intelligent Investor articles click here.

Thursday 4 August 2011

Wednesday 3 August 2011

Three great US stocks on sale

With Aussie dollar riding high, there may never be a better time to buy American shares.

Whole bookshelves of research have been conducted to pin down the exact reasons for currency movements, with only moderate success. Broadly, the economic growth of a country and that country's interest rates (again, relative to others) are widely accepted as two of the key inputs.

Whatever the reasons, the dollar is now sitting well above parity. For many, this has the effect of making shopping and travelling overseas much more attractive. It's little wonder the growth of online retailing has been so strong.

Advertisement: Story continues below

Just as the Australian dollar's appreciation has made buying clothes and books from overseas more attractive, the same should be said of shares. The dollar has appreciated by over 20 per cent from around $US0.90 in the space of a year. You can now buy 20 per cent more shares in a company listed on the New York Stock Exchange than you could this time last year.

Of course, that only applies if the share price is the same as it was 12 months ago. The broader point is that if today's price represents good value in US dollars, you're buying at a discount relative to that same valuation a year ago.

Buy shares like clothes – on sale

Many a value investor uses the analogy of clothes prices to explain their approach to buying shares. When the price of a shirt is reduced, you're likely to buy more, not less. While share price drops can be unnerving, they often provide an opportunity to buy great businesses 'on sale'. Rather than fearing the drop, you should be excited by the opportunity.

A cursory look at some household names on the NYSE and Nasdaq exchanges suggests that some of these companies may well be on sale.

An opportunity to buy?

Microsoft needs no introduction. The maker of the ubiquitous Windows operating system and Office productivity software as well as the must-have X-Box gaming console is trading at around the same price – in US dollars – as it was 5 years ago, while earnings per share (EPS) has grown 92 per cent. Microsoft is now selling for a price that implies little or no growth, at a price-earnings ratio of a touch over 10.

In December 2008, shares of US-based The Coca-Cola Company were trading at around US$63. Two and a half years later, they trade at a little less than 10 per cent more, despite EPS doubling since that time. Coke has a trailing P/E of only 12.6 times earnings.

Branding agency Interbrand ranked Apple as the 17th most valuable brand in the world in 2010. Unsurprisingly, given the success Apple has had with the iPod, iPhone and iPad, the share price has more than doubled in the past three years. Despite that meteoric rise, profits have grown at a faster pace – tripling in the last three completed financial years. While a price-earnings ratio of 15.7 isn't traditionally cheap, Apple's growth trajectory may well make today's price look inexpensive.

Foolish take-away

Great businesses with wonderful economics and significant competitive advantages should be at the top of every investor's watchlist. A United States-based investor has the opportunity to invest in these companies at what history may well deem undemanding multiples.

An investor with Australian dollars to deploy has the same opportunity, but with cash that today buys many more US dollars than this time last year.

Investing in shares overseas has rarely been easier for Australian investors. Many Australian and US-based brokerages offer access to US and European exchanges – just make sure you shop around for a good deal.

This article contains general investment advice only (under AFSL 400691).

Scott Phillips is The Motley Fool's feature columnist. Scott owns shares in Microsoft and Coca-Cola. The Motley Fool's purpose is to educate, amuse and enrich investors.

Read more: http://www.smh.com.au/business/three-great-us-stocks-on-sale-20110803-1iax2.html#ixzz1TwRjap00

Intelligent Investor: Six classic investing mistakes

Done well, value investing is a successful, proven, and safe way to invest.

The logic of the approach - buying an asset for less than its underlying value - is irrefutable, and the records of those that practice it are convincing.

However, an understanding of the principles of value investing isn't enough. In investing, mistakes are inevitable, and the key is to learn from them, and avoid repeating them. Here are six of the best.

Advertisement: Story continues below

1. Focusing only on the numbers

One of the most common investing mistakes, especially for the inexperienced, is to concentrate only on a stock's financial data.

Applying a price-to-earnings ratio, a book value multiple, or a discounted cash flow analysis can provide very precise estimates of value. But that's not all there is to analysing stocks.

The big four banks, for example, all carry forecast dividend yields of about 6% to 7%, and price-to-earnings ratios of around 10 to 12. Looking at the numbers, they're closely matched.

When you consider the risks entailed by ANZ's Asian expansion and National Australia Bank's (NAB) aggressive push for market share however, suddenly the numbers don't seem to tell the whole story.

These qualitative factors are the reason we favour Commonwealth Bank and Westpac over ANZ and NAB. Before looking at the numbers, make sure you truly understand the business that's generating them.

2. Mistaking permanent declines for temporary ones

In the hunt for value, it's often necessary to buy stocks with a few fleas. When businesses hit rough patches and earnings temporarily decline, it can be a great time to buy.

This strategy led to successful 'Buy' recommendations on Cochlear at $19.04 on 18 March 2004, and Leighton Holdings at $7.83 on 11 May of the same year.

We have a positive recommendation on Aristocrat Leisure today for the same reason.

While mismanagement, a poor product line-up, the strong Aussie dollar, and cyclical headwinds are all hurting Aristocrat in the short term, we expect this business to perform well in the long run.

The risk is if its current problems aren't temporary. If Aristocrat's profits stay permanently depressed, we'll have overpaid for this business, and be guilty of having mistaken Aristocrat's structural decline for a cyclical one.

3. Buying low-quality businesses

Owning high-quality businesses over the long run is the key to successful investing.

Unfortunately, high-quality businesses are seldom cheap. Value investors therefore often end up with portfolios full of cheap but low-quality stocks, entailing greater risk, more stress, and higher stock turnover.

It's better to fill your portfolio with high-quality businesses, especially if you're patient and buy opportunistically.

4. Neglecting economic considerations

“If you spend more than 13 minutes analysing economic and market forecasts, you've wasted 10 minutes.”

Ever since uttering that sentence, legendary fund manager Peter Lynch gave value investors a free pass to ignore the economy. Or so they thought.

Lynch's advice does not mean that you can completely ignore the economy. It means that the success of your investments should never rely on specific, short-term economic forecasts.

An investment in Rio Tinto, for example, hinges largely on the continued strength of China's economy and its building and infrastructure boom. That's an economic forecast we're not willing to gamble on at current prices.

An appreciation of cycles, rather than economic predictions, should underpin your stock purchases and disposals.

5. Ignoring the market

As a value investor, a healthy scepticism of the market's wisdom is a necessity: whenever you buy something, it should be because you think the market is pricing it incorrectly.

When you're right, the rewards of ignoring the market can be enormous. The market wrote RHG Group down from $0.95 to $0.05 before our positive recommendations were vindicated.

But when you're wrong, it can be a disaster. Backing ourselves over the market explains why we were far too late in pulling the pin on Timbercorp, for example.

Share price movements should never influence your analytical process. But it is necessary to be aware of them; they can offer a timely prompt to reconsider your thinking. When you're going against the grain, make sure you know why you disagree with the market and have good reason for doing so.

6. Mistaking price and value

If you're aiming to buy stocks for less than their intrinsic value, a lower price can only mean better value, right? Wrong.

Consider Telstra, which is trading close to its lowest ever price. By that simple logic, it should be more attractive than ever. But the decline of its traditional fixed-line business means it's just not worth the high of $9.20 it hit more than a decade ago, nor the $4.80 or so it traded at in 2008.

It's tempting to anchor to previous prices but they offer no clue regarding today's value. The fact that a stock has fallen does not in itself make it cheap; only the difference between its intrinsic value and the price at which it trades does.

Avoiding these classic value investing mistakes will do wonders for your returns. Use this six-point checklist to sift out these mistakes in your own portfolio.

Saturday 30 July 2011

Friday 8 July 2011

Margin of Safety

The margin of safety

Benjamin GrahamOctober 2nd, 2008The genius investor Warren Buffett once called it “buying one dollar for 70 cent”, the Margin of safety which was developed by the brilliant man Benjamin Graham in 1934. The precept of the margin of safety is very logic and works as follows.

Most people believe that the stock markets are rational, so that the stock-rate always reflects the actual value of a company. But that´s not true , you can prove that very easily. We you look back to the big ups and downs in times of a market crash. It´s definitely not logical that a company looses 60 % of its value and wins 120 % back in a short period of 2 years while the earnings constantly grow by 5 %. So we can conclude that the markets are irrational because sometimes the people become too afraid and sell very cheap stocks and sometimes they are just too optimistic and buy too expensive stocks. It´s not very intelligent but most people like to follow the herd.

But now, let´s get back to the margin of safety. If you know that the stock markets are irrational then why don´t make profit of it? First you look for very unpopular “cheap” stocks, the market capitalisation has to be far below the intrinsic value. That could be companies in trouble, after they reported bad news or complete industries with problems.

Now you calculate the value of the company in order to do that you can use different methods. 1. The Earning-capacity value 2. The Net asset value3. The liquidation value. So for example, if you calculated that the intrinsic value of a company has the value of 100 Million USD, but the market capitalisation just lies at 70 Million USD, you get a margin of safety of 30% or 30 Million USD. You buy this stock and when the market capitalisation achieves the intrinsic value again you sell it.

Note: The margin of safety has not to be exactly 30 percent, but the higher it is the safer is the investment.

http://www.pearl-invest.net/benjamin-graham/ben-grahams-margin-of-safety/

Saturday 2 July 2011

Subscribe to:

Posts (Atom)