A great company deserves a higher valuation. It is possible that you paid a slightly higher price than you wanted to pay for the stock, which lowers your overall rate of return, but time is on your side and your long holding time minimizes the impact of the higher purchase price to your overall return. Also, you will always find the opportunity to add to your position at lower valuations, though not necessarily at lower prices.

Deep value investing investors need to be cautious and aware of this approach's inherent problems. Those companies dropping and appearing in the deep-bargain screen probably deserved to be traded by low valuations. Their stock prices were likely low for the right reasons, and buying these would likely have resulted in steep losses.

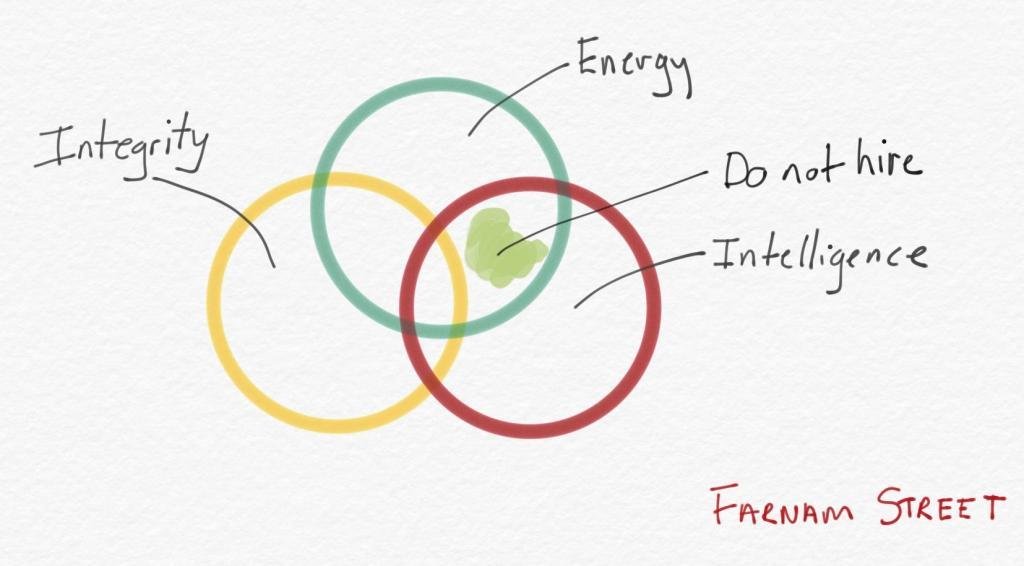

How do you select your stocks: Quality First, then Value.

There are many gruesome companies in the stock market. These companies operate in very competitive environments and have to be managed well to deliver good returns. In the business world, it is often the economics of the business that eventually triumph over the skills of the managers, however superb their skills maybe.

A company that performed well for 3 years and then lose its good performance subsequently is not a great company, by definition. A great company is one that can perform well, consistently and growing its earnings over 20 to 30 years.

Not uncommonly, these gruesome companies trade at below their net tangible asset prices. This is to be expected, especially if their businesses continue to be gruesome. Their low trading prices attract some investors who are enticed by the very low price relative to their net asset value.

Here is a very important point for any investor. When the price of a company falls, all its valuation ratios become very good. Its price to book value, its price to sales and its price to earnings ratios, all fall and its dividend yield (using last year's dividends) rises.

The uninitiated may think these companies are now undervalued using these financial ratios. Here lies the risk of searching for undervalued stocks in gruesome companies.

The more intelligent investors do not solely rely on these financial ratios alone, they require a lot more analysis. As a general rule, most shares are priced appropriately most of the time. It is only some of the time, when they are mis-priced too low or too high.

The risk in buying great companies is overpaying too much to own it. However, great companies do have earning power for many years, by definition. They continue to grow their intrinsic value over time. If you can acquire these companies at bargain prices (very rarely) or at fair prices (commonly), you should do well in your long term investing. Also, it is alright to pay a little bit more to own these companies as over the long time of holding them, they will still reward you handsomely. As these great companies are few, selling them only make a lot of sense if you can find another of equal quality (very difficult indeed) that offers higher reward to downside risk with high degree of probability. Well, not unexpected, this is not easy.

Buffett says: Buying a wonderful company at a fair price is better than buying a fair company at a wonderful price. He is absolutely right. Stay with quality first, then value; and your investing over the long term should be quite safe and mistakes, if any, will be few.

Deep value investing investors need to be cautious and aware of this approach's inherent problems. Those companies dropping and appearing in the deep-bargain screen probably deserved to be traded by low valuations. Their stock prices were likely low for the right reasons, and buying these would likely have resulted in steep losses.

How do you select your stocks: Quality First, then Value.

There are many gruesome companies in the stock market. These companies operate in very competitive environments and have to be managed well to deliver good returns. In the business world, it is often the economics of the business that eventually triumph over the skills of the managers, however superb their skills maybe.

A company that performed well for 3 years and then lose its good performance subsequently is not a great company, by definition. A great company is one that can perform well, consistently and growing its earnings over 20 to 30 years.

Not uncommonly, these gruesome companies trade at below their net tangible asset prices. This is to be expected, especially if their businesses continue to be gruesome. Their low trading prices attract some investors who are enticed by the very low price relative to their net asset value.

Here is a very important point for any investor. When the price of a company falls, all its valuation ratios become very good. Its price to book value, its price to sales and its price to earnings ratios, all fall and its dividend yield (using last year's dividends) rises.

The uninitiated may think these companies are now undervalued using these financial ratios. Here lies the risk of searching for undervalued stocks in gruesome companies.

The more intelligent investors do not solely rely on these financial ratios alone, they require a lot more analysis. As a general rule, most shares are priced appropriately most of the time. It is only some of the time, when they are mis-priced too low or too high.

The risk in buying great companies is overpaying too much to own it. However, great companies do have earning power for many years, by definition. They continue to grow their intrinsic value over time. If you can acquire these companies at bargain prices (very rarely) or at fair prices (commonly), you should do well in your long term investing. Also, it is alright to pay a little bit more to own these companies as over the long time of holding them, they will still reward you handsomely. As these great companies are few, selling them only make a lot of sense if you can find another of equal quality (very difficult indeed) that offers higher reward to downside risk with high degree of probability. Well, not unexpected, this is not easy.

Buffett says: Buying a wonderful company at a fair price is better than buying a fair company at a wonderful price. He is absolutely right. Stay with quality first, then value; and your investing over the long term should be quite safe and mistakes, if any, will be few.