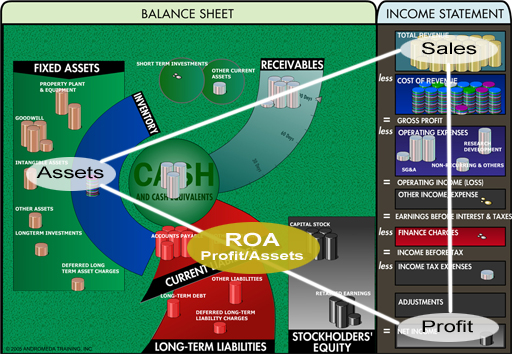

Warren Buffett believes that the return that a company gets on its equity is one of the most important factors in making successful stock investments.

DEFINING EQUITY

‘The interest of the stockholders in a company as measured by the capital and surplus.’

CALCULATING OWNER’S EQUITY

Investors can think of stockholders equity like this. An investor who buys a business for $100,000 has an equity of $100,000 in that investment. This sum represents the total capital provided by the investor.

If the investor then makes a net profit each year from the business of $10,000, the return on equity is 10%:

10,000 x 100

100,000

If however the investor has borrowed $50,000 from a bank and pays an annual amount of interest to the bank of $3500, the calculations change. The total capital in the business remains at $100,000 but the equity in the business (the capital provided by the investor) is now only $50,000 ($100,000 - $50,000).

The profit figures also change. The net profit now is only $6500 ($10,000 - $3,500).

The return on capital (total capital employed, equity plus debt) remains at 10%. The return on equity is different and higher. It is now 13%:

6,500 x 100

50,000

The approach to financing its operations by a company can obviously affect the returns on equity shown by that company.

WHY WARREN BUFFETT THINKS THAT RETURN ON EQUITY IS IMPORTANT

Just as a 10% return on a business is, all other things being equal, better than a 5% return, so too with corporate rates of returns on equity. Also, a higher return on equity means that surplus funds can be invested to improve business operations without the owners of the business (stockholders) having to invest more capital. It also means that there is less need to borrow.

WHAT RATE OF RETURN ON EQUITY DOES WARREN BUFFETT LOOK FOR?

This is a fluctuating requirement. The benchmarks are the return on prime quality bonds and the average rate of returns of companies in the market. In 1981, Buffett identified the average rate of return on equity of American companies at 11%, so an intelligent investor would like more than that, substantially more, preferably. Bond rates change, so the long-term average bond rate must be considered, when viewing a long-term investment.

In 1972, Buffett implied that a rate of return on equity of at least 14% was desirable. Although, at times, Warren Buffett has appeared to downplay the importance of Return on Equity, he constantly refers to a high rate of return as a basic investment principle.

COMPANY RATES OF RETURN ON EQUITY

It is significant that the majority of companies in the Berkshire Hathaway portfolio in 2002 all had higher than average returns on equity over a ten-year period. For example:

| Coca Cola | 45.05 |

| American Express | 20.19 |

| Gillette | 40.43 |

INVESTMENT DANGERS

There can be dangers in averaging returns over a long period. A company might start with high rates which then fall away, but still have a healthy average. Conversely, a company might be going in the opposite direction. As Warren Buffett looks for predictability in a company’s earnings, one would imagine that he would favour companies who increase their ROE or which have consistent levels.

COMPANY ANNUAL RATES OF RETURN

Compare the annual rates of return on equity of the following companies, using summary figures provided by Value Line.

| Year | Coca Cola | Gap Inc | Wal-Mart Stores |

| 1993 | 47.7 | 22.9 | 21.7 |

| 1994 | 48.8 | 23.3 | 21.1 |

| 1995 | 55.4 | 21.6 | 18.6 |

| 1996 | 56.7 | 27.4 | 17.8 |

| 1997 | 56.5 | 33.7 | 19.1 |

| 1998 | 42 | 52.4 | 21 |

| 1999 | 34 | 50.5 | 22.1 |

| 2000 | 39.4 | 30 | 20.1 |

| 2001 | 35 | 4.3 | 19.1 |

| 2002 | 35 | 13.1 | 20.4 |

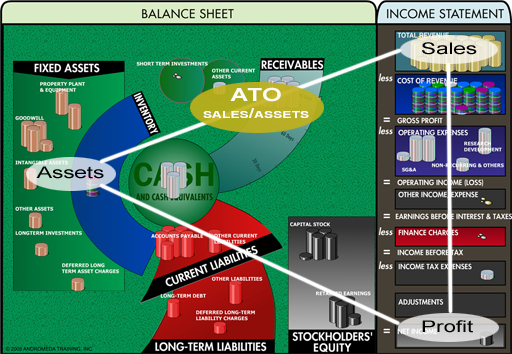

RETURN ON CAPITAL IS VERY IMPORTANT

The example early on this page shows that debt financing can be used to increase the rate of return on equity. This can be misleading and also problematical if interest rates rise or fall. This is probably one reason why Warren Buffett prefers companies with little or no debt. The rate of return on equity is a true one and future earnings are less unpredictable. A careful investor like Buffett would always take rates of return on total capital into account. The average rates of return of capital in the companies referred to above in Berkshire Hathaway portfolio are:

| Coca Cola | 39.12 |

| American Express | 13.68 |

| Gillette | 25.93 |

A comparison of the rates of return on equity and capital for these three companies is significant and the reader can make their own calculations.

http://www.buffettsecrets.com/return-on-equity.htm