The first thing we need to do is look for hard evidence that a firm has an

economic moat by examining its financial results. (Figuring out whether a company might have a moat in the FUTURE is much tougher.)

What we are

looking for are firms that can earn profits (ROIC) in excess of their cost of capital (WACC) - companies that can generate substantial cash relative to the amount of investments they make.

Use the metrics in the following questions to evaluate profitability:

1. Does the firm generate free cash flow? If so, how much?

Firms that generate free cash flow essentially have money left over after reinvesting whatever they need to keep their businesses humming along. In a sense, free cash flow is money that could be extracted from the firm every year without damaging the core business.

FCF Margin: Divide FCF by sales (or revenues). This tells what proportion of each dollar in revenue the firm is able to convert into excess profits.

If a firm's FCF/Sales is around 5% or better, you've found a cash machine.

Strong FCF is an excellent sign that a firm has an economic moat.

(FCF/Total Capital Employed or FCF/Enterprice Value are some measures.)

2. What are the firm's net margins?

Net margins look at probability from another angle.

Net margin = net income/ Sales

It tells how much profits the firm generates per dollar of sales.

In general, firms that can post net margins above 15% are doing something right.

3. What are the returns on equity?

ROE = net income/shareholders' equity

It measures profits per dollar of the capital shareholders have invested in a company.

Although ROE does have some flaws -it still works well as one tool for assessing overall profitability.

As a rule of thumb,

firms that are able to consistently post ROEs above 15% are generating solid returns on shareholders' money, which means they're likely to have economic moats.

4. What are returns on assets?

ROA = (net income + Aftertax Interest Expense )/ firm's average assets

It measures how efficient a firm is at translating its assets into profits.

Use 6% to 7% as a rough benchmark - if a firm is able to consistently post ROAs above these rates, it may have some competitive advantage over its peers.

The company's aftertax interest expense is added back to net income in the calculation. Why is that? ROA measures the profitability a company achieves on all of its assets, regardless if they are financed by equity holders or debtholders; therefore, we add back in what the debtholders are charging the company to borrow money.

Study these metrics over 5 or 10 years

When looking at all four of these metrics, look at more than just one year.

A firm that has

consistently cranked out solid ROEs, ROA, good FCF, and decent net margins

over a number of years is much more likely to truly have an economic moat than a firm with more erratic results.

Five years is the absolute minimum time period for evaluation, 10 years is even better, if you can.

Consistency is Important

Consistency is important when evaluating companies, because it's the

ability to keep competitors at bay for an extended period of time - not just for a year or two - that really makes a firm valuable.

These benchmarks are rules of thumb, not hard-and-fast cut-offs.

Comparing firms with industry averages is always a good idea, as is examining the

trend in profitability metrics - are they getting higher or lower?

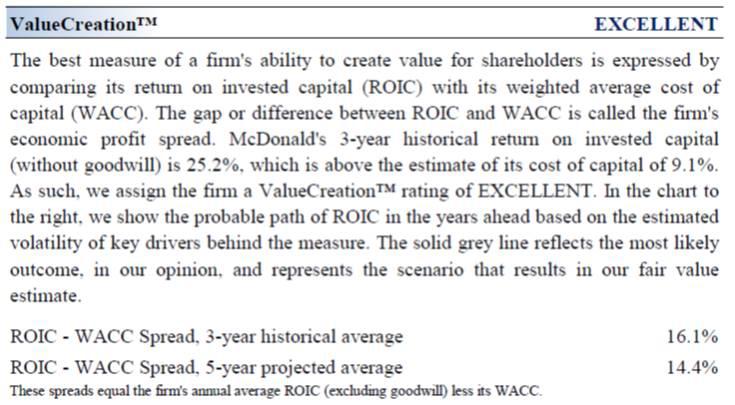

There is a more sophisticated way of measuring a firm's profitability that involves

calculating return on invested capital (ROIC), estimating a weighted average cost of capital (WACC), and then looking at the difference between the two.

Using a combination of FCF, ROE, ROE and net margins will steer you in the right direction.

Additional notes:

DuPont Equation

ROA = Net Profits / Average Assets

ROA = Asset Turnover x Net Profit Margin

ROA

= (Sales/Average Assets) x (Net Profits/Sales)

= Net Profits/Average Assets

ROE = Net Profits / Average Shareholder's Equity

ROE = Asset Turnover x Net Profit Margin x Asset/Equity Ratio*

ROE

= (Sales/Average Assets) x (Net Profits/Sales) x (Average Assets/Average Equity)

= Net Profits./ Average Equity

*Asset/Equity Ratio = Leverage

At each level of debt, calculate Newco's WACC, assuming the CAPM model is used to calculate the cost of equity.

At each level of debt, calculate Newco's WACC, assuming the CAPM model is used to calculate the cost of equity.