Vega

Vega measures the rate of change in the warrant price for each point of movement of its implied volatility.

No matter it is a call warrant or a put warrant, vega is always positive, indicating that the warrant price and its implied volatility always move in the same direction.

Vega can be an absolute value or a percentage relative to the warrant price.

Gamma

Gamma measures the sensitivity of the delta of a warrant to the price movements of its underlying.

The higher the gamma, the bigger the change in delta will be in reaction to a movement in the underlying price.

Gamma = Rate of Change of Delta / Rate of Change of Underlying Price

No matter it is a call warrant or put warrant, gamma is always positive.

Rho

Rho measures the sensitivity of warrant price to changes in the market interest rate.

Call warrants have a positive rho, meaning that the price of a call warrant moves in the same direction as the market interest rate.

In contrast, put warrants have a negative rho, and this shows that the price of a put warrant moves in the opposite direction to the market interest rate.

Given that changes in interest rates tend to be limited in the short term, their effect on warrant prices is minimal.

Showing posts with label vega. Show all posts

Showing posts with label vega. Show all posts

Friday, 11 September 2015

Technical Parameters of Warrants: Theta

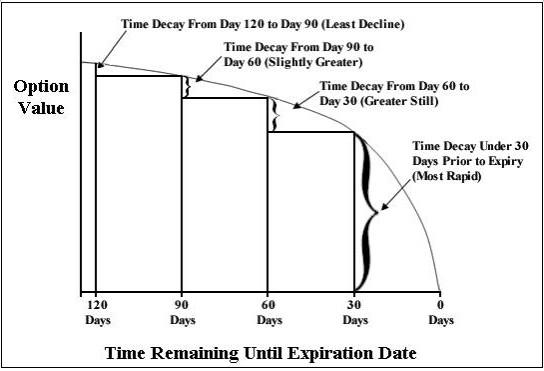

Theta, also called time decay, measures the rate of change in the price of a warrant as its maturity is running short while all other things being equal.

It can be expressed as an absolute value or a percentage relative to the warrant price (theta / warrant price).

Unless in some special circumstances, the value of theta is usually negative, reflecting the declining value of a warrant as time passes.

Depicted in a chart form, the slope of the curve of time value becomes steeper as the warrant gets closer to its maturity.

This shows that time decay accelerates as time passes.

Additional notes:

In percentage terms, time value has the biggest impact on out of the money (OTM) warrants.

The value of a warrant consists of intrinsic value and time value.

They vary in absolute and relative terms for warrants with different strike prices and maturity dates.

In the case of OTM warrants, their intrinsic values are negligible.

In other words, time value makes up most of their values.

Hence, they are more sensitive to the passage of time.

As for in the money (ITM) warrants, given that a large part of their value is made up of intrinsic value, they are less sensitive to the passage of time, and such sensitivity decreases as the maturity date gets nearer.

It can be expressed as an absolute value or a percentage relative to the warrant price (theta / warrant price).

Unless in some special circumstances, the value of theta is usually negative, reflecting the declining value of a warrant as time passes.

Depicted in a chart form, the slope of the curve of time value becomes steeper as the warrant gets closer to its maturity.

This shows that time decay accelerates as time passes.

Additional notes:

In percentage terms, time value has the biggest impact on out of the money (OTM) warrants.

The value of a warrant consists of intrinsic value and time value.

They vary in absolute and relative terms for warrants with different strike prices and maturity dates.

In the case of OTM warrants, their intrinsic values are negligible.

In other words, time value makes up most of their values.

Hence, they are more sensitive to the passage of time.

As for in the money (ITM) warrants, given that a large part of their value is made up of intrinsic value, they are less sensitive to the passage of time, and such sensitivity decreases as the maturity date gets nearer.

Subscribe to:

Posts (Atom)