We can use free cash flow as a tool for checking the quality of a company's profits.

The stock market has been littered with companies that seemed to be very profitable but turned out to be anything but.

Investors can save themselves a lot of heartache and some painful losses by taking a few minutes to study how effectively a company converts profits into free cash flow.

One of the simplest and best ways to test the quality of a company's profits and whether you think they are believable or not is to compare a company's underlying or normalised earnings with its free cash flow.

The free cash flow will show you how much surplus cash the company has left over to pay shareholders. It can often be very different from EPS, even though it is supposed to tell you the same thing. For most years, you want to see the free cash flow has been close to earnings.

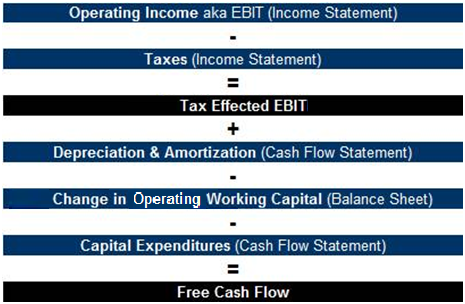

Calculating free cash flow

Example: Company Z ($ m)

Net cash flow from operations 69.0

Capex -6.8

FCF to the firm (FCFF) 62.7

Minority or preference dividend paid 0.0

Interest paid -0.3

Interest received 0.0

FCF for shareholders (FCF) 62.4

Weighted average number of shares in issue 504.6m

FCF per share 12.37 sen

Underlying EPS 11.9 sen

Quality companies turn most of their profits into free cash flow on a regular basis

![{\displaystyle FCFE=NI-[(1-b)(Capex-D\&A)+(1-b)(\Delta WC)]}](https://wikimedia.org/api/rest_v1/media/math/render/svg/13b79e03b9e2ed84404dcc77a21ef8bed0868d3d)