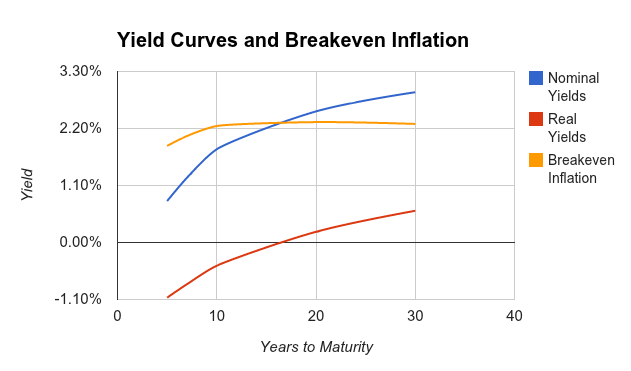

Real Yields = Nominal Yields - Breakeven Inflation

The stock market has the power to turn a single dollar into millions by the forbearance of generations - but few will have the patience or desire to let this happen.

Total Returns vs Total Real Returns

The focus of every long-term investor should be growth of purchasing power - monetary wealth adjusted for the effect of inflation. The growth of purchasing power in equities not only dominates all other assets but also shows remarkable long-term stability. Despite extraordinary changes in the economic, social and political environments over the past two centuries, stocks have yielded between 6.6 and 7.0 percent per year after inflation in all major subperiods.

The wiggles on the stock return line represent the bull and bear markets that equities have suffered throughout history. The long-term perspective radically changes one's view of the risk of stocks. The short-term fluctuations in the stock market, which loom so large to invetors when they occur, are insignificant when compared with the upward movement of equity values over time.

In contrast to the remarkable stability of stock returns, real returns on fixed-income assets have declined markedly over time. From 1802 to 1926, the annual real returns on bonds and bills, although less than those on equities, were significantly positive. However, since 1926, and especially since World War II, fixed-income assets have returned little after inflation.