Is SVB a canary in the coal mine?

Clearly, the situation is quite different in Malaysia. For starters, pandemic cash handouts were far smaller and, while deposits also rose during the pandemic — owing to loan moratoriums and lower spending — it was nowhere near the scale of that in the US. Total deposits increased from RM1.968 trillion to RM2.186 trillion between March 2020 and March 2022, or equivalent to just about 11% growth (see Chart 2).

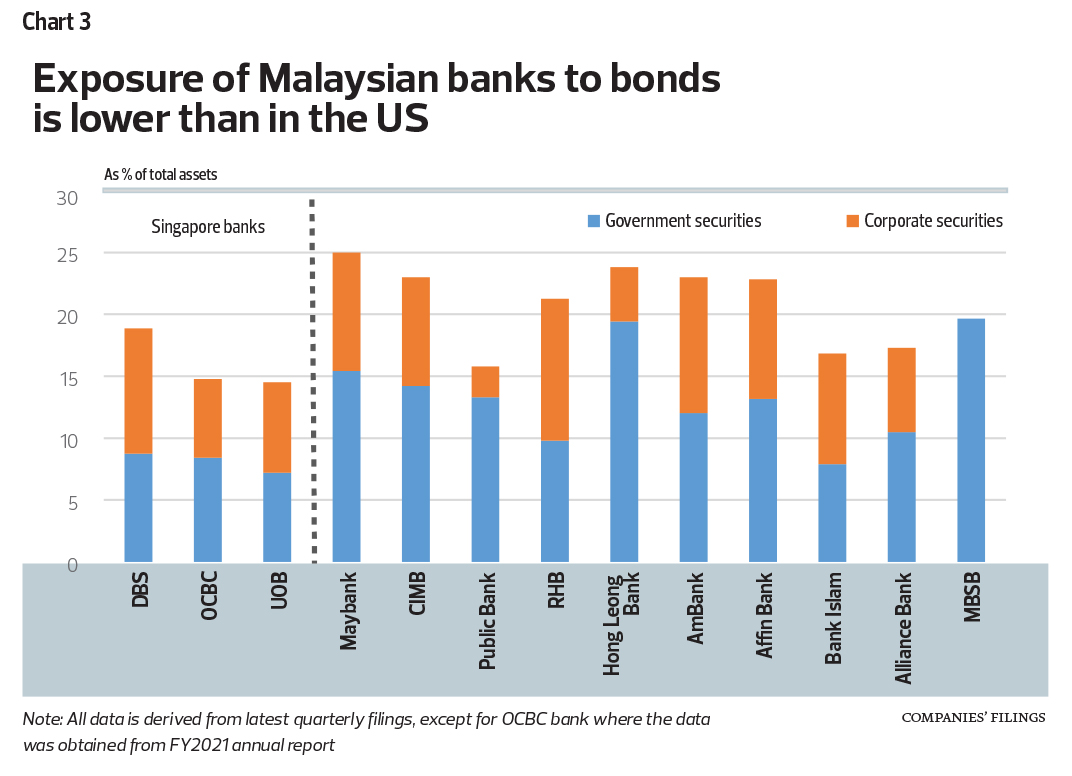

And while investments in government and corporate bonds also rose at the outset of the pandemic — as a result of excess deposits and lower loan demand — the increase was small, from 17.9% in January 2020 to a high of 19.7% of total assets in August 2021. Currently, the average bond holdings among Malaysian banks is 19.1% of total assets, or about RM645.2 billion, compared with 24% in the US banking system. Of note, 90% of the total are made up of local bonds — only 10% of which are foreign currency denominated bonds (see Chart 3).

Bank Negara’s tempered OPR hikes limit interest rate risks for banking system …

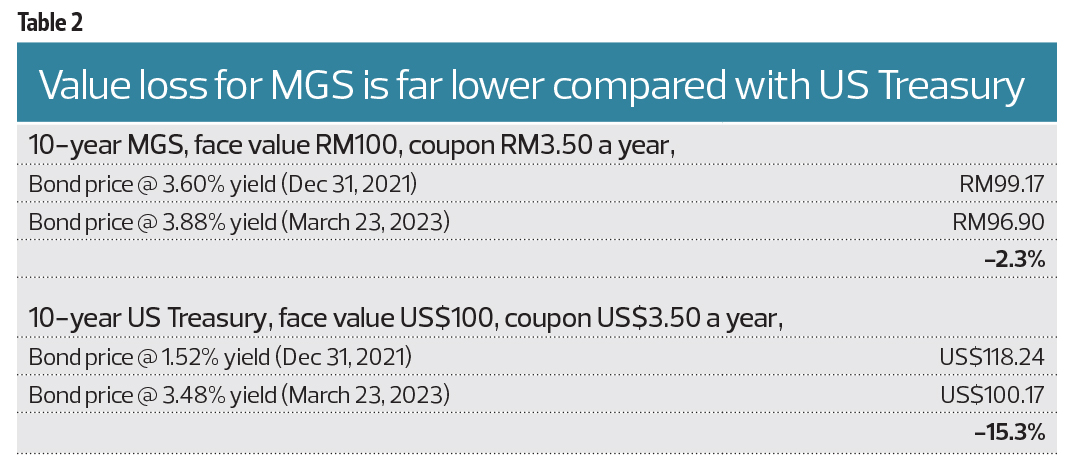

More importantly, Bank Negara Malaysia has raised the overnight policy rate (OPR) by only 1%, from 1.75% to 2.75% over the same period (compared with the 4.75% hike in the US FFR). Yields for the benchmark 10-year Malaysia Government Securities (MGS) have risen by even less — from 3.6% at the start of 2022 to 3.88% currently. The yield differential is less than 0.3%. This means the drop in value for 10-year MGS is only about 2.3%, based on our back-of-the-envelope calculations (see Table 2).

This is a huge difference compared to the 15.3% drop in value for the 10-year Treasury. Furthermore, unrealised losses for shorter duration bonds will be much lower. For instance, more than half of Maybank’s bond holdings have durations of less than five years.

In short, total unrealised losses for local banks should be much lower. (Incidentally, the majority of loans [79%] are based on floating interest rates, which are repriced immediately on Bank Negara’s policy rate changes.) Therefore, we think interest rate risks for the overall Malaysian banking system is low. Naturally, some banks will be affected more than others. For instance, Maybank, CIMB, Hong Leong Bank, Ambank, Affin Bank and RHB Bank have a higher percentage of bonds on their balance sheets compared with banks such as Public Bank, Bank Islam, Alliance Bank and MBSB. This could be due to a combination of factors, including deposit inflows, the ability to make loans and the target customer market.