Peter Lynch ran the Fidelity Magellan between 1977 and 1990. During this time he created the most enviable US mutual fund track record by averaging returns of 29% per year. To give you an idea of the compounding effect, he would have turned $10,000 into just over $270,000 in 13 years.

General Market observations

• The advance versus decline number paint better picture then the performance

of the market than index movements.

• Do not make comparisons between current market trends and other points in

history.

• For five years after July 1st 1994, $100,000 would have turned into $341,722.

If you missed the best 30 days, would have been worth $153,792.

• "The bearish argument always sounds more intelligent"

• Superior companies succeed and mediocre companies will fail. Investors in

each will be rewarded accordingly.

• Investing in stocks is an art not a science.

• If seven out of ten stocks perform, then I am delighted, if six out of ten stocks

perform, I am thankful. Six out of ten stocks is all it takes to create an enviable

record on Wall Street.

• Stand by your stocks as long as the fundamental story of the company has not

changed.

• There was a 16 month recession between July 81 and Nov 82. This time was

the scariest in memory. Sensible professionals wondered if they should take

up hunting and fishing, because soon we'd all be living in the woods, gathering

acorns. Unemployment was 14% and inflation was 15 %. A lot people said

they were expecting this but nobody mentioned it before the fact. Then

moment of greatest pessimism, when 8 out of 10 swore we where heading

into the 1930s the stock market rebounded with a vengeance and suddenly all

was right with the world.

• No matter how we arrive at the latest financial conclusions, we always prepare

ourselves for the last thing that happened.

• The day after the market crashed on Oct 19th 1987 people started worrying

that the market was going to crash.

• The great joke is that the next time is never like the last time.

• Not long ago people were worried that oil would drop to $5 and we would have

a depression. Two years later the same people were worried that oil would

rise to $100 and we would have a depression.

• When ten people would rather talk to a dentist about plaque then to a fund

manager about stocks, then it is likely the market is about to go up.

• “The stock market doesn't exist, it is there as a reference to see of anybody is

offering to do anything foolish” - Warren Buffett

• If you rely on the market to drag your stock along, then u might as well go to

Atlantic City and bet on red or black.

• Investing without research is like playing stud poker without looking at the

cards.

Categorising stocks

When you buy into stocks you need to understand why you are buying. In doing

this, it helps to categorise the company in determining what sort of returns you

can expect. Catergorising also enforces some discipline into your investment

process and aids effective portfolio construction. Peter Lynch uses the six

categories below

•

Sluggards (Slow growers) – Usually large companies in mature industries

with earnings growth below or around GDP growth. Such companies are

usually held for dividend rather than significant price appreciation.

•

Stalwarts (Medium growth) - High quality companies such as Coca-Cola,

P&G and Colgate that can still churn out high single digit/low teens growth.

Earnings patterns are not cyclical meaning that these stocks will protect

you recession.

•

Fast growers – Companies whose earnings are growing at 20%+ and have

plenty of runway to attack e.g. think Google, Apple in their early days. It

doesn’t have to be a company as “sexy” as those mentioned.

•

Cyclicals – Companies whose fortunes are closely linked to the economic

cycle e.g. automobiles, financials, airlines.

•

Turn-arounds – Companies coming out of a depressed phase as a result of

change in management, strategy or corporate restructuring. Successful

turnarounds can deliver stunning returns.

•

Asset plays – Firm has hidden assets which are undervalued or not

recognized at all on the balance sheet or under appreciated by the market

e.g. cash, land, property, holdings in other company.

General observations about different types of stocks

• Wall Street does not look kindly on fast growers that run out of stamina and

turn into slow growers and when that happens the stock is beaten down

accordingly.

Three phases of growth:

•

Start-up phase: during which it works out kinks in the business model.

•

Rapid expansion phase: moves into new locations and markets.

•

Mature phase: begins to prepare for the fact there's no easy to continue to

expand.

• Each of these phases may last several years. The first phase of the riskiest

for the investor, because the success of enterprise isn't yet established.

The second phase in safest, and also where the most money is made,

because the company is going to think about duplicating it's successful

formula. The third phase is when challenges arise, because of company

runs into its limitations. Other ways must be found to increase earnings.

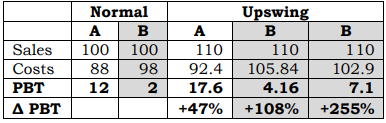

• You can lose more than 50 percent of your investment quickly if you buy

cyclicals in the wrong part of the cycle.

• You just have to be patient, keep up with the news and read it with dispassion.

• After it came out of bankruptcy, Penn Central had a huge tax loss to carry

forward which meant when it had to start earning money it wouldn't have to

pay taxes. It was reborn with a 50% tax advantage.

• It's impossible to say anything about the value of personal experience in

analysing companies and trends.

• Companies don't stay in the same category forever. Things change. Things

are always changing.

• It's simply impossible to find a generic formula that sensibly applies to all the

different kinds of stocks.

• Understand what you are expecting from the stock given its categorisation. Is

it the sort of stock you let run, or do you sell for a 30-50% gain.

• Ask if any idiot can run this joint, because at some point an idiot will run it.

• If you discover an opportunity early enough, you will probably get a few dollars

off its price for its dull name.

• A company that does boring things with a boring name is even better.

• High growth and hot industries attract a very smart crowd that want to get into

the business. That inevitably creates competition which means an exciting

story could quickly change.

• Try summarise the stock story in 2 minutes.

• Ask if the company is able to clone the idea.

• For companies that are meant to be depressed you will find surprises in one

out of ten of these could be a turnaround situation. So it always pays to look

beyond the headlines of depressing companies to find out if there is any thing

potentially good about the stock.

Financial analysis

• When cash is increasing relative to debt that is an improving balance sheet.

The other way around is a deteriorating balance sheet.

• When cash exceeds debt it's very favourable.

• Peter Lynch ignores short-term debt in his calculations. He assumes the

company that other assets can cover short term debt.

• With turnarounds and troubled companies, I pay special attention to debt.

Debt determines which companies survive and which will go bankrupt in a

crisis. Young companies with heavy debts are always a risk.

• Bank debt is the worst kind is due on demand.

• Commercial paper is loaned from one company to another for short periods of

time. It's due very soon and sometimes due on call. Creditors strip the

company and there is nothing left for shareholders.

• Funded debt is the best kind from a shareholders point of view. It can never be

called no matter how bleak the situation is.

• Pay attention to the debt structure as well as amount of debt when looking at

turnarounds. Work if the company has room for maneuver.

• Inventory - The closer you get to a finished product the less predictable the

resale value.

• Overvalued assets on the left of the balance sheet are especially treacherous

when there is a lot of debt on the right. Assets can easily fall in value whilst

debt is fixed.

• Keep a careful eye on inventories and think about what the value of

inventories should be. Finished goods are more likely to be subject to

markdowns then raw materials. In the car industry new cars are not prone to

severe markdowns compared to say the clothes industry.

• Looks for situations where there is high cash flow and low earnings. This may

happen because the company is depreciating a piece of old equipment which

doesn't need to be replaced in the immediate future.

The final checklist

• P/E ratio. Is it high for this particular company other similar companies in the

same industry?

• The percentage of institutional ownership. The lower the better.

• The record of earnings to date and whether the earnings are sporadic or

consistent. The only category where earnings may not be important is in the

asset play.

• Whether the company has a strong balance sheet or a weak balance sheet

and how it's rated for financial strength

When to Sell

Slow Grower

• I try sell when there's been a 30 to 50% appreciation or when the

fundamentals have deteriorated, even if the stock has declined in price.

• The company has lost market share for two consecutive years and is hiring

another advertising agency.

• No new products are being developed, spending research and development is

curtailed, and the company appears to be resting on its laurels.

Stalwart

• These are the stocks that I frequently replace for others in the category. There

is no point expecting a quick tenbagger in stalwarts and if the stock price get

above the earnings line, or if the P/E strays to far beyond on the normal range,

you might think about selling it and waiting to buy back later at a lower price or

buying something else as I do.

Cyclicals

• Extended run in upturn means a downturn could be nearing.

• One of the sell signal is inventories are building up in the company and can't

get rid of them, which means low prices and low profits down the road.

Fast grower

• If the company falls apart and the earnings shrink, and so will the P/E multiple

that investors have bid up on the stock. This is a very expensive double

whammy for the loyal shareholders.

• The main thing to watch for is the end of the second phase of rapid growth.

Turnaround

• The best time to sell a turnaround is after its turned - around. All troubles are

over and everybody knows it. The company has become the old self that was

before it fell apart: growth companies or cyclical or whatever. you have to do

reclassified stock.

Asset Play

• When the stock price has risen to the estimated value of the assets.

Silliest things people say about stocks

• If it's gone down this much already it can't go much lower

• You can always tell when a stocks hit bottom

• If it's gone this high already, how can it possibly go higher?

• It's only three dollars a share: what can I lose?

• Eventually they always come back

Things I have seen and general advice

• Most of the money I make is in the third of fourth-year that I've held the stock.

• In most cases it is better to buy the original good company at the high-priced

than it is to jump on the next “Apple or Microsoft” at a bargain price.

• Trying to predict the direction of the market over one year, or even two years,

is impossible.

• You can make serious money by compounding a series of 20 to 30% gains in

stalwarts.

• Just because the price goes up doesn't mean you are right.

• Just because the price goes down doesn't mean you're wrong.

• Stalwarts with heavy institutional ownership and lots of Wall Street covered

that outperform the market are due for arrest or a decline.

• Buying a company with mediocre prospects just because the stock is cheap is

a losing technique.

• Selling an outstanding fast-growing because the stock seems slightly

overpriced is a losing technique.

• Don't become so attached to a winner that complacency sets in and you stop

monitoring the story.

• By careful pruning and rotation based on fundamentals, you can improve your

results. If stocks are out of line with reality and better alternatives exist, sell

and switch into something else

• There is always something to worry about.

• Stick around to see what happens – as long as the original story continues

make sense, or gets better – and you'll be amazed at the result in several

years.

• One of the biggest troubles with stock-market advice is that good or bad it

sticks in your brain. You can't get it out of there, and someday, sometime, you

may find yourself reacting to it.

• I almost didn't buy La Quinta because in important insider had been selling

shares. Not buying because an insider have started selling can be as big a

mistake as selling because an outsider had stopped buying. In La Quinta's

case I ignored the nonsense, and I'm glad I did.

• You don't have to "kiss all the girls". I've missed my share of 10 baggers and

hasn't kept me from beating the market.

http://twitdoc.com/upload/funalysis/summary-of-one-up-on-wall-street-peter-lynch.pdf