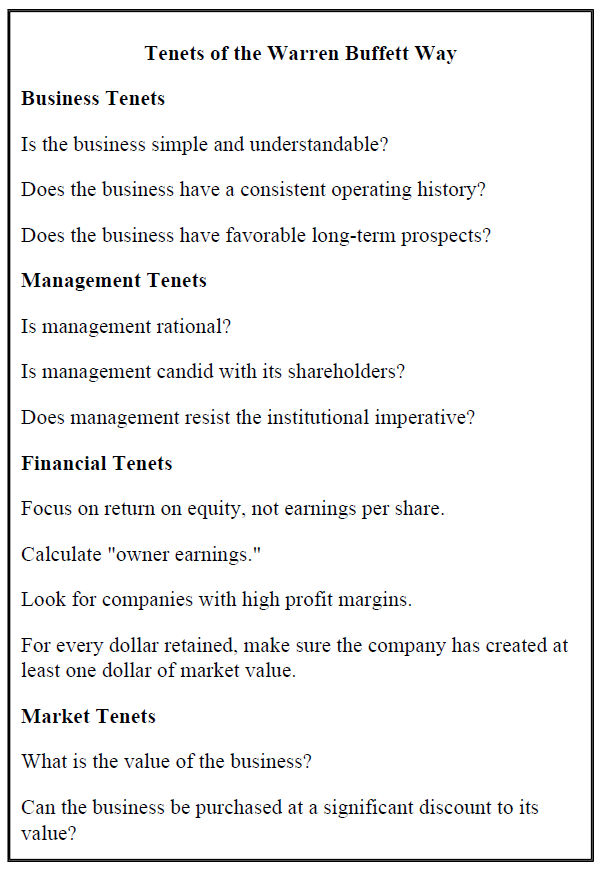

https://cdn5.oldschoolvalue.com/blog/wp-content/uploads/twbw1.png

http://klse.i3investor.com/blogs/oldschool_jaejun/128904.jsp

"I don't love Ben Graham and his ideas the way Warren does. You have to understand, to Warren - who discovered him at such a young age and then went to work for him - Ben Graham's insights changed his whole life, and he spent much of his early years worshiping the master at close range. But I have to say, Ben Graham had a lot to learn as an investor.

"I think Ben Graham wasn't nearly as good an investor as Warren Buffett is or even as good as I am. Buying those cheap, cigar-butt stocks was a snare and a delusion, and it would never work with the kinds of sums of money we have. You can't do it with billions of dollars or even many millions of dollars. But he was a very good writer and a very good teacher and a brilliant man, one of the only intellectuals - probably the only intellectual - in the investing business at the time." - Charlie Munger, The Wall Street Journal September 2014When he arrived at Berkshire, Munger actively tried to push Buffett away from deep value toward quality at a reasonable price, which he did with much success.

"Munger bought cigar butts, did arbitrage, even acquired small businesses. He said to Ed Anderson, 'I just like the great businesses.' He told Anderson to write up companies like Allergan ( AGN ), the contact-lens-solution maker. Anderson misunderstood and wrote a Grahamian report emphasizing the company's balance sheet. Munger dressed him down for it; he wanted to hear about the intangible qualities of Allergan: the strength of its management, the durability of its brand, what it would take for someone else to compete with it.

" Munger had invested in a Caterpillar ( CAT ) tractor dealership and saw how it gobbled up money, which sat in the yard in the form of slow-selling tractors. Munger wanted to own a business that did not require continual investment and spat out more cash than it consumed. Munger was always asking people, 'What's the best business you've ever heard of?'" - "The Snowball: Warren Buffett and the Business of Life" by Alice SchroederMunger understood that it's these businesses where big money is made as the high returns on capital, and a nonexistent need for capital investment ensures shareholders are well rewarded over the long term.

"We've really made the money out of high-quality businesses. In some cases, we bought the whole business. And in some cases, we just bought a big block of stock. But when you analyze what happened, the big money's been made in the high quality businesses. And most of the other people who've made a lot of money have done so in high quality businesses.

" Over the long term, it's hard for a stock to earn a much better return than the business which underlies it earns. If the business earns 6% on capital over 40 years and you hold it for that 40 years, you're not going to make much different than a 6% return -even if you originally buy it at a huge discount. Conversely, if a business earns 18% on capital over 20 or 30 years, even if you pay an expensive-looking price, you'll end up with a fine result.

" So the trick is getting into better businesses. And that involves all of these advantages of scale that you could consider momentum effects."Buffett added some meat to this statement at the 2003 Berkshire Hathaway meeting:

"The ideal business is one that generates very high returns on capital and can invest that capital back into the business at equally high rates. Imagine a $100 million business that earns 20% in one year, reinvests the $20 million profit and in the next year earns 20% of $120 million and so forth. But there are very very few businesses like this. Coke ( KO ) has high returns on capital, but incremental capital doesn't earn anything like its current returns. We love businesses that can earn high rates on even more capital than it earns. Most of our businesses generate lots of money but can't generate high returns on incremental capital - for example, See's and Buffalo News. We look for them [areas to wisely reinvest capital], but they don't exist."These quotes do a great job of summing up Munger and Buffett's investment strategy. Even though there are thousands of pages of investment commentary from both of these billionaires, their investment style can be summed up with the simple description of quality at a reasonable price, and the above quotes show exactly why they've both decided this style is best.