April 21, 2000 8:15 AM PDT

Patience-to-Earnings ratio wears thin for dot-coms

By Tiffany Kary

Staff Writer, CNET News

.With the Nasdaq well below its March 10 high of 5,048, investors are finally asking what the 'E' in the P/E, or price-to-earnings ratio, means.

Although profits suddenly mean something to dot-com investors, some analysts and executives maintain Net companies still need leeway to build out their businesses.

Do profits matter?

The profit tug-of-war will determine the direction of Net stocks for the foreseeable future, said investment experts. The tug-of-war is already underway -- shares of Excite@Home (Nasdaq: ATHM) fell Thursday after the company said it was foregoing near-term profits for long-term market share. The usually optimistic Merrill Lynch analyst Henry Blodget said he didn't 'see any positive catalysts for the stock.'

And in recent weeks, companies with no roadmap to earnings suffered the most (see chart). Shares of companies like CDNow (Nasdaq: CDNW), DrKoop.com (Nasdaq: KOOP) and Webvan (Nasdaq: WBVN) have been decimated.

As investors shun promising ideas for real results, dot-coms will have to generate cash instead of running back to the market for a quick-fix stock offering. To determine the long-term winners, investors will have to scrutinize business models and look for balance between growth and profitability.

Growth vs. profit

It's a fine line to walk between generating profits and growing. Excite@Home was panned by some analysts because it chose international expansion over immediate profits. The problem? Excite@Home has been profitable and has a track record. The market is more forgiving with promising newcomers.

'Companies that have been around for a while should have profits, but newcomers should be allowed time to build market share,' said Abhishek Gami, analyst for William Blair & Co.

Gami said he would allow business-to-consumer e-commerce companies about 12 to 18 months to become profitable. In the business-to-business space, a company should have as much as two to three years to turn a profit. In B2B, there are only a handful of competitors and a lot of market share to grab. With a portal, he wouldn't look at anything that didn't plan on earnings within 12 to 18 months.

About.com (Nasdaq: BOUT), which is far below its 52-week high of 105 13/16, is caught in the middle.

'Investors are looking at the total market, not individual companies,' said About.com CEO Scott Kurnit. 'They are looking at stock charts, and bringing the company down to at least 50 percent below its 52-week high, without regard for when the company reached its peak, or why.'

Kurnit is hoping a path to profits and strong third and fourth quarters will give About.com a boost. But his company is still in danger: Kurnit said About.com won’t be profitable for another 20 months.

The profit club

About.com is on the outside looking into a club that includes Yahoo! Inc. (Nasdaq: YHOO), eBay (Nasdaq: EBAY), America Online (NYSE: AOL), RealNetworks (Nasdaq: RNWK), Lycos (Nasdaq: LCOS) and Go2Net (Nasdaq: GNET). Inktomi (Nasdaq: INKT) and CNet (Nasdaq: CNET) are the latest members to the profitable dot-com club.

'The end game is, everyone will ask about profitability for every Net stock,' said Go2Net president John Keister. 'In 1997, people were talking about investing in earnings multiples for 2000, and now its 2002. People keep pushing it out.

'Smart investors, and institutional investors may not be satisfied with this anymore. Everyone has to trade on a multiple of earnings and revenue growth,' said Keister.

Leadership counts too

Leadership also counts for a lot. Chuck Hill, director of research at earnings tracking firm First Call, noted that profitable companies such as Yahoo, Go2Net, RealNetworks, AOL and Lycos have held up better than others, but said it doesn't have much to do with earnings. Hill said those companies are seen as industry leaders, which will survive. 'Even these companies are selling at multiples that are questionable,' he added.

'When a new company comes along, it's valued as a concept. Then there's a correction, and those that survive go on to be a good growth stock,' Hill said.

http://news.cnet.com/Patience-to-Earnings-ratio-wears-thin-for-dot-coms/2100-12_3-262272.html

Showing posts with label business valuations. Show all posts

Showing posts with label business valuations. Show all posts

Friday 13 November 2009

Valuation Methodologies

Despite their widespread usage, only limited theory is available to guide the application of multiples. With a few exceptions, the finance and accounting literature contain inadequate support on how or why certain multiples or comparable firms should be chosen in specific contexts. Compared to the DCF and RIV approach, standard textbooks on valuation devote little space to discussing the multiples valuation method.

Valuation Methodologies

This note provides an overview of the wide range of methodologies employed by Davy analysts when valuing shares.

One approach used is to apply average valuation multiples derived over multi-year periods, primarily with a view to smoothing cyclical effects.

Share-based multiples include:

Historic and forward price/earnings (P/E) ratios, based on normalised earnings before goodwill amortisation

Historic and forward price/cash-earnings (pre-depreciation) ratios

Price to net asset value per share

Dividend yields

Enterprise-based valuation multiples include:

Historic and forward earnings before depreciation, interest, tax, depreciation or amortisation (EBITDA) ratios; EBITDAR ratios are used where rental/lease charges (R) are material

Historic and forward EBITA ratios

Historic and forward operating cash-flow ratios

Enterprise value (EV)/sales ratios

EV/invested capital ratios

As enterprise values include net financial liabilities and minority interests, these are then deducted to arrive at the residual equity value.

Cyclical considerations

In the case of average earnings multiples, cognisance is given to the stage of the relevant industry cycle, as it may not be appropriate to apply average multiples towards the peak or trough of a cycle. In such cases, earnings multiples prevailing at the corresponding stages of previous cycles may be used.

Asset-based valuations

In the case of asset-based valuations, reported net assets generally provide a floor to a company's valuation. In many cases, however, company accounts can understate the underlying economic value of a company's assets, and a ratio such as return on invested capital to weighted average cost of capital (ROIC/WACC) may provide a more appropriate indicator of the book value multiple.

Company comparisons

The ratings of similar companies may be taken into account in valuing shares, as indeed may average ratings for particular industry sectors. Such ratings are commonly used in analysts' sum-of-the-parts (SOTP) valuations.

Cash-flow based valuation

In discounted cash-flow (DCF) models a company's forecast future free cash-flows are discounted by its weighted WACC. Due to the uncertainties involved in forecasting long-term cash-flows, analysts use a number of different DCF models.

Other valuation techniques

In some instances, other valuation metrics may be used. For instance, enterprise value per tonne of installed capacity may be used in capital-intensive sectors or in the earlier stages of a company's development.

http://www.davy.ie/Generic?page=valuationmethodologies

Valuation Methodologies

This note provides an overview of the wide range of methodologies employed by Davy analysts when valuing shares.

One approach used is to apply average valuation multiples derived over multi-year periods, primarily with a view to smoothing cyclical effects.

Share-based multiples include:

Historic and forward price/earnings (P/E) ratios, based on normalised earnings before goodwill amortisation

Historic and forward price/cash-earnings (pre-depreciation) ratios

Price to net asset value per share

Dividend yields

Enterprise-based valuation multiples include:

Historic and forward earnings before depreciation, interest, tax, depreciation or amortisation (EBITDA) ratios; EBITDAR ratios are used where rental/lease charges (R) are material

Historic and forward EBITA ratios

Historic and forward operating cash-flow ratios

Enterprise value (EV)/sales ratios

EV/invested capital ratios

As enterprise values include net financial liabilities and minority interests, these are then deducted to arrive at the residual equity value.

Cyclical considerations

In the case of average earnings multiples, cognisance is given to the stage of the relevant industry cycle, as it may not be appropriate to apply average multiples towards the peak or trough of a cycle. In such cases, earnings multiples prevailing at the corresponding stages of previous cycles may be used.

Asset-based valuations

In the case of asset-based valuations, reported net assets generally provide a floor to a company's valuation. In many cases, however, company accounts can understate the underlying economic value of a company's assets, and a ratio such as return on invested capital to weighted average cost of capital (ROIC/WACC) may provide a more appropriate indicator of the book value multiple.

Company comparisons

The ratings of similar companies may be taken into account in valuing shares, as indeed may average ratings for particular industry sectors. Such ratings are commonly used in analysts' sum-of-the-parts (SOTP) valuations.

Cash-flow based valuation

In discounted cash-flow (DCF) models a company's forecast future free cash-flows are discounted by its weighted WACC. Due to the uncertainties involved in forecasting long-term cash-flows, analysts use a number of different DCF models.

Other valuation techniques

In some instances, other valuation metrics may be used. For instance, enterprise value per tonne of installed capacity may be used in capital-intensive sectors or in the earlier stages of a company's development.

http://www.davy.ie/Generic?page=valuationmethodologies

Demystifying Small Business Valuation

Demystifying Small Business Valuation

Valuing a business is based on return on your investment (ROI). The value of a Business for Sale does not need to be subjective and can be based on several attributes and industry best practices.

Approach to Business Valuation

Valuing businesses is of paramount importance to a small business. It is one of the several metrics used to ensure the business is growing and creating value for the owners. There are several approaches to valuing a business including:

• Revenue Multiples

Earnings Multiples (including EBITA and operating income)

• Multiple of Book Value

Multiple of a measured unit (Like Restaurant tables, hospital beds, subscribers and more)

Rules of thumb are used by business brokers to ascertain the price of a business and simplify the valuation process. However, one must be mindful that the values determined using “Rule of thumb” are simplifications and only an estimate of the true value of the business. The “Rule of thumb” approach is used as a staring point before conducting detailed due-diligence to ascertain the correct value. Some examples of “Rules of thumb” used in the industry are listed in Table 1 below:

Table 1: Rules of Thumb Valuation

Type of Business “Rule of Thumb” valuation

Book Stores 15% of annual sales + inventory

Coffee Shops 40% - 45% of annual sales + inventory

Food/Gourmet Shops 20% of annual sales + inventory

Gas Stations 15% - 25% of annual sales + equip/inventory

Restaurants (non-franchised) 30% - 45% of annual sales

Dry Cleaners 70% - 100% of annual sales

A common approach to valuing a business is to use earnings or sales multiples. In this case since the price it is derived from annual earnings or sales and it directly addresses a buyer’s motive of estimating the return on investment (ROI) on deals.

When using earnings multipliers, it is inappropriate to get the multiples from Real Estate or Stock Markets. Real Estate is historically priced at 8 to 10 times its net operating income (EBITA). Stock markets are typically priced at 12 to 20 times earnings. These multiples do not apply to small businesses as the risk premium associated with a small business is much higher than managing a building or a stock portfolio.

Therefore, the first step in using the earnings multiplier approach is to determine which earnings multiplier is to be used. For example, one could use the current earnings, next year’s earnings or last 5 years earnings averaged. Other factors to consider include determining the composition of earnings. Do we need to calculate earnings after owner’s pay and perks, interest expenses, depreciation and taxes? The preferred earnings to use are 'Earnings before Interest and Taxes’ (EBIT).

Normalized earnings are adjusted for cyclical ups and downs in the economy. They are also adjusted for unusual or one-time influences. For small businesses normalized earnings projections are quite useful.

Finally we need to determine the multiplier. The number picked for multiplier is based on risk and there usually are “Rules of Thumb” multiplier numbers depending on the industry.

Using a multiplier with annual sales is also a common approach. For example, the “Rule of thumb” for a coffee shop is 40% - 45% of annual sales + inventory.

Tangible and Intangible assets

A tangible asset is an asset that has a physical form such as land, buildings and machinery. Intangible assets are the opposite of tangible assets. Intangible assets include patents, trademarks, brand value etc. Tangible and intangible assets raise interesting questions when valuing a business.

Typically once the value of the business itself has been ascertained, we need to factor in a value for Tangible and Intangible assets. These assets usually have a value separate from the business. One way to determine if an asset should be included as a tangible/intangible asset or included in the price for the business is to determine if the asset was used to generate the projected earnings. If the asset was used to generate earnings it should be included as a part of the multiple derived price of the business.

Factoring in tangible assets separately is especially true for businesses that own land and buildings, as these assets can be sold in the market even if the business failed. Therefore the best way to treat tangible/intangible asset is to separate them from the business and then add them back to the multiple derived value of the business. Obviously during the valuation period, asserts should not be counted twice. For example if the building has been factored out as a tangible and intangible asset, then rent for the premises must be subtracted from the business earnings. Similarly inventory impacts the business value. Typically inventory is valued at cost and treated as a tangible asset.

Earnings Multiples

After the value of tangible and intangible assets is determined we need to determine the value of the business using the correct multiples. Multiples used are very specific to a business and location of the business but broadly speaking it can be between 2 to 5 times normalized EBIT (Earnings before Interest and Taxes). The business can be worth more if it is has distinctive attributes that make it very attractive. To the buyer, 2 to 5 times earnings represent getting back their investment in the business in 2 to 5 years from profits a projected annual return of 20% to 50%.

Eventually the right multiple is the amount the buyer is willing to pay for the business. A business can demand higher multiples by clearly defining a case to increase earnings over time.

Disadvantages and caveats

Based on the content covered earlier, you may wonder how one can be certain the business valuation is perfect for the business buyer and seller. In reality there is no perfect price and techniques described in the earlier sections are just guidelines to derive an acceptable price.

The multiplier approach discussed does not provide sufficient information to assess the uniqueness of the business, such as management depth, customer relationships, industry trends, reputation, location, competition, capital structure and other information unique to the business. Further, two businesses of the same type and same revenue can have different cash flows.

The rules for evaluating a business are more of guidance then a hard and fast rule. They should be thought of as a starting point which can be further refined by factors specifically impacting the business. Proper evaluation will go beyond calculations based on multiples and tangible/intangible asset values. It requires complete business, marketing and financial due-diligence. However the approach describes in this article can play a key role in determining a starting value of your business.

Sites such as http://www.buysellbusiness.org allow entrepreneurs to do deals by buying and selling businesses and partnering. When researching businesses for deals, these guidelines can play an important role in quickly calculating the intrinsic value of a business.

http://www.buysellbusiness.org/BusinessTools/BizValuations.aspx

Valuing a business is based on return on your investment (ROI). The value of a Business for Sale does not need to be subjective and can be based on several attributes and industry best practices.

Approach to Business Valuation

Valuing businesses is of paramount importance to a small business. It is one of the several metrics used to ensure the business is growing and creating value for the owners. There are several approaches to valuing a business including:

• Revenue Multiples

Earnings Multiples (including EBITA and operating income)

• Multiple of Book Value

Multiple of a measured unit (Like Restaurant tables, hospital beds, subscribers and more)

Rules of thumb are used by business brokers to ascertain the price of a business and simplify the valuation process. However, one must be mindful that the values determined using “Rule of thumb” are simplifications and only an estimate of the true value of the business. The “Rule of thumb” approach is used as a staring point before conducting detailed due-diligence to ascertain the correct value. Some examples of “Rules of thumb” used in the industry are listed in Table 1 below:

Table 1: Rules of Thumb Valuation

Type of Business “Rule of Thumb” valuation

Book Stores 15% of annual sales + inventory

Coffee Shops 40% - 45% of annual sales + inventory

Food/Gourmet Shops 20% of annual sales + inventory

Gas Stations 15% - 25% of annual sales + equip/inventory

Restaurants (non-franchised) 30% - 45% of annual sales

Dry Cleaners 70% - 100% of annual sales

A common approach to valuing a business is to use earnings or sales multiples. In this case since the price it is derived from annual earnings or sales and it directly addresses a buyer’s motive of estimating the return on investment (ROI) on deals.

When using earnings multipliers, it is inappropriate to get the multiples from Real Estate or Stock Markets. Real Estate is historically priced at 8 to 10 times its net operating income (EBITA). Stock markets are typically priced at 12 to 20 times earnings. These multiples do not apply to small businesses as the risk premium associated with a small business is much higher than managing a building or a stock portfolio.

Therefore, the first step in using the earnings multiplier approach is to determine which earnings multiplier is to be used. For example, one could use the current earnings, next year’s earnings or last 5 years earnings averaged. Other factors to consider include determining the composition of earnings. Do we need to calculate earnings after owner’s pay and perks, interest expenses, depreciation and taxes? The preferred earnings to use are 'Earnings before Interest and Taxes’ (EBIT).

Normalized earnings are adjusted for cyclical ups and downs in the economy. They are also adjusted for unusual or one-time influences. For small businesses normalized earnings projections are quite useful.

Finally we need to determine the multiplier. The number picked for multiplier is based on risk and there usually are “Rules of Thumb” multiplier numbers depending on the industry.

Using a multiplier with annual sales is also a common approach. For example, the “Rule of thumb” for a coffee shop is 40% - 45% of annual sales + inventory.

Tangible and Intangible assets

A tangible asset is an asset that has a physical form such as land, buildings and machinery. Intangible assets are the opposite of tangible assets. Intangible assets include patents, trademarks, brand value etc. Tangible and intangible assets raise interesting questions when valuing a business.

Typically once the value of the business itself has been ascertained, we need to factor in a value for Tangible and Intangible assets. These assets usually have a value separate from the business. One way to determine if an asset should be included as a tangible/intangible asset or included in the price for the business is to determine if the asset was used to generate the projected earnings. If the asset was used to generate earnings it should be included as a part of the multiple derived price of the business.

Factoring in tangible assets separately is especially true for businesses that own land and buildings, as these assets can be sold in the market even if the business failed. Therefore the best way to treat tangible/intangible asset is to separate them from the business and then add them back to the multiple derived value of the business. Obviously during the valuation period, asserts should not be counted twice. For example if the building has been factored out as a tangible and intangible asset, then rent for the premises must be subtracted from the business earnings. Similarly inventory impacts the business value. Typically inventory is valued at cost and treated as a tangible asset.

Earnings Multiples

After the value of tangible and intangible assets is determined we need to determine the value of the business using the correct multiples. Multiples used are very specific to a business and location of the business but broadly speaking it can be between 2 to 5 times normalized EBIT (Earnings before Interest and Taxes). The business can be worth more if it is has distinctive attributes that make it very attractive. To the buyer, 2 to 5 times earnings represent getting back their investment in the business in 2 to 5 years from profits a projected annual return of 20% to 50%.

Eventually the right multiple is the amount the buyer is willing to pay for the business. A business can demand higher multiples by clearly defining a case to increase earnings over time.

Disadvantages and caveats

Based on the content covered earlier, you may wonder how one can be certain the business valuation is perfect for the business buyer and seller. In reality there is no perfect price and techniques described in the earlier sections are just guidelines to derive an acceptable price.

The multiplier approach discussed does not provide sufficient information to assess the uniqueness of the business, such as management depth, customer relationships, industry trends, reputation, location, competition, capital structure and other information unique to the business. Further, two businesses of the same type and same revenue can have different cash flows.

The rules for evaluating a business are more of guidance then a hard and fast rule. They should be thought of as a starting point which can be further refined by factors specifically impacting the business. Proper evaluation will go beyond calculations based on multiples and tangible/intangible asset values. It requires complete business, marketing and financial due-diligence. However the approach describes in this article can play a key role in determining a starting value of your business.

Sites such as http://www.buysellbusiness.org allow entrepreneurs to do deals by buying and selling businesses and partnering. When researching businesses for deals, these guidelines can play an important role in quickly calculating the intrinsic value of a business.

http://www.buysellbusiness.org/BusinessTools/BizValuations.aspx

Valuation: What's it worth?

What's it worth?

Although there are several formulas you can use, there are no black-and-white answers on valuation techniques.

It’s important to conduct your own research, then get independent advice from a business valuer or broker. Here are four of the most commonly used valuation methods.

Method 1: Asset valuation

Method 2: Capitalised future earnings

Method 3: Earnings multiple

Method 4: Comparable sales

Method 1: Asset valuation

This approach determines the value of a business by adding up the value of its assets and subtracting liabilities. It tells you what the business would be worth if it were closed down today and its assets sold off, but it doesn’t take into account the ability of those assets to generate revenue in the future. For that reason, it may understate the true value of the business.

How it works

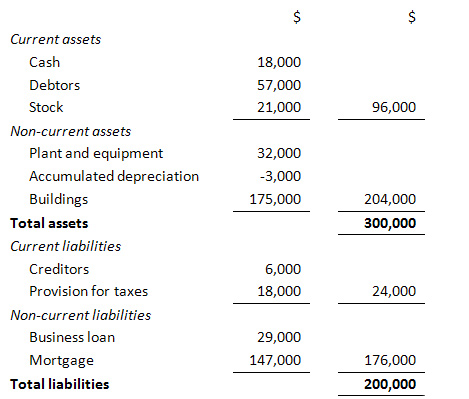

1.Add up the value of all the assets such as cash, stock, plant and equipment and receivables.

2.Add up liabilities, such as any bank debts and payments due.

3.Subtract the business’ liabilities from its assets to get the net asset value.

Example

Richard wants to buy a manufacturing business. Here’s an extract from the business’ balance sheet.

With assets of $300,000 and liabilities of $200,000, the net asset value of the business is $100,000.

What about goodwill?

This method doesn’t include a value for goodwill or the right to earn future profits, so it may understate the true value of a business. Goodwill is the difference between the true value of a business and the value of its net assets. It can be crucial to the value of retail and service-based businesses.

For example, when you are valuing a business such as a hairdressing salon, where the standard of service, location and reputation are important, the value of any goodwill would have to be added to net assets to get a valuation.

You need to consider whether goodwill can be transferred when you buy the business. While goodwill can come from physical features such as location, it can also arise from personal factors, such as the owner’s reputation or their relationships with customers or suppliers, which may not be transferable.

And if the business is underperforming and there is no goodwill attached to it, then using the net assets valuation method could be an accurate way of determining its value.

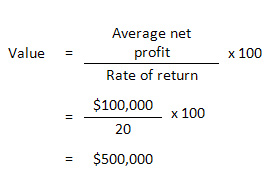

Method 2: Capitalised future earnings

When you buy a business, you’re not only buying its assets. You’re also buying the right to all of the profits that business might generate. Different valuation methods try to capture that.

Capitalising future earnings is the most common method used to value small businesses. The method looks at the rate of return on investment (ROI) that you can expect to get from the business.

How it works

1.Work out the average net profit of the business over the last three years using its profit-and-loss statements. You’ll need to adjust the profit for any one-off expenses or other irregular items each year.

2.Decide the annual rate of return that you’re looking for as a business owner (for example, 20%). There are no hard and fast rules about what number you should choose, except that the higher the risk, the higher your return should be. A good starting point is to compare the business with other investment opportunities — everything from safe havens like term deposits, to riskier investments like shares. You can also look at the rate of return that similar businesses in the same industry achieve.

3.Divide net profits by the rate of return to determine the value of the business, then multiply by 100.

Example

David is looking at buying a bakery business with average net profits of $100,000 per annum after adjustments. David wants an annual rate of return of 20%. The capitalised earnings valuation is:

Method 3: Earnings multiple

If you invest in shares, you might already be familiar with this method, since it’s often used to assess the value of companies whose shares are traded on a stock exchange and therefore reflect market expectations. But it can be used to value unlisted businesses.

Its big advantage is its simplicity. The difficulty lies in deciding which multiple to use.

How it works

Simply multiply the business’ earnings before interest and tax (EBIT) by your selected multiple. For example, you might value the business at twice its annual earnings — so a business with an EBIT of $200,000 might be valued at $400,000.

The multiple you choose will depend on the industry and the growth potential of the business. A service-based business might be valued at as little as one year’s earnings, while an established business with sustainable profits might sell for as much as six times earnings. (Listed companies trade at much higher multiples, because their size and liquidity makes them less risky investments.)

This method can be useful for valuing a business where there are regular sales of similar businesses to help you determine an objective earnings multiple. A business broker should be able to tell you this.

Method 4: Comparable sales

Whatever other valuation method you use, you should also look at prices for recent sales of similar businesses. Like buying a house, it makes sense to know what is happening in the market in which you’re interested.

Speak to a few business brokers and gauge their feeling about the business’ value. They might know what similar operations are selling for and how the market is placed at that particular time. Check business-for-sale listings in relevant industry magazines, newspapers or websites.

Tools and templates

Buying a business checklist

Important information

As this advice has been prepared without considering your objectives, financial situation or needs, you should, before acting on the advice, consider its appropriateness to your circumstances. All products mentioned on this web page are issued by the Commonwealth Bank of Australia; view our Financial Services Guide (PDF 59kb).

http://www.commbank.com.au/business/betterbusiness/buying-a-business/whats-it-worth/

Although there are several formulas you can use, there are no black-and-white answers on valuation techniques.

It’s important to conduct your own research, then get independent advice from a business valuer or broker. Here are four of the most commonly used valuation methods.

Method 1: Asset valuation

Method 2: Capitalised future earnings

Method 3: Earnings multiple

Method 4: Comparable sales

Method 1: Asset valuation

This approach determines the value of a business by adding up the value of its assets and subtracting liabilities. It tells you what the business would be worth if it were closed down today and its assets sold off, but it doesn’t take into account the ability of those assets to generate revenue in the future. For that reason, it may understate the true value of the business.

How it works

1.Add up the value of all the assets such as cash, stock, plant and equipment and receivables.

2.Add up liabilities, such as any bank debts and payments due.

3.Subtract the business’ liabilities from its assets to get the net asset value.

Example

Richard wants to buy a manufacturing business. Here’s an extract from the business’ balance sheet.

With assets of $300,000 and liabilities of $200,000, the net asset value of the business is $100,000.

What about goodwill?

This method doesn’t include a value for goodwill or the right to earn future profits, so it may understate the true value of a business. Goodwill is the difference between the true value of a business and the value of its net assets. It can be crucial to the value of retail and service-based businesses.

For example, when you are valuing a business such as a hairdressing salon, where the standard of service, location and reputation are important, the value of any goodwill would have to be added to net assets to get a valuation.

You need to consider whether goodwill can be transferred when you buy the business. While goodwill can come from physical features such as location, it can also arise from personal factors, such as the owner’s reputation or their relationships with customers or suppliers, which may not be transferable.

And if the business is underperforming and there is no goodwill attached to it, then using the net assets valuation method could be an accurate way of determining its value.

Method 2: Capitalised future earnings

When you buy a business, you’re not only buying its assets. You’re also buying the right to all of the profits that business might generate. Different valuation methods try to capture that.

Capitalising future earnings is the most common method used to value small businesses. The method looks at the rate of return on investment (ROI) that you can expect to get from the business.

How it works

1.Work out the average net profit of the business over the last three years using its profit-and-loss statements. You’ll need to adjust the profit for any one-off expenses or other irregular items each year.

2.Decide the annual rate of return that you’re looking for as a business owner (for example, 20%). There are no hard and fast rules about what number you should choose, except that the higher the risk, the higher your return should be. A good starting point is to compare the business with other investment opportunities — everything from safe havens like term deposits, to riskier investments like shares. You can also look at the rate of return that similar businesses in the same industry achieve.

3.Divide net profits by the rate of return to determine the value of the business, then multiply by 100.

Example

David is looking at buying a bakery business with average net profits of $100,000 per annum after adjustments. David wants an annual rate of return of 20%. The capitalised earnings valuation is:

Method 3: Earnings multiple

If you invest in shares, you might already be familiar with this method, since it’s often used to assess the value of companies whose shares are traded on a stock exchange and therefore reflect market expectations. But it can be used to value unlisted businesses.

Its big advantage is its simplicity. The difficulty lies in deciding which multiple to use.

How it works

Simply multiply the business’ earnings before interest and tax (EBIT) by your selected multiple. For example, you might value the business at twice its annual earnings — so a business with an EBIT of $200,000 might be valued at $400,000.

The multiple you choose will depend on the industry and the growth potential of the business. A service-based business might be valued at as little as one year’s earnings, while an established business with sustainable profits might sell for as much as six times earnings. (Listed companies trade at much higher multiples, because their size and liquidity makes them less risky investments.)

This method can be useful for valuing a business where there are regular sales of similar businesses to help you determine an objective earnings multiple. A business broker should be able to tell you this.

Method 4: Comparable sales

Whatever other valuation method you use, you should also look at prices for recent sales of similar businesses. Like buying a house, it makes sense to know what is happening in the market in which you’re interested.

Speak to a few business brokers and gauge their feeling about the business’ value. They might know what similar operations are selling for and how the market is placed at that particular time. Check business-for-sale listings in relevant industry magazines, newspapers or websites.

Tools and templates

Buying a business checklist

Important information

As this advice has been prepared without considering your objectives, financial situation or needs, you should, before acting on the advice, consider its appropriateness to your circumstances. All products mentioned on this web page are issued by the Commonwealth Bank of Australia; view our Financial Services Guide (PDF 59kb).

http://www.commbank.com.au/business/betterbusiness/buying-a-business/whats-it-worth/

Thursday 12 November 2009

How is a P/E multiple used?

The Price/Earnings Multiple Enigma

If the Price to Earnings Multiple (P/E) were to be judged by usage, it wins hands down compared to any other valuation metric. It is easy to compute, can be applied across companies and across sectors, with a few exceptions. What is this ratio, how is it computed, and how to use it are questions to which you will find answers in this section.

What is a P/E multiple?

The P/E multiple is the premium that the market is willing to pay on the earnings per share of a company, based on its future growth. The ratio is most often used to conclude whether a stock is undervalued or overvalued. The P/E is calculated by dividing the current market price of a company's stock by the last reported full-year earnings per share (EPS). In effect, the ratio uses the company's earnings as a guide to value it. The P/E thus computed is also known as the trailing or historical P/E since it uses the trailing (historical) EPS in its calculations. With the advent of quarterly results, it is also possible to compute P/E, based on the earnings of the latest four quarters’ EPS. This is known as trailing twelve months P/E.

A variant of the P/E - called the forward P/E - has also been developed wherein the current market price of the stock is divided by the expected future EPS. The attempt to study P/E ratios in this manner reflects the effort to factor in the expected growth of a company.

Since stock market valuations factor in the future expectations of the market, a P/E multiple computed using historical earnings can at best be of academic value since it does not factor in the future growth in earnings. It fails to capture events that may have happened after the earnings date. For example, suppose a merger happens after the earnings have been declared, a P/E multiple based on the historical P/E will fail to capture this event in the EPS whereas the price would reflect it, creating a distortion.

The forward P/E is popularly used to find out if the premium the market is willing to pay on the earnings is line with the growth expectations. For example, the market price of Stock A is Rs 1,000, with a P/E multiple of 30 based on historical earnings. Assuming an earnings growth of 50%, the one year forward P/E changes to 20, which means the market is willing to pay 30 times its historical earnings and 20 times its one-year forward earnings.

For an investor it makes much more sense to look at the forward P/E for taking an investment decision. Each investor would have his or her own expectations regarding the future earnings growth. To that extent the forward P/E for a particular stock will vary from investor to investor.

How is a P/E multiple used?

P/E multiples reflect collective investor perception regarding a company's future. This perception is a function of various factors, like industry growth prospects, company’s position in industry, its growth plans, quantum change expected in sales or profit growth, quality of management, and other macroeconomic factors like interest rates and inflation.

Is a stock trading at a P/E of 30 more expensive than a stock trading at a P/E of 60? Such a wide variation in P/E multiples can be owing to a few reasons. If the companies are in the same industry, it could be that the company with a high P/E may be one with superior size and financials, with better prospects or even better management. The market expects this stock to outperform its peers. If they are from different industries, it could also be due to different growth prospects. For example, an energy utility will have a more sedate earnings profile than say a software company.

Besides different expectations regarding future earnings growth, some of the difference in P/E can also be attributed to the disclosures made by the management to their shareholders. Hence, qualitative factors like transparency, quality of management also impact a stock's P/E.

Stock prices, in isolation do not give any indication whether the stock is undervalued or overvalued. They have to be viewed along with the company's future prospects to arrive at any conclusion. Generally, higher the expected growth in a company's earnings, higher is the P/E multiple that it attracts in the market. The time period used for P/E calculations depends on the investment horizon of the investor and would be different for each investor. However, P/E multiples cannot be applied to loss making companies since they do not have any earnings.

Price to Earnings Growth Multiple (PEG)

The PEG multiple takes the P/E analysis to the next stage. Since P/E ratios are computed based on historic earnings, they project an inaccurate picture of the future. The PEG multiple uses expected growth in earnings, to give investors additional information. The PEG divides the historical P/E ratio by the compounded annual growth rate of future earnings. Generally, the compounded earnings growth is calculated using the forecasted earnings for the next two-three years.

For example, if a company is quoting at a P/E of 60 based on historic earnings and the compounded annual growth rate of its earnings for the next three years is 20 per cent, then its PEG is 3.

The lower the PEG, the more attractive the stock becomes as an investment proposition. It is obviously more appealing to buy a stock on a P/E of 20 whose earnings are growing at 50 per cent than to buy a stock on a multiple of 50 whose earnings are growing at 20 per cent. As a thumb rule, stocks quoting at a PEG multiple below 0.5 are considered to be undervalued, 1 to be fairly valued, and 2 to be overvalued.

http://www.hdfcsec.com/KnowledgeCenter/Story.aspx?ArticleID=8153321b-8faa-4429-abba-bbfe5f29e77d

If the Price to Earnings Multiple (P/E) were to be judged by usage, it wins hands down compared to any other valuation metric. It is easy to compute, can be applied across companies and across sectors, with a few exceptions. What is this ratio, how is it computed, and how to use it are questions to which you will find answers in this section.

What is a P/E multiple?

The P/E multiple is the premium that the market is willing to pay on the earnings per share of a company, based on its future growth. The ratio is most often used to conclude whether a stock is undervalued or overvalued. The P/E is calculated by dividing the current market price of a company's stock by the last reported full-year earnings per share (EPS). In effect, the ratio uses the company's earnings as a guide to value it. The P/E thus computed is also known as the trailing or historical P/E since it uses the trailing (historical) EPS in its calculations. With the advent of quarterly results, it is also possible to compute P/E, based on the earnings of the latest four quarters’ EPS. This is known as trailing twelve months P/E.

A variant of the P/E - called the forward P/E - has also been developed wherein the current market price of the stock is divided by the expected future EPS. The attempt to study P/E ratios in this manner reflects the effort to factor in the expected growth of a company.

Since stock market valuations factor in the future expectations of the market, a P/E multiple computed using historical earnings can at best be of academic value since it does not factor in the future growth in earnings. It fails to capture events that may have happened after the earnings date. For example, suppose a merger happens after the earnings have been declared, a P/E multiple based on the historical P/E will fail to capture this event in the EPS whereas the price would reflect it, creating a distortion.

The forward P/E is popularly used to find out if the premium the market is willing to pay on the earnings is line with the growth expectations. For example, the market price of Stock A is Rs 1,000, with a P/E multiple of 30 based on historical earnings. Assuming an earnings growth of 50%, the one year forward P/E changes to 20, which means the market is willing to pay 30 times its historical earnings and 20 times its one-year forward earnings.

For an investor it makes much more sense to look at the forward P/E for taking an investment decision. Each investor would have his or her own expectations regarding the future earnings growth. To that extent the forward P/E for a particular stock will vary from investor to investor.

How is a P/E multiple used?

P/E multiples reflect collective investor perception regarding a company's future. This perception is a function of various factors, like industry growth prospects, company’s position in industry, its growth plans, quantum change expected in sales or profit growth, quality of management, and other macroeconomic factors like interest rates and inflation.

Is a stock trading at a P/E of 30 more expensive than a stock trading at a P/E of 60? Such a wide variation in P/E multiples can be owing to a few reasons. If the companies are in the same industry, it could be that the company with a high P/E may be one with superior size and financials, with better prospects or even better management. The market expects this stock to outperform its peers. If they are from different industries, it could also be due to different growth prospects. For example, an energy utility will have a more sedate earnings profile than say a software company.

Besides different expectations regarding future earnings growth, some of the difference in P/E can also be attributed to the disclosures made by the management to their shareholders. Hence, qualitative factors like transparency, quality of management also impact a stock's P/E.

Stock prices, in isolation do not give any indication whether the stock is undervalued or overvalued. They have to be viewed along with the company's future prospects to arrive at any conclusion. Generally, higher the expected growth in a company's earnings, higher is the P/E multiple that it attracts in the market. The time period used for P/E calculations depends on the investment horizon of the investor and would be different for each investor. However, P/E multiples cannot be applied to loss making companies since they do not have any earnings.

Price to Earnings Growth Multiple (PEG)

The PEG multiple takes the P/E analysis to the next stage. Since P/E ratios are computed based on historic earnings, they project an inaccurate picture of the future. The PEG multiple uses expected growth in earnings, to give investors additional information. The PEG divides the historical P/E ratio by the compounded annual growth rate of future earnings. Generally, the compounded earnings growth is calculated using the forecasted earnings for the next two-three years.

For example, if a company is quoting at a P/E of 60 based on historic earnings and the compounded annual growth rate of its earnings for the next three years is 20 per cent, then its PEG is 3.

The lower the PEG, the more attractive the stock becomes as an investment proposition. It is obviously more appealing to buy a stock on a P/E of 20 whose earnings are growing at 50 per cent than to buy a stock on a multiple of 50 whose earnings are growing at 20 per cent. As a thumb rule, stocks quoting at a PEG multiple below 0.5 are considered to be undervalued, 1 to be fairly valued, and 2 to be overvalued.

http://www.hdfcsec.com/KnowledgeCenter/Story.aspx?ArticleID=8153321b-8faa-4429-abba-bbfe5f29e77d

Business valuation with price earnings multiples

Business valuation with price earnings multiples

Tuesday, 12 December 2006 02:45 Anton Joseph

E-mail | Print | Tags: valuation | business sale/purchase | ip revenue | strategy

When it comes to selling or buying a business the sale price is the greatest obstacle and point of disagreement in many transactions. If there is a reasonable and easily understandable way of determining the value of the business the parties can quickly progress more than half way through the sale process. Although it is said that the right tools must be used to value businesses, no simple method suits all types of businesses. Instead, there are several financial and non-financial performance indicators that are commonly used by businesses to monitor their progress. Some are used to measure profitability whilst others are used to test liquidity.

Financial indicators are normally measured by using ratios calculated using numerical values appearing in the profit and loss account or the balance sheet. Since the indicators are snapshot calculations based on historical figures (figures for the past year), there is an understandable reluctance to always rely on them. This is especially so when a small business is examined for its value for sale.

A prudent business seller or buyer can use financial indicators (such as industry conventions, multiples and ratios) as part of a toolkit to negotiate an acceptable business sale price. One indicator is a price earnings multiple. Elsewhere we have examined business valuation with EBIT multiples.

PE multiple or PE ratio definition

A price earning multiple (PE multiple) is used mostly to estimate the performance of companies whose shares are traded in public and therefore reflect market expectation to a credible extent. The PE multiple of a share is also commonly called its "PE ratio", "earnings multiple", "multiple", "P/E", or "PE").

The PE multiple method, while unorthodox for small and medium-sized businesses, may provide a useful indicator of the value of a business for sale purposes.

Examples of use of PE multiples in Australian business

You can achieve better outcomes as a seller or buyer if you properly prepare for and anticipate positions that various interested parties might hold during the negotiation dance that takes place for a business sale, purchase, takeover, merger or acquisition. It is useful to study prior transactions and to keep a close watch on market developments. Here are recent examples illustrating the use of PE multiples in media commentary, research reports and takeover documents.

Wealth Creator Magazine in its Sep/Oct 2006 issue reviews "hot" stocks in the 2006-07 financial year. In its commentary it says John Fairfax Holdings Ltd (ASX code: FXJ) "...is currently trading on a price earnings of 16 x and provides a yield of 4.5% fully franked..." and Fosters Group Ltd (ASX code: FGL) "...is trading at a price earnings multiple of 15.6 x 2006 earnings, which we believe is reasonable earnings, reduced gearing and upside potential as the cycle improves."

Intersuisse Ltd in an investment research statement dated 24 August 2006 makes a buy recommendation about BHP Billiton (ASX code: BHP) concluding: "We believe the depth and quality of the company's earnings are such that the stock deserved to be placed on a higher price/earnings (p/e) multiple than the prospective p/e of 10.4 times for FY07 and 9.8 times for FY08 and that multiples of at least 12 to 14 times would be more appropriate."

In an Independent Expert's Report Grant Samuel & Associates Pty Ltd assesses the takeover bid by Rank Group Australia Pty Ltd for Burns, Philp & Company Ltd. Grant Samuel states (at its page 18):

"Capitalisation of earnings or cash flows is the most commonly used method for valuation of industrial businesses. This methodology is most appropriate for industrial businesses with a substantial operating history and a consistent earnings trend that is sufficiently stable to be indicative of ongoing earnings potential. This methodology is not particularly suitable for start-up businesses, businesses with an erratic earnings pattern or businesses that have unusual capital expenditure requirements. This methodology involves capitalising the earnings or cash flows of a business at a multiple that reflects the risks of the business and the stream of income that it generates. These multiples can be applied to a number of different earnings or cash flow measures including EBITDA, EBIT or net profit after tax. These are referred to respectively as EBITDA multiples, EBIT multiples and price earnings multiples. Price earnings multiples are commonly used in the context of the sharemarket. EBITDA and EBIT multiples are more commonly used in valuing whole businesses for acquisition purposes where gearing is in the control of the acquirer."

How to calculate the PE multiple for your business

The PE multiple method is the most commonly used earnings capitalisation methodology. It appears in the following two equations:

1.Total value of business = PE multiple x net profit after tax (NPAT)

2.Value per share = PE multiple x earnings per share

The above two equations can be used to provide some indication of the value of a business. First, using the second equation, dividing the market price of a share by the earnings per share you will be able to calculate the PE multiple for the business. Then by multiplying the PE multiple by NPAT a value for the business can be determined.

With a public company, assume the market value of a share of the company is $35 and the earnings per share is $5, then the PE multiple is 25 divided by 5 which is 7. If the NPAT is $110,000 then the value of the business is $110,000 multiplied by 7, which is $770,000.

As a first step in using the above method, one needs to find a listed company carrying on a business similar to the business of the company to be valued. Next, obtain a copy of the most recent financial statements published by the company, from which the NPAT and EPS of the company can be obtained. Now obtain the recent price quoted for the shares in the company from its Website or the ASX Website.

EPS is a measure of the amount of profit that can be attributed to ordinary shares in the company. If the financial statements of the company do not provide the EPS, it can be calculated by dividing NPAT (after deducting NPAT attributable to any outside equity interests, such as preference shares and any payments made to such outside equity interests) by the total number of ordinary shares on issue. The total number of shares on issue can be got from the balance sheet of the company.

If the PE multiple of the company selected is high it can mean that the shares of the company are overpriced and yet the market is expecting a high return in the future. This could be for several reasons, such as potential for growth in the overseas market or even a change of the CEO. Similarly the PE multiple could be low and the shares underpriced because the company selected is about to be brought under a strict regulatory regime by the Government or it has lost a crucial licence. What is suggested here is that the PE multiple calculated using a typical company in the industry may not totally reflect the situation of the business under review.

PE multiple caution

Since the PE multiple method of valuation is dependent on factors that are approximations, consideration of other relevant performance ratios is recommended, eg dividend per share, dividend yield, dividend cover, net tangible assets per share and cash flow per share.

Ultimately working out the PE multiple is a job for a specialist or professional. It is not a job for a lawyer. It is also not a job for a non-financial business executive who is not properly briefed. But it is useful for everyone to be aware of how the numbers are derived.

http://www.dilanchian.com.au/index.php?option=com_content&task=view&id=166&Itemid=148

Tuesday, 12 December 2006 02:45 Anton Joseph

E-mail | Print | Tags: valuation | business sale/purchase | ip revenue | strategy

When it comes to selling or buying a business the sale price is the greatest obstacle and point of disagreement in many transactions. If there is a reasonable and easily understandable way of determining the value of the business the parties can quickly progress more than half way through the sale process. Although it is said that the right tools must be used to value businesses, no simple method suits all types of businesses. Instead, there are several financial and non-financial performance indicators that are commonly used by businesses to monitor their progress. Some are used to measure profitability whilst others are used to test liquidity.

Financial indicators are normally measured by using ratios calculated using numerical values appearing in the profit and loss account or the balance sheet. Since the indicators are snapshot calculations based on historical figures (figures for the past year), there is an understandable reluctance to always rely on them. This is especially so when a small business is examined for its value for sale.

A prudent business seller or buyer can use financial indicators (such as industry conventions, multiples and ratios) as part of a toolkit to negotiate an acceptable business sale price. One indicator is a price earnings multiple. Elsewhere we have examined business valuation with EBIT multiples.

PE multiple or PE ratio definition

A price earning multiple (PE multiple) is used mostly to estimate the performance of companies whose shares are traded in public and therefore reflect market expectation to a credible extent. The PE multiple of a share is also commonly called its "PE ratio", "earnings multiple", "multiple", "P/E", or "PE").

The PE multiple method, while unorthodox for small and medium-sized businesses, may provide a useful indicator of the value of a business for sale purposes.

Examples of use of PE multiples in Australian business

You can achieve better outcomes as a seller or buyer if you properly prepare for and anticipate positions that various interested parties might hold during the negotiation dance that takes place for a business sale, purchase, takeover, merger or acquisition. It is useful to study prior transactions and to keep a close watch on market developments. Here are recent examples illustrating the use of PE multiples in media commentary, research reports and takeover documents.

Wealth Creator Magazine in its Sep/Oct 2006 issue reviews "hot" stocks in the 2006-07 financial year. In its commentary it says John Fairfax Holdings Ltd (ASX code: FXJ) "...is currently trading on a price earnings of 16 x and provides a yield of 4.5% fully franked..." and Fosters Group Ltd (ASX code: FGL) "...is trading at a price earnings multiple of 15.6 x 2006 earnings, which we believe is reasonable earnings, reduced gearing and upside potential as the cycle improves."

Intersuisse Ltd in an investment research statement dated 24 August 2006 makes a buy recommendation about BHP Billiton (ASX code: BHP) concluding: "We believe the depth and quality of the company's earnings are such that the stock deserved to be placed on a higher price/earnings (p/e) multiple than the prospective p/e of 10.4 times for FY07 and 9.8 times for FY08 and that multiples of at least 12 to 14 times would be more appropriate."

In an Independent Expert's Report Grant Samuel & Associates Pty Ltd assesses the takeover bid by Rank Group Australia Pty Ltd for Burns, Philp & Company Ltd. Grant Samuel states (at its page 18):

"Capitalisation of earnings or cash flows is the most commonly used method for valuation of industrial businesses. This methodology is most appropriate for industrial businesses with a substantial operating history and a consistent earnings trend that is sufficiently stable to be indicative of ongoing earnings potential. This methodology is not particularly suitable for start-up businesses, businesses with an erratic earnings pattern or businesses that have unusual capital expenditure requirements. This methodology involves capitalising the earnings or cash flows of a business at a multiple that reflects the risks of the business and the stream of income that it generates. These multiples can be applied to a number of different earnings or cash flow measures including EBITDA, EBIT or net profit after tax. These are referred to respectively as EBITDA multiples, EBIT multiples and price earnings multiples. Price earnings multiples are commonly used in the context of the sharemarket. EBITDA and EBIT multiples are more commonly used in valuing whole businesses for acquisition purposes where gearing is in the control of the acquirer."

How to calculate the PE multiple for your business

The PE multiple method is the most commonly used earnings capitalisation methodology. It appears in the following two equations:

1.Total value of business = PE multiple x net profit after tax (NPAT)

2.Value per share = PE multiple x earnings per share

The above two equations can be used to provide some indication of the value of a business. First, using the second equation, dividing the market price of a share by the earnings per share you will be able to calculate the PE multiple for the business. Then by multiplying the PE multiple by NPAT a value for the business can be determined.

With a public company, assume the market value of a share of the company is $35 and the earnings per share is $5, then the PE multiple is 25 divided by 5 which is 7. If the NPAT is $110,000 then the value of the business is $110,000 multiplied by 7, which is $770,000.

As a first step in using the above method, one needs to find a listed company carrying on a business similar to the business of the company to be valued. Next, obtain a copy of the most recent financial statements published by the company, from which the NPAT and EPS of the company can be obtained. Now obtain the recent price quoted for the shares in the company from its Website or the ASX Website.

EPS is a measure of the amount of profit that can be attributed to ordinary shares in the company. If the financial statements of the company do not provide the EPS, it can be calculated by dividing NPAT (after deducting NPAT attributable to any outside equity interests, such as preference shares and any payments made to such outside equity interests) by the total number of ordinary shares on issue. The total number of shares on issue can be got from the balance sheet of the company.

If the PE multiple of the company selected is high it can mean that the shares of the company are overpriced and yet the market is expecting a high return in the future. This could be for several reasons, such as potential for growth in the overseas market or even a change of the CEO. Similarly the PE multiple could be low and the shares underpriced because the company selected is about to be brought under a strict regulatory regime by the Government or it has lost a crucial licence. What is suggested here is that the PE multiple calculated using a typical company in the industry may not totally reflect the situation of the business under review.

PE multiple caution

Since the PE multiple method of valuation is dependent on factors that are approximations, consideration of other relevant performance ratios is recommended, eg dividend per share, dividend yield, dividend cover, net tangible assets per share and cash flow per share.

Ultimately working out the PE multiple is a job for a specialist or professional. It is not a job for a lawyer. It is also not a job for a non-financial business executive who is not properly briefed. But it is useful for everyone to be aware of how the numbers are derived.

http://www.dilanchian.com.au/index.php?option=com_content&task=view&id=166&Itemid=148

Modern trading making earnings multiples obsolete

Modern trading making earnings multiples obsolete

by Grace Chen on May 19, 2008

Price to earnings multiples were once the basis of investment decisions. The analysis was simple: the return divided by the stock price should properly valuate a certain company. But with many companies all over the map in both PE and PEG ratios, investors are looking for other guidelines for evaluating an investment. Technical trading has all but taken over the short term trader, and it looks ready to conquer the long term as well.

Old value investors

Warren Buffett dominates the field of value investing. Rather than following the world’s hottest stocks, he looks for companies that are considerably undervalued, both by assets and what he believes the company is really worth. While he’s made a large fortune from his studies on value investing, the markets are seemingly turning out of his favor. Valuing a company is no longer as easy as looking for cheap assets, as many companies have little assets to back their valuations. Others trade at huge multiples of their earnings, while their competitors enjoy smaller ratios, and even others are destined to stay cheap forever due only to the nature of the business.

Case in point

It seems that many companies are selling for high premiums, even with little to back up their valuations. Take for example the internet stocks. Google sells for a PE ratio of 41 but a PEG of 1.02. While Google does sell for an extreme premium over its earnings, adjusted for growth Google is still in the buy range. Compare these statistics to the lesser rival Yahoo, which trades for a PE of 33 and a PEG of 2.8. Even prior to the failed Microsoft bid, Yahoo traded at a similar PE and PEG ratio; for the most part, it’s horribly overvalued.

Traditionally, you would think that the two valuations would come to meet each other in the middle. Google’s price would ultimately rise while Yahoo would shed a few points to come back to earth. Though this is what the rational person would think, it seems like Yahoo will forever enjoy being overpriced and Google will always be under priced. In fact, Google has never traded for a PEG ratio higher than 2. Yahoo has traded for both extremely high PE ratios and PEGs, though its data is somewhat skewed by the y2k internet bubble fiasco.

Has technical analysis beat out fundamentals?

It appears as though technical traders have finally won over the market. By looking at today’s measurements, Yahoo’s stock is kept afloat largely by technical support and resistance, while Google is much the same. The difference in trading techniques even from just 2004 to today would suggest that stocks are now traded more independently than ever. Rarely are stocks compared to reasonable value to their competitors by investors. The new age of trading is systematically making investors “one stock” types, those only willing to trade the ups and downs and day to day of a specific stock, rather than comparing it to its competition.

Investing at its roots has been crippled. The sustainability or profitability of future results are rarely calculated in many investors algorithms. Technical analysis has instead brought trading to a whole new level, where stocks are nearly as good as any other commodity. The earnings of a company no longer matter, nor do its assets, nor its valuation. The digits in the stock price are the few things that matter to most modern day traders; forget the business behind the ticker.

http://www.investortrip.com/modern-trading-making-earnings-multiples-obsolete/

Comment: Ohhhh!!!!!

by Grace Chen on May 19, 2008

Price to earnings multiples were once the basis of investment decisions. The analysis was simple: the return divided by the stock price should properly valuate a certain company. But with many companies all over the map in both PE and PEG ratios, investors are looking for other guidelines for evaluating an investment. Technical trading has all but taken over the short term trader, and it looks ready to conquer the long term as well.

Old value investors

Warren Buffett dominates the field of value investing. Rather than following the world’s hottest stocks, he looks for companies that are considerably undervalued, both by assets and what he believes the company is really worth. While he’s made a large fortune from his studies on value investing, the markets are seemingly turning out of his favor. Valuing a company is no longer as easy as looking for cheap assets, as many companies have little assets to back their valuations. Others trade at huge multiples of their earnings, while their competitors enjoy smaller ratios, and even others are destined to stay cheap forever due only to the nature of the business.

Case in point

It seems that many companies are selling for high premiums, even with little to back up their valuations. Take for example the internet stocks. Google sells for a PE ratio of 41 but a PEG of 1.02. While Google does sell for an extreme premium over its earnings, adjusted for growth Google is still in the buy range. Compare these statistics to the lesser rival Yahoo, which trades for a PE of 33 and a PEG of 2.8. Even prior to the failed Microsoft bid, Yahoo traded at a similar PE and PEG ratio; for the most part, it’s horribly overvalued.

Traditionally, you would think that the two valuations would come to meet each other in the middle. Google’s price would ultimately rise while Yahoo would shed a few points to come back to earth. Though this is what the rational person would think, it seems like Yahoo will forever enjoy being overpriced and Google will always be under priced. In fact, Google has never traded for a PEG ratio higher than 2. Yahoo has traded for both extremely high PE ratios and PEGs, though its data is somewhat skewed by the y2k internet bubble fiasco.

Has technical analysis beat out fundamentals?

It appears as though technical traders have finally won over the market. By looking at today’s measurements, Yahoo’s stock is kept afloat largely by technical support and resistance, while Google is much the same. The difference in trading techniques even from just 2004 to today would suggest that stocks are now traded more independently than ever. Rarely are stocks compared to reasonable value to their competitors by investors. The new age of trading is systematically making investors “one stock” types, those only willing to trade the ups and downs and day to day of a specific stock, rather than comparing it to its competition.

Investing at its roots has been crippled. The sustainability or profitability of future results are rarely calculated in many investors algorithms. Technical analysis has instead brought trading to a whole new level, where stocks are nearly as good as any other commodity. The earnings of a company no longer matter, nor do its assets, nor its valuation. The digits in the stock price are the few things that matter to most modern day traders; forget the business behind the ticker.

http://www.investortrip.com/modern-trading-making-earnings-multiples-obsolete/

Comment: Ohhhh!!!!!

A Crash Course on Earnings Multiples

A Crash Course on Earnings Multiples

As a trusted business advisor you’ve probably heard former business owners telling people that they sold their business for “six times earnings.” As investment bankers, the first question we hear from prospective clients is “Can I get the same multiple if I sell my business?” The answer is an unequivocal "it depends." It depends on a number of things, but first and foremost, it depends on how you define “earnings”.

As all investment bankers and sellers know, “Cash is King.” After all, cash removes the seller’s risk in the transaction. However, when a buyer pays cash for a business, that buyer wants to know exactly how much the business is earning.

Let’s start with what seems to be a pretty basic concept: earnings.

The Definitions of Earnings

There are several definitions of earnings; each is potentially different from the other depending on the type of company and the way its owner runs the company. Typical measures of earnings include:

§ Net Operating Income: This is sales less the cost of goods sold and operating expenses.

§ Pre-tax Income: This is net operating income plus non-operating income (like interest on notes, etc.) less non-operating expenses (like one-time, non-recurring expenses).

§ After-tax Income: Pre-tax income, less all company (but not individual) taxes.

§ EBIT: This stands for earnings before interest and taxes.

§ EBITDA: This stands for earnings before interest, taxes, depreciation and amortization

Add to these measures, the need to “adjust" earnings by deducting capital expenditures, and adding back excess rents, excessive salary and bonuses paid to the owner and his or her family. The result is something called:

Owner’s Discretionary Cash Flow or True Cash Flow: This is the amount of pre-tax money distributed to owners via salary, bonus, distributions from the company such as S-distributions, and rental payments in excess of fair market rental value of the equipment or building used in the business. This provides buyers with the most accurate indicator of how much “cash” a company can actually produce and is often the most meaningful indicator of value.

Which brings us back to our original question: Is it realistic for a business owner to expect a six times multiple when he sells his business? There is no one right or wrong answer to this question.

To show you how tricky this can be, let’s look at a former client of ours. His business was not doing well. He had revenues of approximately $7 million but, even using the most generous definition of earnings, the company was not earning more that about $100,000 per year. We ultimately sold the company to a buyer of distressed companies who paid book value for its assets or about $2 million. Despite this low value, our client was extremely happy because his business sold for 20 times earnings! In this case the buyer was buying assets, not earnings, so an earning multiple wasn’t even appropriate.

To determine which measure of earnings is appropriate for a business, you need to look first at how the seller’s industry defines “earnings”. This "earnings" measure reflects how much a buyer can afford to pay for the business. The actual multiple applied will be based on:

§ which definition of cash flow is being used,

§ what is appropriate for a given industry,

§ what the company’s specific growth prospects are,

§ how the company’s earnings compare with similar companies in the same industry, and finally

§ how the company’s earnings compare with the company’s asset value.

Richard E. Jackim, JD, MBA, CEPA is the author of the critically acclaimed book, “The $10 Trillion Opportunity: Designing Successful Exit Strategies for Middle Market Business Owners”, available at http://www.exit-planning-institute.org/

http://www.imakenews.com/epi_hfco/e_article001197834.cfm?x=bdnqbsy,w

As a trusted business advisor you’ve probably heard former business owners telling people that they sold their business for “six times earnings.” As investment bankers, the first question we hear from prospective clients is “Can I get the same multiple if I sell my business?” The answer is an unequivocal "it depends." It depends on a number of things, but first and foremost, it depends on how you define “earnings”.

As all investment bankers and sellers know, “Cash is King.” After all, cash removes the seller’s risk in the transaction. However, when a buyer pays cash for a business, that buyer wants to know exactly how much the business is earning.

Let’s start with what seems to be a pretty basic concept: earnings.

The Definitions of Earnings

There are several definitions of earnings; each is potentially different from the other depending on the type of company and the way its owner runs the company. Typical measures of earnings include:

§ Net Operating Income: This is sales less the cost of goods sold and operating expenses.

§ Pre-tax Income: This is net operating income plus non-operating income (like interest on notes, etc.) less non-operating expenses (like one-time, non-recurring expenses).

§ After-tax Income: Pre-tax income, less all company (but not individual) taxes.

§ EBIT: This stands for earnings before interest and taxes.

§ EBITDA: This stands for earnings before interest, taxes, depreciation and amortization

Add to these measures, the need to “adjust" earnings by deducting capital expenditures, and adding back excess rents, excessive salary and bonuses paid to the owner and his or her family. The result is something called:

Owner’s Discretionary Cash Flow or True Cash Flow: This is the amount of pre-tax money distributed to owners via salary, bonus, distributions from the company such as S-distributions, and rental payments in excess of fair market rental value of the equipment or building used in the business. This provides buyers with the most accurate indicator of how much “cash” a company can actually produce and is often the most meaningful indicator of value.

Which brings us back to our original question: Is it realistic for a business owner to expect a six times multiple when he sells his business? There is no one right or wrong answer to this question.

To show you how tricky this can be, let’s look at a former client of ours. His business was not doing well. He had revenues of approximately $7 million but, even using the most generous definition of earnings, the company was not earning more that about $100,000 per year. We ultimately sold the company to a buyer of distressed companies who paid book value for its assets or about $2 million. Despite this low value, our client was extremely happy because his business sold for 20 times earnings! In this case the buyer was buying assets, not earnings, so an earning multiple wasn’t even appropriate.

To determine which measure of earnings is appropriate for a business, you need to look first at how the seller’s industry defines “earnings”. This "earnings" measure reflects how much a buyer can afford to pay for the business. The actual multiple applied will be based on: