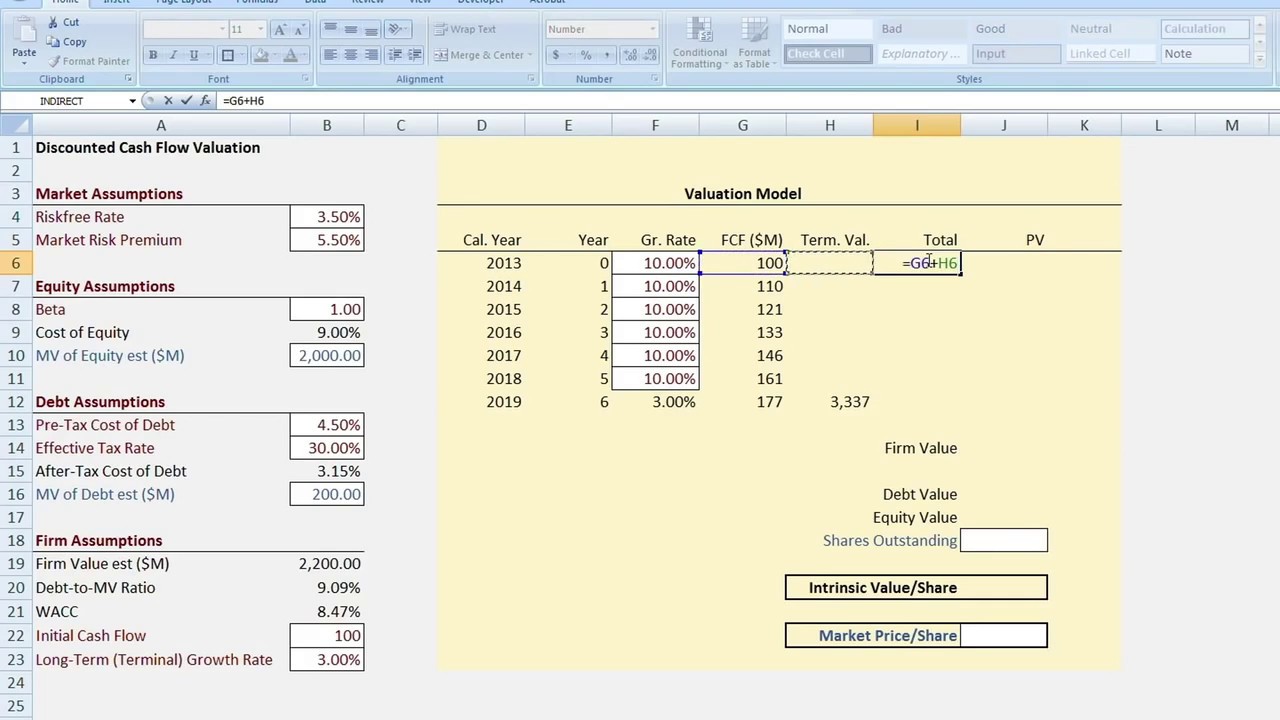

Price is a number that is often a delusion and nearly always a distraction.

The price attached to a stock or other financial asset changes in a frantic hum, often several thousand times a day, causing corrosive intellectual damage.

It may have little relation to VALUE, although it is more interesting and keeps most of the financial media quite busy.

The continual flux and spurious precision of price will cast an illusion of certainty, fooling many investors into thinking that the exact worth of a stock is knowable at any given moment.

That tricks investors into believing that even tiny changes in price can have great significance when, in fact, the constant twitching of stock prices is nothing but statistical noise.

Under the illusion of certainty created by PRICE, investors forget that VALUE is approximate and that it barely changes on even a monthly time scale.

Investors who fixate constantly on price will always end up trading too much and overreacting to other people's mood swings; only those who focus on ascertaining value will achieve superior returns in the long run.

Example:

If asked what your house is worth, would you respond, "$237,432.17?" Of course not.

You know perfectly well that nobody, including you, knows what your house is worth to the nearest thousand dollars, let alone to the nearest penny or fraction of a penny.

Instead, you would say, "Between $200,000 and $250,000 maybe."

With stocks and other financial assets, price is also an approximation; any precision is an illusion.

The price attached to a stock or other financial asset changes in a frantic hum, often several thousand times a day, causing corrosive intellectual damage.

It may have little relation to VALUE, although it is more interesting and keeps most of the financial media quite busy.

The continual flux and spurious precision of price will cast an illusion of certainty, fooling many investors into thinking that the exact worth of a stock is knowable at any given moment.

That tricks investors into believing that even tiny changes in price can have great significance when, in fact, the constant twitching of stock prices is nothing but statistical noise.

Under the illusion of certainty created by PRICE, investors forget that VALUE is approximate and that it barely changes on even a monthly time scale.

Investors who fixate constantly on price will always end up trading too much and overreacting to other people's mood swings; only those who focus on ascertaining value will achieve superior returns in the long run.

Example:

If asked what your house is worth, would you respond, "$237,432.17?" Of course not.

You know perfectly well that nobody, including you, knows what your house is worth to the nearest thousand dollars, let alone to the nearest penny or fraction of a penny.

Instead, you would say, "Between $200,000 and $250,000 maybe."

With stocks and other financial assets, price is also an approximation; any precision is an illusion.