Can you picture China in five years (2011-2015)?

Will it still be difficult to buy a house in big cities like Beijing? Will the income gap between the rich and poor narrow or widen? Is the growth model relying on exports or domestic consumption? How about the investment environment in China? In what areas will the government provide policy support? Are we prepared for an aging Chinese society? Is China ready to shoulder its global responsibilities?

There are no easy answers to these questions, which nonetheless need prudent analysis and well-informed strategies, to realize the ultimate goal of development, reform and opening up.

What goal? “To give all Chinese people a happy life,” in the words of Chinese Premier Wen Jiabao.

The Communist Party of China (CPC) Central Committee's Proposal on Formulating the Twelfth Five-year Program (2011-2015) on National Economic and Social Development was adopted at the Fifth Plenary Session of the 17th CPC Central Committee, which ended Oct 18. The draft is subject to approval by the National People's Congress, China's top legislature, when it convenes its annual session next year.

This special coverage focuses on the proposal and the extensive issues that will shape the country's development over the next five years.

http://www.chinadaily.com.cn/china/2010-11/08/content_11513304.htm

Showing posts with label China. Show all posts

Showing posts with label China. Show all posts

Thursday 11 November 2010

Tuesday 26 October 2010

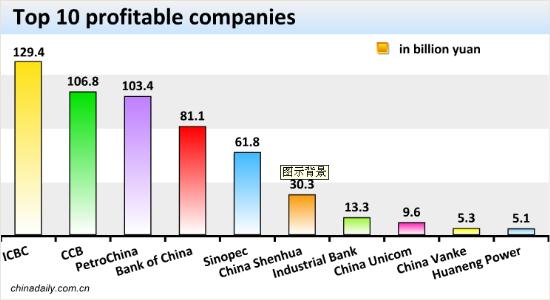

Top 10 profitable companies in China

Web Exclusive

Top 10 profitable companies in China

(chinadaily.com.cn)

Updated: 2010-03-30 11:26

All but two of China's top 10 most profitable Shanghai- or Shenzhen-listed companies in 2009 are from the energy or financial sector, the Beijing Times reported Tuesday, based on 832 annual financial reports, or more than half of the total that were released by Monday morning.

With a staggering 129.4 billion yuan ($18.95 billion) in after-tax profit, the Industrial and Commercial Bank of China (ICBC), the world's biggest lender by market value, replaced PetroChina Co as the country's most profitable listed company, followed by China Construction Bank with 106.84 billion yuan ($15.65 billion), according to the newspaper citing Wind Info, a financial data provider in China.

PetroChina Co, the country's largest oil and gas producer, came in third with 103.39 billion yuan ($15.14 billion) in net profit last year and Bank of China, the country's third-largest lender by market value, took fourth place with 81.07 billion yuan.

Sinopec Corp, Asia's top oil refiner, ranked fifth with 61.76 billion yuan ($9.05 billion), and China Shenhua Energy Co, China's largest coal producer, sixth with 30.28 billion yuan ($4.43 billion).

The other four are Industrial Bank Co (13.3 billion yuan), a mid-sized Chinese lender; China Unicom (9.56 billion yuan), China's No 2 mobile carrier; China Vanke Co (5.33 billion yuan), the country's biggest property developer by market value and Huaneng Power International Co (5.08 billion yuan), China's biggest listed electricity producer.

The total profit of the top 10 companies is 561.14 billion yuan, or 75 percent of the total for the 832 companies combined. The total profit for the 832 companies is 749.55 billion yuan.

Other companies that are likely to make the top 10 list include China Life Insurance Co and China Merchants Bank, which have yet to release their annual reports.

The list excluded Chinese companies that list in Hong Kong, like China Mobile.

http://www.chinadaily.com.cn/business/2010-03/30/content_9661921.htm

Top 10 profitable companies in China

(chinadaily.com.cn)

Updated: 2010-03-30 11:26

All but two of China's top 10 most profitable Shanghai- or Shenzhen-listed companies in 2009 are from the energy or financial sector, the Beijing Times reported Tuesday, based on 832 annual financial reports, or more than half of the total that were released by Monday morning.

With a staggering 129.4 billion yuan ($18.95 billion) in after-tax profit, the Industrial and Commercial Bank of China (ICBC), the world's biggest lender by market value, replaced PetroChina Co as the country's most profitable listed company, followed by China Construction Bank with 106.84 billion yuan ($15.65 billion), according to the newspaper citing Wind Info, a financial data provider in China.

PetroChina Co, the country's largest oil and gas producer, came in third with 103.39 billion yuan ($15.14 billion) in net profit last year and Bank of China, the country's third-largest lender by market value, took fourth place with 81.07 billion yuan.

Related full coverage: 2009 Annual Reports of Listed Companies 2009 Annual Reports of Listed Companies | ||

Sinopec Corp, Asia's top oil refiner, ranked fifth with 61.76 billion yuan ($9.05 billion), and China Shenhua Energy Co, China's largest coal producer, sixth with 30.28 billion yuan ($4.43 billion).

The other four are Industrial Bank Co (13.3 billion yuan), a mid-sized Chinese lender; China Unicom (9.56 billion yuan), China's No 2 mobile carrier; China Vanke Co (5.33 billion yuan), the country's biggest property developer by market value and Huaneng Power International Co (5.08 billion yuan), China's biggest listed electricity producer.

The total profit of the top 10 companies is 561.14 billion yuan, or 75 percent of the total for the 832 companies combined. The total profit for the 832 companies is 749.55 billion yuan.

Other companies that are likely to make the top 10 list include China Life Insurance Co and China Merchants Bank, which have yet to release their annual reports.

The list excluded Chinese companies that list in Hong Kong, like China Mobile.

http://www.chinadaily.com.cn/business/2010-03/30/content_9661921.htm

Wednesday 20 October 2010

China's rate hike complicates bid to control yuan

20 OCT, 2010

China's rate hike complicates bid to control yuan

BEIJING: China's first rate hike since 2007 has laid bare official fears over surging prices but could also complicate Beijing's controversial efforts to keep a lid on its currency, analysts said.

The move announced by the central bank late Tuesday caught global markets by surprise and came before a meeting this week of G20 finance ministers in South Korea , where currency frictions are expected to loom large.

Rising inflation and soaring property prices forced the government to hike one-year lending and deposit rates by 25 basis points each, after a range of previous measures introduced this year proved inadequate, analysts said.

They said the move may also indicate that third-quarter data China is to unveil on Thursday will show the world's second-largest economy grew faster than authorities had expected, easing any qualms about raising rates.

The "decision suggests the acceleration in growth and official worries about property and inflation are more serious than anticipated", said Ben Simpfendorfer, a Hong Kong-based economist at Royal Bank of Scotland .

The rate hike depressed stock markets across Asia Wednesday on worries that any Chinese slowdown could hit fragile global growth. Tokyo's Nikkei index closed 1.65 percent down and the Hang Seng in Hong Kong slipped 0.87 percent.

China's inflation has accelerated in recent months, rising at its fastest pace in nearly two years in August when consumer prices went up 3.5 percent year-on-year, as food prices surged after extreme weather hit crop yields.

At the same time, property prices in major cities have remained stubbornly high and bank lending has continued to grow, defying official moves to dampen both.

"The asymmetric hike suggest that the authorities wished to make deposits a more attractive investment proposition than property to discourage property speculation," Nomura analysts Tomo Kinoshita and Chi Sun said in a note.

Beijing has delayed raising interest rates until now partly due to concerns it could attract speculative money chasing a relatively higher yield, making it more difficult to keep the Chinese yuan stable.

The central bank has to buy the dollars flowing into China's export machine to prevent the yuan from rising too quickly. The dollars then pile up on the country's world-beating stockpile of foreign currency reserves.

Beijing pledged in June to let the yuan trade more freely and the currency has since strengthened slightly. But Beijing maintains a tight grip on the yuan despite US and European pressure to let it appreciate.

The yuan was trading Wednesday at 6.6546 to the dollar, weaker than Tuesday's close of 6.6447.

Critics of China's yuan policy say it undervalues the currency by as much as 40 percent to give Chinese exports an unfair edge on world markets.

Higher interest rates could lead to an "intractable monetary policy dilemma" for Beijing by encouraging more foreign capital inflows into China, said Nicholas Consonery, an analyst at Washington-based Eurasia Group.

http://economictimes.indiatimes.com/articleshow/6779921.cms

China's rate hike complicates bid to control yuan

BEIJING: China's first rate hike since 2007 has laid bare official fears over surging prices but could also complicate Beijing's controversial efforts to keep a lid on its currency, analysts said.

The move announced by the central bank late Tuesday caught global markets by surprise and came before a meeting this week of G20 finance ministers in South Korea , where currency frictions are expected to loom large.

Rising inflation and soaring property prices forced the government to hike one-year lending and deposit rates by 25 basis points each, after a range of previous measures introduced this year proved inadequate, analysts said.

They said the move may also indicate that third-quarter data China is to unveil on Thursday will show the world's second-largest economy grew faster than authorities had expected, easing any qualms about raising rates.

The "decision suggests the acceleration in growth and official worries about property and inflation are more serious than anticipated", said Ben Simpfendorfer, a Hong Kong-based economist at Royal Bank of Scotland .

The rate hike depressed stock markets across Asia Wednesday on worries that any Chinese slowdown could hit fragile global growth. Tokyo's Nikkei index closed 1.65 percent down and the Hang Seng in Hong Kong slipped 0.87 percent.

China's inflation has accelerated in recent months, rising at its fastest pace in nearly two years in August when consumer prices went up 3.5 percent year-on-year, as food prices surged after extreme weather hit crop yields.

At the same time, property prices in major cities have remained stubbornly high and bank lending has continued to grow, defying official moves to dampen both.

"The asymmetric hike suggest that the authorities wished to make deposits a more attractive investment proposition than property to discourage property speculation," Nomura analysts Tomo Kinoshita and Chi Sun said in a note.

Beijing has delayed raising interest rates until now partly due to concerns it could attract speculative money chasing a relatively higher yield, making it more difficult to keep the Chinese yuan stable.

The central bank has to buy the dollars flowing into China's export machine to prevent the yuan from rising too quickly. The dollars then pile up on the country's world-beating stockpile of foreign currency reserves.

Beijing pledged in June to let the yuan trade more freely and the currency has since strengthened slightly. But Beijing maintains a tight grip on the yuan despite US and European pressure to let it appreciate.

The yuan was trading Wednesday at 6.6546 to the dollar, weaker than Tuesday's close of 6.6447.

Critics of China's yuan policy say it undervalues the currency by as much as 40 percent to give Chinese exports an unfair edge on world markets.

Higher interest rates could lead to an "intractable monetary policy dilemma" for Beijing by encouraging more foreign capital inflows into China, said Nicholas Consonery, an analyst at Washington-based Eurasia Group.

http://economictimes.indiatimes.com/articleshow/6779921.cms

Friday 15 October 2010

How manufacturing declines impoverish the majority of the working population

Making a big mistake

John Legge

October 15, 2010

To accept the decline of manufacturing in Australia is to ignore history and threatens to condemn our workers to a low-wage future.

THE Treasury ''red book'' advises the Gillard government to suppress manufacturing in order to balance the growth of the mining industry. Many economists, including at least two members of the federal cabinet, don't need excuses to applaud the decline of manufacturing in Australia: they consider the move of manufacturing to low-wage countries inevitable and that the sooner the process is complete the better.

Few economists study history, and fewer realise how critical manufacturing industry was and is in creating a relatively just and harmonious Australian society. Before the rise of manufacturing the major occupations were farm labourer and domestic servant: hard work for little pay. Manufacturing provided jobs for ordinary people with ordinary backgrounds and modest educational achievements.

It paid vastly better than farm labouring or domestic service, and diligent workers who were prepared to accept responsibility could earn middle-class wages as leading hands and foremen. Even production-line workers in some industries could earn middle-class wages: high wages made the discipline and boredom of production-line work tolerable.

Complex manufacturing offers opportunities for men and women with no more than high school education to earn real middle-class wages because they are going to be responsible for expensive precision machinery and the production of complex, valuable products. Most of the simple, repetitive tasks have been automated; humans are used where skill and judgment are needed. Adam Smith famously visited a pin factory (or on some accounts read about a pin factory and described it as if he had visited it). Few economists have crossed a factory threshold since; most seem to believe that nothing has changed since 1776.

Economists have noticed that as manufacturing declines, the majority of the working population gets relatively poorer (or in the case of the US, absolutely poorer) while well-educated professionals continue to enjoy rising living standards. Most economists draw the conclusion that it is the higher educational level achieved by these professional workers that accounts for their higher incomes. They argue that better educational opportunities and higher school retention rates will halt the increase in inequality.

Unfortunately, the orthodox explanation is, at best, oversimplified.

Better education means nothing in the job market if the jobs for well-educated people aren't there. Much, possibly most, of the employment in modern manufacturing enterprises isn't on the shop floor at all. Manufacturers need engineers, designers, programmers, marketers and accountants; the robots need maintenance and setting up; specialist craftsmen must make the tools and dies that the production machines use. Software has become incredibly important: a single modern car has more computer power in it that was available to the Apollo mission to the moon.

Some economists seem to believe that only the physical part of the manufacturing process will be moved to China: the professional tasks will continue to be performed by Australians in Australia. These views can only come from a fundamental misunderstanding of the way manufacturing industry works. It also assumes that the Chinese are incapable of training their own engineers, designers and programmers. Finally, the idea that China's apparent cost advantages will continue requires the assumption that Chinese workers are prepared to spend their working lives making goods that they cannot afford themselves.

None of these assumptions is supported by facts. While Australia spent the Howard years cutting higher education and loading young engineers and scientists with penal HECS debts, the Chinese poured public money into education at all levels. China now produces more engineering and science graduates annually than the number of graduates Australian universities produce each year in every discipline.

Chinese workers are no longer prepared to work long hours for low pay in order to make toys for Westerners. Foxconn, the Chinese company that makes iPhones and iPads among many other familiar products, has raised production-line wages by half over the past year and the process is not going to stop. The Chinese regime is oppressive by Australian standards but Chinese workers are not slaves: they can and do switch jobs when offered improved pay and conditions. As wages rise, Chinese companies will automate more; and, with more sophisticated machinery and higher responsibilities, wages will rise still further.

Australia's mining boom is transient, as all booms are; but should we destroy our manufacturing industry, the loss of competitive strength will be almost impossible to reverse. Do we really want Chinese pundits in a few years' time promoting Australia as a country with a docile, low-wage workforce prepared to do work that Chinese workers disdain?

John Legge is a Melbourne-based educator, author and consultant.

http://www.smh.com.au/business/making-a-big-mistake-20101014-16ly7.html

John Legge

October 15, 2010

To accept the decline of manufacturing in Australia is to ignore history and threatens to condemn our workers to a low-wage future.

THE Treasury ''red book'' advises the Gillard government to suppress manufacturing in order to balance the growth of the mining industry. Many economists, including at least two members of the federal cabinet, don't need excuses to applaud the decline of manufacturing in Australia: they consider the move of manufacturing to low-wage countries inevitable and that the sooner the process is complete the better.

Few economists study history, and fewer realise how critical manufacturing industry was and is in creating a relatively just and harmonious Australian society. Before the rise of manufacturing the major occupations were farm labourer and domestic servant: hard work for little pay. Manufacturing provided jobs for ordinary people with ordinary backgrounds and modest educational achievements.

It paid vastly better than farm labouring or domestic service, and diligent workers who were prepared to accept responsibility could earn middle-class wages as leading hands and foremen. Even production-line workers in some industries could earn middle-class wages: high wages made the discipline and boredom of production-line work tolerable.

Complex manufacturing offers opportunities for men and women with no more than high school education to earn real middle-class wages because they are going to be responsible for expensive precision machinery and the production of complex, valuable products. Most of the simple, repetitive tasks have been automated; humans are used where skill and judgment are needed. Adam Smith famously visited a pin factory (or on some accounts read about a pin factory and described it as if he had visited it). Few economists have crossed a factory threshold since; most seem to believe that nothing has changed since 1776.

Economists have noticed that as manufacturing declines, the majority of the working population gets relatively poorer (or in the case of the US, absolutely poorer) while well-educated professionals continue to enjoy rising living standards. Most economists draw the conclusion that it is the higher educational level achieved by these professional workers that accounts for their higher incomes. They argue that better educational opportunities and higher school retention rates will halt the increase in inequality.

Unfortunately, the orthodox explanation is, at best, oversimplified.

Better education means nothing in the job market if the jobs for well-educated people aren't there. Much, possibly most, of the employment in modern manufacturing enterprises isn't on the shop floor at all. Manufacturers need engineers, designers, programmers, marketers and accountants; the robots need maintenance and setting up; specialist craftsmen must make the tools and dies that the production machines use. Software has become incredibly important: a single modern car has more computer power in it that was available to the Apollo mission to the moon.

Some economists seem to believe that only the physical part of the manufacturing process will be moved to China: the professional tasks will continue to be performed by Australians in Australia. These views can only come from a fundamental misunderstanding of the way manufacturing industry works. It also assumes that the Chinese are incapable of training their own engineers, designers and programmers. Finally, the idea that China's apparent cost advantages will continue requires the assumption that Chinese workers are prepared to spend their working lives making goods that they cannot afford themselves.

None of these assumptions is supported by facts. While Australia spent the Howard years cutting higher education and loading young engineers and scientists with penal HECS debts, the Chinese poured public money into education at all levels. China now produces more engineering and science graduates annually than the number of graduates Australian universities produce each year in every discipline.

Chinese workers are no longer prepared to work long hours for low pay in order to make toys for Westerners. Foxconn, the Chinese company that makes iPhones and iPads among many other familiar products, has raised production-line wages by half over the past year and the process is not going to stop. The Chinese regime is oppressive by Australian standards but Chinese workers are not slaves: they can and do switch jobs when offered improved pay and conditions. As wages rise, Chinese companies will automate more; and, with more sophisticated machinery and higher responsibilities, wages will rise still further.

The low wages favouring China for manufacturing are transient; the created competitive advantages of a skilled workforce backed up by an experienced cadre of engineers, scientists and marketers are permanent.

Australia's mining boom is transient, as all booms are; but should we destroy our manufacturing industry, the loss of competitive strength will be almost impossible to reverse. Do we really want Chinese pundits in a few years' time promoting Australia as a country with a docile, low-wage workforce prepared to do work that Chinese workers disdain?

John Legge is a Melbourne-based educator, author and consultant.

http://www.smh.com.au/business/making-a-big-mistake-20101014-16ly7.html

Saturday 9 October 2010

India is tipped to emerge from China's shadow

India has been overlooked by investors, but it should not be ignored.

By Emma Wall

Published: 5:21PM BST 08 Oct 2010

2 Comments

If there were a popularity contest for emerging markets, India would struggle to win a medal. As the Commonwealth Games host has had difficulty enticing crowds to the sporting event, so too have investors shunned its economy in favour of India's bigger neighbour, China.

British fund investors have put £4bn more into China than into India, according to Morningstar, the analyst – China has attracted £15bn from UK-registered unit trusts, compared with £11bn for India.

Related Articles

Are British investors missing a trick by shunning Wall St?

Scottish social housing needs investment as safe as 'gilts'

Silver price boosts Hochschild to near all-time high

Super-rich buy gold by the ton

'We are going to have higher prices for commodities'

Emerging markets second wind blows in the face of short-term thinking

But the smart money may do well not to just follow the crowd China may be the current star of the BRIC show, but India could eclipse its neighbour in the not-too-distant future.

"In the last year, the MSCI India index is up by 22pc, whereas China is up by only 5.8pc," said Allan Conway of Schroders. "China may have better short-term prospects, but India is less developed and so has further to grow. Add to this China's prematurely ageing population due to the one-child policy, and I would say on a five-year-plus view that India is the more attractive investment opportunity."

India's economy is expected to grow by about 9pc next year, and although the budget deficit is 4.5pc, very little of this is in foreign currency, making it manageable.

India's past performance has been impressive too. If you had invested £1,000 in J P Morgan's Indian investment trust a decade ago, it would now be worth more than £6,000; had you invested a similar sum in the HSBC GIF Indian Equity unit trust, it would have grown to £7,433.

Short-term performance has also been positive. In the past year First State's Indian Subcontinent fund has returned 39pc and the India Capital Growth investment trust has risen by 58pc.

The past year has been prosperous for India. A new single-party government – India had been governed by coalitions since 1991 – was elected in May 2009 and has focused on corporate governance and tax regulation. It is introducing identity cards, which will be used to tax workers more efficiently and provide income for the state.

"It used to take a year to build the same number of roads that are being constructed in a day," said Pinakin Patel of J P Morgan.

India is a domestic market, supporting its own industry rather than relying heavily on exports like Russia and Brazil. This means that it was less affected by the global economic downturn than some of its emerging market peers, and can offer investors a hedge against a European or American double-dip.

India has a lower dependence on commodities than other emerging markets, contributing just 25pc of the equity market, compared with 36pc in South Africa, 46pc in Brazil and 70pc in Russia. The more diverse market offers more stability instead, mainly being a composite of financials at 30pc and energy, which is 25pc of the market.

Future investment opportunities lie not in big cities such as Mumbai and Delhi, but in smaller centres. Investors will be able to get the growth prospects of a frontier market, but with the stability of a more developed country.

The consumer story is big in these regions. Not only are the growing middle classes buying more goods and eating more meat, but their rise in social status is encouraging more infrastructure to be built and bringing big business to the financials.

"I come from a rural part of India," said Mr Patel. "I know how much people keep under the mattress. But more people are getting bank accounts, mortgages and credit cards – which is why we chose to play the consumer trend more indirectly through the financials." Four of the top five holdings in the J P Morgan investment trust are banks.

The newly launched Insynergy Absolute India fund favours financials too. It is run by India's largest business, Reliance Group, which invests in HDFC Bank. The high savings and investment rate, 37pc of GDP, coupled with the large as yet untapped market make it a good long-term growth holding.

Other sectors touted as opportunities for growth are pharmaceuticals, technology and infrastructure.

As the Commonwealth Games have proved, however, regulation in emerging economies is simply not on a par with the Western world. Fund managers may have puffed infrastructure as an area to invest in, but who wants to invest in the kind of bridges that collapse?

"India remains a very rough diamond," said Darius McDermott of Chelsea Financial Services. "In terms of infrastructure it remains a decade behind China – in many parts of the country roads are truly catastrophic. Energy supply is a perennial problem, as is the supply of skilled workers."

Mr Patel stressed that investors should not confuse publicly funded infrastructure, which is poorly regulated, with privately funded infrastructure. "Privately funded construction has many success stories, such as the Delhi metro," he said. "India is not perfect, but it has an English legal system and a proper accounting system. We chose to work with leading companies with a good track record." The JPM fund holds Larsen & Toubro, which builds power plants, and BHEL, a builder of roads and airports – both with 40-year histories.

While the Empire may have left India with an impressive rail system, the leftover democracy has stifled growth. "The legacy of the British Raj is a heavy-handed civil service," said Schroders' Mr Conway. "The administration system is onerous and means any development applications are beset with delays."

Financial advisers are not convinced that India is for everyone, as it remains at the higher end of the risk spectrum. Mr McDermott said: "In terms of an investment case India shows lots of promise, but there are endemic problems. Given the inherent problems associated with its nascent economic boom I consider this a high-risk investment. I recommend that exposure to the region should be less than 5pc and part of a balanced portfolio."

He suggested the more cautious strategy of getting exposure to India through an emerging market fund such as Allianz BRIC. For investors set on a specialist fund he recommended Fidelity India Focus Fund.

Charlie Nicholls of Investment-advice-online.com backed First State Indian fund or Invesco Perpetual Asia.

"India only has a 20-year economic history, compared to China's 35-year one," said Mr Conway. "In five to 10 years China will slow down and India will consistently grow each year faster than China."

http://www.telegraph.co.uk/finance/personalfinance/investing/8051265/India-is-tipped-to-emerge-from-Chinas-shadow.html

By Emma Wall

Published: 5:21PM BST 08 Oct 2010

2 Comments

If there were a popularity contest for emerging markets, India would struggle to win a medal. As the Commonwealth Games host has had difficulty enticing crowds to the sporting event, so too have investors shunned its economy in favour of India's bigger neighbour, China.

British fund investors have put £4bn more into China than into India, according to Morningstar, the analyst – China has attracted £15bn from UK-registered unit trusts, compared with £11bn for India.

Related Articles

Are British investors missing a trick by shunning Wall St?

Scottish social housing needs investment as safe as 'gilts'

Silver price boosts Hochschild to near all-time high

Super-rich buy gold by the ton

'We are going to have higher prices for commodities'

Emerging markets second wind blows in the face of short-term thinking

But the smart money may do well not to just follow the crowd China may be the current star of the BRIC show, but India could eclipse its neighbour in the not-too-distant future.

"In the last year, the MSCI India index is up by 22pc, whereas China is up by only 5.8pc," said Allan Conway of Schroders. "China may have better short-term prospects, but India is less developed and so has further to grow. Add to this China's prematurely ageing population due to the one-child policy, and I would say on a five-year-plus view that India is the more attractive investment opportunity."

India's economy is expected to grow by about 9pc next year, and although the budget deficit is 4.5pc, very little of this is in foreign currency, making it manageable.

India's past performance has been impressive too. If you had invested £1,000 in J P Morgan's Indian investment trust a decade ago, it would now be worth more than £6,000; had you invested a similar sum in the HSBC GIF Indian Equity unit trust, it would have grown to £7,433.

Short-term performance has also been positive. In the past year First State's Indian Subcontinent fund has returned 39pc and the India Capital Growth investment trust has risen by 58pc.

The past year has been prosperous for India. A new single-party government – India had been governed by coalitions since 1991 – was elected in May 2009 and has focused on corporate governance and tax regulation. It is introducing identity cards, which will be used to tax workers more efficiently and provide income for the state.

"It used to take a year to build the same number of roads that are being constructed in a day," said Pinakin Patel of J P Morgan.

India is a domestic market, supporting its own industry rather than relying heavily on exports like Russia and Brazil. This means that it was less affected by the global economic downturn than some of its emerging market peers, and can offer investors a hedge against a European or American double-dip.

India has a lower dependence on commodities than other emerging markets, contributing just 25pc of the equity market, compared with 36pc in South Africa, 46pc in Brazil and 70pc in Russia. The more diverse market offers more stability instead, mainly being a composite of financials at 30pc and energy, which is 25pc of the market.

Future investment opportunities lie not in big cities such as Mumbai and Delhi, but in smaller centres. Investors will be able to get the growth prospects of a frontier market, but with the stability of a more developed country.

The consumer story is big in these regions. Not only are the growing middle classes buying more goods and eating more meat, but their rise in social status is encouraging more infrastructure to be built and bringing big business to the financials.

"I come from a rural part of India," said Mr Patel. "I know how much people keep under the mattress. But more people are getting bank accounts, mortgages and credit cards – which is why we chose to play the consumer trend more indirectly through the financials." Four of the top five holdings in the J P Morgan investment trust are banks.

The newly launched Insynergy Absolute India fund favours financials too. It is run by India's largest business, Reliance Group, which invests in HDFC Bank. The high savings and investment rate, 37pc of GDP, coupled with the large as yet untapped market make it a good long-term growth holding.

Other sectors touted as opportunities for growth are pharmaceuticals, technology and infrastructure.

As the Commonwealth Games have proved, however, regulation in emerging economies is simply not on a par with the Western world. Fund managers may have puffed infrastructure as an area to invest in, but who wants to invest in the kind of bridges that collapse?

"India remains a very rough diamond," said Darius McDermott of Chelsea Financial Services. "In terms of infrastructure it remains a decade behind China – in many parts of the country roads are truly catastrophic. Energy supply is a perennial problem, as is the supply of skilled workers."

Mr Patel stressed that investors should not confuse publicly funded infrastructure, which is poorly regulated, with privately funded infrastructure. "Privately funded construction has many success stories, such as the Delhi metro," he said. "India is not perfect, but it has an English legal system and a proper accounting system. We chose to work with leading companies with a good track record." The JPM fund holds Larsen & Toubro, which builds power plants, and BHEL, a builder of roads and airports – both with 40-year histories.

While the Empire may have left India with an impressive rail system, the leftover democracy has stifled growth. "The legacy of the British Raj is a heavy-handed civil service," said Schroders' Mr Conway. "The administration system is onerous and means any development applications are beset with delays."

Financial advisers are not convinced that India is for everyone, as it remains at the higher end of the risk spectrum. Mr McDermott said: "In terms of an investment case India shows lots of promise, but there are endemic problems. Given the inherent problems associated with its nascent economic boom I consider this a high-risk investment. I recommend that exposure to the region should be less than 5pc and part of a balanced portfolio."

He suggested the more cautious strategy of getting exposure to India through an emerging market fund such as Allianz BRIC. For investors set on a specialist fund he recommended Fidelity India Focus Fund.

Charlie Nicholls of Investment-advice-online.com backed First State Indian fund or Invesco Perpetual Asia.

"India only has a 20-year economic history, compared to China's 35-year one," said Mr Conway. "In five to 10 years China will slow down and India will consistently grow each year faster than China."

http://www.telegraph.co.uk/finance/personalfinance/investing/8051265/India-is-tipped-to-emerge-from-Chinas-shadow.html

Tuesday 5 October 2010

China calls for more Asian clout in global economy

October 5, 2010 - 7:03AM

The surging economies of Asia should be granted more power in the traditionally Western-dominated global financial institutions, Chinese Premier Wen Jiabao said on Monday at the opening of the Euro-Asian summit.

The start of the two-day 48-nation meeting, set amid the high security and gilded opulence at the Belgian royal palace, underscored the Asian nations’ demands for a rebalancing of international financial structures as they lead the world out of recession.

Premier Wen stressed that Asian leaders expect Europe to relinquish some seats at the International Monetary Fund (IMF), the international lender charged with helping nations that get into currency and financial crises.

‘‘We need to improve the decision-making process and mechanisms of the international financial institutions, increase the representation and voice of developing countries, encourage wider participation,’’ Wen told the other leaders.

The Chinese premier and some other Asian leaders made it clear that Asia would start making its robust economic growth count on the global stage.

Cambodian President Hun Sen stressed the Asian economies should be recognised for leading the global economic recovery.

While demand in the EU (European Union) and US economies was once the driver of growth, it is in decline compared to demand growth in Asia.Even Germany, the economic giant of the European Union, paid tribute.

‘‘We have to thank the Asian upswing for the positive economic development,’’ German Chancellor Angela Merkel said.

Last week, the 27-nation EU said it could give up some of its power base at the IMF to emerging countries, a concession that could cost it two seats on the governing board and the right to have a European heading the Washington DC organisation, which hands out billions of US dollars around the world.

At the moment, EU countries occupy nine of the 24 seats.

‘‘The fact that Europeans show us the flexibility and willingness to negotiate is important,’’ said Rhee Chang-yong, a South Korean delegate.

‘‘For us, the IMF quota reform is very symbolic and very important,’’ he said.

South Korea will organise the Group of 20 (G20) meeting of the world’s major economies next month and expects to have an agreement then.

On Wednesday, there will also be bilateral EU summits with China and South Korea.

Overall, the nations from the two continents represent about half the world’s economic output and 60 per cent of global trade.

But, instead of Europe driving the summits, the emergence of China as a new trading juggernaut has somewhat turned the tables at the biennial meetings.

Last week, the IMF said that Asian and Latin American economies were doing well but prospects for some European countries, including Greece, remain uncertain.

On Wednesday, the EU leaders and South Korean President Lee Myung-bak will sign a free trade pact that will slash billions of dollars in industrial and agricultural duties, despite some nations’ worries that Europe’s auto industry could be hurt by a flood of cheaper cars.

The deal - the first such pact between the EU and an Asian trading partner - will begin on July 1, 2011.

Japan’s Prime Minister Naoto Kan will pursue a free trade agreement in his bilateral meetings with European leaders, said Foreign Ministry spokesman Satoru Satoh.He said Japanese business was ‘‘alarmed’’ by the EU’s deal with Seoul.

Japan feels it will be at a competitive disadvantage with South Korea, which has an agreement with the EU that threatens to take a bite out of Japanese exports, particularly of cars and televisions, he said.

While Japan is anxious for an agreement as soon as possible, he said the Europeans still lack consensus among its 27 members.

Besides the economy, Japan also has an issue with China, as both continue a diplomatic row following the arrest of a Chinese fishing boat captain whose trawler collided with Japanese patrol vessels near disputed islands.

Despite the formal opening, economic discord might also surface at the summit.

AP

http://www.smh.com.au/business/world-business/china-calls-for-more-asian-clout-in-global-economy-20101005-164p5.html

The surging economies of Asia should be granted more power in the traditionally Western-dominated global financial institutions, Chinese Premier Wen Jiabao said on Monday at the opening of the Euro-Asian summit.

The start of the two-day 48-nation meeting, set amid the high security and gilded opulence at the Belgian royal palace, underscored the Asian nations’ demands for a rebalancing of international financial structures as they lead the world out of recession.

Premier Wen stressed that Asian leaders expect Europe to relinquish some seats at the International Monetary Fund (IMF), the international lender charged with helping nations that get into currency and financial crises.

‘‘We need to improve the decision-making process and mechanisms of the international financial institutions, increase the representation and voice of developing countries, encourage wider participation,’’ Wen told the other leaders.

‘‘We must explore ways to establish a more effective global economic governance system.’’

The Chinese premier and some other Asian leaders made it clear that Asia would start making its robust economic growth count on the global stage.

Cambodian President Hun Sen stressed the Asian economies should be recognised for leading the global economic recovery.

While demand in the EU (European Union) and US economies was once the driver of growth, it is in decline compared to demand growth in Asia.Even Germany, the economic giant of the European Union, paid tribute.

‘‘We have to thank the Asian upswing for the positive economic development,’’ German Chancellor Angela Merkel said.

Because of the swing in economic momentum, the battle for seats at the IMF has become a symbolic battle ground.

Last week, the 27-nation EU said it could give up some of its power base at the IMF to emerging countries, a concession that could cost it two seats on the governing board and the right to have a European heading the Washington DC organisation, which hands out billions of US dollars around the world.

At the moment, EU countries occupy nine of the 24 seats.

‘‘The fact that Europeans show us the flexibility and willingness to negotiate is important,’’ said Rhee Chang-yong, a South Korean delegate.

‘‘For us, the IMF quota reform is very symbolic and very important,’’ he said.

South Korea will organise the Group of 20 (G20) meeting of the world’s major economies next month and expects to have an agreement then.

The leaders of 48 nations face potential clashes on market restrictions and trade surpluses.

On Wednesday, there will also be bilateral EU summits with China and South Korea.

Overall, the nations from the two continents represent about half the world’s economic output and 60 per cent of global trade.

But, instead of Europe driving the summits, the emergence of China as a new trading juggernaut has somewhat turned the tables at the biennial meetings.

Last week, the IMF said that Asian and Latin American economies were doing well but prospects for some European countries, including Greece, remain uncertain.

On Wednesday, the EU leaders and South Korean President Lee Myung-bak will sign a free trade pact that will slash billions of dollars in industrial and agricultural duties, despite some nations’ worries that Europe’s auto industry could be hurt by a flood of cheaper cars.

The deal - the first such pact between the EU and an Asian trading partner - will begin on July 1, 2011.

Japan’s Prime Minister Naoto Kan will pursue a free trade agreement in his bilateral meetings with European leaders, said Foreign Ministry spokesman Satoru Satoh.He said Japanese business was ‘‘alarmed’’ by the EU’s deal with Seoul.

Japan feels it will be at a competitive disadvantage with South Korea, which has an agreement with the EU that threatens to take a bite out of Japanese exports, particularly of cars and televisions, he said.

While Japan is anxious for an agreement as soon as possible, he said the Europeans still lack consensus among its 27 members.

Besides the economy, Japan also has an issue with China, as both continue a diplomatic row following the arrest of a Chinese fishing boat captain whose trawler collided with Japanese patrol vessels near disputed islands.

Despite the formal opening, economic discord might also surface at the summit.

Many Western nations have complained that China keeps its currency undervalued to give its exporters an unfair price advantage on international markets while at the same time China closes off its markets, keeping European businesses out.

AP

http://www.smh.com.au/business/world-business/china-calls-for-more-asian-clout-in-global-economy-20101005-164p5.html

Spectre of international trade war looms as recovery proves elusive

October 5, 2010

As world economies continue to falter, central banks are running out of options and the spectre of protectionism grows, writes Larry Elliott.

In all the comparisons between the Great Recession of the past three years and the Great Depression of the 1930s, one comforting thought for policymakers has been that there has been no return to tit-for-tat protectionism, which saw one country after another impose high tariffs to cut the dole queues.

Yet the commitment of governments this time round to keep markets open was based on the belief that recovery would be swift and sustained. If, as many now suspect, the global economy is stuck in a low-growth, high-unemployment rut, the pressures for protectionism will grow.

The former British chancellor Kenneth Clarke summed up the mood when he said in the Observer that it is hard to be ''sunnily optimistic'' about the West's economic prospects.

Despite a colossal stimulus, the recovery has been shortlived and, by historical standards, feeble. The traditional tools - cutting interest rates and spending more public money - were not enough, so have had to be supplemented by the creation of electronic money. In both the US and Britain, policymakers are canvassing the idea that more quantitative easing will be required, even though they well understand its limitations.

There is the sense of finance ministries and central banks running out of options. They cannot cut interest rates any further; there is strong resistance from both markets and voters to further fiscal stimulus, and so far quantitative easing has had a more discernible effect on asset prices than it has on the real economy.

So what is left? The answer is that countries can try to give themselves an edge by manipulating their currencies, or they can go the whole hog and put up trade barriers.

Brazil's Finance Minister, Guido Mantega, warned that an ''international currency war'' has broken out following the recent moves by Japan, South Korea and Taiwan to intervene directly in the foreign exchange markets. China has long been criticised by other nations, the US in particular, for building up massive trade surpluses by holding down the level of its currency, the renminbi.

The currencies under the most upward pressure are the yen and the euro. Why? Because the Chinese have all but pegged the renminbi to a US dollar that has been weakened by the prospect of more quantitative easing over the coming months.

But currency intervention is one thing, full-on protectionism another. The existence of the World Trade Organisation has made it more difficult to indiscriminately slap tariffs on imports. What's more, there is still a strong attachment to the concept of free trade.

The question now is whether the commitment to free trade is as deep as it seems. The round of trade liberalisation talks started in Doha almost nine years ago remain in deep freeze. Attempts to conclude the talks have run into the same problem: trade ministers talk like free traders but they act like mercantilists, seeking to extract the maximum amount of concessions for their exporters while giving away as little as possible in terms of access to their own domestic markets.

The approach taken by countries at the WTO talks also governs their thinking when it comes to steering their countries out of trouble. There are plenty of nations extolling the virtues of export-led growth, but very few keen on boosting their domestic demand so that those exports can find willing buyers.

The global imbalances between those countries running trade surpluses and those running trade deficits are almost as pronounced as they were before the crisis, and are getting wider. This is a recipe for tension, especially between Beijing and Washington.

This tension manifested itself last week when the House of Representatives passed a bill that would allow US companies to apply for duties to be put on imports from countries where the government actively weakened the currency - in other words, China.

The Senate will debate its version of the same bill after the mid-term elections next month, but it was interesting that the House bill was passed by a big majority and with considerable bipartisan support.

China responded swiftly and testily to the developments on Capitol Hill. It argued that the move would contravene WTO rules and quite deliberately tweaked its currency lower.

It is not hard to see why Beijing got the hump. It introduced the biggest fiscal stimulus (in relation to GDP) of any country and helped lift the global economy out of its trough. It can only fulfil its domestic policy goal of alleviating poverty if it can shift large numbers of people out of the fields and into the factories, and that requires a cheap currency. It has been financing the US twin deficits.

Unsurprisingly, then, its message to the Americans was clear: ''It is not smart to get on the wrong side of your bank manager, so do not mess with us.''

What happens next depends to a great extent on whether the global economy can make it through the current soft patch.

Guardian News & Media

http://www.smh.com.au/business/spectre-of-international-trade-war-looms-as-recovery-proves-elusive-20101004-164e1.html

As world economies continue to falter, central banks are running out of options and the spectre of protectionism grows, writes Larry Elliott.

In all the comparisons between the Great Recession of the past three years and the Great Depression of the 1930s, one comforting thought for policymakers has been that there has been no return to tit-for-tat protectionism, which saw one country after another impose high tariffs to cut the dole queues.

Yet the commitment of governments this time round to keep markets open was based on the belief that recovery would be swift and sustained. If, as many now suspect, the global economy is stuck in a low-growth, high-unemployment rut, the pressures for protectionism will grow.

The former British chancellor Kenneth Clarke summed up the mood when he said in the Observer that it is hard to be ''sunnily optimistic'' about the West's economic prospects.

Despite a colossal stimulus, the recovery has been shortlived and, by historical standards, feeble. The traditional tools - cutting interest rates and spending more public money - were not enough, so have had to be supplemented by the creation of electronic money. In both the US and Britain, policymakers are canvassing the idea that more quantitative easing will be required, even though they well understand its limitations.

There is the sense of finance ministries and central banks running out of options. They cannot cut interest rates any further; there is strong resistance from both markets and voters to further fiscal stimulus, and so far quantitative easing has had a more discernible effect on asset prices than it has on the real economy.

So what is left? The answer is that countries can try to give themselves an edge by manipulating their currencies, or they can go the whole hog and put up trade barriers.

Brazil's Finance Minister, Guido Mantega, warned that an ''international currency war'' has broken out following the recent moves by Japan, South Korea and Taiwan to intervene directly in the foreign exchange markets. China has long been criticised by other nations, the US in particular, for building up massive trade surpluses by holding down the level of its currency, the renminbi.

The currencies under the most upward pressure are the yen and the euro. Why? Because the Chinese have all but pegged the renminbi to a US dollar that has been weakened by the prospect of more quantitative easing over the coming months.

The question now is whether the commitment to free trade is as deep as it seems. The round of trade liberalisation talks started in Doha almost nine years ago remain in deep freeze. Attempts to conclude the talks have run into the same problem: trade ministers talk like free traders but they act like mercantilists, seeking to extract the maximum amount of concessions for their exporters while giving away as little as possible in terms of access to their own domestic markets.

The approach taken by countries at the WTO talks also governs their thinking when it comes to steering their countries out of trouble. There are plenty of nations extolling the virtues of export-led growth, but very few keen on boosting their domestic demand so that those exports can find willing buyers.

The global imbalances between those countries running trade surpluses and those running trade deficits are almost as pronounced as they were before the crisis, and are getting wider. This is a recipe for tension, especially between Beijing and Washington.

This tension manifested itself last week when the House of Representatives passed a bill that would allow US companies to apply for duties to be put on imports from countries where the government actively weakened the currency - in other words, China.

The Senate will debate its version of the same bill after the mid-term elections next month, but it was interesting that the House bill was passed by a big majority and with considerable bipartisan support.

China responded swiftly and testily to the developments on Capitol Hill. It argued that the move would contravene WTO rules and quite deliberately tweaked its currency lower.

It is not hard to see why Beijing got the hump. It introduced the biggest fiscal stimulus (in relation to GDP) of any country and helped lift the global economy out of its trough. It can only fulfil its domestic policy goal of alleviating poverty if it can shift large numbers of people out of the fields and into the factories, and that requires a cheap currency. It has been financing the US twin deficits.

Unsurprisingly, then, its message to the Americans was clear: ''It is not smart to get on the wrong side of your bank manager, so do not mess with us.''

What happens next depends to a great extent on whether the global economy can make it through the current soft patch.

But imagine that the next three months see the traditional policy tools becoming increasingly ineffective, that the slowdown intensifies and broadens, and that the Democrats get a pasting in the mid-term elections. In those circumstances, a trade war would be entirely feasible.

Guardian News & Media

http://www.smh.com.au/business/spectre-of-international-trade-war-looms-as-recovery-proves-elusive-20101004-164e1.html

Thursday 16 September 2010

Chinese think tank warns US it will emerge as loser in trade war

A State Council think-tank in China has warned Washington that the US will come off worst in a trade war if it imposes sanctions against Beijing over the two nations' currency spat.

The US is considering legislation to punish Beijing for holding down the yuan Photo: AFP

Ding Yifan, a policy guru at the Development Research Centre, said China could respond by selling holdings of US debt, estimated at over $1.5 trillion (£963bn). This would trigger a rise in US interest rates. His comments at a forum in Beijing follow a string of remarks by Chinese officials questioning US credit-worthiness and the reliability of the dollar.

China's authorities seem split over how to respond to moves on Capitol Hill for legislation to punish Beijing for holding down the yuan. The central bank has ruled out use of its "nuclear weapon", insisting that it would not exploit its $2.45 trillion of foreign reserves for political purposes. "The US Treasury market is a very important market for China," it said.

However, the mood is hardening on both sides of the Pacific. The dispute risks escalating if China's trade surplus with the US climbs further and more US jobs are lost. US Treasury Secretary Tim Geithner, who has taken a softly-softly line in the past, said on Friday that China had done "very little" to correct the undervaluation of the yuan since ending the dollar peg in June.

Mr Ding reflects thinking among some in the Poltiburo, who seem convinced that the US is in decline and that China's rise as an exporter of goods and capital give it the upper hand.

"They are utterly wrong," said Gabriel Stein from Lombard Street Research. "The lesson of the 1930s is that surplus countries with structurally weak domestic demand come off worst in a trade war."

He described the implicit threat to sell Treasuries as "empty bluster" because Beijing's purchase of these bonds is a side-effect of its yuan policy. "Bring it on: it will weaken the dollar, which is what the US wants. The interest rate effect can be countered by the Fed."

"Some Chinese officials seem to believe that buying Treasuries underpins US public spending. In fact China's mercantilist policy is forcing the US to run large deficits against its own interest. China should be terrified of a trade war."

http://www.telegraph.co.uk/finance/currency/8002719/Chinese-think-tank-warns-US-it-will-emerge-as-loser-in-trade-war.html

Mr Ding reflects thinking among some in the Poltiburo, who seem convinced that the US is in decline and that China's rise as an exporter of goods and capital give it the upper hand.

"They are utterly wrong," said Gabriel Stein from Lombard Street Research. "The lesson of the 1930s is that surplus countries with structurally weak domestic demand come off worst in a trade war."

He described the implicit threat to sell Treasuries as "empty bluster" because Beijing's purchase of these bonds is a side-effect of its yuan policy. "Bring it on: it will weaken the dollar, which is what the US wants. The interest rate effect can be countered by the Fed."

"Some Chinese officials seem to believe that buying Treasuries underpins US public spending. In fact China's mercantilist policy is forcing the US to run large deficits against its own interest. China should be terrified of a trade war."

http://www.telegraph.co.uk/finance/currency/8002719/Chinese-think-tank-warns-US-it-will-emerge-as-loser-in-trade-war.html

China – How to prevent a housing bubble

China – How to prevent a housing bubble

Written by Standard Chartered Global Research

Tuesday, 14 September 2010 14:17

Key points

* Wealth management products offer higher rates than standard fixed-term deposit rates

* But real negative rates mean these products do not prevent asset inflation pressure

* We expect house prices to rise more; without rate reform, nationwide housing bubble is likely

KUALA LUMPUR: There is more interest rate freedom in China than meets the eye – but not enough to stop an asset bubble forming, we believe. Real People’s Bank of China (PBoC) base rates are super-low for an economy growing at 8-10% in real terms.

The real 1Y PBoC deposit rate is currently at -1.25% (using current CPI inflation to adjust the nominal rate). In other words, depositing money at the bank costs you money. For corporates, borrowing is super-cheap, at 1% for a one-year loan (using producer price index, or PPI, inflation to deflate the nominal 5.31% rate).

As a result, while the central authorities may occasionally roll out higher down-payment requirements for home purchases or build more low cost housing, we expect a nationwide housing bubble to form in the next few years if interest rates are left where they are.

Officially, banks can offer loans at rates as much as 10% below the loan rate, and at any rate above it; on the deposit side, banks can offer lower rates than the base, but not higher.

However, there is a lot more to interest rates in China than the official rates. For instance, short-term draft financing (via instruments such as banker’s acceptance drafts) is done below the PBoC base loan rate. A reasonably sized corporate can currently obtain a three-month draft at 3.2-4.0%, versus the 4.9% base rate for a three- to six-month loan.

A big, cash-rich company can on lend to a cash-poor company, via a bank, through an entrustment loan structure, and negotiate its own rates – at present, a large multinational can lend to another large multinational, all onshore, at a rate of 3.0-3.5% for up to six months, or at 4.0-4.5% for up to one year, compared with official rates of 4.9% and 5.3%, respectively.

Non-bank financial institutions with large deposits (more than CNY 30mn) can negotiate a higher-than-benchmark rate with their banks – the rate as of end-June was around 4% for a deposit of more than five years (compared with the 3.60% PBoC base rate). And for wealthy retail depositors, China’s banks have offered a feast of wealth management products (WMPs) in recent years which offer higher returns on retail deposits for a bit of extra risk.

We recently reported on the informal banning of one type of WMP – those offered by trust companies via banks.

These products were the packaged results of corporate loans extended by banks or trust companies. As a result, they could offer relatively high interest rates (around 3% on a trust loan in March 2010).

With the removal of these products, what is a wealthy Shanghai depositor to do with all her cash? Are the banks still able to offer enough through other structures to keep real rates above zero?

What can you get for your deposit now?

We asked this question of several branches of shareholding and city commercial banks in Beijing and Shanghai last week.

Smaller shareholding banks are more in need of deposits, since they lack the branch networks of the biggest banks. We wanted to find out which rates and structured deposit products were on offer. We also looked into whether trust products have been taken off the market entirely.

Our key findings:

• Banks are not offering floating deposit rates (as has been suggested in various media reports). PBoC benchmark rates are applied to all fixed-term deposits.

• Only one bank offered anything close to a floating-rate deposit. This small bank, which opened its first branch in Shanghai recently, offers attractive rates on demand deposits, basically paying a fixed-term interest rate for the period the deposit is with them. (In contrast, if you put your money in a standard term account and withdraw it early, you are paid the on-demand interest rate of 0.36%.) This small bank currently offers a 1.19% 1M deposit rate, for example. The downside is that it only has one Shanghai branch so far, so access is limited.

• There is an array of WMPs on offer, some very short-term and low-risk. One salesperson even told us, “Fixed deposits are so out these days!” We found three basic types of WMPs during our visits to the banks:

1. PBoC bill-based products. These are issued each day, the total amount depending on the bank’s asset-liability ratio (or perhaps even the branch’s, given that Beijing and Shanghai branches of the same bank were offering different rates), and are issued on an ad-hoc basis. Products range from 7-day to 1Y, with annualised rates ranging from 2.3% to 3.45%.

2. ‘Residual’ trust products. Most banks warned us that the bank regulator is now prohibiting them from selling trust products (as we reported) and new, stricter regulations are now in place for high-risk wealth products. Most banks we visited were not offering trust loans. In Beijing, though, a couple of banks were still offering trust products which had been launched before the regulator stopped them.

And one bank in Shanghai was selling a bundled quasi-trust product which included a trust loan along with bills, bonds, and FX. This product ranged from 1M to 6M, with annualised rates of 2.5% to 3.2% – well below the rates offered on trust products before the ban in April.

3. Banks marketing others’ WMPs. One major commercial bank in Shanghai was marketing a high-yield WMPs on behalf of a relatively new insurance company. This is a 5Y product with a 12.5% total yield at maturity. It also comes with additional perks: five annual bonuses based on the insurance company’s performance (at least 1.3%, we were told) and an accident insurance policy offering five times the standard cover. One bank in Shanghai was offering a one-off bonus on top of returns for customers who bundle their deposits, equity and fund investments together and entrust them all to the bank’s partner securities broker.

On average, we found that one can expect to receive returns of around 2.6% on a 3M WMP deposit, or 2.9% for a 1Y WMP deposit, compared with the 1.71% and 2.25% PBoC fixed rates, respectively. In other words, although WMPs offer significantly higher rates than standard deposits, given that inflation is running at 3.5% y/y, these rates are still negative in real terms. (The trust companies are still able to market and sell trust products to their VIP clients; rates in July were reported to be around 8.5%.)

Banks’ policies on principal protection seem to vary. In Shanghai, several banks told us specifically that they were no longer able to offer 100% principal protection on WMPs (which suggests that they were previously allowed to). In practice, the bankers we spoke to offered a verbal promise of principal protection. However, in Beijing, a number of city commercial and large commercial banks that we visited still offer 100% principal protection in the contract, as long as the deposit reaches the maturity date.

To conclude, while wealthy depositors have access to better rates on structured deposit WMPs, these rates are still not high enough to eliminate the negative real rate problem. At the same time, the real mortgage rate is low – a first-home buyer will pay about a 4.5% nominal rate (the PBoC benchmark 1Y loan rate discounted by 15%) for a 10-year mortgage.

This works out to 1% in real terms, using CPI inflation to deflate.

This means a property bubble will, over time, spill over in to the Tier 2 and Tier 3 cities. As soon as monetary policy is loosened, whether it is at the end of this year (as we expect) or later, or as soon as the central government signals even the mildest of loosening of housing policy, we worry that house prices will rise again – particularly outside the Tier 1 cities, where prices are already pretty elevated.

Comments from an official at Shenyang People’s Bank (a branch of the PBoC) on the need for interest rate reforms have attracted much interest in recent weeks. His idea is to allow banks to offer higher deposit rates, starting off in north eastern China.

We are unsure how much backing this idea has from the leaders of the PBoC, but the comments highlights a long-running and frustrated ambition of many at the central bank to liberalise rates and raise them to nearer to China’s nominal growth rate. As we have explained in this note, interest rate liberalisation has happened in the nooks and crannies of the market, but the base rate system still dominates, and it is unreformed.

It strikes us that allowing one region of China to raise rates would not be easy, given the ease with which money moves around the country. We also believe that, given the ‘no-change’ macroeconomic stance of the State Council, it would be hard to persuade other ministries of the rationale for raising rates, whatever the medium-term benefits (though, of course,there will never be a ‘good’ time for rate reform).

We believe that this problem needs to be solved if China is to prevent a debilitating asset bubble from forming over the next five years. Before the housing market existed, in the 1980s-1990s, liquidity had no choice but to sit idle in deposit accounts. Now a big housing market does exist, and deposits – even structured deposits – are not priced right.

http://www.theedgemalaysia.com/business-news/173483-china--how-to-prevent-a-housing-bubble.html

Written by Standard Chartered Global Research

Tuesday, 14 September 2010 14:17

Key points

* Wealth management products offer higher rates than standard fixed-term deposit rates

* But real negative rates mean these products do not prevent asset inflation pressure

* We expect house prices to rise more; without rate reform, nationwide housing bubble is likely

KUALA LUMPUR: There is more interest rate freedom in China than meets the eye – but not enough to stop an asset bubble forming, we believe. Real People’s Bank of China (PBoC) base rates are super-low for an economy growing at 8-10% in real terms.

The real 1Y PBoC deposit rate is currently at -1.25% (using current CPI inflation to adjust the nominal rate). In other words, depositing money at the bank costs you money. For corporates, borrowing is super-cheap, at 1% for a one-year loan (using producer price index, or PPI, inflation to deflate the nominal 5.31% rate).

As a result, while the central authorities may occasionally roll out higher down-payment requirements for home purchases or build more low cost housing, we expect a nationwide housing bubble to form in the next few years if interest rates are left where they are.

Officially, banks can offer loans at rates as much as 10% below the loan rate, and at any rate above it; on the deposit side, banks can offer lower rates than the base, but not higher.

However, there is a lot more to interest rates in China than the official rates. For instance, short-term draft financing (via instruments such as banker’s acceptance drafts) is done below the PBoC base loan rate. A reasonably sized corporate can currently obtain a three-month draft at 3.2-4.0%, versus the 4.9% base rate for a three- to six-month loan.

A big, cash-rich company can on lend to a cash-poor company, via a bank, through an entrustment loan structure, and negotiate its own rates – at present, a large multinational can lend to another large multinational, all onshore, at a rate of 3.0-3.5% for up to six months, or at 4.0-4.5% for up to one year, compared with official rates of 4.9% and 5.3%, respectively.

Non-bank financial institutions with large deposits (more than CNY 30mn) can negotiate a higher-than-benchmark rate with their banks – the rate as of end-June was around 4% for a deposit of more than five years (compared with the 3.60% PBoC base rate). And for wealthy retail depositors, China’s banks have offered a feast of wealth management products (WMPs) in recent years which offer higher returns on retail deposits for a bit of extra risk.

We recently reported on the informal banning of one type of WMP – those offered by trust companies via banks.

These products were the packaged results of corporate loans extended by banks or trust companies. As a result, they could offer relatively high interest rates (around 3% on a trust loan in March 2010).

With the removal of these products, what is a wealthy Shanghai depositor to do with all her cash? Are the banks still able to offer enough through other structures to keep real rates above zero?

What can you get for your deposit now?

We asked this question of several branches of shareholding and city commercial banks in Beijing and Shanghai last week.

Smaller shareholding banks are more in need of deposits, since they lack the branch networks of the biggest banks. We wanted to find out which rates and structured deposit products were on offer. We also looked into whether trust products have been taken off the market entirely.

Our key findings:

• Banks are not offering floating deposit rates (as has been suggested in various media reports). PBoC benchmark rates are applied to all fixed-term deposits.

• Only one bank offered anything close to a floating-rate deposit. This small bank, which opened its first branch in Shanghai recently, offers attractive rates on demand deposits, basically paying a fixed-term interest rate for the period the deposit is with them. (In contrast, if you put your money in a standard term account and withdraw it early, you are paid the on-demand interest rate of 0.36%.) This small bank currently offers a 1.19% 1M deposit rate, for example. The downside is that it only has one Shanghai branch so far, so access is limited.

• There is an array of WMPs on offer, some very short-term and low-risk. One salesperson even told us, “Fixed deposits are so out these days!” We found three basic types of WMPs during our visits to the banks:

1. PBoC bill-based products. These are issued each day, the total amount depending on the bank’s asset-liability ratio (or perhaps even the branch’s, given that Beijing and Shanghai branches of the same bank were offering different rates), and are issued on an ad-hoc basis. Products range from 7-day to 1Y, with annualised rates ranging from 2.3% to 3.45%.

2. ‘Residual’ trust products. Most banks warned us that the bank regulator is now prohibiting them from selling trust products (as we reported) and new, stricter regulations are now in place for high-risk wealth products. Most banks we visited were not offering trust loans. In Beijing, though, a couple of banks were still offering trust products which had been launched before the regulator stopped them.

And one bank in Shanghai was selling a bundled quasi-trust product which included a trust loan along with bills, bonds, and FX. This product ranged from 1M to 6M, with annualised rates of 2.5% to 3.2% – well below the rates offered on trust products before the ban in April.

3. Banks marketing others’ WMPs. One major commercial bank in Shanghai was marketing a high-yield WMPs on behalf of a relatively new insurance company. This is a 5Y product with a 12.5% total yield at maturity. It also comes with additional perks: five annual bonuses based on the insurance company’s performance (at least 1.3%, we were told) and an accident insurance policy offering five times the standard cover. One bank in Shanghai was offering a one-off bonus on top of returns for customers who bundle their deposits, equity and fund investments together and entrust them all to the bank’s partner securities broker.

On average, we found that one can expect to receive returns of around 2.6% on a 3M WMP deposit, or 2.9% for a 1Y WMP deposit, compared with the 1.71% and 2.25% PBoC fixed rates, respectively. In other words, although WMPs offer significantly higher rates than standard deposits, given that inflation is running at 3.5% y/y, these rates are still negative in real terms. (The trust companies are still able to market and sell trust products to their VIP clients; rates in July were reported to be around 8.5%.)

Banks’ policies on principal protection seem to vary. In Shanghai, several banks told us specifically that they were no longer able to offer 100% principal protection on WMPs (which suggests that they were previously allowed to). In practice, the bankers we spoke to offered a verbal promise of principal protection. However, in Beijing, a number of city commercial and large commercial banks that we visited still offer 100% principal protection in the contract, as long as the deposit reaches the maturity date.

Freeing up deposit rates is necessary to prevent a housing bubble

To conclude, while wealthy depositors have access to better rates on structured deposit WMPs, these rates are still not high enough to eliminate the negative real rate problem. At the same time, the real mortgage rate is low – a first-home buyer will pay about a 4.5% nominal rate (the PBoC benchmark 1Y loan rate discounted by 15%) for a 10-year mortgage.

This works out to 1% in real terms, using CPI inflation to deflate.

This means a property bubble will, over time, spill over in to the Tier 2 and Tier 3 cities. As soon as monetary policy is loosened, whether it is at the end of this year (as we expect) or later, or as soon as the central government signals even the mildest of loosening of housing policy, we worry that house prices will rise again – particularly outside the Tier 1 cities, where prices are already pretty elevated.

Comments from an official at Shenyang People’s Bank (a branch of the PBoC) on the need for interest rate reforms have attracted much interest in recent weeks. His idea is to allow banks to offer higher deposit rates, starting off in north eastern China.

We are unsure how much backing this idea has from the leaders of the PBoC, but the comments highlights a long-running and frustrated ambition of many at the central bank to liberalise rates and raise them to nearer to China’s nominal growth rate. As we have explained in this note, interest rate liberalisation has happened in the nooks and crannies of the market, but the base rate system still dominates, and it is unreformed.