Below we look at where the smart money has gone in recent years, and assess each area's chances of outperforming in the decade ahead.

GOLD

This has been the star performer of the decade, rising in value by 606pc since the stock market peaked in 1999. Those canny enough to have bought a few gold bars as the stock market started to slip in 2000 are now sitting on substantial gains.

Other metals, such as copper, silver and platinum, have also risen in value, as have oil and agricultural commodities such as corn and coffee. Not surprisingly, funds that invest in gold and commodities have seen even more stellar gains: BlackRock Gold & General has risen by 768pc over the past 10 years, while JP Morgan Natural Resources is 610pc higher.

As long as equity markets remain in turmoil the price of gold is likely to remain high – but most experts warn that at some point there will be a sharp correction. Commodity prices, though, continue to be fuelled by demand from rapidly industrialising emerging markets, in particular China, India, Brazil and Russia.

EMERGING MARKETS

In times of market volatility share price falls can be more dramatic in these emerging economies. Over the "lost decade", though, investors have seen a positive return on their money – although much will depend of course on where and when you were invested.

Since the end of 1999 the MSCI Emerging Markets index has delivered a total return of 163pc, compared with a FTSE 100 return of just 6.72pc (this is positive only because of dividend payments) and a return of 4.78pc from the MSCI World index.

However, many funds investing in this area have done far better than the index. Henderson China Opportunities has risen by 313pc over the period. First State Global Emerging Markets, managed for most of the period by Angus Tulloch, is up by 320pc over the past 10 years, while the Indian Nifty index (its 50 biggest companies) has grown by 551pc over the past decade.

Given the demographics of the region and its potential for growth, most experts agree that it has the potential to deliver returns in future. However, markets can be volatile, so investors are often warned to bank gains after periods of strong growth, perhaps using profits to invest in other undervalued assets.

PROPERTY

Given that house prices are on the slide again, property might not feel like a particularly robust investment. But the figures show that over the past decade it has remained one of the top performing assets. Based on the Halifax Property Price Index, home owners have seen a return of 101pc on bricks and mortar since the end of 1999.

Of course there will be huge regional variations within these figures – and the vast majority of us borrow to buy our homes, so clearly have interest charges to factor in to any notional "return". And we still do need a roof over our heads: it's not as if we can cash it all in and go and live in an Isa. However, this doesn't detract from the fact that when it comes to long-term saving and retirement planning people shouldn't overlook their property.

FUNDS

Even though the UK stock market has not regained its previous highs, this doesn't mean that funds investing in British shares haven't made money over this period. Dividend income remains an important part of the total return on pensions and Isas. In addition, most fund managers won't slavishly follow an index but will be looking to invest in companies whose share price will rise faster than peers in a rising market, but won't fall like a stone when things head south.

Special situation funds, for example, try to find undervalued companies with the potential to deliver gains and good managers in this sector are among the top performers. Marlborough Special Situations has delivered a 289pc return over 10 years; Fidelity Special Situations has returned 101pc.

Another notable success story has been Neil Woodford's Invesco Perpetual High Income fund, one of the biggest and most popular unit trusts. This defensive fund, which concentrates on stocks that have the potential to deliver a rising dividend stream as well as capital growth, has returned 120pc over the past 10 years – hardly a lost decade for the thousands of private investors who have entrusted their long-term savings to this fund manager.

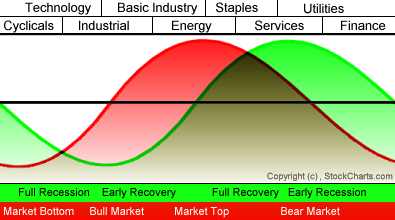

states that different sectors are stronger at different points along the business cycle. The table below describes this theoretical model throughout the business cycle.

states that different sectors are stronger at different points along the business cycle. The table below describes this theoretical model throughout the business cycle.

2 Comments

2 Comments