No changes in GDP growth upgrade following plunging oil prices: Merrill Lynch

BY - 23 JANUARY 2015 @ 11:25 PM

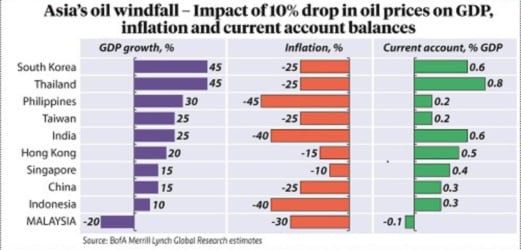

KUALA LUMPUR: Lower oil prices have yet to result in any sizeable goss domestic product (GDP) growth upgrade for emerging Asia, partly because of slowing global growth outside the US, said Bank of America Merrill Lynch.

“Lower oil prices have, however, improved the trade surplus significantly, supporting the current account balance and forex reserves positions.”

The research house said lower oil prices have also resulted in a sharp drop in inflation, particularly in Thailand, Philippines and India, which has allowed central banks to stay accommodative.

The Reserve Bank of India cut policy rates last week as inflation pressures and expectations fell sharply, while markets are starting to price in possible cuts in Thailand and South Korea.

“Emerging Asian countries will likely see a boost to GDP growth in the range of 10 basis points to 45 basis points with every 10 per cent fall in oil prices, if the oil price drop was purely a supply shock.”

Big beneficiaries are consumers as fuel prices at the pump fall, it said.

Savings from reduced fuel costs could be channeled to investments, which for example, is showing in Indonesia's government doubling of capital spending.

”Malaysia, is however an exception and will see overall GDP growth slow with lower oil, given its heavy reliance on oil & gas revenues.”

The government downgraded the growth outlook and raised its fiscal deficit projections this week.

“We remain cautious on the fiscal and current account outlook, given the heavy fiscal dependence on oil and downward trajectory of LNG prices in the coming months.”

The research house has downgraded the average oil price to US$52 for 2015, with oil prices likely to spiral to US$31 per barrel at the end of the first quarter before recovering.

“Asia’s oil windfall will likely see a significant shift in the relative positions of sovereign wealth funds. Oil and gas-related sovereign wealth funds (US$4.3 trillion) – which account for about 60 per cent of total sovereign wealth funds -- will likely see their size stagnate or erode on falling oil prices.”

Falling oil prices will likely dampen the overall growth of sovereign funds, as a large proportion is oil-related.

Norway's government pension fund (US$893 billion), Abu Dhabi Investment Authority (US$773 billion) and Saudi Arabia's SAMA (US$753 billion) are the three largest sovereign funds in the world, and are all oil-related.

“Recycling of Asia-dollars might partly replace the recycling of petrodollars.”

Asian sovereign wealth funds (US$2.8 trillion) account for about 39 per cent of total sovereign wealth funds, and will likely see their size increase at a faster clip.

Sovereign wealth funds of China (CIC & SAFE), Hong Kong (HKMA), Singapore (GIC & Temasek) and Korea (KIC) rank in the Top-15 globally.

http://www.nst.com.my/node/70742