Market Fluctuations

Fluctuations of Common Stock Prices

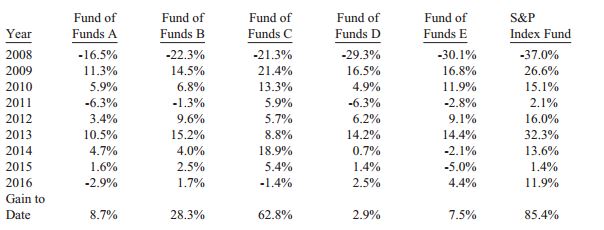

Since common stocks are subject to wide price swings, the investor should seek to profit from these opportunities. However, attempting to time the market usually ends in unsatisfactory results. Graham believes that market timing is pure speculation and is not an investing activity. The best an investor can do is the change the bond and stock proportions in his portfolio after major market swings.

Formulas do not work, although they have been in vogue since the 1950s. When the market reached new highs in the mid-1950s, many formula investors sold their equities according to formula only to witness the market grow increasingly higher. Any approach to the market that is easily described is sure to fail (except for Graham’s method).

The investor also can focus on the price of a security. Graham recommends this practice. Short-term fluctuations should not matter. Over a period of 5 years, the investor should not be surprised if the average value of his portfolio increases more than 50% from its low point or decreases 1/3 from its high point.

Market advances and declines tempt investors to make foolish decisions. Varying the proportion of stocks and bonds between the 25%-75% ratio occupies an investor’s time during turbulent markets and prevents him from making gross errors in judgement. The true investor takes comfort that his actions are opposite from the actions of the crowd.

The better a firm’s record and its prospects, the less relationship that its price will have to its book value. The more successful the company, the more likely its share price is to fluctuate. More often than not, a fast growing firm’s market price will exceed its intrinsic value. So, the better the quality of the stock, the more speculative it will be. This explains the erratic price behavior of some of the most successful and impressive enterprises, such as IBM and Xerox.

The investor should purchase issues close to their tangible asset values and at no more than 33% above that figure. These purchases logically are related to a company’s balance sheet and not to its earnings. Any premium over book value may be thought of as a fee for liquidity that accompanies any publicly traded stock.

Just because a stock sells at or below its net asset value does not warrant that it is a sound purchase. In addition to below market values, the investor also must demand a strong financial position, a satisfactory p/e ratio, and an assurance that the firm’s earnings will be sustained over the years. This is not an entirely difficult bill to fill except under dangerously high market conditions. At the end of 1970 more than half of the DJIA met these investment criteria. However, the investor will forgo the most brilliant, high growth prospects.

With a portfolio purchased at close to book value, the investor can take a more detached view of market fluctuations. In fact, so long as the earning power of the portfolio remains satisfactory, the investor can use these market vagaries to buy low and sell high.

As seen with the stock fluctuations of A & P over many years, the market often goes wrong. Although the stock market may fall, a true investor is rarely forced to sell his shares. Rather, the investor is free to disregard the market quotes. Thus, the investor who allows himself to be unduly worried about the market transforms his basic advantage into a disadvantage. In fact, the investor who owns common stock owns a piece of these companies as a private owner would, and a private owner would not sell his business when it is undervalued by the market. A quoted stock provides an option for the investor to sell at a given price and nothing more. The investor with a diversified portfolio of good stocks should neither worry about sizeable declines nor become excited about sizeable advances. An investor never should sell a stock just because it has gone down or purchase it because it has gone up.

Graham provides the parable of “Mr. Market”, who like the stock market, quotes you a price for your shares each and every day. Mr. Market will either buy your shares or sell you his. The price will depend upon Mr. Market’s mood. You can ignore his efforts, or you can take advantage of him when he quotes you a price that you believe is priced advantageously. Finally, one should not forget the effect of management on a firm’s results. Good management produces acceptable results and bad management does not.

Fluctuation of Bond Prices

Short-term bonds, defined as those with a duration of less than 7 years, are not significantly affected by changes in the market. This applies to US Savings Bonds, which can be redeemed at anytime. Long term bonds, however, may experience wide price swings as a result of fluctuations in the interest rate. Thus, long term bonds may seem attractive when discounted, but this practice often leads to speculation and losses.

Low yields correspond with high bond prices and vice versa; prices and yields are inversely related. The period from 1960 to 1975 is marked by reversing swings in the price of bonds so much so that it reminded Graham of Newton’s law: “every action has an opposite and equal reaction.” Of course, nothing on Wall Street actually occurs the same way twice.

Graham acknowledges the impossibility of attempting to predict bond prices, even if common stock prices were predictable. Therefore, the investor must choose between long- term and short-term bonds chiefly on the basis of personal preference. If the investor wishes to ensure that his market values will not decrease, then the investor is best served by US Savings Bonds. With higher yield long term bonds, the investor must be prepared to see their market values fluctuate.

Convertible issues should be avoided. Their prices fluctuate widely and unpredictably based upon the price of the underlying common stock, the credit standing of the firm, and the market interest rate. Because convertible issues experience huge swings in market value, they are largely speculative investments.