Following are the three most important questions to answer about the stock market:

Is the Stock Market too expensive?

Is the Fed (government) in the way?

Is the Market going up?

The answers to these questions cover nearly all of the bases that affect the markets.

http://books.google.com/books?id=aydxD_IkJBMC&pg=PA65&lpg=PA65&dq=understanding+stock+market+conditions&source=bl&ots=9Q0jwhuGQj&sig=6XdEIyPTZUFI-v1kOHQXKFyF460&hl=en&ei=2MGtSuyINtSBkQX618CVBg&sa=X&oi=book_result&ct=result&resnum=8#v=onepage&q=understanding%20stock%20market%20conditions&f=false

Safe Strategies for Financial Freedom

By Van K. Tharp, Doyle Rayburn Barton, Steve Sjuggerud

Monday, 14 September 2009

Stock Market Sectors Classification

Stock Market Sectors Classification

There are many ways in which stocks can be classified. One of the most preferred ones is by the sector in which the particular business that issues the stocks falls. This classification, which includes the grouping together of companies from the same sector, is done for the purposes of facilitating comparisons between the companies' stocks.

However, many classifications by sectors can be found. One of them divides the market into eleven sectors, where two of them are referred to as defensive, whereas the other nine are referred to as cyclical.

Let's now turn our attention to these two classifications and examine them at a closer look.

Cyclical Stocks

Stocks from the cyclical classification tend to be sensitive to the market conditions, especially to its cycles, as their name implies. The good news is that if one sector is down, another sector may experience an upward trend.

This classification includes nine of the sectors that fall in the sector division. They are as follows:

1.Capital Goods

2.Energy

3.Technology

4.Health care

5.Communications

6.Transportation

7.Basic materials

8.Consumer cyclical

9.Financial

As it can be seen from the list above, investors will not find any difficulty in recognizing whether a particular business belongs to one cyclical sector or another.

Defensive Stocks

This classification includes two of the sectors that fall in the sector division. They are as follows:

1.Utilities

2.Consumer staples

These sectors are less susceptible to market cycles since no matter what the market conditions are people will not stop consume food or electricity. Stocks from these sectors are used as a balancing and protection mechanism by many investors in their portfolios in case the market starts to go down.

However, the advantage of defensive stocks can be their drawback as well. This is so, since no matter what the conditions of the market are people will probably not start to consume more energy or food, so when the market is up, the prices of defensive stocks may not go up as well.

Stock Sectors Purpose

The main purpose of stocks sectors is to facilitate investors' comparison of different stocks. Moreover, comparison of stocks within a particular sector can be very useful if you want to see how your sectors are performing relative to stocks within the same sector.

However, try to use the classifications of various sources, since different sources use different set of sectors.

Final Piece of Advice

Use stock sectors to make effective and reliable comparisons between your stocks and the other from the same sector. This is recommended in order to see whether there are any drastic differences in the performance and if there are such to regulate the disparities.

For knowledge we can highly recommend you subscribe to the The Wall Street Journal.

http://www.stock-market-investors.com/stock-investing-basics/stock-market-sectors-classification.html

There are many ways in which stocks can be classified. One of the most preferred ones is by the sector in which the particular business that issues the stocks falls. This classification, which includes the grouping together of companies from the same sector, is done for the purposes of facilitating comparisons between the companies' stocks.

However, many classifications by sectors can be found. One of them divides the market into eleven sectors, where two of them are referred to as defensive, whereas the other nine are referred to as cyclical.

Let's now turn our attention to these two classifications and examine them at a closer look.

Cyclical Stocks

Stocks from the cyclical classification tend to be sensitive to the market conditions, especially to its cycles, as their name implies. The good news is that if one sector is down, another sector may experience an upward trend.

This classification includes nine of the sectors that fall in the sector division. They are as follows:

1.Capital Goods

2.Energy

3.Technology

4.Health care

5.Communications

6.Transportation

7.Basic materials

8.Consumer cyclical

9.Financial

As it can be seen from the list above, investors will not find any difficulty in recognizing whether a particular business belongs to one cyclical sector or another.

Defensive Stocks

This classification includes two of the sectors that fall in the sector division. They are as follows:

1.Utilities

2.Consumer staples

These sectors are less susceptible to market cycles since no matter what the market conditions are people will not stop consume food or electricity. Stocks from these sectors are used as a balancing and protection mechanism by many investors in their portfolios in case the market starts to go down.

However, the advantage of defensive stocks can be their drawback as well. This is so, since no matter what the conditions of the market are people will probably not start to consume more energy or food, so when the market is up, the prices of defensive stocks may not go up as well.

Stock Sectors Purpose

The main purpose of stocks sectors is to facilitate investors' comparison of different stocks. Moreover, comparison of stocks within a particular sector can be very useful if you want to see how your sectors are performing relative to stocks within the same sector.

However, try to use the classifications of various sources, since different sources use different set of sectors.

Final Piece of Advice

Use stock sectors to make effective and reliable comparisons between your stocks and the other from the same sector. This is recommended in order to see whether there are any drastic differences in the performance and if there are such to regulate the disparities.

For knowledge we can highly recommend you subscribe to the The Wall Street Journal.

http://www.stock-market-investors.com/stock-investing-basics/stock-market-sectors-classification.html

Find a Stock Investing Strategy that Works for You

Find a Stock Investing Strategy that Works for You

By Ken Little, About.com

Investing in stocks can be as simple or as complicated as you want to make it. The important part of that sentence is the personal pronoun “you.”

Too often investors are led to believe that investing in stocks must be a complicated, deeply analytical process involving hours of pouring over financial statements, analysts’ reports, spreadsheets and market analysis before making a decision.

For some investors, this is the only way they feel comfortable investing and they enjoy the digging for information as much as the actual return on investing.

What Works

The complicated analytical approach to investing works for them, but that doesn’t mean it is the only way to successful investing or that it works for every investor.

You may not have the time or educational background to do the complicated financial analysis of every stock you make buy. Does that mean you will be less successful?

Not necessarily, some investors who do tons of research still get it wrong. Still, what can you do to improve your chances for investing success if you aren’t the analytical type and don’t have a lot of time to devote to research?

•Keep the number of targets small. Set your parameters tight to limit your universe. For example, say you’re interested in the health care industry. Pick out a sector in that industry and focus on the leaders (market leaders, not price leaders).

•If your objective is growth, invest in growth industries. This may seem obvious, but it is easy for investors to get side tracked. You will probably do better with a so-so company in a growth industry than a great company in an industry that’s going nowhere. If you want growth, invest in technology or one of the other growth industries and don’t waste your time on utilities alone.

•Invest in market leader wherever you find them if they are overpriced. Market leaders are companies that dominate their corner of the industry and the ones you are looking for are so entrenched it will be hard to dislodge them. Microsoft is the obvious example of a market leader. I’m not suggesting investing in Microsoft, that’s your decision, but they are in no danger of losing their position of market dominance. Of course, you would have said the same thing about GM 10 or 15 years ago.

Conclusion

The point is that you should find an investing strategy that works for you. If it is complicated and data heavy or simple and more intuitive, make it yours and don’t be bullied into adopting another’s strategy.

By Ken Little, About.com

Investing in stocks can be as simple or as complicated as you want to make it. The important part of that sentence is the personal pronoun “you.”

Too often investors are led to believe that investing in stocks must be a complicated, deeply analytical process involving hours of pouring over financial statements, analysts’ reports, spreadsheets and market analysis before making a decision.

For some investors, this is the only way they feel comfortable investing and they enjoy the digging for information as much as the actual return on investing.

What Works

The complicated analytical approach to investing works for them, but that doesn’t mean it is the only way to successful investing or that it works for every investor.

You may not have the time or educational background to do the complicated financial analysis of every stock you make buy. Does that mean you will be less successful?

Not necessarily, some investors who do tons of research still get it wrong. Still, what can you do to improve your chances for investing success if you aren’t the analytical type and don’t have a lot of time to devote to research?

•Keep the number of targets small. Set your parameters tight to limit your universe. For example, say you’re interested in the health care industry. Pick out a sector in that industry and focus on the leaders (market leaders, not price leaders).

•If your objective is growth, invest in growth industries. This may seem obvious, but it is easy for investors to get side tracked. You will probably do better with a so-so company in a growth industry than a great company in an industry that’s going nowhere. If you want growth, invest in technology or one of the other growth industries and don’t waste your time on utilities alone.

•Invest in market leader wherever you find them if they are overpriced. Market leaders are companies that dominate their corner of the industry and the ones you are looking for are so entrenched it will be hard to dislodge them. Microsoft is the obvious example of a market leader. I’m not suggesting investing in Microsoft, that’s your decision, but they are in no danger of losing their position of market dominance. Of course, you would have said the same thing about GM 10 or 15 years ago.

Conclusion

The point is that you should find an investing strategy that works for you. If it is complicated and data heavy or simple and more intuitive, make it yours and don’t be bullied into adopting another’s strategy.

Normal Stock Guidance Doesn’t Apply

Normal Stock Guidance Doesn’t Apply

Extreme Conditions May Distort Normal Market Evaluations

By Ken Little, About.com

In a normal market, I would (and have) advised that investors look for bargains in stocks that have fallen into the value category.

A value stock is one that has been under-priced by the market. Value investors look for these stocks and buy them at a discount to their intrinsic value.

When the market corrects the price of the stock - meaning others have discovered this under-priced gem and are buying the shares - the value investor pockets a nice profit.

One of the keys to this strategy is the phrase “normal market.”

The market of late is anything but normal, in case you hadn’t noticed.

If you are confused about what to do in this market, don’t feel like you’re alone.

Experts are confused and frustrated by market conditions that don’t fit the typical models.

With large swings from low to high and back again, the long-term investor may be better off doing nothing.

If you are invested in good companies, you are probably better off sitting tight and waiting for the current crisis to work its way out.

This is not a rule, but a suggestion. If you are so concerned about your investments that you can’t sleep, then take whatever steps you need to protect you mental and emotional health.

No one can tell you with certainty what is the proper course of action.

Normal markets will return one day, but there is no way to know how long that will take.

In the meantime, if you spot a good buy in a stock, consider whether you are willing to hold it through more turbulent times that are surely to come.

http://stocks.about.com/od/evaluatingstocks/a/092208Marrisk.htm

Extreme Conditions May Distort Normal Market Evaluations

By Ken Little, About.com

In a normal market, I would (and have) advised that investors look for bargains in stocks that have fallen into the value category.

A value stock is one that has been under-priced by the market. Value investors look for these stocks and buy them at a discount to their intrinsic value.

When the market corrects the price of the stock - meaning others have discovered this under-priced gem and are buying the shares - the value investor pockets a nice profit.

One of the keys to this strategy is the phrase “normal market.”

The market of late is anything but normal, in case you hadn’t noticed.

If you are confused about what to do in this market, don’t feel like you’re alone.

Experts are confused and frustrated by market conditions that don’t fit the typical models.

With large swings from low to high and back again, the long-term investor may be better off doing nothing.

If you are invested in good companies, you are probably better off sitting tight and waiting for the current crisis to work its way out.

This is not a rule, but a suggestion. If you are so concerned about your investments that you can’t sleep, then take whatever steps you need to protect you mental and emotional health.

No one can tell you with certainty what is the proper course of action.

Normal markets will return one day, but there is no way to know how long that will take.

In the meantime, if you spot a good buy in a stock, consider whether you are willing to hold it through more turbulent times that are surely to come.

http://stocks.about.com/od/evaluatingstocks/a/092208Marrisk.htm

How to Boost Your Earning Power in a Recession

How to Boost Your Earning Power in a Recession

While some people see the current economic recession as a time of worry, a small but growing group is actually taking advantage of current conditions to boost their long term earnings power.

These people are using the slowdown and the resulting changes in government and corporate priorities to ensure that they are better positioned than the competition to get and keep the best jobs in the coming years.

And they are doing it by getting an online degree.

Experts have long known that the higher the level of your degree the more you will earn throughout your life. In fact, compared to a high school degree, an employee with:

an associate degree will earn an average of $5,600 more per year

a bachelor's degree will earn an average of $21,100 more per year

a master's degrees will earn an average of $33,900 more per year

Why now?

What is it about our current economic climate that makes the right degree so much more important and, above all, achievable:

Firstly, the recession has made companies' future profits very uncertain. As a result they are being far more selective in whom they hire. Today, having a relevant degree on your resume often means the difference between being considered for a position and being passed over completely.

Secondly, the economy is changing. Traditional industries are fading, while new industries such as health care, information services, and homeland security are growing. These generally pay well, but require workers with specific technical skills. These skills are typically not learned in standard 4 year degrees, but can easily be obtained through shorter associate degrees in specific vocational fields.

Thirdly, the rapid expansion of high speed Internet has made it possible for universities to offer online degrees that are highly respected by employers. This makes it far easier for people that are currently employed, or have family responsibilities to obtain their degree.

Lastly, as a result of the recession, the government has stepped in to help subsidize individuals' efforts to return to school to get better trained - and these subsidies are available for online education degrees as well.

Where to start?

If you're interested in maximizing your value to employers and your earnings power, the first thing to do is identify the best degree based on your preferences, job experience, and education. Next, determine which schools offer the right courses. Then investigate financing options that can help pay for all or some of the degree.

Fortunately, there are some great free online services that will quickly help you navigate through available options and find the programs that are exactly right for you.

One of the best is a service called BuildACareer.net. They work with dozens of universities offering associate, bachelor's and master's degrees along with financial aid.

If you want to be one of those people that comes out of this recession in a stronger position, BuildACareer.net may be the place to start.

http://howlifeworks.com/career/boost_earnings/?cid=8088kf_finance_rm

While some people see the current economic recession as a time of worry, a small but growing group is actually taking advantage of current conditions to boost their long term earnings power.

These people are using the slowdown and the resulting changes in government and corporate priorities to ensure that they are better positioned than the competition to get and keep the best jobs in the coming years.

And they are doing it by getting an online degree.

Experts have long known that the higher the level of your degree the more you will earn throughout your life. In fact, compared to a high school degree, an employee with:

an associate degree will earn an average of $5,600 more per year

a bachelor's degree will earn an average of $21,100 more per year

a master's degrees will earn an average of $33,900 more per year

Why now?

What is it about our current economic climate that makes the right degree so much more important and, above all, achievable:

Firstly, the recession has made companies' future profits very uncertain. As a result they are being far more selective in whom they hire. Today, having a relevant degree on your resume often means the difference between being considered for a position and being passed over completely.

Secondly, the economy is changing. Traditional industries are fading, while new industries such as health care, information services, and homeland security are growing. These generally pay well, but require workers with specific technical skills. These skills are typically not learned in standard 4 year degrees, but can easily be obtained through shorter associate degrees in specific vocational fields.

Thirdly, the rapid expansion of high speed Internet has made it possible for universities to offer online degrees that are highly respected by employers. This makes it far easier for people that are currently employed, or have family responsibilities to obtain their degree.

Lastly, as a result of the recession, the government has stepped in to help subsidize individuals' efforts to return to school to get better trained - and these subsidies are available for online education degrees as well.

Where to start?

If you're interested in maximizing your value to employers and your earnings power, the first thing to do is identify the best degree based on your preferences, job experience, and education. Next, determine which schools offer the right courses. Then investigate financing options that can help pay for all or some of the degree.

Fortunately, there are some great free online services that will quickly help you navigate through available options and find the programs that are exactly right for you.

One of the best is a service called BuildACareer.net. They work with dozens of universities offering associate, bachelor's and master's degrees along with financial aid.

If you want to be one of those people that comes out of this recession in a stronger position, BuildACareer.net may be the place to start.

http://howlifeworks.com/career/boost_earnings/?cid=8088kf_finance_rm

The Buy and Hold Strategy And Your Long Term Investment Horizon

The consequences of the buy and hold investment strategy.

http://www.thedigeratilife.com/blog/index.php/2009/03/20/buy-and-hold-strategy-long-term-investment-horizon/

http://www.thedigeratilife.com/blog/index.php/2009/03/20/buy-and-hold-strategy-long-term-investment-horizon/

My Long Term Experience With An Investment Newsletter

My Long Term Experience With An Investment Newsletter

by Silicon Valley Blogger on November 12, 2007

http://www.thedigeratilife.com/blog/index.php/2007/11/12/my-long-term-experience-with-an-investment-newsletter/

by Silicon Valley Blogger on November 12, 2007

http://www.thedigeratilife.com/blog/index.php/2007/11/12/my-long-term-experience-with-an-investment-newsletter/

Bullish Trends and Significant Corrections

- Bullish Trends and Significant Corrections

June 19, 2009 - Non-Client Version

We were recently asked by a client, "If you see signs of a possible new bull market, why are we still sitting on so much cash?" It can be answered by using a fence analogy. We have been taking some smaller positions while maintaining a relatively high cash position in order to play both sides of the fence:

The Far Side Of The Fence: If stocks move lower,

- Our smaller positions reduce risk during a correction, and we have cash on hand to invest during/after a correction. If the bear market resumes (anything is possible), we have less exposure to losses with some cash on hand.

- Numerous asset classes have had significant moves off the March 2009 lows.

- Even markets which have a positive trend, correct from time to time.

- Corrections, within the context of an uptrend, can be significant.

- If a correction is orderly, we can use cash to enter markets at lower levels.

- If the correction is not orderly and a resumption of the bear looks more likely, cash and smaller positions enable us to better manage risk. If your investments lose 12%, but you have 50% of your account in cash, the loss to your account is 6%.

- As our strategy dictates, we gradually make the transition from a bear market portfolio to a bull market portfolio, and remain aware we could be wrong about bullish outcomes. If we are wrong, we stop the transition and reverse course gradually.

The Near Side Of The Fence: If stocks continue to move higher,

- We have an opportunity to participate.

- In the 2007-2009 bear market, markets came down rapidly with little in the way of countertrend moves, which means it is possible a similar situation may occur on the way back up – a rapid climb with little in the way of significant countertrend moves (which is what has happened so far during this rally). It is possible those who wait for a significant correction, will only get that opportunity from much higher levels. A significant correction is coming - the question is from what levels (now or later).

- In early June, numerous asset classes “broke out” above resistance levels which can offer a lower risk entry point since what was resistance becomes support.

http://www.ciovaccocapital.com/sys-tmpl/fencesitting/

2009-2010: Evidence of Cyclical Bull and Reflation

2009-2010: Evidence of New Cyclical Bull Markets

At CCM, we do not believe in making investment decisions based exclusively on financial market forecasting. We instead look for fundamental and technical alignment to support and confirm forecasts. The transition from a bear market to a bull market takes time. Long-term investors can migrate from bear market allocations to bull market allocations as evidence of a primary trend change unfolds over several months.

In mid-April of 2009, the NASDAQ made an important new high, which may have signaled the first major step in the transition from a bear market to a bull market. The research below covers numerous observable events which point to the possibility of a new cyclical bull market taking shape in 2009. Cyclical bull markets can last from a few months to a few years, which is in contrast to a secular bull market which can last for 20 years or more. We do not believe all the elements are in place for a secular bull market, but we must respect that cyclical bull markets can last continue for years. For example, many believe the 2003-2007 bull market was of the cyclical variety. Cyclical or secular, the market went up for four years in the last bull market, which presented an opportunity for investors. Based on studies of post recession periods and periods after the S&P 500’s 200-day moving average turns up, it is reasonable to surmise stocks could rally into the early spring of 2010.

Corrections To Be Expected

A cyclical bull market does not mean the coming months will be easy for investors. The market never makes anything easy for anyone. Significant corrections coupled with periods of uneasiness and fear are to be expected in any bull market, secular or cyclical. With a recent successful retest of lows in the S&P 500 and many markets well above their 200-day moving averages, we can afford to give our investments a little more rope during the inevitable corrections in asset prices. As time goes on, stop-loss orders and risk management techniques should be able to take on a diminished role as we will err on the side of remaining invested into early 2010.

If conditions deteriorate and the markets migrate back toward a bearish stance, we will be willing to accept the possibility that the current bear has further to run. However, bullish evidence is not in short supply as we enter the second half of 2009. We will continue to monitor the markets and invest based on the observable evidence at hand. The observable evidence at hand remains bullish.

Focus Remains on Money Supply Expansion, Asia, and Commodities

Since we have economic data and technical evidence in hand that support further gains in asset prices, for the balance of 2009 and for a portion of 2010, we will focus on the three themes below and place a reduced empasis on the two themes that follow.

Primary Drivers Next 10-12 Months

Expansion of the money supply / fiat currency concerns / inflation

Commodities, clean energy, and water

Economic shift from United States to Asia

Secondary Drivers Next 10-12 Months

Infrastructure & government programs (slow implementation of some programs)

Baby boomers' transition from consumers to savers / consumer deleveraging (still important long-term)

http://www.ciovaccocapital.com/sys-tmpl/2009bullmarkets/

At CCM, we do not believe in making investment decisions based exclusively on financial market forecasting. We instead look for fundamental and technical alignment to support and confirm forecasts. The transition from a bear market to a bull market takes time. Long-term investors can migrate from bear market allocations to bull market allocations as evidence of a primary trend change unfolds over several months.

In mid-April of 2009, the NASDAQ made an important new high, which may have signaled the first major step in the transition from a bear market to a bull market. The research below covers numerous observable events which point to the possibility of a new cyclical bull market taking shape in 2009. Cyclical bull markets can last from a few months to a few years, which is in contrast to a secular bull market which can last for 20 years or more. We do not believe all the elements are in place for a secular bull market, but we must respect that cyclical bull markets can last continue for years. For example, many believe the 2003-2007 bull market was of the cyclical variety. Cyclical or secular, the market went up for four years in the last bull market, which presented an opportunity for investors. Based on studies of post recession periods and periods after the S&P 500’s 200-day moving average turns up, it is reasonable to surmise stocks could rally into the early spring of 2010.

Corrections To Be Expected

A cyclical bull market does not mean the coming months will be easy for investors. The market never makes anything easy for anyone. Significant corrections coupled with periods of uneasiness and fear are to be expected in any bull market, secular or cyclical. With a recent successful retest of lows in the S&P 500 and many markets well above their 200-day moving averages, we can afford to give our investments a little more rope during the inevitable corrections in asset prices. As time goes on, stop-loss orders and risk management techniques should be able to take on a diminished role as we will err on the side of remaining invested into early 2010.

If conditions deteriorate and the markets migrate back toward a bearish stance, we will be willing to accept the possibility that the current bear has further to run. However, bullish evidence is not in short supply as we enter the second half of 2009. We will continue to monitor the markets and invest based on the observable evidence at hand. The observable evidence at hand remains bullish.

Focus Remains on Money Supply Expansion, Asia, and Commodities

Since we have economic data and technical evidence in hand that support further gains in asset prices, for the balance of 2009 and for a portion of 2010, we will focus on the three themes below and place a reduced empasis on the two themes that follow.

Primary Drivers Next 10-12 Months

Expansion of the money supply / fiat currency concerns / inflation

Commodities, clean energy, and water

Economic shift from United States to Asia

Secondary Drivers Next 10-12 Months

Infrastructure & government programs (slow implementation of some programs)

Baby boomers' transition from consumers to savers / consumer deleveraging (still important long-term)

http://www.ciovaccocapital.com/sys-tmpl/2009bullmarkets/

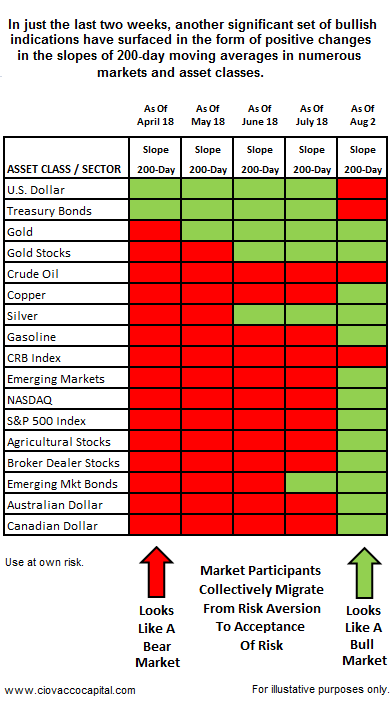

Markets Make Significant Progress In Transitions From Bear Markets To Bull Markets

The transition from a bear market to a bull market is just that; a transition. Transitions take time and are not binary events like turning a light on or off. Transitions in any market can be frustrating and stressful, but if we continue to focus on the most important and telling indicators, the market should get us pointed in the right direction and aligned with the primary trends.

While there are numerous signs which can indicate the possible transition from a bear market to a bull market, the following two milestones are of uppermost importance:

- When the 50-day moving average crosses, and more importantly holds above, the 200-day moving average,

- When the slope of the 200-day moving average turns positive.

During an established bull market, a good way to eliminate less attractive markets or investment alternatives is to discard those that have a negatively sloped 200-day moving average. At the end of a bear market, it takes time for a market to send signals of the potential staying power of a rally via a positive change in the slope of a 200-day moving average. As shown in the chart below, even though stocks began to bottom in mass in March of this year, we only started to see positive changes in the slopes of 200-day moving averages in the last two weeks.

http://www.ciovaccocapital.com/sys-tmpl/200turnuppublic/

Stocks Perform Well After A Recession

If the recession has already ended as evidence suggests, then the next six to twelve months may offer an opportunity for investors.

Stocks were higher both six and twelve months after the end of nine out of the ten recessions („49, „54, „58, „61, „70, „75, „80, „82, „91, „01). The exception was 2001. However, the slope of the S&P 500‟s 200-day moving average never turned positive in 2001, which is not the case in 2009. Commodities historically have performed well following recessions.

http://ciovaccocapital.com/CCM%20ASD%20AUG%202009%20PDF.pdf

Stocks were higher both six and twelve months after the end of nine out of the ten recessions („49, „54, „58, „61, „70, „75, „80, „82, „91, „01). The exception was 2001. However, the slope of the S&P 500‟s 200-day moving average never turned positive in 2001, which is not the case in 2009. Commodities historically have performed well following recessions.

http://ciovaccocapital.com/CCM%20ASD%20AUG%202009%20PDF.pdf

Sunday, 13 September 2009

*****Buffett's shrinking portfolio of the 1980s (2)

http://spreadsheets.google.com/pub?key=t7u4BYlpDKstozulNims5Hw&output=html

The above table shows, Buffett entered the 1980s energetic, ready to dive into a market he saw as woefully underappraised. As the market rose in value without pause, Buffett's conservatism got the better of him. By 1987, he was holding large stakes in just three stocks. When the decade began, Buffett had amassed large positions in 18 different companies.

Warren Buffett does not possess a magic formula for determining when the stock market is grossly overvalued or undervalued. By all accounts, his decisons to plunge into or escape from the marekt are based on several commonsense factors, namely:

1. The relationship between stock yields and bond yields.

2. The rate of climb in the market.

3. Earnings multiples.

4. The state of the economy.

5. The big picture (holistic view of companies, industries, and the entire market).

The above table shows, Buffett entered the 1980s energetic, ready to dive into a market he saw as woefully underappraised. As the market rose in value without pause, Buffett's conservatism got the better of him. By 1987, he was holding large stakes in just three stocks. When the decade began, Buffett had amassed large positions in 18 different companies.

Warren Buffett does not possess a magic formula for determining when the stock market is grossly overvalued or undervalued. By all accounts, his decisons to plunge into or escape from the marekt are based on several commonsense factors, namely:

1. The relationship between stock yields and bond yields.

2. The rate of climb in the market.

3. Earnings multiples.

4. The state of the economy.

5. The big picture (holistic view of companies, industries, and the entire market).

*****Buffett's Shrinking Portfolio of the 1980s (1)

http://spreadsheets.google.com/pub?key=t7u4BYlpDKstozulNims5Hw&output=html

Market Call by Buffett: Seeing the opportunities that would open up in the 1980s

By 1979, the Dow Jones Industrial Average traded no higher than it did in 1964 - 15 years without a single point gain!

Pessimism hit extreme levels. The public had gradually shifted their portfolios into bonds, real estate, and precious metals, and brokers found it difficult to peddle even stocks with 15 percent dividend yields.

Leading market strategists of the day, predicting more of the same financial morass, implored investors to buy bonds and avoid stocks. Buffett saw things differently. From his perspective, quality blue-chip stocks were being given away; some sold for less than their book values, despite the fact that econmic prospects for the United States still appeared bright.

Corporate returns on equity remained healthy, blue-chip earnings were advancing at double-digit rtes, and the speculative frenzy that had destroyed the integrity of the late-1960s markets had finally been removed from the equation.

"Stocks now sell at levels that should produce long-term returns superior to bonds," he told shareholders. "Yet pension managers, usually encouraged by corporate sponsors that must necessarily please, are pouring funds in record proportion into bonds. Meanwhile, orders for stocks are being placed with eyedropper." How right Buffett was.

As Tilson pointed out, the stock market has returned an annualised 17.2 percent since Buffett penned those words. Bonds returned 9.6%.

Market Call by Buffett: Avoiding the 1987 Crash

By the mid-1980s, Buffett's buy-and-hold philosophy had been carved in stone. He maintained large stakes in his three favorite companies - GEICO, Washington Post Co., and Capital Cities/ABC (which later merged with Walt Disney) - and pledged to hold these "inevitables", as he called them, forever. He didn't share the same convictions about the rest of the stock market.

At the Berkshire Hathaway annual meeting in 1986, Buffett lamented that he could not find suitable companies trading at low prices. Rather than dilute his portfolio with short-term stock investments, and given the fact that Buffett's stock holdings had already provided him tens of millions of dollars in gains, Buffett opted to take profits and shrink his portfolio.

"I still can't find any bargains in today's market," he told shareholders. "We don't currently own any equities to speak of." Just 5 months before the 1987 crash, he told shareholders of his inability to find any large-cap stocks offering a high rate-of-return potential: "There's nothing that we could see buying even if it went down 10 percent."

In retrospect, Buffett's comments about a 10 percent decline ultimately proved conservative. Five months after telling shareholders of his dilemma, the stock market lost 30 percent within a matter of days.

His decision to whittle away his portfolio slowly before the crash undoubtedly kept Berkshire's stock portfolio from imparting too big a negative influence on book value.

Market Call by Buffett: Seeing the opportunities that would open up in the 1980s

By 1979, the Dow Jones Industrial Average traded no higher than it did in 1964 - 15 years without a single point gain!

Pessimism hit extreme levels. The public had gradually shifted their portfolios into bonds, real estate, and precious metals, and brokers found it difficult to peddle even stocks with 15 percent dividend yields.

Leading market strategists of the day, predicting more of the same financial morass, implored investors to buy bonds and avoid stocks. Buffett saw things differently. From his perspective, quality blue-chip stocks were being given away; some sold for less than their book values, despite the fact that econmic prospects for the United States still appeared bright.

Corporate returns on equity remained healthy, blue-chip earnings were advancing at double-digit rtes, and the speculative frenzy that had destroyed the integrity of the late-1960s markets had finally been removed from the equation.

"Stocks now sell at levels that should produce long-term returns superior to bonds," he told shareholders. "Yet pension managers, usually encouraged by corporate sponsors that must necessarily please, are pouring funds in record proportion into bonds. Meanwhile, orders for stocks are being placed with eyedropper." How right Buffett was.

As Tilson pointed out, the stock market has returned an annualised 17.2 percent since Buffett penned those words. Bonds returned 9.6%.

Market Call by Buffett: Avoiding the 1987 Crash

By the mid-1980s, Buffett's buy-and-hold philosophy had been carved in stone. He maintained large stakes in his three favorite companies - GEICO, Washington Post Co., and Capital Cities/ABC (which later merged with Walt Disney) - and pledged to hold these "inevitables", as he called them, forever. He didn't share the same convictions about the rest of the stock market.

At the Berkshire Hathaway annual meeting in 1986, Buffett lamented that he could not find suitable companies trading at low prices. Rather than dilute his portfolio with short-term stock investments, and given the fact that Buffett's stock holdings had already provided him tens of millions of dollars in gains, Buffett opted to take profits and shrink his portfolio.

"I still can't find any bargains in today's market," he told shareholders. "We don't currently own any equities to speak of." Just 5 months before the 1987 crash, he told shareholders of his inability to find any large-cap stocks offering a high rate-of-return potential: "There's nothing that we could see buying even if it went down 10 percent."

In retrospect, Buffett's comments about a 10 percent decline ultimately proved conservative. Five months after telling shareholders of his dilemma, the stock market lost 30 percent within a matter of days.

His decision to whittle away his portfolio slowly before the crash undoubtedly kept Berkshire's stock portfolio from imparting too big a negative influence on book value.

Focus on how Buffett best avoids losses

List Your Top 5 Rules for Success in Investing

If I polled 1,000 investors and asked them to list their top 5 rules for success, their answers would differ from Buffett's. Here is what they would probably say:

Rule 1: Take a long term perspective.

Rule 2: Keep adding money to the market and let the magic of compounding work for you.

Rule 3: Don't try to time the market.

Rule 4: Stick to companies you understand.

Rule 5: Diversify.

Few investors would think to mention Buffett's cardinal "don't lose money" rule.

Why?

1. Avoiding losses is probably the most important tool for long-term success in investing. No investor, even Buffett, can avoid periodic losses on individual stocks. Even, if you resigned yourself to buying only at incredibly cheap prices, occasional mistakes will still occur. What differentiates Buffett from nearly all other investors is his ability to avoid yearly losses in his entire portfolio.

2. Diversification alone can't prevent losses. All diversification can do is minimise the chances that a few stocks implode (non-market risk or stock specific risk) and drag the performance of the portfolio with them. Even if you hold 100 stocks, you are forever vulnerable to "market risk," the risk that a declining market causes nearly all stocks to drop together.

3. Most investors use the market as their mechanism for avoiding losses. What does this mean? They simply sell when a stock falls below its break-even point, no matter the fundamentals. One highly touted strategy of the 1990s, espoused by Investor's Business Daily, implores investors to sell any issue that falls more than 8% below its purchase price, irrespective of events. Market timers rely on similar strategies. They make short-term bets on the direction of individual stocks and are prepared to exit quickly if the market turns against them.

4. These strategies ultimately degrade into a form of gambling, where the odds of success shrink because the investors' holding period is too short. Other investos avoid losses by continuing to hold poor-performing stocks, sometimes for years, until they rally back above their original cost. To profit from this strategy, you must pin your hopes on the market's ultimately validating your decision.

How Warren Buffett avoids yearly losses in his entire portfolio?

Warren Buffett would rather not place his faith in the hands of investors and traders. The methods he uses to lock in yearly gains take the market out of the equation.

He reckons that if he can guarantee himself returns, even in poor markets, he will ultimately be way ahead of the game.

To learn more, we should focus on how Buffett best avoids losses.

These include:

Timing the market. He is not concerned about the day-to-day fluctuations in the stock market. However, Buffett - whether by accident or calculation - must be recognized as one of the most astute market timers in history.

Convertibles. Some of Buffett's most lucrative investments in the late 1980s and early 1990s involved convertibles, which are hybrid securities that possess features of a stock and an income-producing security such as a bond or preferred stock.

Options. On a number of occsions, Buffett has expressed his disdain for derivative securities such as futures and options contracts. Because these securities are bets on shorter-term price movements within a market, they fall under the definition of "gambling" rather than of "investing." If Warren Buffett does dabble in options, and few doubt he could dabble successfully, he does so quietly. He once acknowledged writing put options on Coca-Cola's stock; at the time he was thinking of adding to his stake in the soft-drink company.

#Arbitrage. Not only did Buffett continue to beat the major market averages, but he suffered few single-year declines along the way. That second accomplishment is, by far, the more remarkable. Buffett's scorecard shows that he has increased the book value of Berkshire Hathaway's stock 35 consecutive years. In only 4 years, did the S&P 500 Index beat the growth of Berkshire's equity. Right from the start of his investment management career, Buffett resorted extensively to takeover arbitrage (the trading of securities involved in mergers) to keep his portfolio results positive. In poor market years, arbitrage activities have greatly enhanced Buffett's performance and keep returns positive. In strong markets, Buffett has exploited the profit opportunities of mergers to exceed the returns of the indexes. Benjamin Graham, Buffett's mentor, had made arbitrage one of the keystones of his teachings and money management activities at Graham-Newman between 1926 and 1956. Graham's clients were informed that some of their money would be deployed in shorter term situations to exploit irrational price discrepancies. These situations included reorganizations, liquidations, hedges involving convertible bonds and preferred stocks, and takeovers.

----

There are only 3 ways an investor can attain a long-term, loss-free track record:

1. Buy short-term Treasury bills and bonds and hold them to maturity, thereby locking in 4 to 6 percent average annual gains.

2. Concentrate on private-market investments by buying properties that consistently generate higher profits and that can sell for greater prices each year.

3. Own publicly traded securities and minimise your exposure to price fluctuations by devoiting some of the portfolio to unconventional "sure things.# "

If I polled 1,000 investors and asked them to list their top 5 rules for success, their answers would differ from Buffett's. Here is what they would probably say:

Rule 1: Take a long term perspective.

Rule 2: Keep adding money to the market and let the magic of compounding work for you.

Rule 3: Don't try to time the market.

Rule 4: Stick to companies you understand.

Rule 5: Diversify.

Few investors would think to mention Buffett's cardinal "don't lose money" rule.

Why?

- Some investors, sadly, refuse to believe that losses can occur, so accustomed are they to the unprecedented rally in the major indexes since 1987.

- Surveys done by mutual fund companies during the past few years indicate that a high percentage of individual investors still don't believe that mutual funds can lose money or that the market is capable of dropping more than 10% anymore.

- Other investors see losses as temporary setbacks or as opportunities to add to their positions.

- Still others, acting out a psychological defense mechanism, try to avoid losses by violating their own rules. They let the ticker tape infect decision making and trade in and out of winners and losers to avoid the psychological trauma of having to report a loss.

1. Avoiding losses is probably the most important tool for long-term success in investing. No investor, even Buffett, can avoid periodic losses on individual stocks. Even, if you resigned yourself to buying only at incredibly cheap prices, occasional mistakes will still occur. What differentiates Buffett from nearly all other investors is his ability to avoid yearly losses in his entire portfolio.

2. Diversification alone can't prevent losses. All diversification can do is minimise the chances that a few stocks implode (non-market risk or stock specific risk) and drag the performance of the portfolio with them. Even if you hold 100 stocks, you are forever vulnerable to "market risk," the risk that a declining market causes nearly all stocks to drop together.

3. Most investors use the market as their mechanism for avoiding losses. What does this mean? They simply sell when a stock falls below its break-even point, no matter the fundamentals. One highly touted strategy of the 1990s, espoused by Investor's Business Daily, implores investors to sell any issue that falls more than 8% below its purchase price, irrespective of events. Market timers rely on similar strategies. They make short-term bets on the direction of individual stocks and are prepared to exit quickly if the market turns against them.

4. These strategies ultimately degrade into a form of gambling, where the odds of success shrink because the investors' holding period is too short. Other investos avoid losses by continuing to hold poor-performing stocks, sometimes for years, until they rally back above their original cost. To profit from this strategy, you must pin your hopes on the market's ultimately validating your decision.

How Warren Buffett avoids yearly losses in his entire portfolio?

Warren Buffett would rather not place his faith in the hands of investors and traders. The methods he uses to lock in yearly gains take the market out of the equation.

He reckons that if he can guarantee himself returns, even in poor markets, he will ultimately be way ahead of the game.

To learn more, we should focus on how Buffett best avoids losses.

These include:

Timing the market. He is not concerned about the day-to-day fluctuations in the stock market. However, Buffett - whether by accident or calculation - must be recognized as one of the most astute market timers in history.

Convertibles. Some of Buffett's most lucrative investments in the late 1980s and early 1990s involved convertibles, which are hybrid securities that possess features of a stock and an income-producing security such as a bond or preferred stock.

Options. On a number of occsions, Buffett has expressed his disdain for derivative securities such as futures and options contracts. Because these securities are bets on shorter-term price movements within a market, they fall under the definition of "gambling" rather than of "investing." If Warren Buffett does dabble in options, and few doubt he could dabble successfully, he does so quietly. He once acknowledged writing put options on Coca-Cola's stock; at the time he was thinking of adding to his stake in the soft-drink company.

#Arbitrage. Not only did Buffett continue to beat the major market averages, but he suffered few single-year declines along the way. That second accomplishment is, by far, the more remarkable. Buffett's scorecard shows that he has increased the book value of Berkshire Hathaway's stock 35 consecutive years. In only 4 years, did the S&P 500 Index beat the growth of Berkshire's equity. Right from the start of his investment management career, Buffett resorted extensively to takeover arbitrage (the trading of securities involved in mergers) to keep his portfolio results positive. In poor market years, arbitrage activities have greatly enhanced Buffett's performance and keep returns positive. In strong markets, Buffett has exploited the profit opportunities of mergers to exceed the returns of the indexes. Benjamin Graham, Buffett's mentor, had made arbitrage one of the keystones of his teachings and money management activities at Graham-Newman between 1926 and 1956. Graham's clients were informed that some of their money would be deployed in shorter term situations to exploit irrational price discrepancies. These situations included reorganizations, liquidations, hedges involving convertible bonds and preferred stocks, and takeovers.

----

There are only 3 ways an investor can attain a long-term, loss-free track record:

1. Buy short-term Treasury bills and bonds and hold them to maturity, thereby locking in 4 to 6 percent average annual gains.

2. Concentrate on private-market investments by buying properties that consistently generate higher profits and that can sell for greater prices each year.

3. Own publicly traded securities and minimise your exposure to price fluctuations by devoiting some of the portfolio to unconventional "sure things.# "

Why Buffett is top in the financial world of investing?

If you understand the rules of the loser's games, you have taken a critical first step toward success in investments.

Warren Buffett sits atop the financial world because he made the fewest mistakes over his 40-year career. His most common mistakes, he admits, are "sins of omission," in which he

They are simply lost opportunities.

Avoiding losses is probably the most important tool for long-term success in investing. No investor, even Buffett, can avoid periodic losses on individual stocks.

What differentiates Buffett from nearly all other investors is his ability to avoid yearly losses in his entire portfolio.

Warren Buffett sits atop the financial world because he made the fewest mistakes over his 40-year career. His most common mistakes, he admits, are "sins of omission," in which he

- failed to buy a stock that rallied, or

- sold a stock too soon.

They are simply lost opportunities.

Avoiding losses is probably the most important tool for long-term success in investing. No investor, even Buffett, can avoid periodic losses on individual stocks.

What differentiates Buffett from nearly all other investors is his ability to avoid yearly losses in his entire portfolio.

The Benefits of Avoiding Mistakes

1. A typical investor who spreads his or her money over a basket of stocks can expect to achieve 10 to 12 percent annualized gains over great periods.

2. The same investor who focuses on the types of stocks Buffett owns - Coca-Cola, Gillette, Capital Cities, Wells Fargo, etc. - could expect to gain perhaps a few percentage points more each year. These stocks have shown a tendency to outperform the market over long periods because they exhibited growth rates greater than the average US corporation.

3. A shrewd, full time investor who focussed on Buffett-like stocks and made sure to buy them at wonderfully cheap prices could add a couple of extra percentage points of gain a year.

But the combined effects of these strategies still don't come close to producing the 33 percent compounded annual gain Buffett attained between the mid-1950s and the late 1990s.

Peter Lynch's managed the Magellan Fund. He bought and sold common stocks like the rest of us, including many of the same types of stocks you probably placed in your own portfolio.

Why, then, did Lynch and Buffett attain vastly superior results? There's got to be more to the story.

We tend to overlook the fact that the success of investors such as Lynch and Buffett derived from thousands of critical decisions they made over the course of decades, many of which were made on the fly; but the majority of which were correct.

In our quest to find shortcut answers to how they did it, we tend to look at only the beginning - that Buffett started with $100 - and at the end - his $30 billion fortune and dismiss the daily rituals that got him from point A to point B. Those rituals, however, are what pushed Buffett's returns well above those of the crowd.

"If everybody had seen what he had seen, he wouldn't have made huge gains from his visions," Forbes magazine once wrote.

2. The same investor who focuses on the types of stocks Buffett owns - Coca-Cola, Gillette, Capital Cities, Wells Fargo, etc. - could expect to gain perhaps a few percentage points more each year. These stocks have shown a tendency to outperform the market over long periods because they exhibited growth rates greater than the average US corporation.

3. A shrewd, full time investor who focussed on Buffett-like stocks and made sure to buy them at wonderfully cheap prices could add a couple of extra percentage points of gain a year.

But the combined effects of these strategies still don't come close to producing the 33 percent compounded annual gain Buffett attained between the mid-1950s and the late 1990s.

Peter Lynch's managed the Magellan Fund. He bought and sold common stocks like the rest of us, including many of the same types of stocks you probably placed in your own portfolio.

Why, then, did Lynch and Buffett attain vastly superior results? There's got to be more to the story.

We tend to overlook the fact that the success of investors such as Lynch and Buffett derived from thousands of critical decisions they made over the course of decades, many of which were made on the fly; but the majority of which were correct.

In our quest to find shortcut answers to how they did it, we tend to look at only the beginning - that Buffett started with $100 - and at the end - his $30 billion fortune and dismiss the daily rituals that got him from point A to point B. Those rituals, however, are what pushed Buffett's returns well above those of the crowd.

"If everybody had seen what he had seen, he wouldn't have made huge gains from his visions," Forbes magazine once wrote.

The Power of Avoiding Losses

Losses occur for three primary reasons:

1. You took bigger risks and exposed yourself to a higher probability of loss.

2. You invested in an instrument that failed to keep pace with inflation and interest rates (e.g. CDs).

3. You didn't hold the instrument long enough to let its true intrinsic value be realized.

There aren't many ways an investor can avoid periodic losses. The best way is to invest all of your assets in bonds and hold them to maturity. You would, of course, experience an erosion in the value of the bond due to inflation. If interest rates rise during your holding period, the intrinsic value of the bond would fall and the yearly coupon wouldn't compensate you for inflationary pressures.

To reduce the chance of losses, you must minimise mistakes. The fewer errors made over your investing career, the better your long-term returns.

We've seen the advantage of adding extra points of gain to your yearly returns. Earnings an extra 2% points a year on your portfolio compounds into tremendous amounts. Beating the market's presumed 11% yearly return by 2% points would translate into hundreds of thousands of dollars of extra profits over time.

The same holds true if you can avoid a loss. When you lose money, even if for just a year, you greatly erode the terminal value of your portfolio.

1. You took bigger risks and exposed yourself to a higher probability of loss.

2. You invested in an instrument that failed to keep pace with inflation and interest rates (e.g. CDs).

3. You didn't hold the instrument long enough to let its true intrinsic value be realized.

There aren't many ways an investor can avoid periodic losses. The best way is to invest all of your assets in bonds and hold them to maturity. You would, of course, experience an erosion in the value of the bond due to inflation. If interest rates rise during your holding period, the intrinsic value of the bond would fall and the yearly coupon wouldn't compensate you for inflationary pressures.

To reduce the chance of losses, you must minimise mistakes. The fewer errors made over your investing career, the better your long-term returns.

We've seen the advantage of adding extra points of gain to your yearly returns. Earnings an extra 2% points a year on your portfolio compounds into tremendous amounts. Beating the market's presumed 11% yearly return by 2% points would translate into hundreds of thousands of dollars of extra profits over time.

The same holds true if you can avoid a loss. When you lose money, even if for just a year, you greatly erode the terminal value of your portfolio.

- You consume precious resources that must be replaced.

- In addition, you waste precious time trying to make up lost ground.

- Losses also reduce the positive effects of compounding.

The effects of avoiding losses can be studied by considering 3 portfolios, A, B, and C, each of which normally gains 10% a year for 30 years. Portfolio B, obtains zero gains (0%) in years 10, 20, and 30. Portfolio C suffers a 10% loss in years 10, 20 and 30.

- A $10,000 investment in portfolio A would return $174,490 by the 30th year.

- Portfolio B would return considerably less - $131,100 - because of three break-even years. The portfolio never actually lost money, but will forever lag far behind porfolio A by virtue of having three mediocre years. Historically speaking, portfolio B's returns aren't all that bad, for the investor managed to avoid losses every year.

- Portfolio C, by contrast, loses 10% in years 10, 20, and 30. It's return of $95,572 was considerably lower. The effects of those three not-so-unreasonable years is to lop nearly $79,000 off the final value of the portfolio. That's what compounding can do. The actual loss in the 10th year was only $2,357. The loss in the 20th year was just $5,004; the final year loss was $10,619. But the power of compounding turned $17,980 in total yearly losses into $79,000 of lost opportunities.

Buffett once summarized the essence of successful investing in a simple quip:

Rule number 1: Don't lose money

Rule number 2: Don't forget rule number 1

The dollar carry-trade

Cheap dollars are sowing the seeds of the next world crisis

After years of selling cheap goods to debt-fuelled Western consumers, China now has $2 trillion dollars of foreign exchange reserves. That's 2,000 billion – a reserve haul no less 25 times bigger than that of the UK.

By Liam Halligan

Published: 6:05PM BST 12 Sep 2009

Comments 25 Comment on this article

In a world of systemic instability, reserves mean power. Reserves mean you can defend your currency, stabilise your banking system and boost your economy without resorting to yet more borrowing – or, worse still, the printing press.

More than half of China's reserves are denominated in dollars. So when the dollar falls, China loses serious money. When you're talking about a dollar-reserve number involving 12 zeros, even a modest weakening of the greenback sees China's wealth takes a mighty hit.

In recent years, America has run massive budget and trade deficits, both of which put downward pressure on the dollar – so devaluing China's reserves. Beijing has remained tight-lipped, worried less about diplomatic niceties than the financial implications of voicing its concerns. If the markets thought China would buy less dollar-denominated debt going forward, the US currency would weaken further, compounding Beijing's wealth-loss.

American leaders have relied on this Catch-22 for some time, guffawing that China is in so deep it has no choice but to carry on "sucking-up" US debt. But Beijing's Communist hierarchy is now so worried about America's wildly expansionary monetary policy that it is speaking out, despite the damage that does to the value of China's reserves.

Last weekend, Cheng Siwei, a leading Chinese policy maker, said that his country's leaders were "dismayed" by America's recourse to quantitative easing. "If they keep printing money to buy bonds, it will lead to inflation," he said. "So we'll diversify incremental reserves into euros, yen and other currencies".

This is hugely significant. China is now more worried about America inflating away its debts than about those debts being exposed to currency risk. Economists at Western banks making money from QE still say deflation is more likely than inflation. As this column has long argued, they are talking self-serving tosh.

The entire non-Western world rightly sees serious inflationary pressures down the track in the US, UK and other nations where political cowardice has resulted in irresponsible money printing.

Following Mr Cheng's comments, the dollar fell throughout last week, hitting a 12-month low against the euro. As the dollar's "safe haven" status was questioned, gold surged above $1,000 an ounce to an 18-month high.

The US currency could well keep falling. America's trade deficit grew in July at the fastest rate in almost a decade. Imports exceeded exports by $32bn last month – a gap 16pc wider than the month before. One reason was that as oil prices strengthened, so did the cost of US crude imports.

Oil touched $72 a barrel last week. If the greenback weakens further, prices will keep going up. That's because crude is priced in dollars and global investors will increasingly use commodities as an anti-inflation hedge.

These forces could combine to send the dollar into freefall. US inflation would then soar and interest rates would have to be jacked up. Even if a fast-collapsing dollar is avoided, Fed rates may have to rise quickly if China is serious about dollar-divesting and the US has to sell its debt elsewhere. Under both scenarios, the world's largest economy could get caught in the stagflation trap – recession and high inflation.

Beijing doesn't want the US to stagnate. China has too much to lose. But even if China and US work together to avoid a meltdown, the currency markets could provide one anyway.

The dollar is now being used as a "carry" currency. Traders are using low Fed rates to take out cheap dollar loans, then converting the money into currencies generating higher yields.

"Carrying" credit in this way is currently the source of huge gains. No one knows the true scale, but the world has, of course, been flooded with cheap dollars.

This presents serious systemic danger. A dollar weighed down by Chinese divestment, then suppressed further by carry-trading, could easily spring back. Those who had borrowed in dollars would owe more, while their dollar-funded investments would be worth less. This "unwinding" could send financial shock around the globe.

This is what happened in 1998, when yen carry-trades went wrong, causing the collapse of Long-Term Capital Management and sparking a global slowdown.

So even if the Western world manages to fix its banking system, the Fed's money printing could well be stoking up the next financial crisis. The dollar carry-trade. You heard it here first.

Liam Halligan is chief economist at Prosperity Capital Management

http://www.telegraph.co.uk/finance/comment/liamhalligan/6179482/Cheap-dollars-are-sowing-the-seeds-of-the-next-world-crisis.html

After years of selling cheap goods to debt-fuelled Western consumers, China now has $2 trillion dollars of foreign exchange reserves. That's 2,000 billion – a reserve haul no less 25 times bigger than that of the UK.

By Liam Halligan

Published: 6:05PM BST 12 Sep 2009

Comments 25 Comment on this article

In a world of systemic instability, reserves mean power. Reserves mean you can defend your currency, stabilise your banking system and boost your economy without resorting to yet more borrowing – or, worse still, the printing press.

More than half of China's reserves are denominated in dollars. So when the dollar falls, China loses serious money. When you're talking about a dollar-reserve number involving 12 zeros, even a modest weakening of the greenback sees China's wealth takes a mighty hit.

In recent years, America has run massive budget and trade deficits, both of which put downward pressure on the dollar – so devaluing China's reserves. Beijing has remained tight-lipped, worried less about diplomatic niceties than the financial implications of voicing its concerns. If the markets thought China would buy less dollar-denominated debt going forward, the US currency would weaken further, compounding Beijing's wealth-loss.

American leaders have relied on this Catch-22 for some time, guffawing that China is in so deep it has no choice but to carry on "sucking-up" US debt. But Beijing's Communist hierarchy is now so worried about America's wildly expansionary monetary policy that it is speaking out, despite the damage that does to the value of China's reserves.

Last weekend, Cheng Siwei, a leading Chinese policy maker, said that his country's leaders were "dismayed" by America's recourse to quantitative easing. "If they keep printing money to buy bonds, it will lead to inflation," he said. "So we'll diversify incremental reserves into euros, yen and other currencies".

This is hugely significant. China is now more worried about America inflating away its debts than about those debts being exposed to currency risk. Economists at Western banks making money from QE still say deflation is more likely than inflation. As this column has long argued, they are talking self-serving tosh.

The entire non-Western world rightly sees serious inflationary pressures down the track in the US, UK and other nations where political cowardice has resulted in irresponsible money printing.

Following Mr Cheng's comments, the dollar fell throughout last week, hitting a 12-month low against the euro. As the dollar's "safe haven" status was questioned, gold surged above $1,000 an ounce to an 18-month high.

The US currency could well keep falling. America's trade deficit grew in July at the fastest rate in almost a decade. Imports exceeded exports by $32bn last month – a gap 16pc wider than the month before. One reason was that as oil prices strengthened, so did the cost of US crude imports.

Oil touched $72 a barrel last week. If the greenback weakens further, prices will keep going up. That's because crude is priced in dollars and global investors will increasingly use commodities as an anti-inflation hedge.

These forces could combine to send the dollar into freefall. US inflation would then soar and interest rates would have to be jacked up. Even if a fast-collapsing dollar is avoided, Fed rates may have to rise quickly if China is serious about dollar-divesting and the US has to sell its debt elsewhere. Under both scenarios, the world's largest economy could get caught in the stagflation trap – recession and high inflation.

Beijing doesn't want the US to stagnate. China has too much to lose. But even if China and US work together to avoid a meltdown, the currency markets could provide one anyway.

The dollar is now being used as a "carry" currency. Traders are using low Fed rates to take out cheap dollar loans, then converting the money into currencies generating higher yields.

"Carrying" credit in this way is currently the source of huge gains. No one knows the true scale, but the world has, of course, been flooded with cheap dollars.

This presents serious systemic danger. A dollar weighed down by Chinese divestment, then suppressed further by carry-trading, could easily spring back. Those who had borrowed in dollars would owe more, while their dollar-funded investments would be worth less. This "unwinding" could send financial shock around the globe.

This is what happened in 1998, when yen carry-trades went wrong, causing the collapse of Long-Term Capital Management and sparking a global slowdown.

So even if the Western world manages to fix its banking system, the Fed's money printing could well be stoking up the next financial crisis. The dollar carry-trade. You heard it here first.

Liam Halligan is chief economist at Prosperity Capital Management

http://www.telegraph.co.uk/finance/comment/liamhalligan/6179482/Cheap-dollars-are-sowing-the-seeds-of-the-next-world-crisis.html

Vietnam is a clever way to play Asia

{kind=link}

Vietnam is a clever way to play Asia

Imagine the amount of money you would have made if you had started investing in China 10 years before the hot money started to flow. Your profits would have been absolutely phenomenal – even after the correction over the last two years.

By Garry White

Published: 5:41PM BST 12 Sep 2009

VinaCapital Vietnam Opportunities Fund

$1.71 +0.01

Questor says BUY

For investors keen on getting in ahead of the crowd, Vietnam could offer you a similar opportunity today.

For the 10 years before the credit crunch hit, Vietnam was Asia's second-fastest growing economy after China. The country tabled an average growth in GDP of 7.5pc a year. This year's government target is 5pc.

The country was hit hard by the financial crisis, but it has now started to recover – and a return to stellar growth in the next few years is very likely. Questor urges investors to buy into Vietnam now, while it is still cheap.

The country certainly has a lot going for it. It has one of the highest literacy rates in Asia, at 90pc, and the workforce is young, hard-working and optimistic.

Almost two-thirds of Vietnam's 85m people are under the age of 35 – and this should support economic growth over the medium term. A young population implies significant population growth in the future, which should stimulate demand further.

Significantly, labour in the country is even cheaper than in China, which should underpin investment in areas such as manufacturing.

A good example of the attractiveness of Vietnam was seen last week when Coca-Cola said it planned to double its investment in the country to $400m over the next three years. The company did not didn't send a minor representative to make this announcement; Muhtar Kent, Coke's chairman and chief executive, went to the country personally.

Arguably, Vietnam is now in the same position as China was a decade ago, but there are limited ways that a UK investor can invest in this fledgling economy.

The Vietnam Opportunity Fund (LSE: VOF), which is managed by country specialist VinaCapital, is one of the easiest ways for UK investors to play growth in the Asian nation.

The shares peaked at $4.78 in 2007, but the sharp risk aversion that gripped the markets means the shares have plunged significantly. They hit a low of 65 cents in December last year, but have since more than doubled to the current level.

The fund's mandate is to invest at least 70pc of its cash in Vietnam, with the remaining 30pc in China, Cambodia and Laos.

Its managers target medium to long-term capital gains with some recurring income and short-term profit taking – which appears to be a sensible strategy. The fund will invest in private companies, not just listed entities, as well as taking part in any privatisations the government proposes.

The largest portfolio constituent of this open-ended investment trust, at 7.6pc, is financial group Eximbank. It also has major holdings in HPG, a steel manufacturer, dairy group VNM, real estate group DI and fertiliser group DPM.

As of August 31, Vietnam Opportunity Fund's net asset value per share was $2.44 – up 12.2pc in just one month.

The shares can be bought as normal through your broker and the investment trust is priced in dollars. For investors seeking substantial long-term capital growth, Questor recommends an investment in this Asian market, as it is not fully recovered from the recent plunge and should return to significant growth soon. Shares in the Vietnam Opportunity Fund are a buy.

Catlin

332.8p +2.60

Questor says BUY

Lloyd's of London insurers had a good first half of the year and Catlin, the largest syndicate in the market, was no exception. The group posted a record half-year profit of $240m (£143m) as investment returns more than tripled.

In February, Questor recommended buying the shares, despite the insurer falling into the red. The group was one of many that needed a rights issue – and £200m was raised at a hefty 47pc discount. The cash call was sensible, as the company could invest in its business.

Insurance premiums had started to rise, as underwriters tried to rebuild their balance sheets following an active hurricane season in 2008 and heavy investment losses.

Since this time, market conditions have continued to improve and insurers including Amlin, Chaucer and Hiscox have benefited as returns from hedge funds and equities begin to improve. With a market capitalisation of more than £1bn, Catlin was always going to be well positioned to seize these fertile market conditions.

The company now covers about 30 different types of risks and has an international network in 17 countries across five continents.

Although short-term risks hang over the Lloyd's market – including the onset of the Atlantic hurricane season – Questor believes Catlin shares are worth buying for their impressive yield, despite the shares being 10pc below their recommendation price.

The shares are currently yielding 7.2pc and the stance remains buy.

Cisco Systems

$23.12 +0.03

Questor says TAKE PROFITS

Shares in networking group Cisco were recommended in January at $16.91. Questor argued that the group's earnings would be supported by the US stimulus package, which aimed to connect many US schools to the internet.