Understanding China

China has expanded its economy for the last 20 years. Its growth over the last 10 years was even more impressive than the first 10 years.

Its present stock market is trading at a PE of 50. This is not sustainable.

Why is the PE so high?

Being a relatively new stock market, the 'investors' are not savvy and the price fluctuations are expected to be larger than a mature market.

Another reason is the absence of other assets for the growing affluent Chinese to invest in. Besides keeping money in the bank, most Chinese invest into the property sectors and the stock markets. The high prices in these markets are reflecting the disparity in the excess demand over supply.

Properties in China's biggest cities, Shanghai and Peking have doubled in price over the last 5 years. This rise appears unabated. Some properties have risen another 2% to 10% over the last few months. Rental yields can support about 50% of the mortgage repayments in most cases. The gains in investing into these properties are purely capital gains from property price appreciations.

In Peking, it is not uncommon to find a 3 bedroom flat in a condominium centrally located priced at 5 million yuan. The average per capital income of the local Peking resident is around 2,000 yuan per month. How can such prices be supported? Are these properties affordable? Is there a disconnect between the prices of properties and the affordability of the people who are going to buy and live in them? Giving the present limited supply relative to demand, the price can continue to be supported. This can be explained by the unequal distribution of wealth among the population. There is a small group enjoying a large percentage of the wealth and this group will continue to invest into the property and the stock market in China. There is still some time to go to equilibrium.

There are many businesses in China with huge business opportunities tapping the capital market. The A shares cannot be traded by foreigners. To participate in the Chinese companies one would need to buy the H shares of these Chinese companies listed in the Hong Kong Stock Exchange (HangSeng).

Friday, 6 November 2009

Lityan: Selling to Suckers

Friday November 6, 2009

Lityan MD sells stake and pockets RM3.9mil

PETALING JAYA: Lityan Holdings Bhd group managing director and chief executive officer Nor Badli Mohd Alias has disposed of his entire stake in the company, a filing on Wednesday with Bursa Malaysia showed.

The stake, comprising 1.25 million shares or 1.98% of the issued shares, was disposed of at RM3.13 per share at a total value of RM3.91mil on Tuesday.

Nor Badli had purchased the shares en bloc on Oct 27 at RM1 per share, a separate filing on Oct 30 showed.

According to a source familiar with the restructuring of Lityan, the stake acquired and then sold by Nor Badli was part of the company’s restructuring scheme.

“As part of the resolutions passed by the shareholders for the restructuring programme, the group managing director and the executive director were both allowed to acquire up to a maximum 1.25 million shares and 750,000 shares respectively in support of the placement exercise,” he told StarBiz.

He added that as part of the restructuring plan, 17.2 million shares were issued to creditors, of which 16.8 million were successfully placed out and issued on Oct 27 at a reference price of RM1 per share.

The stock had traded at 1.6 sen in June 2006 before it was suspended.

Lityan’s share price has been surging since it emerged from Practice Note 17 status and relisted on Oct 30.

The stock closed yesterday at RM2.65.

Sources said interest in the company was largely due to it being in a partnership with Huawei Technologies Co Ltd, and that the partnership had successfully bid for one component of Telekom Malaysia Bhd’s RM11.3bil high-speed broadband project.

Lityan was queried by Bursa, which issued an unusual market activity advisory on the counter on Tuesday, following which the shares tumbled 9.25% to RM2.45 on that day.

Trading in the company’s shares was halted less than half an hour before the market closed on the same day.

-----

Thursday November 5, 2009

Investors continue buying into Lityan

By FINTAN NG

PETALING JAYA: Investor interest in Lityan Holdings Bhd, which recently emerged from Practice Note 17 status as a listed subsidiary of Lembaga Tabung Haji (LTH), has been intense on speculation of the company’s earnings potential resulting from a tie-up with Huawei Technologies Co Ltd as well as other Middle East project tenders.

Lityan group managing director and chief executive officer Nor Badli Mohd Alias said the share price volatility was likely due to the relatively lower public shareholding spread of the company with LTH having a 56% stake in the company.

“There’s a lot of interest in the company but people are not selling. Coupled with the low public shareholding spread, there’s bound to be a rise in the share price,” he told StarBiz.

On Tuesday, Lityan’s share price volatility earned the company an unusual market activity query from Bursa Malaysia.

The stock tumbled 9.3% to RM2.45 on the same day before trading in its shares was halted less than 30 minutes before the market closed.

Last Friday, the company’s shares surged 25.17% to close at RM1.74 from an opening price of RM1.39. From Oct 30 to Nov 4, the average trading volume was 13.68 million shares or 21.67% of the total share capital of 63.1 million shares.

Nor Badli had said last Friday that the company was in a tie-up with Huawei for Telekom Malaysia Bhd’s (TM) high-speed broadband (HSBB) project as well as tendering for projects in the Middle East.

Although TM group chief executive officer Datuk Zam Isa did not identify Huawei as one of the partners in the project in an earlier report, industry sources said the Shenzhen-based company was one of the technology partners in the RM11.3bil HSBB project.

Nor Badli said the company was in a tie-up with Huawei to tender for three packages in the HSBB project but declined to reveal details except that the company’s share of the packages would be based on its scope of works.

According to AmResearch Sdn Bhd, Lityan’s work in the project would involve fibre-to-the-home implementation and Internet protocol television infrastructure.

So far, only the package involving the roll-out of fibre optics for the last-mile to targeted high-density areas of Kuala Lumpur and Selangor has been announced.

“We don’t know when the results of the tender for the other packages will be announced. It’s been delayed six months,” Nor Badli said, adding that the tenders in the Middle East were done in conjunction with LTH.

“This will involve projects with a minimum total value of US$1bil,” he said.

Lityan MD sells stake and pockets RM3.9mil

PETALING JAYA: Lityan Holdings Bhd group managing director and chief executive officer Nor Badli Mohd Alias has disposed of his entire stake in the company, a filing on Wednesday with Bursa Malaysia showed.

The stake, comprising 1.25 million shares or 1.98% of the issued shares, was disposed of at RM3.13 per share at a total value of RM3.91mil on Tuesday.

Nor Badli had purchased the shares en bloc on Oct 27 at RM1 per share, a separate filing on Oct 30 showed.

According to a source familiar with the restructuring of Lityan, the stake acquired and then sold by Nor Badli was part of the company’s restructuring scheme.

“As part of the resolutions passed by the shareholders for the restructuring programme, the group managing director and the executive director were both allowed to acquire up to a maximum 1.25 million shares and 750,000 shares respectively in support of the placement exercise,” he told StarBiz.

He added that as part of the restructuring plan, 17.2 million shares were issued to creditors, of which 16.8 million were successfully placed out and issued on Oct 27 at a reference price of RM1 per share.

The stock had traded at 1.6 sen in June 2006 before it was suspended.

Lityan’s share price has been surging since it emerged from Practice Note 17 status and relisted on Oct 30.

The stock closed yesterday at RM2.65.

Sources said interest in the company was largely due to it being in a partnership with Huawei Technologies Co Ltd, and that the partnership had successfully bid for one component of Telekom Malaysia Bhd’s RM11.3bil high-speed broadband project.

Lityan was queried by Bursa, which issued an unusual market activity advisory on the counter on Tuesday, following which the shares tumbled 9.25% to RM2.45 on that day.

Trading in the company’s shares was halted less than half an hour before the market closed on the same day.

-----

Thursday November 5, 2009

Investors continue buying into Lityan

By FINTAN NG

PETALING JAYA: Investor interest in Lityan Holdings Bhd, which recently emerged from Practice Note 17 status as a listed subsidiary of Lembaga Tabung Haji (LTH), has been intense on speculation of the company’s earnings potential resulting from a tie-up with Huawei Technologies Co Ltd as well as other Middle East project tenders.

Lityan group managing director and chief executive officer Nor Badli Mohd Alias said the share price volatility was likely due to the relatively lower public shareholding spread of the company with LTH having a 56% stake in the company.

“There’s a lot of interest in the company but people are not selling. Coupled with the low public shareholding spread, there’s bound to be a rise in the share price,” he told StarBiz.

On Tuesday, Lityan’s share price volatility earned the company an unusual market activity query from Bursa Malaysia.

The stock tumbled 9.3% to RM2.45 on the same day before trading in its shares was halted less than 30 minutes before the market closed.

Last Friday, the company’s shares surged 25.17% to close at RM1.74 from an opening price of RM1.39. From Oct 30 to Nov 4, the average trading volume was 13.68 million shares or 21.67% of the total share capital of 63.1 million shares.

Nor Badli had said last Friday that the company was in a tie-up with Huawei for Telekom Malaysia Bhd’s (TM) high-speed broadband (HSBB) project as well as tendering for projects in the Middle East.

Although TM group chief executive officer Datuk Zam Isa did not identify Huawei as one of the partners in the project in an earlier report, industry sources said the Shenzhen-based company was one of the technology partners in the RM11.3bil HSBB project.

Nor Badli said the company was in a tie-up with Huawei to tender for three packages in the HSBB project but declined to reveal details except that the company’s share of the packages would be based on its scope of works.

According to AmResearch Sdn Bhd, Lityan’s work in the project would involve fibre-to-the-home implementation and Internet protocol television infrastructure.

So far, only the package involving the roll-out of fibre optics for the last-mile to targeted high-density areas of Kuala Lumpur and Selangor has been announced.

“We don’t know when the results of the tender for the other packages will be announced. It’s been delayed six months,” Nor Badli said, adding that the tenders in the Middle East were done in conjunction with LTH.

“This will involve projects with a minimum total value of US$1bil,” he said.

Analysts bullish on Malaysian banking sector

Analysts bullish on banking sector

By Goh Thean Eu

Published: 2009/11/06

Analysts believe the war to attract more customers to take up loans by lowering interest rates has come to an end, if not near to an end, as lenders are beginning to raise interest rates.

ANALYSTS and fund managers are generally bullish on the banking sector next year, as economic recovery, higher interest rates and lower non-performing loans (NPL) are expected to lift banks earnings.

"This year, people were worried about how the economy would shape up, and on the banking sector, people were concerned about banks' NPL. A lot of these concerns were addressed and we are now more optimistic about next year.

"We believe asset quality would not deteriorate significantly next year and we are also expecting the central bank to increase the OPR some time next year, which would offer a good earning driver and higher margin for the banks and we believe earnings and margins to be better next year," said a TA Securities analyst.

For more than a year, banks were in a fierce competition to attract more customers to take up loans by lowering interest rates. Analysts believe the war has come to an end, if not near to an end, as lenders are beginning to raise interest rates.

"Moving forward, the competition landscape would not be as bad as we expected earlier, thanks to the revision of interest rates. It will certainly help increase the net interest margins of banks.

"As long as the economic recovery story remains intact, we expect banks provision will eventually come down and we expect most local banks to post a double-digit growth on revenue and earnings next year," said an analyst from a local research house.

Aberdeen Asset Management managing director Gerald Ambrose thinks likewise.

"Companies must meet a set of criteria before we invest in them. From our company visits so far, I must say, a lot of companies that met our criteria are banks," he said.

He said companies that meet the criteria are companies that are well-managed, has a long-term business plan, good corporate governance, transparent and willing to return excess cash to minority shareholders as dividend, among others.

Although the Kuala Lumpur Financial Index rose by more than 55 per cent this year alone, compared with the 42 per cent year-to-date increase of the benchmark FTSE Bursa Malaysia KLCI, analysts still believe that it's not too late to invest in banks.

"We are maintaining our overweight call on the sector on the grounds that NPLs are likely to be benign while the downtrend in provisions and strong capitalisation positions will provide future earnings and capital management upside surprises, which may not have been fully reflected in banks' valuation," said OSK Research Sdn Bhd analyst Keith Wee in a report.

OSK placed a "buy" call on CIMB and EON Capital, while TA Securities has a "buy" on Public Bank and Hong Leong Bank.

Thursday, 5 November 2009

****Be a Better Investor

Be a Better Investor

Sponsored by

by Bob Frick

Thursday, October 8, 2009

Outsmart your emotions, cut your fees, keep it simple -- and reap higher returns.

Damn, it happened again. Ten years after the internet bubble ballooned, then burst, we're left to pick up our shattered portfolios from another cycle of hope, anxiety and regret. To make matters worse, our own actions added insult to the injury inflicted by the catastrophic bear market that ended last March.

By buying high and selling low, mutual fund investors, for instance, lost $42 billion more than they should have during the 12-month period that ended last May, estimates The Hulbert Financial Digest. (In a similar vein, columnist Russel Kinnel tells us that the typical investor earns far less than funds' reported returns.)

How could this have happened? The simple answer is that emotion, not logic, usually rules our investing habits. In many ways we're predisposed not just to buy high and sell low, but to cling to losing investments we should sell, ignore threats to our wealth and follow the investing herd off a cliff again and again.

These tendencies are now well documented in the burgeoning fields of investor psychology and behavioral finance. Scholars in both disciplines are arriving at a new understanding of how humans make decisions. For instance, in the bestseller Nudge: Improving Decisions About Health, Wealth and Happiness, authors Richard Thaler and Cass Sunstein say long-held assumptions that people "think like Albert Einstein, store as much memory as IBM's Big Blue and exercise the willpower of Mahatma Gandhi" are falling by the wayside. To help people, including investors, make better choices, we have to understand and embrace our emotions and predilections, say the authors, and figure out how to avoid becoming our own worst enemy.

Teachable Moments

But just recognizing our mental kinks won't help us undo them, experts say. "I don't believe it's possible to change behavior that's really hard-wired into our biology," says Andrew Lo, director of the Massachusetts Institute of Technology Laboratory for Financial Engineering. But "Homo sapiens can do what we've always done: adapt. We don't have wings, but we can fly. So we develop tools to protect ourselves from these emotional shortcomings."

The silver lining to the recent bear market is that painful experiences remain in our memories for a long time and provide lessons for the future. So let's review the past few years through the eyes of experts in investor psychology and behavioral finance, studying events not as a financial roller coaster, but rather as an emotional one.

Humans are wired to organize facts around stories. The Internet bubble was fueled by a fable that the Web would lead to an unending explosion of commerce. The explosion in real estate speculation that began in the early 2000s was firmly built on the same kind of fiction. Stories of people getting rich as property prices rose year after year "replicated and spread like thought viruses," says Robert Shiller, the Yale economist who warned of the Internet and real estate bubbles in different editions of his book Irrational Exuberance. Such tales instill confidence in people and inspire them to move fast to get rich themselves.

These stories proliferate even when they fly in the face of facts. That's because we tend to look only for facts that support our story, something called confirmation bias. So, for instance, real estate prices in Las Vegas and Phoenix rose at double-digit rates, as if land in those Sun Belt cities was a scarce commodity. The desire to cash in on the property boom ignored "obvious facts," says Thaler, such as a virtually "infinite supply of land" that facilitated an abundant supply of homes.

So think back to 2006. Real estate is on fire, the stock market is doing pretty well, and both investments look like sure bets. That's about the time the dangerous psychological juju started kicking in. Greg Davies, head of behavioral finance for Barclays Wealth, the London-based financial-services giant, says investors fell victim to the recency effect and began to lose their sense of caution because they'd known nothing but gains for several years.

As a result of the recency effect, says Davies, "what's most recent in our minds stands out." For instance, "if investments have been going up for a while, I start seeing them as less risky. I start thinking, Well, my budget for risky investments isn't full -- I can put more in there."

Buying Stimuli

As investors pile in and the markets continue to rise, herd behavior and regret drive our actions. One consequence of herd behavior is that it makes us think something is safe because it seems safe if everyone is doing it. And regret causes those who can't stand being left out to jump in.

Then, as our portfolios swell, we start to feel a collective buzz courtesy of dopamine, a feel-good chemical that the brain produces at the mere thought of making money (or driving a sports car or having sex). The more dopamine produced, the more decision-making is kicked to the primitive, emotional parts of our brain, making it harder for us to think logically. As the reward system gets excited, the fear centers in the brain are deactivated, says Richard Peterson, a psychiatrist who runs a hedge fund that aims to make money by taking advantage of investors' overreactions. "We're no longer able to observe the threats," says Peterson. "We observe only what we want to."

Now recall the mood in September 2008. The real estate sector is crumbling, and the stock market has been slipping for nearly a year. Uncle Sam has taken over Fannie Mae and Freddie Mac, and Bear Stearns and Lehman Brothers have failed. Investors, who couldn't wait to check their account balances when the market was rising, monitor them much less frequently now. They are suffering from the ostrich effect, a term coined by George Loewenstein, a professor of economics and psychology at Carnegie Mellon University.

Many investors who know intellectually that they're overloaded in stocks can't pull back, even if they're suffering steep losses. The reason is something called the disposition effect. On some level we feel that if we don't actually sell a stock that's underwater, we're not actually realizing the loss and the pain that goes with it.

Then, from mid September to mid October, the sum of our suppressed financial fears came to fruition. Stocks tumbled 30%. Do you remember that as an especially painful period? If you do, you're not imagining that pain. When we lose money, our brain reacts in the same way that it processes physical pain. Losing money hurts.

For many people, plunging portfolio values became too much to bear, and they just wanted the pain to end. So they sold. According to the Investment Company Institute, the greatest net monthly outflow from stock funds in the past two years -- $25 billion -- came in February 2009. The timing couldn't have been much worse for those who sold then. As it turned out, stocks bottomed on March 9 and surged about 50% over the ensuing six months.

As stocks have recovered, our emotions have begun to heal. Lo, the MIT professor, thinks most investors have already dealt with three of the five stages of grief-the denial, anger and bargaining phases-and are now working through the last two: depression and acceptance.

Now is a perfect time, while the trauma is still fresh in our minds, to figure out how to prevent similar mistakes in the future. Unfortunately, says Peterson, the psychiatrist and hedge-fund manager, the bear market was so painful that many investors don't want to think about it. As a result, he says, "five years from now they'll make the same mistakes."

So, if you recognize yourself in some of the actions (or lack thereof) we've just described, now's the time to take steps to make sure you don't suffer the same mental miscues in the future. You may not be able to change your behavior in trying times, but you can change your investing strategy to neutralize negative impulses.

One bold idea: If you handle your own investments and you find that emotions are tripping you up, hire an adviser. A good adviser should help you avoid those impulses-which typically stem from short-term fluctuations in the value of your investments-and keep you focused on meeting long-term goals. The extra cost could be worth the money.

You can also use a psychological quirk, called mental accounting, to your advantage. Mental accounting holds that even though a dollar is a dollar, we often mentally separate our wealth into different accounts. Consider opening a separate account to house your "safe" money-cash-type investments and other low-risk stuff that should hold up even during a stock-market crash. The size of your safe account depends on your risk tolerance and other factors. But while the pain of the bear market is fresh in your mind, determine how much of a cushion you need so that another 40% drop in the rest of your investments won't lead to poorly conceived actions that are driven by panic.

You may also want to tone down the risk in your other accounts as an antidote for increasing volatility in all sorts of markets. A more stable portfolio will leave you calmer and better able to make decisions based on logic rather than emotion.

Beware of merely mixing stocks and bonds, which Lo says creates "diversification deficit disorder." You need other assets, such as real estate, commodities and other alternative investments.

One of the best vaccines against emotional decision-making is the tried-and-true technique of dollar-cost averaging. By investing a fixed amount of money on a regular basis-the practice of just about anyone who participates in a 401(k) or similar retirement plan-you're conceding that you can't time the market. You avoid the temptation to buy high, or to pull out precipitously if the market sours. Plus, you'll continue to invest when markets decline, so -- voilà -- you're buying low. Who knew that controlling emotions could be so easy?

http://finance.yahoo.com/focus-retirement/article/107912/be-a-better-investor.html;_ylt=ApAH9skfEtqpCrB.0qa.Qc2VBa1_;_ylu=X3oDMTFiZGM1OXZpBHBvcwMxNARzZWMDZmlkZWxpdHlBcmNoaXZlBHNsawN3aGljaGluc3RpbmM-?mod=fidelity-buildingwealth

Summary:

Rather than being emotional, investing should be rational.

Learn from the recent severe bear market. Analyse your emotions, actions and adapt strategies to optimise your investing. Here are 3 strategies:

Sponsored by

by Bob Frick

Thursday, October 8, 2009

Outsmart your emotions, cut your fees, keep it simple -- and reap higher returns.

Damn, it happened again. Ten years after the internet bubble ballooned, then burst, we're left to pick up our shattered portfolios from another cycle of hope, anxiety and regret. To make matters worse, our own actions added insult to the injury inflicted by the catastrophic bear market that ended last March.

By buying high and selling low, mutual fund investors, for instance, lost $42 billion more than they should have during the 12-month period that ended last May, estimates The Hulbert Financial Digest. (In a similar vein, columnist Russel Kinnel tells us that the typical investor earns far less than funds' reported returns.)

How could this have happened? The simple answer is that emotion, not logic, usually rules our investing habits. In many ways we're predisposed not just to buy high and sell low, but to cling to losing investments we should sell, ignore threats to our wealth and follow the investing herd off a cliff again and again.

These tendencies are now well documented in the burgeoning fields of investor psychology and behavioral finance. Scholars in both disciplines are arriving at a new understanding of how humans make decisions. For instance, in the bestseller Nudge: Improving Decisions About Health, Wealth and Happiness, authors Richard Thaler and Cass Sunstein say long-held assumptions that people "think like Albert Einstein, store as much memory as IBM's Big Blue and exercise the willpower of Mahatma Gandhi" are falling by the wayside. To help people, including investors, make better choices, we have to understand and embrace our emotions and predilections, say the authors, and figure out how to avoid becoming our own worst enemy.

Teachable Moments

But just recognizing our mental kinks won't help us undo them, experts say. "I don't believe it's possible to change behavior that's really hard-wired into our biology," says Andrew Lo, director of the Massachusetts Institute of Technology Laboratory for Financial Engineering. But "Homo sapiens can do what we've always done: adapt. We don't have wings, but we can fly. So we develop tools to protect ourselves from these emotional shortcomings."

The silver lining to the recent bear market is that painful experiences remain in our memories for a long time and provide lessons for the future. So let's review the past few years through the eyes of experts in investor psychology and behavioral finance, studying events not as a financial roller coaster, but rather as an emotional one.

Humans are wired to organize facts around stories. The Internet bubble was fueled by a fable that the Web would lead to an unending explosion of commerce. The explosion in real estate speculation that began in the early 2000s was firmly built on the same kind of fiction. Stories of people getting rich as property prices rose year after year "replicated and spread like thought viruses," says Robert Shiller, the Yale economist who warned of the Internet and real estate bubbles in different editions of his book Irrational Exuberance. Such tales instill confidence in people and inspire them to move fast to get rich themselves.

These stories proliferate even when they fly in the face of facts. That's because we tend to look only for facts that support our story, something called confirmation bias. So, for instance, real estate prices in Las Vegas and Phoenix rose at double-digit rates, as if land in those Sun Belt cities was a scarce commodity. The desire to cash in on the property boom ignored "obvious facts," says Thaler, such as a virtually "infinite supply of land" that facilitated an abundant supply of homes.

So think back to 2006. Real estate is on fire, the stock market is doing pretty well, and both investments look like sure bets. That's about the time the dangerous psychological juju started kicking in. Greg Davies, head of behavioral finance for Barclays Wealth, the London-based financial-services giant, says investors fell victim to the recency effect and began to lose their sense of caution because they'd known nothing but gains for several years.

As a result of the recency effect, says Davies, "what's most recent in our minds stands out." For instance, "if investments have been going up for a while, I start seeing them as less risky. I start thinking, Well, my budget for risky investments isn't full -- I can put more in there."

Buying Stimuli

As investors pile in and the markets continue to rise, herd behavior and regret drive our actions. One consequence of herd behavior is that it makes us think something is safe because it seems safe if everyone is doing it. And regret causes those who can't stand being left out to jump in.

Then, as our portfolios swell, we start to feel a collective buzz courtesy of dopamine, a feel-good chemical that the brain produces at the mere thought of making money (or driving a sports car or having sex). The more dopamine produced, the more decision-making is kicked to the primitive, emotional parts of our brain, making it harder for us to think logically. As the reward system gets excited, the fear centers in the brain are deactivated, says Richard Peterson, a psychiatrist who runs a hedge fund that aims to make money by taking advantage of investors' overreactions. "We're no longer able to observe the threats," says Peterson. "We observe only what we want to."

Now recall the mood in September 2008. The real estate sector is crumbling, and the stock market has been slipping for nearly a year. Uncle Sam has taken over Fannie Mae and Freddie Mac, and Bear Stearns and Lehman Brothers have failed. Investors, who couldn't wait to check their account balances when the market was rising, monitor them much less frequently now. They are suffering from the ostrich effect, a term coined by George Loewenstein, a professor of economics and psychology at Carnegie Mellon University.

Many investors who know intellectually that they're overloaded in stocks can't pull back, even if they're suffering steep losses. The reason is something called the disposition effect. On some level we feel that if we don't actually sell a stock that's underwater, we're not actually realizing the loss and the pain that goes with it.

Then, from mid September to mid October, the sum of our suppressed financial fears came to fruition. Stocks tumbled 30%. Do you remember that as an especially painful period? If you do, you're not imagining that pain. When we lose money, our brain reacts in the same way that it processes physical pain. Losing money hurts.

For many people, plunging portfolio values became too much to bear, and they just wanted the pain to end. So they sold. According to the Investment Company Institute, the greatest net monthly outflow from stock funds in the past two years -- $25 billion -- came in February 2009. The timing couldn't have been much worse for those who sold then. As it turned out, stocks bottomed on March 9 and surged about 50% over the ensuing six months.

As stocks have recovered, our emotions have begun to heal. Lo, the MIT professor, thinks most investors have already dealt with three of the five stages of grief-the denial, anger and bargaining phases-and are now working through the last two: depression and acceptance.

Now is a perfect time, while the trauma is still fresh in our minds, to figure out how to prevent similar mistakes in the future. Unfortunately, says Peterson, the psychiatrist and hedge-fund manager, the bear market was so painful that many investors don't want to think about it. As a result, he says, "five years from now they'll make the same mistakes."

So, if you recognize yourself in some of the actions (or lack thereof) we've just described, now's the time to take steps to make sure you don't suffer the same mental miscues in the future. You may not be able to change your behavior in trying times, but you can change your investing strategy to neutralize negative impulses.

One bold idea: If you handle your own investments and you find that emotions are tripping you up, hire an adviser. A good adviser should help you avoid those impulses-which typically stem from short-term fluctuations in the value of your investments-and keep you focused on meeting long-term goals. The extra cost could be worth the money.

You can also use a psychological quirk, called mental accounting, to your advantage. Mental accounting holds that even though a dollar is a dollar, we often mentally separate our wealth into different accounts. Consider opening a separate account to house your "safe" money-cash-type investments and other low-risk stuff that should hold up even during a stock-market crash. The size of your safe account depends on your risk tolerance and other factors. But while the pain of the bear market is fresh in your mind, determine how much of a cushion you need so that another 40% drop in the rest of your investments won't lead to poorly conceived actions that are driven by panic.

You may also want to tone down the risk in your other accounts as an antidote for increasing volatility in all sorts of markets. A more stable portfolio will leave you calmer and better able to make decisions based on logic rather than emotion.

Beware of merely mixing stocks and bonds, which Lo says creates "diversification deficit disorder." You need other assets, such as real estate, commodities and other alternative investments.

One of the best vaccines against emotional decision-making is the tried-and-true technique of dollar-cost averaging. By investing a fixed amount of money on a regular basis-the practice of just about anyone who participates in a 401(k) or similar retirement plan-you're conceding that you can't time the market. You avoid the temptation to buy high, or to pull out precipitously if the market sours. Plus, you'll continue to invest when markets decline, so -- voilà -- you're buying low. Who knew that controlling emotions could be so easy?

http://finance.yahoo.com/focus-retirement/article/107912/be-a-better-investor.html;_ylt=ApAH9skfEtqpCrB.0qa.Qc2VBa1_;_ylu=X3oDMTFiZGM1OXZpBHBvcwMxNARzZWMDZmlkZWxpdHlBcmNoaXZlBHNsawN3aGljaGluc3RpbmM-?mod=fidelity-buildingwealth

Summary:

Rather than being emotional, investing should be rational.

Learn from the recent severe bear market. Analyse your emotions, actions and adapt strategies to optimise your investing. Here are 3 strategies:

- By using mental accounting, create a portfolio for those good quality stocks you wish or will hold long term. This prevents you from reacting emotionally in the face of a falling market.

- Build a portfolio of stocks with lower price volatilities. This ensure that you will be subjected less to the folly of the market price fluctuations which can be huge at times.

- By using dollar cost averaging, you can have the 'gut' to invest into the market when the prices are obviously low in a falling market. Similarly, do not be carried away during the height of a bull market. This can be prevented to certain extent by dollar cost averaging strategy, though the smarter investors will probably allocate more to cash during this period.

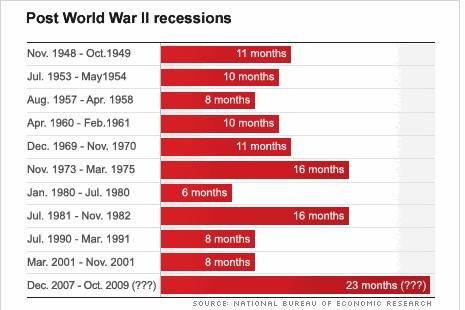

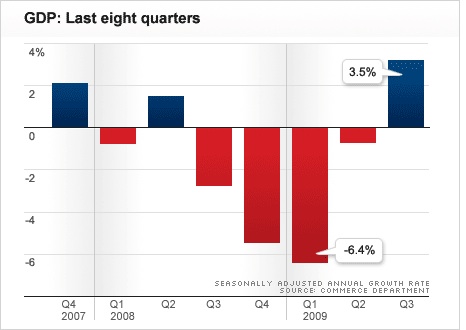

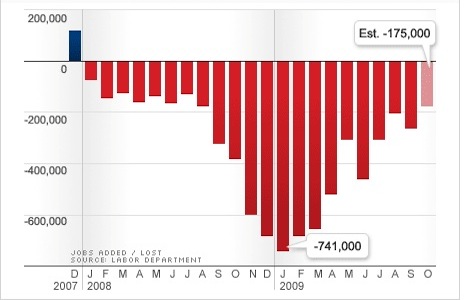

This recession is the longest we’ve had post World War II.

CNN Money just released an interesting slideshow about the state of the economy as of late. If you’re wondering about when (or whether) this economy will be *truly* turning around and whether your vague unsettling feelings about it have any basis, then these hard numbers should help give you perspective. If you’re going to get anything from this post, maybe it’s this: that this recession is the longest, most grating one we’ve had post World War II.

http://money.cnn.com/2009/10/29/news/economy/gdp/index.htm

Bear Markets Do Wonders for Retirement

Bear Markets Do Wonders for Retirement

by Joe Mont

Tuesday, October 27, 2009

The six-month bear market that wiped out nearly half of Americans' retirement savings threatens to scare away the class of investor who has the most to gain from it: young people.

Mutual fund manager T. Rowe Price says in a study that those who began to systematically invest in equities in severe bear markets were "significantly better off 30 years later than investors who began in bull markets."

The analysis charted four hypothetical investors who each contributed $500 a month (15 percent of a $40,000 annual salary) toward a retirement account that replicated the S&P 500 Index over three decades. The starting date marked a severe stock-market downturn: 1929, 1950, 1970 and 1979.

The four investors were initially hard-hit. The S&P 500, for example, had an annualized return of minus 0.9 percent from 1929 to 1938, the second-worst 10-year period in history. The benchmark index grew a mere 5.9 percent in the recessionary era of the 1970s.

But for all four investors, there was good news to go with the bad: They had the opportunity to buy at low prices, accumulating more shares for what would be coming bull markets.

By the end of their first decade, the investors were poised to shake off market drops. The projections built upon 1950 and 1979 showed the greatest success. The S&P 500 returned an annualized 19.4 percent from 1950 to 1959, and 16.3 percent from 1979 to 1988, and their nest eggs swelled to $152,359 and $137,370, respectively.

The study makes its point in dramatic fashion by pointing out that a 30-year investment that began in 1929 ended with a total gain of 960 percent. The investor who started in 1970 fared even better: 1,753 percent.

By comparing the results with investors who began saving during bull markets in the 1980s and 1990s, the four investors did twice as well with their money.

"As counterintuitive as it may feel, it is actually a silver lining that the prices have gone down," says Stuart Ritter, assistant vice president of T. Rowe Price Investment Services. "For young investors still in the accumulation phase, it is better to have the bear market first, because then you buy a whole lot of shares at a lower price than when the bull market hits."

Ritter, who also teaches a class on personal finance at John Hopkins University in Baltimore, says the younger generation is starting to embrace that message despite rampant pessimism.

"They see older people panicking, and they understand why," he says. "But they are saying, 'Gee, 2008 felt bad and people worried about it, but I'm 22 years old and it's a long time before I am going to use this money.' It is a little bit easier for them to put 2008 in perspective, which I find interesting because, for their investing lifetime, 2008 represents all of it. But they are still pretty good at putting it in perspective and saying, 'It is just one year. I have a whole lot more ahead of me.' "

Ritter says it's a challenge to keep investors, young and old, from overreacting to bubbles and cycles.

"How do we change people's perspective from what happened in the past 18 months into the broader perspective that is appropriate for their goals and time horizon?" he says. "We see it at both times [bull and bear]. At the peak of the tech boom, all people see is that, 'Tech stocks always go up; why shouldn't I have everything in stocks?' With the real-estate boom, it was, 'Real estate has been doubling; why don't I have everything in real estate?' Then it was, 'Oh, no, 2008 was a disaster; why would anyone have anything in stocks.' It is just a different variation on the same theme. Our advice is to look beyond the short term and be appropriately invested for your time horizon."

http://finance.yahoo.com/focus-retirement/article/108005/bear-markets-do-wonders-for-retirement;_ylt=AhH8Y2ATfFWh212MY3qwLOCVBa1_;_ylu=X3oDMTFiazVuNXNiBHBvcwMxMgRzZWMDZmlkZWxpdHlBcmNoaXZlBHNsawNiZWFybWFya2V0c20-?mod=fidelity-buildingwealth

by Joe Mont

Tuesday, October 27, 2009

The six-month bear market that wiped out nearly half of Americans' retirement savings threatens to scare away the class of investor who has the most to gain from it: young people.

Mutual fund manager T. Rowe Price says in a study that those who began to systematically invest in equities in severe bear markets were "significantly better off 30 years later than investors who began in bull markets."

The analysis charted four hypothetical investors who each contributed $500 a month (15 percent of a $40,000 annual salary) toward a retirement account that replicated the S&P 500 Index over three decades. The starting date marked a severe stock-market downturn: 1929, 1950, 1970 and 1979.

The four investors were initially hard-hit. The S&P 500, for example, had an annualized return of minus 0.9 percent from 1929 to 1938, the second-worst 10-year period in history. The benchmark index grew a mere 5.9 percent in the recessionary era of the 1970s.

But for all four investors, there was good news to go with the bad: They had the opportunity to buy at low prices, accumulating more shares for what would be coming bull markets.

By the end of their first decade, the investors were poised to shake off market drops. The projections built upon 1950 and 1979 showed the greatest success. The S&P 500 returned an annualized 19.4 percent from 1950 to 1959, and 16.3 percent from 1979 to 1988, and their nest eggs swelled to $152,359 and $137,370, respectively.

The study makes its point in dramatic fashion by pointing out that a 30-year investment that began in 1929 ended with a total gain of 960 percent. The investor who started in 1970 fared even better: 1,753 percent.

By comparing the results with investors who began saving during bull markets in the 1980s and 1990s, the four investors did twice as well with their money.

"As counterintuitive as it may feel, it is actually a silver lining that the prices have gone down," says Stuart Ritter, assistant vice president of T. Rowe Price Investment Services. "For young investors still in the accumulation phase, it is better to have the bear market first, because then you buy a whole lot of shares at a lower price than when the bull market hits."

Ritter, who also teaches a class on personal finance at John Hopkins University in Baltimore, says the younger generation is starting to embrace that message despite rampant pessimism.

"They see older people panicking, and they understand why," he says. "But they are saying, 'Gee, 2008 felt bad and people worried about it, but I'm 22 years old and it's a long time before I am going to use this money.' It is a little bit easier for them to put 2008 in perspective, which I find interesting because, for their investing lifetime, 2008 represents all of it. But they are still pretty good at putting it in perspective and saying, 'It is just one year. I have a whole lot more ahead of me.' "

Ritter says it's a challenge to keep investors, young and old, from overreacting to bubbles and cycles.

"How do we change people's perspective from what happened in the past 18 months into the broader perspective that is appropriate for their goals and time horizon?" he says. "We see it at both times [bull and bear]. At the peak of the tech boom, all people see is that, 'Tech stocks always go up; why shouldn't I have everything in stocks?' With the real-estate boom, it was, 'Real estate has been doubling; why don't I have everything in real estate?' Then it was, 'Oh, no, 2008 was a disaster; why would anyone have anything in stocks.' It is just a different variation on the same theme. Our advice is to look beyond the short term and be appropriately invested for your time horizon."

http://finance.yahoo.com/focus-retirement/article/108005/bear-markets-do-wonders-for-retirement;_ylt=AhH8Y2ATfFWh212MY3qwLOCVBa1_;_ylu=X3oDMTFiazVuNXNiBHBvcwMxMgRzZWMDZmlkZWxpdHlBcmNoaXZlBHNsawNiZWFybWFya2V0c20-?mod=fidelity-buildingwealth

Retiring on Investment Interest: Can It Be Done?

Retiring on Investment Interest: Can It Be Done?

Sponsored by

by Steven P. Orlowski, CFP

Thursday, October 29, 2009

provided by

The first and sometimes only retirement income plan that comes to mind for the average investor is interest only. Interest only is just what it sounds like: you are invested in interest-bearing investments and whatever interest you earn is the money you spend. This is a simple strategy, but it isn't as easy to implement as you might imagine.

The simplicity of the strategy is one of its appeals. Who hasn't thought of retirement that way? You retire with $1 million and invest the total in a portfolio of fixed-income investments at 6% and live off of the interest ($60,000 per year plus Social Security and your pension if you're so lucky). Then, at death, you leave behind the entire $1 million you started with. What could be better? As it turns out, there are some serious flaws to this approach. Let's take a look.

The Principal Principle

More from Investopedia.com:

• 5 Retirement Questions Everyone Must Answer

• 10 Retirement-Wrecking Moves

• Retire a Millionaire in 10 Steps

For starters, interest only means interest only. The principal is out of reach. This can be referred to as the "principal principle". You need all of the principal to create the income, therefore the entire principal is off limits, unless you want a declining principal balance and declining income. Let's say you implement this strategy and then need to buy a car, or put a roof on the house, and withdraw $30,000 to do it. In this case, you are left with $970,000 in principal. As a result, your income will decline from $60,000 per year to $58,200 (6% of $970,000). So even if you don't withdraw any more money for the rest of your life except the $60,000 per year in income (ignoring inflation for now), then you will still be reducing your principal every year, and by ever-increasing amounts. In year two, your principal will fall to $968,200, causing you to earn less and requiring you to withdraw even more principal in the years to come.

When Interest Only Works

A true interest-only strategy can work only for those with excess capital. If you retire with $1 million but only need $55,000 per year of supplemental income, keeping with our 6% assumption, you will need $917,000 to produce your income. That will leave you with $83,000 that could be used for emergencies or irregular expenditures.

The structure of the interest-only portfolio is simple, which can give you plenty of room to customize the portfolio for your personal preferences. The first consideration is the average yield of the portfolio. If you know you need $25,000 per year and you have $500,000 to invest, then divide $25,000 by $500,000 (25/500) and you'll get 0.05, or 5%, your cash-flow requirement. You'll also need to consider taxes, depending on what type of account you have (tax-deferred or not). Certain types of fixed-income securities may or may not be appropriate.

Once you've determined the yield you need, it's time to go shopping. Even though the yield on a fixed-income security may be lower than your target, it may still fit as a piece of your portfolio. In order to boost the average yield, you can look to other bond types, like agency, corporate and even foreign bonds. Ultimately, each investor needs to be aware of the risk inherent in each type of bond, like the risk of default or market risk and the likelihood of large price fluctuations. You can even lose money with Treasuries if you sell them at the wrong time.

In addition to diversifying the portfolio by type of bond, you can and should also buy bonds with varying maturities (called laddering). This will help you hedge against some of the aforementioned risks.

Mutual Funds and Interest Only

Some investors try to use mutual funds for their interest-only strategies, but this is not really interest only. Theoretically, it could work, so long as the funds being used pay out a consistent amount of interest. But since bonds mature, bond mutual funds' interest payments don't stay the same. In years of lower interest, you'd likely be forced to liquidate principal, which is more akin to a systematic withdrawal plan, which is in violation of the principal principle. Investing in a portfolio of mutual funds is easier than building a portfolio of fixed-income securities but it does not provide the same benefits.

Deferred Annuities

Another useful tool is the fixed deferred annuity. A fixed deferred annuity is an interest-bearing account with similar characteristics to a certificate of deposit (CD). Unlike a CD, it is not FDIC insured, although most have guaranteed principal and interest. Deferred annuities are often overlooked as an option, but the interest rates on fixed annuities are frequently, if not usually, higher than CDs and Treasuries; they also provide a high level of safety.

Remember that there are many types of annuities. For an interest-only strategy, a fixed deferred annuity is appropriate. A fixed immediate (income) annuity is not; neither is a variable deferred or variable immediate annuity. You want predictable interest coupled with safety of principal. Immediate annuities use up the principal and variable annuities, like mutual funds, can decline (or increase) in value. Each type has its place, but for an interest-only strategy, fixed deferred is the one.

The Hidden Problem: Inflation

Inflation will likely always be a problem. The historical rate of inflation is about 3% per year. In our original scenario - the retiree with $1 million and a 6% yield - we ignored the impact of inflation. Unfortunately, that person might immediately experience erosion of the portfolio because by year two, $60,000 could be insufficient. This is critical. We don't want to accidentally violate the principal principle, but if we do violate it, we want to do so intentionally. Some people do retire and decide up front to allow some erosion. Managed erosion is OK. Accidental erosion is not. Therefore, when establishing a retirement income plan, you need to inflate your income need to the end of your planning period (life expectancy). Our fictional retiree would not be living on $60,000 for long after inflation is taken into consideration. This is a big strike against interest only. A portfolio of fixed-income securities offers little to no opportunity for inflation protection (except for Treasury inflation protected securities (TIPS)). This is also why you really need to have excess savings to do interest-only properly.

The Bottom Line

Ideally, if you've done your homework and have accurately concluded that interest only is not only doable but sustainable, you'll want to blend your holdings, using bonds, CDs and annuities, into a "rainbow portfolio". All portfolios, regardless of strategy, should have elements of a rainbow in them. A rainbow covers the entire spectrum of color, which means that a rainbow portfolio should be as well diversified as possible. Use many types of securities and stagger the maturities to create that ladder. You'll be happier and more successful if you do.

Be thorough and careful when working out the numbers. Interest-only portfolios can work, but if you assume that one will work for you without working out the details, you may find yourself without adequate retirement funds.

by Steven P. Orlowski

Steven P. Orlowski, CFP® is President of Orlowski Financial Counsel, LLC, a Registered Investment Advisor providing fee-based Financial Planning, Portfolio Management and Insurance and Investment Advisory services. Steven is a twenty year veteran of the financial services industry, having served in the capacity of a stock broker, trader, financial planner and portfolio manager during that time.

http://finance.yahoo.com/focus-retirement/article/108036/retiring-on-investment-interest-can-it-be-done;_ylt=AkcUF0S50n0tA9ITMnCqZ8SVBa1_;_ylu=X3oDMTFiNWI2ODRnBHBvcwMyNgRzZWMDZmlkZWxpdHlBcmNoaXZlBHNsawNyZXRpcmluZ29uaW4-?mod=fidelity-managingwealth

Sponsored by

by Steven P. Orlowski, CFP

Thursday, October 29, 2009

provided by

The first and sometimes only retirement income plan that comes to mind for the average investor is interest only. Interest only is just what it sounds like: you are invested in interest-bearing investments and whatever interest you earn is the money you spend. This is a simple strategy, but it isn't as easy to implement as you might imagine.

The simplicity of the strategy is one of its appeals. Who hasn't thought of retirement that way? You retire with $1 million and invest the total in a portfolio of fixed-income investments at 6% and live off of the interest ($60,000 per year plus Social Security and your pension if you're so lucky). Then, at death, you leave behind the entire $1 million you started with. What could be better? As it turns out, there are some serious flaws to this approach. Let's take a look.

The Principal Principle

More from Investopedia.com:

• 5 Retirement Questions Everyone Must Answer

• 10 Retirement-Wrecking Moves

• Retire a Millionaire in 10 Steps

For starters, interest only means interest only. The principal is out of reach. This can be referred to as the "principal principle". You need all of the principal to create the income, therefore the entire principal is off limits, unless you want a declining principal balance and declining income. Let's say you implement this strategy and then need to buy a car, or put a roof on the house, and withdraw $30,000 to do it. In this case, you are left with $970,000 in principal. As a result, your income will decline from $60,000 per year to $58,200 (6% of $970,000). So even if you don't withdraw any more money for the rest of your life except the $60,000 per year in income (ignoring inflation for now), then you will still be reducing your principal every year, and by ever-increasing amounts. In year two, your principal will fall to $968,200, causing you to earn less and requiring you to withdraw even more principal in the years to come.

When Interest Only Works

A true interest-only strategy can work only for those with excess capital. If you retire with $1 million but only need $55,000 per year of supplemental income, keeping with our 6% assumption, you will need $917,000 to produce your income. That will leave you with $83,000 that could be used for emergencies or irregular expenditures.

The structure of the interest-only portfolio is simple, which can give you plenty of room to customize the portfolio for your personal preferences. The first consideration is the average yield of the portfolio. If you know you need $25,000 per year and you have $500,000 to invest, then divide $25,000 by $500,000 (25/500) and you'll get 0.05, or 5%, your cash-flow requirement. You'll also need to consider taxes, depending on what type of account you have (tax-deferred or not). Certain types of fixed-income securities may or may not be appropriate.

Once you've determined the yield you need, it's time to go shopping. Even though the yield on a fixed-income security may be lower than your target, it may still fit as a piece of your portfolio. In order to boost the average yield, you can look to other bond types, like agency, corporate and even foreign bonds. Ultimately, each investor needs to be aware of the risk inherent in each type of bond, like the risk of default or market risk and the likelihood of large price fluctuations. You can even lose money with Treasuries if you sell them at the wrong time.

In addition to diversifying the portfolio by type of bond, you can and should also buy bonds with varying maturities (called laddering). This will help you hedge against some of the aforementioned risks.

Mutual Funds and Interest Only

Some investors try to use mutual funds for their interest-only strategies, but this is not really interest only. Theoretically, it could work, so long as the funds being used pay out a consistent amount of interest. But since bonds mature, bond mutual funds' interest payments don't stay the same. In years of lower interest, you'd likely be forced to liquidate principal, which is more akin to a systematic withdrawal plan, which is in violation of the principal principle. Investing in a portfolio of mutual funds is easier than building a portfolio of fixed-income securities but it does not provide the same benefits.

Deferred Annuities

Another useful tool is the fixed deferred annuity. A fixed deferred annuity is an interest-bearing account with similar characteristics to a certificate of deposit (CD). Unlike a CD, it is not FDIC insured, although most have guaranteed principal and interest. Deferred annuities are often overlooked as an option, but the interest rates on fixed annuities are frequently, if not usually, higher than CDs and Treasuries; they also provide a high level of safety.

Remember that there are many types of annuities. For an interest-only strategy, a fixed deferred annuity is appropriate. A fixed immediate (income) annuity is not; neither is a variable deferred or variable immediate annuity. You want predictable interest coupled with safety of principal. Immediate annuities use up the principal and variable annuities, like mutual funds, can decline (or increase) in value. Each type has its place, but for an interest-only strategy, fixed deferred is the one.

The Hidden Problem: Inflation

Inflation will likely always be a problem. The historical rate of inflation is about 3% per year. In our original scenario - the retiree with $1 million and a 6% yield - we ignored the impact of inflation. Unfortunately, that person might immediately experience erosion of the portfolio because by year two, $60,000 could be insufficient. This is critical. We don't want to accidentally violate the principal principle, but if we do violate it, we want to do so intentionally. Some people do retire and decide up front to allow some erosion. Managed erosion is OK. Accidental erosion is not. Therefore, when establishing a retirement income plan, you need to inflate your income need to the end of your planning period (life expectancy). Our fictional retiree would not be living on $60,000 for long after inflation is taken into consideration. This is a big strike against interest only. A portfolio of fixed-income securities offers little to no opportunity for inflation protection (except for Treasury inflation protected securities (TIPS)). This is also why you really need to have excess savings to do interest-only properly.

The Bottom Line

Ideally, if you've done your homework and have accurately concluded that interest only is not only doable but sustainable, you'll want to blend your holdings, using bonds, CDs and annuities, into a "rainbow portfolio". All portfolios, regardless of strategy, should have elements of a rainbow in them. A rainbow covers the entire spectrum of color, which means that a rainbow portfolio should be as well diversified as possible. Use many types of securities and stagger the maturities to create that ladder. You'll be happier and more successful if you do.

Be thorough and careful when working out the numbers. Interest-only portfolios can work, but if you assume that one will work for you without working out the details, you may find yourself without adequate retirement funds.

by Steven P. Orlowski

Steven P. Orlowski, CFP® is President of Orlowski Financial Counsel, LLC, a Registered Investment Advisor providing fee-based Financial Planning, Portfolio Management and Insurance and Investment Advisory services. Steven is a twenty year veteran of the financial services industry, having served in the capacity of a stock broker, trader, financial planner and portfolio manager during that time.

http://finance.yahoo.com/focus-retirement/article/108036/retiring-on-investment-interest-can-it-be-done;_ylt=AkcUF0S50n0tA9ITMnCqZ8SVBa1_;_ylu=X3oDMTFiNWI2ODRnBHBvcwMyNgRzZWMDZmlkZWxpdHlBcmNoaXZlBHNsawNyZXRpcmluZ29uaW4-?mod=fidelity-managingwealth

How to Make Your Money Last

How to Make Your Money Last

by Walter Updegrave

Wednesday, September 23, 2009

There are ways to guarantee you won't run out of income, regardless of what the market does next — but you'll have to make some tradeoffs to do so.

Once you have your Social Security strategy down, there's just one little retirement question left to consider: How can you make the money that you've so diligently saved provide the life you want for as long as you live? Oh. That.

Figuring out how to draw secure retirement income from a portfolio is a challenge in the best of times; today it's made more complicated by fear. Having seen the worst-case scenario unfold in the past year, you've probably gone into loss-avoidance mode. But deflecting market risk leaves you vulnerable to inflation risk — and the risk that you'll outlive your money. So hiding in cash won't save you.

"No one investment can protect you from every risk you'll face," says John Ameriks, head of Vanguard Investment Counseling & Research. What you need, rather, is a basket of investments that provides:

1. Stable income you're not likely to outlive.

2. The potential for that income to grow to beat inflation.

3. The ability to access cash to meet unexpected needs.

4. Adequate protection from market downturns.

Here are three smart strategies to achieve those goals. The second offers the best chance of making your money last; however, you'll lose access to a big chunk of your savings. The others give you more control, but less certainty. There's no free lunch in retirement — but the menu that follows presents some interesting options.

Strategy 1: The Traditional Stock-and-Bond Portfolio

You're a Candidate if ...

You have enough income from Social Security and pensions to cover most of your basic expenses (so you could weather a market storm) and/or you're confident in your ability to manage your portfolio.

The Premise: You invest in a diversified portfolio of stocks, bonds, and cash that has the potential to generate current income and capital gains. You pull out money as needed, starting off with a 4% annual withdrawal — $40,000 on a $1 million portfolio — then increasing the dollar amount by the inflation rate each year.

Done correctly, this gives you a 77% shot of your money lasting 30 years, says Ibbotson Associates. The higher the withdrawal rate, the lower your odds. So this strategy may not work if you need more income than 4% would provide.

The Drawbacks: A sizable loss early in retirement could undo you. If your portfolio loses 20% the first year, the chances of your savings lasting 30 years could drop to roughly 50%. Alternatively, if the market does well over the long run, you could be left with a huge sum late in life, so you would have lived more frugally than you had to.

How to Pull It Off: Allocation is key. Going 100% into bonds might protect you from a market meltdown, but such cataclysms are rare. And you'd lose out on inflation protection. Loading up on stocks gives you a better shot at increasing your income, yet you may get mauled by a bear market. So aim for the middle ground: For someone just entering retirement, a broadly diversified fifty-fifty stock-to-bond blend like the one in the chart above, right is a reasonable starting point.

You also have to be flexible with withdrawals. In a declining market you may have to skip the inflation boost or scale back the amount you draw down. Conversely, if the markets go on a run, you may be able to take more. Check yearly at T. Rowe Price's Retirement Income Calculator.

Finally, be strategic in the way you tap assets. Start with taxable accounts; then tax-deferred (401(k)s and traditional IRAs); then tax-free Roths. That way the latter accounts compound longer without the drag of taxes, so you can build bigger balances and draw more income over time.

Strategy 2: Stocks, Bonds — and an Immediate Annuity

You're a Candidate if ...

You need more income for basic expenses than you'll get from Social Security and pensions. Or you'd like to avoid subjecting all your savings to market volatility.

The Premise: Invest a portion of your savings in a lifetime immediate annuity, an insurance product that will send you fixed monthly checks for as long as you and/or your spouse live. You'll manage the rest of your portfolio as in Strategy 1. The payoff: You'll have another layer of guaranteed income and still have funds to tap.

This strategy provides longer income security than the first because the payout from an immediate annuity can't be easily matched by another sure-bet investment. Recently immediate annuities paid out roughly 8% for a 65-year-old man, or about $40,000 a year on $500,000. You'd have to invest significantly more to get the same assured lifetime income from long-term Treasuries. The reason immediate annuities pay so well? Investors' money is pooled, allowing insurers to essentially transfer funds from early croakers to those who hang on past life expectancy.

The Drawbacks: Once you hand over, say, a few hundred grand for an immediate annuity, you typically give up access to the money. You can't use it for a new roof or a vacation in France, or pass it down to your kids. Plus, if you're hit by a bus early in retirement, the annuity will have paid out less than you put in. For those reasons, many people perceive immediate annuities as potentially wasted money.

Another concern: Annuity payments are usually fixed, meaning they'll be worth less over time because of inflation. A few insurers offer inflation-adjusted immediate annuities, but the payouts start considerably lower.

Finally, while annuities eliminate market and longevity risk, they introduce another risk: Your income security is based on the financial health of the insurer.

How to Pull It Off: In reality, money in an annuity is no more "wasted" than the premiums you pay to insure your house. So try to get over that psychological hurdle, since this strategy presents your best chance of maintaining income.

To make it work, you want to devote enough to the annuity so that the income, along with Social Security and pensions, covers your basic expenses. But you don't want to go overboard, as you'll lose too much liquidity. Plus, you'll need to use what's left to try to beat inflation, since your annuity payments won't.

There's no one "right" mix. Splitting savings fifty-fifty between an immediate annuity and a diversified portfolio can provide the same 4% inflation-adjusted income as in Strategy 1 — but with a 99% chance of lasting 30 years. If you can live with less certainty, you can boost your income to, say, 4.5% by drawing more from your portfolio. Or, you could invest less in the annuity.

Consider buying in stages. That prevents you from over-committing and from investing all your money when interest rates — which drive payouts — are lowest. To mitigate the risk of insurer failure, stick to companies highly rated by Standard & Poor's and A.M. Best, then spread your money among two or three companies. Check at nolhga.com that the amount you'll invest with each company is covered by your state's insurance guaranty association.

Strategy 3: All of the Above, Plus a Variable Annuity

You're a Candidate if ...

You need more income than Social Security and pensions will provide, but you want access to more of your savings than Strategy 2 allows.

The Premise: While maintaining a stock/bond portfolio, you'll also invest a portion of savings in an immediate annuity and a portion in a variable annuity with a guaranteed lifetime withdrawal benefit (a.k.a. VA with GLWB), an investment account promising a minimum withdrawal for the rest of your life.

In a VA with GLWB, you choose the investments, within limits. You can dip into the account as needed. And you can typically leave the greater of (a) the account balance or (b) your original investment minus withdrawals to your heirs. So it's more flexible than an immediate annuity.

The other advertised benefit: Your income has the potential to grow if your investments appreciate. Say you invest $250,000 and are guaranteed 5%, or $12,500 a year. If, on your contract anniversary date, a rising market has pushed your balance to $300,000 after fees, your 5% will be applied to that amount, boosting your income to $15,000.

Even if a market crash later knocks your account to $200,000, you're still guaranteed 15 grand (though if you want to cash out, you're limited to the actual account value).

The Drawbacks: Flexibility comes at a price. First, variable annuities pay significantly less than immediate annuities, only about 5% for a 65-year-old. Second, the plans come with such high fees, often 3% or more a year, that it's difficult for your account value to grow at all, let alone keep pace with inflation. Third, though you can draw more than your guaranteed amount from the account, doing so will reduce your income for future years. Last, you face the same insurer risks as in Strategy 2.

How to Pull It Off: The high fees and low payout of the VA explain why you need an immediate annuity in the mix: Without it, the odds of maintaining your target income are slightly lower than with a stock/bond portfolio alone.

Together you want the payouts, along with Social Security and pensions, to cover your basic expenses. So how much in each? The more you put in the variable annuity vs. the immediate, the more of your assets you'll have access to.

In exchange, you'll settle for a lower guaranteed payout. A reasonable mix: Put 25% of savings into an immediate annuity, put 25% in a VA, and invest the other 50%. That gives you a 92% chance of getting the income you want for 30 years. You'll end up giving away more of your savings to fees than with the other strategies, but, alas, you have to pay for security one way or another.

http://finance.yahoo.com/focus-retirement/article/107791/how-to-make-your-money-last.html;_ylt=AlsUAXxZXh4WfyMFKaxAuD.VBa1_;_ylu=X3oDMTFiYmtsc242BHBvcwMyOQRzZWMDZmlkZWxpdHlBcmNoaXZlBHNsawNob3d0b21ha2V5b3U-?mod=fidelity-managingwealth

by Walter Updegrave

Wednesday, September 23, 2009

There are ways to guarantee you won't run out of income, regardless of what the market does next — but you'll have to make some tradeoffs to do so.

Once you have your Social Security strategy down, there's just one little retirement question left to consider: How can you make the money that you've so diligently saved provide the life you want for as long as you live? Oh. That.

Figuring out how to draw secure retirement income from a portfolio is a challenge in the best of times; today it's made more complicated by fear. Having seen the worst-case scenario unfold in the past year, you've probably gone into loss-avoidance mode. But deflecting market risk leaves you vulnerable to inflation risk — and the risk that you'll outlive your money. So hiding in cash won't save you.

"No one investment can protect you from every risk you'll face," says John Ameriks, head of Vanguard Investment Counseling & Research. What you need, rather, is a basket of investments that provides:

1. Stable income you're not likely to outlive.

2. The potential for that income to grow to beat inflation.

3. The ability to access cash to meet unexpected needs.

4. Adequate protection from market downturns.

Here are three smart strategies to achieve those goals. The second offers the best chance of making your money last; however, you'll lose access to a big chunk of your savings. The others give you more control, but less certainty. There's no free lunch in retirement — but the menu that follows presents some interesting options.

Strategy 1: The Traditional Stock-and-Bond Portfolio

You're a Candidate if ...

You have enough income from Social Security and pensions to cover most of your basic expenses (so you could weather a market storm) and/or you're confident in your ability to manage your portfolio.

The Premise: You invest in a diversified portfolio of stocks, bonds, and cash that has the potential to generate current income and capital gains. You pull out money as needed, starting off with a 4% annual withdrawal — $40,000 on a $1 million portfolio — then increasing the dollar amount by the inflation rate each year.

Done correctly, this gives you a 77% shot of your money lasting 30 years, says Ibbotson Associates. The higher the withdrawal rate, the lower your odds. So this strategy may not work if you need more income than 4% would provide.

The Drawbacks: A sizable loss early in retirement could undo you. If your portfolio loses 20% the first year, the chances of your savings lasting 30 years could drop to roughly 50%. Alternatively, if the market does well over the long run, you could be left with a huge sum late in life, so you would have lived more frugally than you had to.

How to Pull It Off: Allocation is key. Going 100% into bonds might protect you from a market meltdown, but such cataclysms are rare. And you'd lose out on inflation protection. Loading up on stocks gives you a better shot at increasing your income, yet you may get mauled by a bear market. So aim for the middle ground: For someone just entering retirement, a broadly diversified fifty-fifty stock-to-bond blend like the one in the chart above, right is a reasonable starting point.

You also have to be flexible with withdrawals. In a declining market you may have to skip the inflation boost or scale back the amount you draw down. Conversely, if the markets go on a run, you may be able to take more. Check yearly at T. Rowe Price's Retirement Income Calculator.

Finally, be strategic in the way you tap assets. Start with taxable accounts; then tax-deferred (401(k)s and traditional IRAs); then tax-free Roths. That way the latter accounts compound longer without the drag of taxes, so you can build bigger balances and draw more income over time.

Strategy 2: Stocks, Bonds — and an Immediate Annuity

You're a Candidate if ...

You need more income for basic expenses than you'll get from Social Security and pensions. Or you'd like to avoid subjecting all your savings to market volatility.

The Premise: Invest a portion of your savings in a lifetime immediate annuity, an insurance product that will send you fixed monthly checks for as long as you and/or your spouse live. You'll manage the rest of your portfolio as in Strategy 1. The payoff: You'll have another layer of guaranteed income and still have funds to tap.

This strategy provides longer income security than the first because the payout from an immediate annuity can't be easily matched by another sure-bet investment. Recently immediate annuities paid out roughly 8% for a 65-year-old man, or about $40,000 a year on $500,000. You'd have to invest significantly more to get the same assured lifetime income from long-term Treasuries. The reason immediate annuities pay so well? Investors' money is pooled, allowing insurers to essentially transfer funds from early croakers to those who hang on past life expectancy.

The Drawbacks: Once you hand over, say, a few hundred grand for an immediate annuity, you typically give up access to the money. You can't use it for a new roof or a vacation in France, or pass it down to your kids. Plus, if you're hit by a bus early in retirement, the annuity will have paid out less than you put in. For those reasons, many people perceive immediate annuities as potentially wasted money.

Another concern: Annuity payments are usually fixed, meaning they'll be worth less over time because of inflation. A few insurers offer inflation-adjusted immediate annuities, but the payouts start considerably lower.

Finally, while annuities eliminate market and longevity risk, they introduce another risk: Your income security is based on the financial health of the insurer.

How to Pull It Off: In reality, money in an annuity is no more "wasted" than the premiums you pay to insure your house. So try to get over that psychological hurdle, since this strategy presents your best chance of maintaining income.

To make it work, you want to devote enough to the annuity so that the income, along with Social Security and pensions, covers your basic expenses. But you don't want to go overboard, as you'll lose too much liquidity. Plus, you'll need to use what's left to try to beat inflation, since your annuity payments won't.

There's no one "right" mix. Splitting savings fifty-fifty between an immediate annuity and a diversified portfolio can provide the same 4% inflation-adjusted income as in Strategy 1 — but with a 99% chance of lasting 30 years. If you can live with less certainty, you can boost your income to, say, 4.5% by drawing more from your portfolio. Or, you could invest less in the annuity.

Consider buying in stages. That prevents you from over-committing and from investing all your money when interest rates — which drive payouts — are lowest. To mitigate the risk of insurer failure, stick to companies highly rated by Standard & Poor's and A.M. Best, then spread your money among two or three companies. Check at nolhga.com that the amount you'll invest with each company is covered by your state's insurance guaranty association.

Strategy 3: All of the Above, Plus a Variable Annuity

You're a Candidate if ...

You need more income than Social Security and pensions will provide, but you want access to more of your savings than Strategy 2 allows.