Options have many uses and investors need to be aware of their ramifications in order to be able to use them.

In order to do so, investors need to familiarize themselves with knowledge about options.

Learning the Vocabulary

Options: They are stock derivative investments.

Derivative security: A financial security that derives its value from another security.

Options and futures: These are stock derivatives that offer investors some of the benefits of stocks without having to own them.

Options contract: This gives the holder the right to buy or sell shares of a particular common stock at a predetermined price (strike price) on or before a specified date (expiration date).

Option: An option is a right, not an obligation, to buy or to sell stock at a specified price before or on an expiration date.

Strike price: The price at which the holder of the option can buy or sell the stock.

Expiration date: An option expires on its expiration date.

Stock Option: This is a derivative security because its value depends on the underlying security, which is the common stock of the company.

Options market: Chicago Board Options Exchange (CBOE), New York Stock Exchange (NYSE), the American Options Exchange (AOE), the Philadelphia Exchange (PHO), and the Pacific Exchange (PSE). Options can also be traded in the over-the-counter market.

Options websites: www.cboe.com, www.nyse.com/futuresoptions/nyseamex, www.amex.com, www.phlx.com. Click on all exchanges and list all options and LEAPS. Click on Submit, and a list of options for the stock you requested will appear.

Options contracts: Calls and Puts

Call option: A call option gives the option owner the right to buy shares of the underlying company at a predetermined price (strike price) before expiration.

Put option: A put option contract gives the option owner the right to sell shares of the underlying company at the strike price before expiration.

Option holder: Option holder has the right to convert the contract at his/her discretion. It is not an obligation. Holders of the option can exercise the option when it is to their advantage and let the options contract expire if it is not advantageous.

Options contract: SIX items of note in an options contract. 1. Name of the company whose shares can be bought or sold. 2. The number of shares that can be bought or sold, generally 100 shares per contract. 3. The exercise or strike price, which is the stated purchase or sale price of the shares in the contract. 4. The expiration date, which is the date when the option to buy or sell expires. 5. The settlement procedure. 6. The options exercise style.

Option buyer: The option buyer is also referred to as the option holder.

Option seller: The seller of the original contract is referred to as the option writer. In any contract, there are at least two parties: buyers and sellers.

Settlement procedure: This is stipulated for stock options, which indicates when delivery of the underlying common stock takes place after the holder exercises the option.

Options exercise style: There are two basic exercise styles that determine when the option can be exercised, namely, American style and European style.

American style: Options on individual stocks can be exercised ANY time before the expiration date.

European style: Stock index options can be exercised ONLY on expiration date.

Life of the option: The expiration date is also important, as it specifies the life of the option.

Standardized expiration dates: The expiration dates are standardized for options contracts listed on the exchanges. There are three cycles for listed option expirations, and each option is assigned to one of these cycles: January cycle: January-April-July-October; February:cycle: February-May-August-November; and March cycle: March-June-September-December.

Options Clearing Corporation (OCC): The trading of options is greatly facilitated by the Options Clearing Corporation, which, besides maintaining a liquid marketplace, also keeps track of the options and the positions of each investor. Buyers and writers of options do not deal directly with one another but instead with the OCC.

Contract period for stock options: The contract period for stock options is standardized with three-, six-, and nine-month expiration dates. Generally, two options on a stock are introduced to the market at the same time with identical terms except for the strike (exercise) price.

LEAPS (long-term equity anticipation securities): Longer-term options contracts, called LEAPS have life spans of up to three years before expiry. They have similar characteristics to the short-term options contracts but, because of their longer expiration periods, have higher premium prices.

Time value of an option: An option is a wasting asset. There is a time value to the price of an option. The more time before the option expires, the greater is the time value of the option. As the option moves closer to its expiration, so the time value of the option decreases in value. Generally, options are not normally exercised until they are close to expiry because an earlier exercise means throwing away the remaining time value. Another generalization with options (both calls and puts) is that most options are not bought with the intention of exercising them. Instead, they are bought with the intention of selling them.

Intrinsic value of the call option: The intrinsic value of a call option is the difference between the market price of the stock and the strike price. Intrinsic Value of Call Option = Market Price of the Stock - Strike Price.

In the money call option: When the market price is greater than the strike price, the call option is said to be in the money.

Out of the money call option: A call option is said to be out of the money when the market price of the stock is less than the strike price.

At the money call option: The market price of the option equals the strike price.

Time value of put option: Puts are wasting assets and have no value at expiration.

Intrinsic value of put option: The intrinsic value of the put option is determined by subtracting the market price of the stock from the strike price. Intrinsic Value of a Put Option = Strike Price - Market Price of the Stock.

Out of the money put option: If the put option has no intrinsic value, it is out of the money.

In the money put option: If the put option has intrinsic value, it is in the money; and it is profitable to exercise the put option.

At the money put option: If the strike price equals the market price of the stock, the option is at the money.

Writing options: Investors can also write or sell options, which provide additional income from the premiums received from the buyers of the option contracts. The upside potential to this strategy for option writers is limited, however, because the most money the writer can make is the amount of the option premium.

Writing covered option: A covered option is an option that is written against an underlying stock that is owned, or sold short, by the writer. The writer of the option owns the stock against which the options are written.

Writing naked option: This is the second method of writing an option. A naked option, is an option written on an underlying stock that is not owned or sold short by the writer.

Writing covered calls: A covered call limits the appreciation the writer can realize. Therefore, it is a good idea to write covered calls on the stocks you think won't rise or fall very much in price.

Writing naked call: Writing a naked call on a stock is more risky than writing a covered call because of the potential for unlimited losses. A naked call is when the writer does not own the underlying stock, which would limit the losses if the stock rocketed up in the price. Investors can profit from writing naked calls on stocks whose prices either decline or remain relatively flat below the strike price for calls.

Writing covered puts: The writer of a covered put sells short the underlying stock and receives a premium for the covered put. If the option is exercised, the writer would buy back the stock at the strike price and use the shares to close out his short position.

Writing naked puts: The writer of a put option expects the stock to rise or at best not fall in price. If the put writer does not own the underlying stock, the contract is a naked or uncovered put, which necessitates that the writer deposits an amount of money with the brokerage firm for the required margin.Without owning the underlying stocks, the potential loss is not cushioned if the price of the stock falls rapidly.

Combination of Puts and Calls: Straddle and Spread

Straddle: A straddle is the purchase (or sale) of a put and a call with the same strike price and the same expiration date.

Spread: A spread is the purchase or sale of a combination of put and call options contracts with different strike prices.

Stock Index Options: Stock index options allow investors to take long and short positions on the market without having to buy or sell short the stocks that make up the index. A stock index option is a put or call written on a market index. With stock index options you can track the markets without having to buy or sell the stocks. Options on stock indices are valued and trade in the same way as options on individual stocks with the notable exceptions that settlement is made in cash for the former.

Rights: A right, also known as a preemptive right, is an option allowing a shareholder to by additional shares of new stock of the company at a specified price within a specified time period before the shares are offered to the public. A right allows a current shareholder to buy more common stock of the company in advance of the public at a discounted price (subscription price). Stock rights are issued to existing shareholders on a stated date. These rights give existing shareholders the opportunity to maintain their same proportionate ownership in the company after the new issue of common stock. Rights, like options, can be bought for one of two reasons: either to exercise the rights or to speculate on the rights.

Trading cum rights: To be eligible to buy these additional shares at the subscription price, the common stock of the company must be owned as of the record date set by the board of directors. Most rights offering have a short period of time (between two and six weeks) for existing shareholders to either subscribe to the new shares or sell the rights. It is during this period that the stock is said to be trading cum rights, where the value of the right is included in the market price of the stock.

Trading ex-rights date: After a specified date, known as the ex-rights date, stock transactions do not include the rights. Theoretically, the stock price goes down after this date, when the rights trade separately.

Value of a right: The value of a right depends on the market price of the stock, the subscription price of the right, and the number of rights necessary to buy each new share.

Cum Rights Value: The formula to determine the value of the rights before they trade independently of the stock is as follows: Cum Rights Value = (Market Price of Stock - Subscription Price) / (Number of Rights to Buy a Share + 1)

Ex-rights Value: After the stock trades ex-rights, its price declines by the value of the right, because rights trade separately from the stock. Investors who want to buy the rights can purchase them on the market in the same way they can purchase the stock. The ex-rights value is calculated as follows; Ex-rights Value = (Market Price of Stock - Subscription Price) / (Number of Rights Needed to Buy a Share)

Warrants: A warrant is a security that allows its owner to purchase a stated number of shares of common stock at a specified price within a specified time period. A warrant is similar to a long-term option in that it gives the owner the right to by a stated number of shares of the underlying company's stock at a specific price within a specific period of time. The differences between warrants and options are that with warrants the specified price can be fixed or it can rise at certain intervals, such as every five years, and the company can extend the expiration date. Warrants have longer lives than options. An option can have a life of nine months or less; warrants extend for years, and some companies have issued perpetual warrants. Generally, there is a waiting period before warrants can be exercised. Corporations issue warrants as sweeteners with other securities issued by the company. Warrants can be attached to bonds or preferred stocks. In some cases, warrants have been distributed to shareholders in place of stock or cash dividends. The major advantage of warrants over options is that warrants have longer lives. Warrants do well when stock prices are rising, but investors should still be selective about the warrants they buy. If the stock never goes up in price, there is little to no opportunity to profit from buying the warrants. Generally, as with options, warrants should be bought to trade and not to exercise.

Value of a warrant: When a company issues warrants, the purchase price of the stock is generally fixed at a higher price than the market price of the stock at issue. Value of a warrant = (Market price of stock - Exercise price ) x (Number of shares purchased with the warrant).

Premium of a warrant: Premium = Market price of the warrant - Value of the warrant. If the market price of the stock never rises to the strike price of the warrant during its life, the warrant is not exercised and expires.

Related:

http://www.investlah.com/forum/index.php/topic,42222.0.html

Thursday 20 February 2014

Tuesday 18 February 2014

Everything You Need to Know About Personal Investing in One Page

Scott Adams - Dilbert and the Way of the Weasel

"Everything You Need to Know About Personal Investing."

1. Make a will

2. Pay off your credit cards.

3. Get term life insurance if you have a family to support.

4. Fund your 401k to the maximum.

5. Fund your IRA to the maximum.

6. Buy a house if you want to live in a house and you can afford it.

7. Put six month's expenses in a money market account.

8. Take whatever money is left over and invest 70 percent in a stock index fund and 30 percent in a bond fund through any discount broker and never touch it until retirement.

9. If any of this confuses you, or if you have something special going on (retirement, college planning , tax issues), hire a fee-based financial planner.

"Everything You Need to Know About Personal Investing."

1. Make a will

2. Pay off your credit cards.

3. Get term life insurance if you have a family to support.

4. Fund your 401k to the maximum.

5. Fund your IRA to the maximum.

6. Buy a house if you want to live in a house and you can afford it.

7. Put six month's expenses in a money market account.

8. Take whatever money is left over and invest 70 percent in a stock index fund and 30 percent in a bond fund through any discount broker and never touch it until retirement.

9. If any of this confuses you, or if you have something special going on (retirement, college planning , tax issues), hire a fee-based financial planner.

Sunday 16 February 2014

Courage becomes the supreme virtue after adequate knowledge and a tested judgment are at hand.

A fourth business rule is more positive: “Have the courage of

your knowledge and experience. If you have formed a conclusion

from the facts and if you know your judgment is sound, act on it—

even though others may hesitate or differ.” (You are neither right

nor wrong because the crowd disagrees with you. You are right

because your data and reasoning are right.) Similarly, in the world

of securities, courage becomes the supreme virtue after adequate

knowledge and a tested judgment are at hand.

Fortunately for the typical investor, it is by no means necessary for his success that he bring these qualities to bear upon his pro- gram—provided he limits his ambition to his capacity and confines his activities within the safe and narrow path of standard, defen- sive investment. To achieve satisfactory investment results is easier than most people realize; to achieve superior results is harder than it looks.

Benjamin Graham

The Intelligent Investor

Fortunately for the typical investor, it is by no means necessary for his success that he bring these qualities to bear upon his pro- gram—provided he limits his ambition to his capacity and confines his activities within the safe and narrow path of standard, defen- sive investment. To achieve satisfactory investment results is easier than most people realize; to achieve superior results is harder than it looks.

Benjamin Graham

The Intelligent Investor

Thursday 13 February 2014

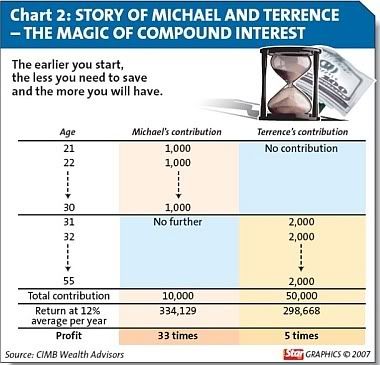

The FRIEND of your cash - The Magic of Compounding

Know the enemy of your cash: INFLATION

Know the friend of your cash: COMPOUNDING

Michael saved $1,000 per year from age of 21 for 10 years.

Terrence saved $2,000 per year from the age of 31 for 25 years.

Assuming they both had the same rate of return at 12% per year, at the age of 55 years, Michael grew his money more than Terrence.

The earlier you start, the less you need to save and the more you will have.

http://www.investlah.com/forum/index.php/topic,47111.msg1170071.html#msg1170071

Know the friend of your cash: COMPOUNDING

Michael saved $1,000 per year from age of 21 for 10 years.

Terrence saved $2,000 per year from the age of 31 for 25 years.

Assuming they both had the same rate of return at 12% per year, at the age of 55 years, Michael grew his money more than Terrence.

The earlier you start, the less you need to save and the more you will have.

http://www.investlah.com/forum/index.php/topic,47111.msg1170071.html#msg1170071

Sunday 9 February 2014

Property Investments

Understanding the figures behind property investments.

Here are the important calculations

Income Statement

Gross Rental Income

Vacancy Allowance (%)

Gross Operating Income = Gross Rental Income - Vacancy Allowance

Annual Operating Expenses

Total Expenses include assessment tax, quit/annual rent, management service charge, fire insurance, householder's insurance, MRTA, and others.

MRTA = mortgage-reducing term assurance

MLTA = mortgage-level term assurance (MLTA)

Net Operating Income

Net Operating Income = Gross Operating Income - Total Expenses

Cash Flow (before tax) from your property investment

Having calculated the net operating income, subtract the annual mortgage payments to obtain the cash flow (before tax) from the property investment.

Cash flow (before tax) = Net Operating Income - Annual Mortgage Payments

How much do you value or pay for the property?

Purchase price

Down payment / Equity

Balance financed by mortgage

Mortgage Summary

Bank

Term (Years)

Interest (% )

Total Monthly Payment

Total Yearly Payment

Total Debt Payment

Reference: Mortgage Calculators

Initial Yield Computation

Initial Yield = Gross Annual Rental / Purchase Price

Those more enterprising aim for initial yield of :

House 4 to 6%

Condo 8 to 12%

Return on Equity (ROE)

Your returns come from these 3 sources:

1. Cash Flow (before tax) provided by the property

2. Gains from your equity growth in the property

3. Appreciation of your property price over the period.

Your TOTAL RETURNS at the end of the mortgage period = 1 + 2 + 3

TOTAL ROE = (1+2+3) / Initial Down-payment for the Property

My general rules:

1. Properties prices appreciate by 100% every 10 years, higher for those in good locations..

2. Rental yields are around 3%/year based on present market price.

3. Rentals increase generally by 10% every 3 years, but only for selected properties in good locations.

When you own a good or great property in a great location at a good price, you will enjoy great ROE on your property investment, using the generous leverage provided by your bank mortgage (using other people's money). You paid an initial down-payment, and your tenants pay for the mortgages and the expenses. On top of this, you may even enjoy a positive cash flow from the property giving you regular income. During the tenure, you continue to enjoy increasing rental, after-all, you have no problem getting the best tenants and the existing tenants will likely pay up since they are making good earnings from the use of the property. At the end of the mortgage period, you would have owned 100% equity of the property, the property would have appreciated over the long period, and you have also pocketed incomes from the positive cash flow generated by the property. Totaling all these gains and then working back to your initial down-payment (your equity), you would have realised a great ROE.

Those less knowledgeable in share investing may wish to go the property route.

Summary:

1. Location, location, location = good or great properties

2. Net Operating Income = Gross Operating Income - Total Expenses

3. Cash flow (before tax) = Net Operating Income - Mortgage Payments

4. Mortgage - go for the largest available mortgage, with the longest term and the lowest interest

5. Ensure that 2 & 3 are always positive.

(Types of properties: squatter homes, low cost houses and apartments, houses, apartments and condominiums, townhouses/duplexes, commercial, service apartments, luxury homes, mobile homes, raw land, recreational, ranches, agriculture, industrial, specialty buildings such as stadiums and theaters.)(

Summary:

1. Location, location, location = good or great properties

2. Net Operating Income = Gross Operating Income - Total Expenses

3. Cash flow (before tax) = Net Operating Income - Mortgage Payments

4. Mortgage - go for the largest available mortgage, with the longest term and the lowest interest

5. Ensure that 2 & 3 are always positive.

(Types of properties: squatter homes, low cost houses and apartments, houses, apartments and condominiums, townhouses/duplexes, commercial, service apartments, luxury homes, mobile homes, raw land, recreational, ranches, agriculture, industrial, specialty buildings such as stadiums and theaters.)(

Tuesday 28 January 2014

Get to Know the Magic of Compounding

| Starting Value | Double | Triple | Quadruple | Rise 1,000% | |||||

| $1.00 | $2.00 | $3.00 | $4.00 | $10.00 | |||||

| 100% | 200% | 300% | 400% | 1000% | |||||

| Years | Years | Years | Years | ||||||

| Return | to | to | to | to | |||||

| Rates | Double | Triple | Quadruple | Rise 1,000% | |||||

| 6% | 12 | 19 | 24 | 40 | |||||

| 10% | 8 | 12 | 15 | 25 | |||||

| 14% | 6 | 9 | 11 | 18 | |||||

| 18% | 5 | 7 | 9 | 14 | |||||

| 22% | 4 | 6 | 7 | 12 | |||||

| 26% | 3 | 5 | 6 | 10 | |||||

| 30% | 3 | 5 | 6 | 9 | |||||

| Compounding factor | |||||||||

| Years | 6% | 10% | 14% | 18% | 22% | 26% | 30% | ||

| 0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | ||

| 1 | 1.1 | 1.1 | 1.1 | 1.2 | 1.2 | 1.3 | 1.3 | ||

| 2 | 1.1 | 1.2 | 1.3 | 1.4 | 1.5 | 1.6 | 1.7 | ||

| 3 | 1.2 | 1.3 | 1.5 | 1.6 | 1.8 | 2.0 | 2.2 | ||

| 4 | 1.3 | 1.5 | 1.7 | 1.9 | 2.2 | 2.5 | 2.9 | ||

| 5 | 1.3 | 1.6 | 1.9 | 2.3 | 2.7 | 3.2 | 3.7 | ||

| 6 | 1.4 | 1.8 | 2.2 | 2.7 | 3.3 | 4.0 | 4.8 | ||

| 7 | 1.5 | 1.9 | 2.5 | 3.2 | 4.0 | 5.0 | 6.3 | ||

| 8 | 1.6 | 2.1 | 2.9 | 3.8 | 4.9 | 6.4 | 8.2 | ||

| 9 | 1.7 | 2.4 | 3.3 | 4.4 | 6.0 | 8.0 | 10.6 | ||

| 10 | 1.8 | 2.6 | 3.7 | 5.2 | 7.3 | 10.1 | 13.8 | ||

| 11 | 1.9 | 2.9 | 4.2 | 6.2 | 8.9 | 12.7 | 17.9 | ||

| 12 | 2.0 | 3.1 | 4.8 | 7.3 | 10.9 | 16.0 | 23.3 | ||

| 13 | 2.1 | 3.5 | 5.5 | 8.6 | 13.3 | 20.2 | 30.3 | ||

| 14 | 2.3 | 3.8 | 6.3 | 10.1 | 16.2 | 25.4 | 39.4 | ||

| 15 | 2.4 | 4.2 | 7.1 | 12.0 | 19.7 | 32.0 | 51.2 | ||

| 16 | 2.5 | 4.6 | 8.1 | 14.1 | 24.1 | 40.4 | 66.5 | ||

| 17 | 2.7 | 5.1 | 9.3 | 16.7 | 29.4 | 50.9 | 86.5 | ||

| 18 | 2.9 | 5.6 | 10.6 | 19.7 | 35.8 | 64.1 | 112.5 | ||

| 19 | 3.0 | 6.1 | 12.1 | 23.2 | 43.7 | 80.7 | 146.2 | ||

| 20 | 3.2 | 6.7 | 13.7 | 27.4 | 53.4 | 101.7 | 190.0 | ||

| 21 | 3.4 | 7.4 | 15.7 | 32.3 | 65.1 | 128.2 | 247.1 | ||

| 22 | 3.6 | 8.1 | 17.9 | 38.1 | 79.4 | 161.5 | 321.2 | ||

| 23 | 3.8 | 9.0 | 20.4 | 45.0 | 96.9 | 203.5 | 417.5 | ||

| 24 | 4.0 | 9.8 | 23.2 | 53.1 | 118.2 | 256.4 | 542.8 | ||

| 25 | 4.3 | 10.8 | 26.5 | 62.7 | 144.2 | 323.0 | 705.6 | ||

| 26 | 4.5 | 11.9 | 30.2 | 73.9 | 175.9 | 407.0 | 917.3 | ||

| 27 | 4.8 | 13.1 | 34.4 | 87.3 | 214.6 | 512.9 | 1192.5 | ||

| 28 | 5.1 | 14.4 | 39.2 | 103.0 | 261.9 | 646.2 | 1550.3 | ||

| 29 | 5.4 | 15.9 | 44.7 | 121.5 | 319.5 | 814.2 | 2015.4 | ||

| 30 | 5.7 | 17.4 | 51.0 | 143.4 | 389.8 | 1025.9 | 2620.0 | ||

| 31 | 6.1 | 19.2 | 58.1 | 169.2 | 475.5 | 1292.7 | 3406.0 | ||

| 32 | 6.5 | 21.1 | 66.2 | 199.6 | 580.1 | 1628.8 | 4427.8 | ||

| 33 | 6.8 | 23.2 | 75.5 | 235.6 | 707.7 | 2052.2 | 5756.1 | ||

| 34 | 7.3 | 25.5 | 86.1 | 278.0 | 863.4 | 2585.8 | 7483.0 | ||

| 35 | 7.7 | 28.1 | 98.1 | 328.0 | 1053.4 | 3258.1 | 9727.9 | ||

| 36 | 8.1 | 30.9 | 111.8 | 387.0 | 1285.2 | 4105.3 | 12646.2 | ||

| 37 | 8.6 | 34.0 | 127.5 | 456.7 | 1567.9 | 5172.6 | 16440.1 | ||

| 38 | 9.2 | 37.4 | 145.3 | 538.9 | 1912.8 | 6517.5 | 21372.1 | ||

| 39 | 9.7 | 41.1 | 165.7 | 635.9 | 2333.6 | 8212.0 | 27783.7 | ||

| 40 | 10.3 | 45.3 | 188.9 | 750.4 | 2847.0 | 10347.2 | 36118.9 | ||

| 41 | 10.9 | 49.8 | 215.3 | 885.4 | 3473.4 | 13037.4 | 46954.5 | ||

Monday 27 January 2014

To maintain your portfolio at peak performance.

To pick the right stock for the long term, you should keep to:

1. Buying quality companies

2. Buying at the right price - potential return > 15% at acceptable risk (where the potential return to potential loss of >3x.)

Your ability to do the above is all you need to build a great portfolio that will meet your expectations.

To maintain your portfolio at peak performance, you will need to manage it well, optimizing its performance and preventing the companies that occasionally go south from damaging it.

Portfolio management chores take a minimal amount of time.

1. Buying quality companies

2. Buying at the right price - potential return > 15% at acceptable risk (where the potential return to potential loss of >3x.)

Your ability to do the above is all you need to build a great portfolio that will meet your expectations.

To maintain your portfolio at peak performance, you will need to manage it well, optimizing its performance and preventing the companies that occasionally go south from damaging it.

Portfolio management chores take a minimal amount of time.

Related:

My strategies for buying and selling (KISS version)

Sunday 26 January 2014

Evaluating Quality first, then Price. Fair price is one associated with adequate return at acceptable risk.

1. The most important task in buying a stock is to determine that the company is a good company in which to own stock for the long term. (QUALITY)

2. However, no matter how good the company, if the price of its stock is too high, it is not going to be a good investment.

3. A stock price must pass two tests to be considered reasonable:

(i) The hypothetical total return from the investment must be adequate - enough to contribute to a portfolio average of around 15% - sufficient to double its value every 5 years. (REWARD).

(ii) The potential gain should be at least 3x the potential loss. (RISK)

4. To complete these tasks, you have to have learned how to do the following:

(i) Estimate future sales and earnings growth.

(ii) Estimate future earnings.

(iii) Analyze past PEs (Check the current PE with the average past PEs)

(iv) Estimate future PEs.

(v) Forecast the potential high and low prices.

(vi) Calculate the potential return.

(vii) Calculate the potential risk.

(viii) Calculate a fair price.

5. If you take each of these steps in 4(i) to 4(viii), cautiously and shun excesses, your actual results is likely to be as good or better than the forecast at least four out of the five times.

6. And you will have a track record to rival any professional.

That's all folks!

2. However, no matter how good the company, if the price of its stock is too high, it is not going to be a good investment.

3. A stock price must pass two tests to be considered reasonable:

(i) The hypothetical total return from the investment must be adequate - enough to contribute to a portfolio average of around 15% - sufficient to double its value every 5 years. (REWARD).

(ii) The potential gain should be at least 3x the potential loss. (RISK)

4. To complete these tasks, you have to have learned how to do the following:

(i) Estimate future sales and earnings growth.

(ii) Estimate future earnings.

(iii) Analyze past PEs (Check the current PE with the average past PEs)

(iv) Estimate future PEs.

(v) Forecast the potential high and low prices.

(vi) Calculate the potential return.

(vii) Calculate the potential risk.

(viii) Calculate a fair price.

5. If you take each of these steps in 4(i) to 4(viii), cautiously and shun excesses, your actual results is likely to be as good or better than the forecast at least four out of the five times.

6. And you will have a track record to rival any professional.

That's all folks!

Quality Persists

Once you have determined that a company does meet your quality standards, its status is not likely to change - at least for a while.

In fact, the only factor that could change your assessment is the data that is reported every three months, so you can be reasonably confident that your assessment will survive at east that long.

And there's an 80% chance it will last a good deal longer.

So it pays you to collect and maintain a "watch-list" of good companies and wait for them to hit an attractive price - just have them available should your portfolio management strategy call for selling or replacing one you already own.

In fact, the only factor that could change your assessment is the data that is reported every three months, so you can be reasonably confident that your assessment will survive at east that long.

And there's an 80% chance it will last a good deal longer.

So it pays you to collect and maintain a "watch-list" of good companies and wait for them to hit an attractive price - just have them available should your portfolio management strategy call for selling or replacing one you already own.

To Buy or Not to Buy: Quality first, then Potential Return at an Acceptable Risk.

To buy or not to buy - the bottom line is the potential reward and the amount of risk that you must accept to achieve it.

Always assuming you have done your due diligence concerning the quality issues, look to see if the hypothetical total return is sufficient to warrant adding the stock to your portfolio. If the stock appears to be capable of doubling its value in five years, it's probably a good buy.

If you have been cautious enough in your estimates of earnings growth and future PEs, and if the potential reward is at least 3x the risk of loss, you'll have no qualms about buying the stock.

Use Your Common Sense

Investing is far from a precise science.

What you lose in accuracy because you are building one estimate upon another, you gain by being conservative in your estimates.

If you are careful to take the more cautious choice at every opportunity, you are rarely going to be disappointed at the outcome.

A small difference - a 1% difference in the risk would translate into only a small difference in the share price - is not enough to warrant waiting for the price to be just right.

If the price is more than just a little too high for the value parameters to satisfy you, however, you'll want to complete your study and wait for the price to come down to a more reasonable figure.

Summary:

1. Always the Quality criteria must be met first

2. Then look at the Total Return - this must be >15% per year.

3. Only buy when the Risk is acceptable, that is, the potential reward must be at least 3x the risk of loss.

4. Don't squabble over pennies when you are buying.

REMEMBER: Prices can fluctuate by as much as 50% on either side of their averages during the course of the year; so you might be pleasantly surprised when a price you thought beyond hope just happens to materialize one day.

Always assuming you have done your due diligence concerning the quality issues, look to see if the hypothetical total return is sufficient to warrant adding the stock to your portfolio. If the stock appears to be capable of doubling its value in five years, it's probably a good buy.

If you have been cautious enough in your estimates of earnings growth and future PEs, and if the potential reward is at least 3x the risk of loss, you'll have no qualms about buying the stock.

Use Your Common Sense

Investing is far from a precise science.

What you lose in accuracy because you are building one estimate upon another, you gain by being conservative in your estimates.

If you are careful to take the more cautious choice at every opportunity, you are rarely going to be disappointed at the outcome.

A small difference - a 1% difference in the risk would translate into only a small difference in the share price - is not enough to warrant waiting for the price to be just right.

If the price is more than just a little too high for the value parameters to satisfy you, however, you'll want to complete your study and wait for the price to come down to a more reasonable figure.

Summary:

1. Always the Quality criteria must be met first

2. Then look at the Total Return - this must be >15% per year.

3. Only buy when the Risk is acceptable, that is, the potential reward must be at least 3x the risk of loss.

4. Don't squabble over pennies when you are buying.

REMEMBER: Prices can fluctuate by as much as 50% on either side of their averages during the course of the year; so you might be pleasantly surprised when a price you thought beyond hope just happens to materialize one day.

Saturday 25 January 2014

When evaluating the price, look at the potential return and the risk you must take to get that return.

When it comes to evaluating the price of a stock, you're really interested in just 2 things:

1. The potential return, and

2. The risk you must take to get that return.

If the potential return is worth the risk, the price is right.

If it is not, you can simply wait until it is.

As volatile as the stock market is, most stocks will sell at a favourable price sometime during the year.

To estimate the potential return, you will have to come up with a reasonable forecast of how high the price might go. Knowing the hypothetical potential high price, you can estimate the potential return.

To evaluate risk, you will need to conservatively estimate the stock's potential lowest price. If your potential gain is at least three times as much as you risk losing, your stock is probably selling at a fair price.

For example:

Stock TUW

Potential high price = $20

Potential low price = $10

Market price = $12

Potential gain = $20 - $12 = $18

Potential loss = $ $12 - $10 = $2

Therefore, potential gain : potential loss = $8 : $2 = 4 : 1

As the potential gain is at least 3x as much as you risk losing, the stock is probably selling at a fair price.

1. The potential return, and

2. The risk you must take to get that return.

If the potential return is worth the risk, the price is right.

If it is not, you can simply wait until it is.

As volatile as the stock market is, most stocks will sell at a favourable price sometime during the year.

To estimate the potential return, you will have to come up with a reasonable forecast of how high the price might go. Knowing the hypothetical potential high price, you can estimate the potential return.

To evaluate risk, you will need to conservatively estimate the stock's potential lowest price. If your potential gain is at least three times as much as you risk losing, your stock is probably selling at a fair price.

For example:

Stock TUW

Potential high price = $20

Potential low price = $10

Market price = $12

Potential gain = $20 - $12 = $18

Potential loss = $ $12 - $10 = $2

Therefore, potential gain : potential loss = $8 : $2 = 4 : 1

As the potential gain is at least 3x as much as you risk losing, the stock is probably selling at a fair price.

Hopefully, you won't have to find out the hard way - QUALITY first, then PRICE. When in doubt, throw it out!

The most important task is in investing into a company is in assessing its quality.

Hopefully you won't have to find out the hard way that buying a good company for too high a price is still better than buying a poor company - even at what you may think is a bargain price.

No matter how low it may be, a company that doesn't meet the quality requirements will always be too expensive - at any price!

If you are not critical enough about quality, you can easily be seduced into believing that a stock is a bargain when you actually shouldn't touch it with a 10-foot pole.

Here is a statement you may have to think about a little: The worse a company performs, the better a value it will appear to be. Why do you suppose that is?

If you ignore the poor operational performance and just look at the price, you'll be in the market for someone else's mistake!

Sure, you will be able to pick up the stock at bargain-basement prices - but for a good reason.

You will think you made out like a bandit when, in fact, whomever you bought the stock from will turn out to be the lucky one.

The most important point here is that you simply cannot afford to ignore the quality issues or treat them lightly.

Unless the company completely satisfies your quality requirements - and I don't mean it's marginal or might have some problem - your evaluation of the price of the stock can be invalid and, in fact, hazardous to your financial health.

When in doubt, throw it out!

Hopefully you won't have to find out the hard way that buying a good company for too high a price is still better than buying a poor company - even at what you may think is a bargain price.

No matter how low it may be, a company that doesn't meet the quality requirements will always be too expensive - at any price!

If you are not critical enough about quality, you can easily be seduced into believing that a stock is a bargain when you actually shouldn't touch it with a 10-foot pole.

Here is a statement you may have to think about a little: The worse a company performs, the better a value it will appear to be. Why do you suppose that is?

If you ignore the poor operational performance and just look at the price, you'll be in the market for someone else's mistake!

Sure, you will be able to pick up the stock at bargain-basement prices - but for a good reason.

You will think you made out like a bandit when, in fact, whomever you bought the stock from will turn out to be the lucky one.

The most important point here is that you simply cannot afford to ignore the quality issues or treat them lightly.

Unless the company completely satisfies your quality requirements - and I don't mean it's marginal or might have some problem - your evaluation of the price of the stock can be invalid and, in fact, hazardous to your financial health.

When in doubt, throw it out!

Friday 24 January 2014

CIMB’s private placement exercise draws mixed reactions from analysts

CIMB’s private placement exercise draws mixed reactions from analysts

by Sharon Kong, sharonkong@theborneopost.com.

Posted on January 16, 2014, Thursday

KUCHING: CIMB Group Holdings Bhd’s (CIMB) recent private placement exercise has garnered mixed reactions from various analysts, with adverse market movements the cause of this latest development.

According to RHB Research Institute Sdn Bhd (RHB Research), the capital-raising could possibly have been prompted by adverse market movements. This is due to CIMB having said in its statement to Bursa Malaysia that the sharp depreciation of the Indonesian Rupiah had set back to its capital accumulation plan.

The research house further pointed out that the adverse direction that bond yields have seen in 2013 may have also prompted the fund-raising exercise.

“Based on its first nine months of 2013 (9M13) results, adverse forex and interest rate movements have shaved off RM1.5 billion in shareholders’ equity – exchange fluctuation reserve of RM693 millon and available for sale (AFS) revaluation reserve of RM817 million.

“By our estimates, this translates to RM1.1 billion in CET-1 capital, after taking into account the required regulatory adjustment of a 55 per cent haircut for AFS reserves,” RHB Research said.

With the issue of capital addressed, two things that RHB Research thinks investors will now seek further guidance on from management are the sustainable return on equity (ROE) level going forward, and whether the dividend reinvestment schem (DRS) will continue.

Looking ahead, for 2014, it thinks a 15 per cent ROE target may be possible. This will also be similar to Malayan Bank Bhd’s (Maybank) 2013 ROE target, post the RM3.66 billion capital raising exercise it did in 2012.

Also, now that CIMB has shored up its capital, it remains to be seen whether management will opt to keep in place the DRS, the research house added.

“The latter appears to be well received, achieving a take-up rate of 80.2 per cent for the recent second quarter of 2013 (2Q13) interim dividend.

“The flipside is that the DRS is slightly dilutive, with an estimated one per cent impact on financial year 2014 forecast (FY14F) earnings per share (EPS) and 40 basis points (bps) to FY14F ROE,” it noted.

According to analyst Cheah King Yoong of Alliance Research Sdn Bhd (Alliance Research), the capital raising exercise engaged by CIMB came as a surprise to them.

He similarly opined that they are not certain whether the group will continue with its dividend reinvestment plan (DRP) upon the completion of this private placement exercise.

“Should the research house assume that the group will be utilising the net proceeds raised to retire part of its borrowing and continuing with its DRP, its FY14-FY15 earnings per share (EPS) forecasts will be diluted by three to four per cent,” he noted.

In terms of earnings forecast for CIMB, Cheah highlighted that pending further clarifications by the management with regards to the utilisation of its net proceeds, and the continuity of its DRP, they made no changes to their earnings estimates for now.

“We will revise our earnings estimates for the group post our meeting with the management next week,” he added.

Read more: http://www.theborneopost.com/2014/01/16/cimbs-private-placement-exercise-draws-mixed-reactions-from-analysts/#ixzz2rEaYfgwL

Main points:

1. Adverse forex and interest rate movements have shaved off RM1.5 billion in shareholders' equity.

2. This translates t RM1.1 billion in CET-1 capital.

3. The capital raising exercise by CIMB came as a surprise.

4. What will be the sustainable ROE going forward?

5. Will the DRS (dividend reinvestment scheme) be kept in place?

6. DRS is slightly dilutive, with an estimated 1% impact on financial year 2014 forecast (FY14F) EPS and 40 basis points (bps) to FY14F ROE.

Scenario analysis:

Assuming:

1. No changes to the earnings estimates.

2. CIMB utilising the net proceeds raised to retire part of its borrowing and continuing with its DRP.

It is forecasted that these will impact on CIMB's FY14-FY15 EPS, diluting it by 3 to 4%.

(Share price of CIMB closed at 6.80 per share on 23.1.2014.)

1 Year Chart

Long term Chart

by Sharon Kong, sharonkong@theborneopost.com.

Posted on January 16, 2014, Thursday

KUCHING: CIMB Group Holdings Bhd’s (CIMB) recent private placement exercise has garnered mixed reactions from various analysts, with adverse market movements the cause of this latest development.

According to RHB Research Institute Sdn Bhd (RHB Research), the capital-raising could possibly have been prompted by adverse market movements. This is due to CIMB having said in its statement to Bursa Malaysia that the sharp depreciation of the Indonesian Rupiah had set back to its capital accumulation plan.

The research house further pointed out that the adverse direction that bond yields have seen in 2013 may have also prompted the fund-raising exercise.

“Based on its first nine months of 2013 (9M13) results, adverse forex and interest rate movements have shaved off RM1.5 billion in shareholders’ equity – exchange fluctuation reserve of RM693 millon and available for sale (AFS) revaluation reserve of RM817 million.

“By our estimates, this translates to RM1.1 billion in CET-1 capital, after taking into account the required regulatory adjustment of a 55 per cent haircut for AFS reserves,” RHB Research said.

With the issue of capital addressed, two things that RHB Research thinks investors will now seek further guidance on from management are the sustainable return on equity (ROE) level going forward, and whether the dividend reinvestment schem (DRS) will continue.

Looking ahead, for 2014, it thinks a 15 per cent ROE target may be possible. This will also be similar to Malayan Bank Bhd’s (Maybank) 2013 ROE target, post the RM3.66 billion capital raising exercise it did in 2012.

Also, now that CIMB has shored up its capital, it remains to be seen whether management will opt to keep in place the DRS, the research house added.

“The latter appears to be well received, achieving a take-up rate of 80.2 per cent for the recent second quarter of 2013 (2Q13) interim dividend.

“The flipside is that the DRS is slightly dilutive, with an estimated one per cent impact on financial year 2014 forecast (FY14F) earnings per share (EPS) and 40 basis points (bps) to FY14F ROE,” it noted.

According to analyst Cheah King Yoong of Alliance Research Sdn Bhd (Alliance Research), the capital raising exercise engaged by CIMB came as a surprise to them.

He similarly opined that they are not certain whether the group will continue with its dividend reinvestment plan (DRP) upon the completion of this private placement exercise.

“Should the research house assume that the group will be utilising the net proceeds raised to retire part of its borrowing and continuing with its DRP, its FY14-FY15 earnings per share (EPS) forecasts will be diluted by three to four per cent,” he noted.

In terms of earnings forecast for CIMB, Cheah highlighted that pending further clarifications by the management with regards to the utilisation of its net proceeds, and the continuity of its DRP, they made no changes to their earnings estimates for now.

“We will revise our earnings estimates for the group post our meeting with the management next week,” he added.

Read more: http://www.theborneopost.com/2014/01/16/cimbs-private-placement-exercise-draws-mixed-reactions-from-analysts/#ixzz2rEaYfgwL

Main points:

1. Adverse forex and interest rate movements have shaved off RM1.5 billion in shareholders' equity.

2. This translates t RM1.1 billion in CET-1 capital.

3. The capital raising exercise by CIMB came as a surprise.

4. What will be the sustainable ROE going forward?

5. Will the DRS (dividend reinvestment scheme) be kept in place?

6. DRS is slightly dilutive, with an estimated 1% impact on financial year 2014 forecast (FY14F) EPS and 40 basis points (bps) to FY14F ROE.

Scenario analysis:

Assuming:

1. No changes to the earnings estimates.

2. CIMB utilising the net proceeds raised to retire part of its borrowing and continuing with its DRP.

It is forecasted that these will impact on CIMB's FY14-FY15 EPS, diluting it by 3 to 4%.

(Share price of CIMB closed at 6.80 per share on 23.1.2014.)

1 Year Chart

Long term Chart

Sunday 19 January 2014

Top 100 Companies of KLSE 3.1.2014 (Sorted by DY)

Top 100 Companies of KLSE 3.1.2014 (Sorted according to DY)

Top 100 Companies of KLSE 3.1.2014 (Market P/E is 17.1 and DY is 3.2%)

| #Rank | Company | Price | PE | EY % | DY % | |||||

| 66 | Kulim | 3.38 | 5 | 20.0 | 29.1 | |||||

| 54 | MBSB | 2.17 | 6.8 | 14.7 | 13.3 | |||||

| 48 | AirAsia | 2.37 | 3.5 | 28.6 | 10.1 | |||||

| 56 | BJToto | 4.01 | 13.8 | 7.2 | 7 | |||||

| 1 | Maybank | 9.91 | 13.6 | 7.4 | 6.6 | |||||

| 77 | SunReit | 1.25 | 8.9 | 11.2 | 6.6 | |||||

| 93 | UOADev | 1.87 | 7.6 | 13.2 | 6.4 | |||||

| 83 | Parkson | 2.86 | 12.9 | 7.8 | 6.3 | |||||

| 94 | CMMT | 1.4 | 9.9 | 10.1 | 6 | |||||

| 52 | Bstead | 5.6 | 13.9 | 7.2 | 5.8 | |||||

| 8 | Maxis | 7.13 | 28.9 | 3.5 | 5.6 | |||||

| 85 | Dlady | 47.3 | 24.5 | 4.1 | 5.5 | |||||

| 10 | DiGi | 4.85 | 31.3 | 3.2 | 5.4 | |||||

| 72 | PavReit | 1.32 | 6.3 | 15.9 | 5.2 | |||||

| 4 | Axiata | 6.8 | 22.7 | 4.4 | 5.1 | |||||

| 76 | Carlsbg | 12.24 | 19.5 | 5.1 | 5.1 | |||||

| 65 | Magnum | 3.15 | 13.3 | 7.5 | 5.1 | |||||

| 89 | Media | 2.62 | 13.5 | 7.4 | 5 | |||||

| 55 | Utd Plant | 26.18 | 15.9 | 6.3 | 4.8 | |||||

| 46 | LAFMSIA | 8.41 | 20.5 | 4.9 | 4.4 | |||||

| 24 | BAT | 63.88 | 22.9 | 4.4 | 4.3 | |||||

| 62 | GAB | 15.9 | 22.1 | 4.5 | 4.3 | |||||

| 22 | TM | 5.39 | 15.3 | 6.5 | 4.1 | |||||

| 30 | UMW | 12.28 | 15.1 | 6.6 | 4.1 | |||||

| 80 | Bintulu Port | 7.5 | 20.5 | 4.9 | 4 | |||||

| 75 | LPI | 17.46 | 23 | 4.3 | 3.7 | |||||

| 78 | MSM | 5.1 | 17.7 | 5.6 | 3.7 | |||||

| 45 | SPSetia | 2.95 | 16.5 | 6.1 | 3.7 | |||||

| 6 | Sime | 9.39 | 15.2 | 6.6 | 3.6 | |||||

| 50 | HapSeng | 2.95 | 15.1 | 6.6 | 3.6 | |||||

| 13 | PetDag | 30.4 | 36.1 | 2.8 | 3.5 | |||||

| 44 | AFG | 4.8 | 13.6 | 7.4 | 3.5 | |||||

| 51 | Affin | 4.26 | 10.1 | 9.9 | 3.5 | |||||

| 14 | IOICorp | 4.58 | 14.9 | 6.7 | 3.4 | |||||

| 67 | Bursa | 8.13 | 28.5 | 3.5 | 3.3 | |||||

| 47 | F&N | 18.4 | 25.7 | 3.9 | 3.3 | |||||

| 61 | GasMsia | 3.95 | 31.2 | 3.2 | 3.2 | |||||

| 7 | Pchem | 6.84 | 15.5 | 6.5 | 3.2 | |||||

| 16 | HLBank | 14.24 | 13.5 | 7.4 | 3.2 | |||||

| 28 | Nestle | 67.96 | 31.5 | 3.2 | 3.1 | |||||

| 86 | Pos | 5.57 | 19.7 | 5.1 | 3.1 | |||||

| 100 | Zhulian | 4.93 | 19.4 | 5.2 | 3.1 | |||||

| 26 | FGV | 4.53 | 15.9 | 6.3 | 3.1 | |||||

| 5 | CIMB | 7.51 | 12.9 | 7.8 | 3.1 | |||||

| 20 | AMBank | 7.29 | 13.4 | 7.5 | 3 | |||||

| 53 | MHB | 3.61 | 23.9 | 4.2 | 2.8 | |||||

| 70 | IGB | 2.72 | 21.8 | 4.6 | 2.8 | |||||

| 79 | Top Glove | 5.73 | 18.1 | 5.5 | 2.8 | |||||

| 39 | Bkawan | 19.6 | 16.8 | 6.0 | 2.8 | |||||

| 21 | RHBCap | 7.97 | 10.1 | 9.9 | 2.8 | |||||

| 82 | Mah Sing | 2.27 | 9.9 | 10.1 | 2.7 | |||||

| 49 | BIMB | 4.38 | 19.5 | 5.1 | 2.6 | |||||

| 35 | Gamuda | 4.61 | 18.2 | 5.5 | 2.6 | |||||

| 2 | PBBank | 18.9 | 17.1 | 5.8 | 2.6 | |||||

| 99 | CMSB | 6.78 | 16 | 6.3 | 2.5 | |||||

| 3 | Tenaga | 11 | 13.3 | 7.5 | 2.3 | |||||

| 27 | HLFG | 15.5 | 10.9 | 9.2 | 2.3 | |||||

| 43 | IJM | 5.85 | 19.2 | 5.2 | 2.2 | |||||

| 59 | DRBHCOM | 2.72 | 9.1 | 11.0 | 2.2 | |||||

| 9 | PetGas | 23.6 | 33.2 | 3.0 | 2.1 | |||||

| 18 | KLK | 24.12 | 28 | 3.6 | 2.1 | |||||

| 71 | Tchong | 5.98 | 24.7 | 4.0 | 2 | |||||

| 73 | KPJ | 3.87 | 24.7 | 4.0 | 2 | |||||

| 90 | IJMPlnt | 3.48 | 23.3 | 4.3 | 2 | |||||

| 57 | Harta | 7.23 | 22.5 | 4.4 | 2 | |||||

| 17 | GENM | 4.38 | 17.7 | 5.6 | 2 | |||||

| 74 | IJMLand | 2.52 | 16.4 | 6.1 | 2 | |||||

| 64 | Sunway | 2.75 | 7.7 | 13.0 | 1.9 | |||||

| 84 | Dayang | 5.66 | 30.5 | 3.3 | 1.8 | |||||

| 97 | BJCorp | 0.56 | 29.6 | 3.4 | 1.8 | |||||

| 63 | Aeon | 13.64 | 22.5 | 4.4 | 1.8 | |||||

| 98 | WCT | 2.14 | 5.5 | 18.2 | 1.8 | |||||

| 25 | YTL | 1.6 | 12.4 | 8.1 | 1.6 | |||||

| 37 | MMCCorp | 2.85 | 9.4 | 10.6 | 1.6 | |||||

| 87 | Shang | 6.78 | 44.3 | 2.3 | 1.5 | |||||

| 96 | Kseng | 6.73 | 28.7 | 3.5 | 1.5 | |||||

| 69 | IGBReit | 1.2 | 26.6 | 3.8 | 1.5 | |||||

| 33 | Airport | 8.8 | 26.5 | 3.8 | 1.5 | |||||

| 92 | Kossan | 4.1 | 25.1 | 4.0 | 1.4 | |||||

| 23 | PPB | 15.92 | 22.4 | 4.5 | 1.3 | |||||

| 36 | UEMS | 2.32 | 22.4 | 4.5 | 1.3 | |||||

| 29 | Astro | 2.98 | 13.4 | 7.5 | 1.3 | |||||

| 68 | BJLand | 0.82 | 124.2 | 0.8 | 1.2 | |||||

| 81 | QL | 4.1 | 25.9 | 3.9 | 1.1 | |||||

| 42 | GENP | 10.98 | 25.5 | 3.9 | 1.1 | |||||

| 41 | Dialog | 3.4 | 42.1 | 2.4 | 1 | |||||

| 60 | Orient | 8.39 | 22.1 | 4.5 | 1 | |||||

| 91 | TSH | 2.92 | 31.4 | 3.2 | 0.9 | |||||

| 88 | SOP | 6.65 | 21.5 | 4.7 | 0.9 | |||||

| 11 | Genting | 10.08 | 9.3 | 10.8 | 0.8 | |||||

| 32 | Armada | 4.08 | 31 | 3.2 | 0.7 | |||||

| 31 | YTLPowr | 1.85 | 12.5 | 8.0 | 0.5 | |||||

| 15 | SKPetro | 4.57 | 43.6 | 2.3 | 0 | |||||

| 12 | IHH | 3.91 | 34.1 | 2.9 | 0 | |||||

| 95 | HLCap | 10 | 26.1 | 3.8 | 0 | |||||

| 19 | MISC | 5.51 | 0 | 0.0 | 0 | |||||

| 34 | KLCC | 5.94 | 0 | 0.0 | 0 | |||||

| 38 | WPRTS | 2.53 | 0 | 0.0 | 0 | |||||

| 40 | UMWOG | 3.91 | 0 | 0.0 | 0 | |||||

| 58 | MAS | 0.32 | 0 | 0.0 | 0 |

# Rank is based on market capitalization

Top 100 Companies of KLSE 3.1.2014 (Market P/E is 17.1 and DY is 3.2%)

Subscribe to:

Posts (Atom)