Vega

Vega measures the rate of change in the warrant price for each point of movement of its implied volatility.

No matter it is a call warrant or a put warrant, vega is always positive, indicating that the warrant price and its implied volatility always move in the same direction.

Vega can be an absolute value or a percentage relative to the warrant price.

Gamma

Gamma measures the sensitivity of the delta of a warrant to the price movements of its underlying.

The higher the gamma, the bigger the change in delta will be in reaction to a movement in the underlying price.

Gamma = Rate of Change of Delta / Rate of Change of Underlying Price

No matter it is a call warrant or put warrant, gamma is always positive.

Rho

Rho measures the sensitivity of warrant price to changes in the market interest rate.

Call warrants have a positive rho, meaning that the price of a call warrant moves in the same direction as the market interest rate.

In contrast, put warrants have a negative rho, and this shows that the price of a put warrant moves in the opposite direction to the market interest rate.

Given that changes in interest rates tend to be limited in the short term, their effect on warrant prices is minimal.

Friday 11 September 2015

Technical Parameters of Warrants: Theta

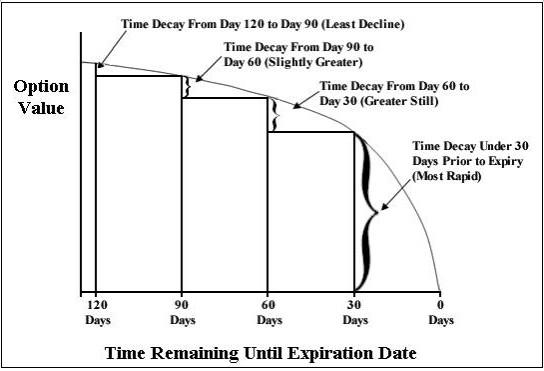

Theta, also called time decay, measures the rate of change in the price of a warrant as its maturity is running short while all other things being equal.

It can be expressed as an absolute value or a percentage relative to the warrant price (theta / warrant price).

Unless in some special circumstances, the value of theta is usually negative, reflecting the declining value of a warrant as time passes.

Depicted in a chart form, the slope of the curve of time value becomes steeper as the warrant gets closer to its maturity.

This shows that time decay accelerates as time passes.

Additional notes:

In percentage terms, time value has the biggest impact on out of the money (OTM) warrants.

The value of a warrant consists of intrinsic value and time value.

They vary in absolute and relative terms for warrants with different strike prices and maturity dates.

In the case of OTM warrants, their intrinsic values are negligible.

In other words, time value makes up most of their values.

Hence, they are more sensitive to the passage of time.

As for in the money (ITM) warrants, given that a large part of their value is made up of intrinsic value, they are less sensitive to the passage of time, and such sensitivity decreases as the maturity date gets nearer.

It can be expressed as an absolute value or a percentage relative to the warrant price (theta / warrant price).

Unless in some special circumstances, the value of theta is usually negative, reflecting the declining value of a warrant as time passes.

Depicted in a chart form, the slope of the curve of time value becomes steeper as the warrant gets closer to its maturity.

This shows that time decay accelerates as time passes.

Additional notes:

In percentage terms, time value has the biggest impact on out of the money (OTM) warrants.

The value of a warrant consists of intrinsic value and time value.

They vary in absolute and relative terms for warrants with different strike prices and maturity dates.

In the case of OTM warrants, their intrinsic values are negligible.

In other words, time value makes up most of their values.

Hence, they are more sensitive to the passage of time.

As for in the money (ITM) warrants, given that a large part of their value is made up of intrinsic value, they are less sensitive to the passage of time, and such sensitivity decreases as the maturity date gets nearer.

Warrants: Effective Gearing versus Gearing

The biggest appeal of warrant trading lies in the leverage effect.

Investors only need to invest a small sum to earn a potential return close to or even higher than that from directly investing in the underlying.

Gearing

Gearing only reflects how many times the underlying costs versus the warrant.

Its calculation formula is:

Gearing = Underlying Price / (Warrant Price x Conversion Ratio)

Effective Gearing

However, the rate of increase/decrease in the warrant price relative to the underlying price is not the same as gearing.

To estimate the increase/decrease in the warrant price relative to the underlying price, we should look to the effective gearing.

Effective gearing reflects the relationship between changes in the warrant price and in the underlying price.

Its calculation formula is:

Effective Gearing = Gearing x Delta

For example, the effective gearing of a warrant is 10 times, then, other things being equal, for every 1% change in the underlying price, the warrant price will in theory move by 10%.

Put simply, delta measures how much, in theory, the warrant price will move for a $1 change in the underlying price.

When you invest in warrants, you should look to their effective gearing, not gearing, as a reference for their risk/return performance.

Investors only need to invest a small sum to earn a potential return close to or even higher than that from directly investing in the underlying.

Gearing

Gearing only reflects how many times the underlying costs versus the warrant.

Its calculation formula is:

Gearing = Underlying Price / (Warrant Price x Conversion Ratio)

Effective Gearing

However, the rate of increase/decrease in the warrant price relative to the underlying price is not the same as gearing.

To estimate the increase/decrease in the warrant price relative to the underlying price, we should look to the effective gearing.

Effective gearing reflects the relationship between changes in the warrant price and in the underlying price.

Its calculation formula is:

Effective Gearing = Gearing x Delta

For example, the effective gearing of a warrant is 10 times, then, other things being equal, for every 1% change in the underlying price, the warrant price will in theory move by 10%.

Put simply, delta measures how much, in theory, the warrant price will move for a $1 change in the underlying price.

When you invest in warrants, you should look to their effective gearing, not gearing, as a reference for their risk/return performance.

Warrants: Days to Maturity

Warrants can be classified accordingly to the length of their remaining days to maturity.

Short term warrant: Warrant with less than 3 months to maturity

Medium term warrant: Warrants with 3 to 6 months left to maturity

Long term warrant: Warrants with more than 6 months running to maturity.

Whether it is long-term or short-term, ITM or OTM, a warrant is after all a leveraged investment instrument.

Be cautious in funds allocation and stop-loss arrangements.

Do not get carried away by the potential return without considering your risk tolerance.

For example:

A general investor may consider a medium-term warrant with around 3 months running to maturity and a strike price around 5% above or below the underlying price.

More aggressive investors may go for OTM warrants with a shorter maturity.

For conservative investors, they may choose ITM warrants with a longer maturity.

The warrant price tends to be positively related to the length of maturity.

In theory, the longer the maturity, the more room for changes in the underlying price will be.

Given the greater chance for the warrant to be exercised, the warrant price will tend to be higher.

No matter for call warrants or put warrants, the warrant price tends to be positively related to the length of maturity.

Besides, a warrant expiring in 6 months is less affected by time decay than one expiring in 3 months.

Warrants with a longer maturity will see their time values fall slower, while those with a shorter maturity will see their time values fall faster.

Short term warrant: Warrant with less than 3 months to maturity

Medium term warrant: Warrants with 3 to 6 months left to maturity

Long term warrant: Warrants with more than 6 months running to maturity.

Whether it is long-term or short-term, ITM or OTM, a warrant is after all a leveraged investment instrument.

Be cautious in funds allocation and stop-loss arrangements.

Do not get carried away by the potential return without considering your risk tolerance.

For example:

A general investor may consider a medium-term warrant with around 3 months running to maturity and a strike price around 5% above or below the underlying price.

More aggressive investors may go for OTM warrants with a shorter maturity.

For conservative investors, they may choose ITM warrants with a longer maturity.

The warrant price tends to be positively related to the length of maturity.

In theory, the longer the maturity, the more room for changes in the underlying price will be.

Given the greater chance for the warrant to be exercised, the warrant price will tend to be higher.

No matter for call warrants or put warrants, the warrant price tends to be positively related to the length of maturity.

Besides, a warrant expiring in 6 months is less affected by time decay than one expiring in 3 months.

Warrants with a longer maturity will see their time values fall slower, while those with a shorter maturity will see their time values fall faster.

Thursday 10 September 2015

Deep in the money (deep ITM) and far out of the money (far OTM) warrants

If we take into account the extent of difference between the strike price and the underlying price, warrants can be further classified into:

ITM

deep ITM

OTM and

far OTM.

Generally, where there is a 15% or above difference between the strike price and the underlying price, a warrant will be considered far OTM or deep ITM.

However, this 15% mark is merely a rough idea, not an absolute threshold.

One must also look in the volatitlity of the underlying.

Some warrants may be considered deep ITM or far OTM even if the difference between strike price and the underlying price is only 10% or more.

ITM

deep ITM

OTM and

far OTM.

Generally, where there is a 15% or above difference between the strike price and the underlying price, a warrant will be considered far OTM or deep ITM.

However, this 15% mark is merely a rough idea, not an absolute threshold.

One must also look in the volatitlity of the underlying.

Some warrants may be considered deep ITM or far OTM even if the difference between strike price and the underlying price is only 10% or more.

Warrants - In the money, at the money and out of the money

A warrant is described as in-the-money (ITM), at-the-money (ATM) or out-of-the-money (OTM), depending on the relationship between its strike price and its underlying price.

A call warrant is OTM when its strike price is higher than its underlying price.

It is ITM, when its strike price is lower than its underlying price.

The situation is just the opposite for put warrants.

When its strike price is higher than its underlying price, a put warrant is ITM; and when its strike price is lower than its underlying price, it is OTM.

No matter it is a call or put, if the strike price is equal to the underlying price, the warrant is said to be ATM.

Summary

Call Warrant

ITM Strike Price < Underlying Price

ATM Strike Price = Underlying Price

OTM Strike Price > Underlying Price

Put Warrant

ITM Strike Price > Underlying Price

ATM Strike Price = Underlying Price

OTM Strike Price < Underlying Price

Additional Notes

Call Warrant

An investor can buy a call warrant if he is optimistic about the outlook for its underlying.

When the underlying price does go above the strike price, in theory, the investor can exercise the warrant to buy the underlying at the strike price.

Then he can sell it in the market to earn the difference.

In practice, warrants are traded on a cash settlement basis, and investors will be paid the difference directly.

Put Warrant

In the case of a put warrant, an investor can go for it when he is pessimistic about the market outlook.

If the underlying price is lower than the strike price, in theory, the invstor can exercise the warrant and buy the underlying from the market for delivery to the issuer at the strike price to earn the difference.

In reality, investors will be paid the difference directly.

If it turns out that the underlying price is higher than the strike price, the investor will lose the cost of the warrant.

(The above assumes that the investor will hold the warrant until maturity. Indeed, investors can also "buy low, sell high", and trade warrants just like stocks.)

A call warrant is OTM when its strike price is higher than its underlying price.

It is ITM, when its strike price is lower than its underlying price.

The situation is just the opposite for put warrants.

When its strike price is higher than its underlying price, a put warrant is ITM; and when its strike price is lower than its underlying price, it is OTM.

No matter it is a call or put, if the strike price is equal to the underlying price, the warrant is said to be ATM.

Summary

Call Warrant

ITM Strike Price < Underlying Price

ATM Strike Price = Underlying Price

OTM Strike Price > Underlying Price

Put Warrant

ITM Strike Price > Underlying Price

ATM Strike Price = Underlying Price

OTM Strike Price < Underlying Price

Additional Notes

Call Warrant

An investor can buy a call warrant if he is optimistic about the outlook for its underlying.

When the underlying price does go above the strike price, in theory, the investor can exercise the warrant to buy the underlying at the strike price.

Then he can sell it in the market to earn the difference.

In practice, warrants are traded on a cash settlement basis, and investors will be paid the difference directly.

Put Warrant

In the case of a put warrant, an investor can go for it when he is pessimistic about the market outlook.

If the underlying price is lower than the strike price, in theory, the invstor can exercise the warrant and buy the underlying from the market for delivery to the issuer at the strike price to earn the difference.

In reality, investors will be paid the difference directly.

If it turns out that the underlying price is higher than the strike price, the investor will lose the cost of the warrant.

(The above assumes that the investor will hold the warrant until maturity. Indeed, investors can also "buy low, sell high", and trade warrants just like stocks.)

Covered Warrants

Covered Warrants are mainly issued by investment banks.

They are issued to offer a leveraged investment tool for investors.

Cash settlement is the norm for Covered Warrants; thus companies will not face any changes in their shareholding structures as a result.

In other words, Covered Warrants will not dilute a company shareholding.

Unlike Company Warrants, Covered Warrants have good liquidity due to the market making system.

Their pricing mechanism is more transparent (statistics such as effective gearing is readily available).

It is possible to track changes in the theoretical prices of Covered Warrants.

Investors should study the relevant information carefully and bear in mind their own risk tolearance in making the decision whether to invest in Covered Warrants.

They are issued to offer a leveraged investment tool for investors.

Cash settlement is the norm for Covered Warrants; thus companies will not face any changes in their shareholding structures as a result.

In other words, Covered Warrants will not dilute a company shareholding.

Unlike Company Warrants, Covered Warrants have good liquidity due to the market making system.

Their pricing mechanism is more transparent (statistics such as effective gearing is readily available).

It is possible to track changes in the theoretical prices of Covered Warrants.

Investors should study the relevant information carefully and bear in mind their own risk tolearance in making the decision whether to invest in Covered Warrants.

Penny Warrants are very risky.

Warrants with only 1 - 2 weeks left to maturity and over 10% out-of-the-money (OTM) are called penny warrants.

They are very risky and their odds are low. The reasons are as follows:

1. The bid/ask spreads of penny warrants are rather wide.

2. Penny warrants have a very high rate of time decay.

3. It is easy to lose money with penny warrants.

4. Penny warrants may be not that price sensitive.

5. Penny warrants can hardly edge up but easily plummet.

They are very risky and their odds are low. The reasons are as follows:

1. The bid/ask spreads of penny warrants are rather wide.

2. Penny warrants have a very high rate of time decay.

3. It is easy to lose money with penny warrants.

4. Penny warrants may be not that price sensitive.

5. Penny warrants can hardly edge up but easily plummet.

Company Warrants

The basic concept of warrants is to give investors the right to buy or sell the underlying at the pre-determined strike price on the pre-determined date.

Company Warrants are issued by companies to raise funds or to reward employees or shareholders.

Upon maturity of a Company Warrant, provided that the stock price is higher than the strike price at the time, the holder is entitled to buy a certain number of shares of the company at the strike price.

When the holder does exercise the warrant, the company must issue new shares to meet the promise.

So, when Company Warrants are exercised, the shareholding of the company will be diluted.

Company Warrants normally have lower liquidity, and there is no way to compare their prices.

This is because the price of a Company Warrant is mainly determined by the board of directors.

Therefore, the warrant price is very likely to deviate from the underlying price.

Put another way, Company Warrants are less transparent and, sometimes, more speculative.

Investors should study the relveant information carefully and bear in mind their own risk tolerance in making the decision whether to invest in Company Warrants.

Company Warrants are issued by companies to raise funds or to reward employees or shareholders.

Upon maturity of a Company Warrant, provided that the stock price is higher than the strike price at the time, the holder is entitled to buy a certain number of shares of the company at the strike price.

When the holder does exercise the warrant, the company must issue new shares to meet the promise.

So, when Company Warrants are exercised, the shareholding of the company will be diluted.

Company Warrants normally have lower liquidity, and there is no way to compare their prices.

This is because the price of a Company Warrant is mainly determined by the board of directors.

Therefore, the warrant price is very likely to deviate from the underlying price.

Put another way, Company Warrants are less transparent and, sometimes, more speculative.

Investors should study the relveant information carefully and bear in mind their own risk tolerance in making the decision whether to invest in Company Warrants.

Warrants versus Stocks

If you are optimistic about a stock, the most direct investment strategy is to buy the stock.

However, some investors may choose to buy a related warrant instead.

Pros: Limited investment amount.

The biggest advantage of warrants is the leverage effect, which allows you to invest with less capital for the same return, as compared with stock trading.

The lower capital required for warrants means that, in case there is a market downturn, the loss will be limited as compared with investing directly in the stock.

In fact, in a number of major setbacks in the past, even giant blue chips fell sharply. Buying warrants instead of stocks can help minimize one's exposure to such market risks.

Cons: Time constraint

Of course, warrants are not without their shortcomings.

It takes a lot of time to understand the factors that may affect warrant prices before one can master the leverage effect to one's advantage.

Investors must get to know that warrants are subject to the time constraint.

The price of a warrant may change along with the implied volatility and dividend payout of its underlying and interest rates.

Even if you get the underlying direction right, you may still fail to reap the expected return.

In case you get it wrong, you should stop the loss.

Never sit on your holdings like a stock investor does to wait for a rebound. The price of a warrant will be dragged down by not only a falling underlying price, but also a declining time value.

Additional notes:

Warrants are derivatives.

They are an alternative investment to their underlying, and vice versa.

Warrants can never be an absolute substitute for their underlying.

Do manage your portfolio flexibly by investing in warrants and/or their underlying in light of the market conditions and outlook, as well as your own risk tolerance.

If one gets the market wrong, one will lose more from warrants (actual loss over investment cost) than from stocks.

That means the leverage effect of warrants is a double-edged sword. (Investors must take caution.)

The investment cost for warrants is lower than that for stocks, but they are more volatile.

Hence, their rate of potential gain or loss is much higher than their underlying.

Summary:

Warrants are a leveraged investment tool.

Don't foreget that the leverage effect can mean more profit, but also more loss.

So do limit your investment amount in warrants.

However, some investors may choose to buy a related warrant instead.

Pros: Limited investment amount.

The biggest advantage of warrants is the leverage effect, which allows you to invest with less capital for the same return, as compared with stock trading.

The lower capital required for warrants means that, in case there is a market downturn, the loss will be limited as compared with investing directly in the stock.

In fact, in a number of major setbacks in the past, even giant blue chips fell sharply. Buying warrants instead of stocks can help minimize one's exposure to such market risks.

Cons: Time constraint

Of course, warrants are not without their shortcomings.

It takes a lot of time to understand the factors that may affect warrant prices before one can master the leverage effect to one's advantage.

Investors must get to know that warrants are subject to the time constraint.

The price of a warrant may change along with the implied volatility and dividend payout of its underlying and interest rates.

Even if you get the underlying direction right, you may still fail to reap the expected return.

In case you get it wrong, you should stop the loss.

Never sit on your holdings like a stock investor does to wait for a rebound. The price of a warrant will be dragged down by not only a falling underlying price, but also a declining time value.

Additional notes:

Warrants are derivatives.

They are an alternative investment to their underlying, and vice versa.

Warrants can never be an absolute substitute for their underlying.

Do manage your portfolio flexibly by investing in warrants and/or their underlying in light of the market conditions and outlook, as well as your own risk tolerance.

If one gets the market wrong, one will lose more from warrants (actual loss over investment cost) than from stocks.

That means the leverage effect of warrants is a double-edged sword. (Investors must take caution.)

The investment cost for warrants is lower than that for stocks, but they are more volatile.

Hence, their rate of potential gain or loss is much higher than their underlying.

Summary:

Warrants are a leveraged investment tool.

Don't foreget that the leverage effect can mean more profit, but also more loss.

So do limit your investment amount in warrants.

Index Futures

In terms of trading, index futures are more straightforward.

When the index rises by a certain percentage, an index future buyer will gain while an index future seller will lose, exactly the same amount.

Trading in index futures is a zero sum game, and buyers and sellers gamble against each other.

Regarding capital requirement, a margin is payable upfront for an index future contract.

The investor has to pay the shortfall (margin call) to maintain the account balance at not less than the maintenance margin level.

An example: The initial margin required for a particular Index futures contract is $688 and the maintenance margin required is $550. Each point of the index is priced at $16. The investor will face a margin call if the particular index drops by more than 13 points, as the investor has to pay the shortfall to maintain the account balance at not less than the maintenance margin level.

When the index rises by a certain percentage, an index future buyer will gain while an index future seller will lose, exactly the same amount.

Trading in index futures is a zero sum game, and buyers and sellers gamble against each other.

Regarding capital requirement, a margin is payable upfront for an index future contract.

The investor has to pay the shortfall (margin call) to maintain the account balance at not less than the maintenance margin level.

An example: The initial margin required for a particular Index futures contract is $688 and the maintenance margin required is $550. Each point of the index is priced at $16. The investor will face a margin call if the particular index drops by more than 13 points, as the investor has to pay the shortfall to maintain the account balance at not less than the maintenance margin level.

Wednesday 9 September 2015

Currency plays - Foreign Currency Deposit, Foreign Exchange Futures and Currency Warrants.

Foreign Currency Deposit

The easiest way to invest in foreign exchange (FX) is to switch your Ringgit dollar deposit for a foreign currency deposit.

FX futures or leveraged FX

To capture short term movements, some investors may choose to invest in FX futures or leveraged FX products. (However, foreign exchange spreads charged by banks vary from one to another. Besides, for futures trading, investors are required to open a futures account. There is also the risk of margin calls. This is obviously not every investor's cup of tea.)

Currency Warrants

The trading mechanism of Currency Warrants is much the same as other warrants. Investors only have to pick a suitable warrant in terms of price and maturity, as well as implied volatility, which should be relatively low as compared with others with similar terms.

Foreign exchange is a relative game. For a Currency Warrant, investors must always make sure which one in the currency pair is the positive play and which on the negative play.

Additional notes:

Compared with other investment instruments, Currency Warrants are more flexible. They can give a higher potential return without the risk of margin calls in futures trading. So, they are suitable for investors who want to profit from foreign exchange, but have relatively low tolerance for high risks.

Currency Warrants have limited downside, but unlimited upside. So, if one gets the market wrong and is wise enough to stop loss, the loss will be just a portion of the capital Yet, no matter how small the investment amount is, one should always stop loss if one gets the market wrong.

The easiest way to invest in foreign exchange (FX) is to switch your Ringgit dollar deposit for a foreign currency deposit.

FX futures or leveraged FX

To capture short term movements, some investors may choose to invest in FX futures or leveraged FX products. (However, foreign exchange spreads charged by banks vary from one to another. Besides, for futures trading, investors are required to open a futures account. There is also the risk of margin calls. This is obviously not every investor's cup of tea.)

Currency Warrants

The trading mechanism of Currency Warrants is much the same as other warrants. Investors only have to pick a suitable warrant in terms of price and maturity, as well as implied volatility, which should be relatively low as compared with others with similar terms.

Foreign exchange is a relative game. For a Currency Warrant, investors must always make sure which one in the currency pair is the positive play and which on the negative play.

Additional notes:

Compared with other investment instruments, Currency Warrants are more flexible. They can give a higher potential return without the risk of margin calls in futures trading. So, they are suitable for investors who want to profit from foreign exchange, but have relatively low tolerance for high risks.

Currency Warrants have limited downside, but unlimited upside. So, if one gets the market wrong and is wise enough to stop loss, the loss will be just a portion of the capital Yet, no matter how small the investment amount is, one should always stop loss if one gets the market wrong.

Options - Trading mechanism

If you are optimistic about the underlying, you can buy a call option or write a put option.

If you are negative about the underlying, you can choose to buy a put option or write a call option.

If you are positive about the underlying

If an investor wants to buy a call option, he needs to pay a premium upfront. In case the underlying price does rise above the strike price, the investor can exercise the option to earn the difference.

If the investor chooses to write a put option, he will receive a premium. If the underlying price climbs above the strike price, the put option will become worthless (and not exercised), leaving the premium safe in the hands of the investor. In writing a put option, the investor is required to deposit a margin and face the risk of unlimited loss (in theory), the underlying price can drop to zero).

If you are negative about the underlying

If the investor chooses to buy a put option, he needs to pay a premium upfront. In case the underlying price does fall below the strike price, the investor can exercise the option to earn the difference.

If the investor chooses to write a call option, and if the underlying price falls below the strike price, he will pocket the full amount of the premium. On the other hand, if the underlying price is higher than the strike price, he will face the risk of unlimited loss (in theory, the underlying price can go up indefinitely).

Warrants versus Options

In the case of warrants, the investor can only be a buyer, and choose between call warrants or put warrants. The seller is always the issuer.

While options offer more possibilities, the risk is also much bigger. In contrast, warrants are only subject to limited risk exposure.

If you are negative about the underlying, you can choose to buy a put option or write a call option.

If you are positive about the underlying

If an investor wants to buy a call option, he needs to pay a premium upfront. In case the underlying price does rise above the strike price, the investor can exercise the option to earn the difference.

If the investor chooses to write a put option, he will receive a premium. If the underlying price climbs above the strike price, the put option will become worthless (and not exercised), leaving the premium safe in the hands of the investor. In writing a put option, the investor is required to deposit a margin and face the risk of unlimited loss (in theory), the underlying price can drop to zero).

If you are negative about the underlying

If the investor chooses to buy a put option, he needs to pay a premium upfront. In case the underlying price does fall below the strike price, the investor can exercise the option to earn the difference.

If the investor chooses to write a call option, and if the underlying price falls below the strike price, he will pocket the full amount of the premium. On the other hand, if the underlying price is higher than the strike price, he will face the risk of unlimited loss (in theory, the underlying price can go up indefinitely).

Warrants versus Options

In the case of warrants, the investor can only be a buyer, and choose between call warrants or put warrants. The seller is always the issuer.

While options offer more possibilities, the risk is also much bigger. In contrast, warrants are only subject to limited risk exposure.

Five Major Factors influencing Warrant Price

1. Underlying price

2. Days to Maturity.

3. Implied Volatility

4. Interest Rate

5. Dividend.

2. Days to Maturity.

3. Implied Volatility

4. Interest Rate

5. Dividend.

How to trade warrants?

1. Select a bank or broker.

2. Open a securities account.

3. Monitor warrant trading through a stock quote terminal.

4. Study carefully the underlying stock and the terms of the warrant.

5. Trade warrant.

2. Open a securities account.

3. Monitor warrant trading through a stock quote terminal.

4. Study carefully the underlying stock and the terms of the warrant.

5. Trade warrant.

Saturday 22 August 2015

Saturday 15 August 2015

"I'm in prison, but I'm on just the same playing field as Warren Buffett,"

Curtis Carroll discovered the stock market in prison. Through friends and family on the outside, he invests from San Quentin State Prison in Northern California, and he's also an informal financial adviser to fellow inmates and correctional officers. Everyone in prison calls him Wall Street.

Read more here.

"I couldn't believe that this kind of access to this type of money could be accessible to anybody. Everybody should do it. And it's legal!" he says.

He pores over financial news: the Wall Street Journal, USA Today, Forbes. Business is like a soap opera, he says, and he's always trying to anticipate what will happen next. "I like to know what the CEO's doing," he says. "I like to know who's in trouble."

Read more here.

Wednesday 12 August 2015

Chinese central bank under pressure to weaken yuan further

Sources say China's move to devalue its currency reflects a growing clamour within government circles for a weaker yuan to help struggling exporters, ensuring the central bank remains under pressure to drag it down further in the months ahead. – Reuters pic, August 12, 2015.

China's move to devalue its currency reflects a growing clamour within government circles for a weaker yuan to help struggling exporters, ensuring the central bank remains under pressure to drag it down further in the months ahead, sources said.

The yuan has fallen almost 4% in two days since the central bank announced the devaluation yesterday, but sources involved in the policy-making process said powerful voices inside the government were pushing for it to go still lower.

Their comments, which offer a rare insight into the argument going on behind the scenes in Beijing, suggest there is pressure for an overall devaluation of almost 10%.

"There have been internal calls for the exchange rate to be more flexible, or depreciated appropriately, to help stabilise external demand and growth," said a senior economist at a government think-tank that advises policy-makers in Beijing.

"I think yuan deprecation within 10% will be manageable. There should be enough depreciation, otherwise it won't be able to stimulate exports."

The Commerce Ministry, which today publicly welcomed the devaluation as an export stimulus, had led the push for Beijing to abandon its previous strong-yuan policy.

Reuters could not verify how much influence Commerce Ministry officials had wielded in the decision to drive the yuan lower, but the sources said its officials were claiming victory after a long lobbying campaign against what some of them regarded as over-zealous reform led by the central bank.

The People's bank of China (PBOC) had been keeping the yuan strong to support the ruling Communist Party's goal of shifting the economy's main engine from exports to domestic demand.

A stronger yuan boosts domestic buying power, helps Chinese firms to borrow and invest abroad, and encourages foreign firms and governments to increase their use of the currency.

Until the devaluation, the currency had appreciated overall by 14% over the past 12 months on a trade-weighted basis, according to data from the Bank for International Settlements.

Premier Li Keqiang had repeatedly ruled out devaluation, but increased risks to economic growth, exacerbated by recent stock market turmoil, increased pressure to reverse course, the sources said.

At the weekend, China posted a shock 8.3% slump in July exports.

"Exporters face very big pressure, and China's economy also faces very big downward pressure," said a researcher at the commerce ministry's own think-tank, which recommended earlier this year that the government should unshackle the yuan.

"The yuan depreciated only slightly versus the dollar, but it has gained sharply against other currencies. China's economy and trade are no longer strong; why should the yuan be strong?"

He said he believed the yuan could fall to 6.7 by year-end, which would represent a near 9% decline since the eve of the devaluation. It traded around 6.43 against the dollar today, its lowest since August 2011.

The PBOC described its devaluation as a one-off move designed to make the currency more responsive to market forces.

The central bank guides the market daily by setting a reference rate for the yuan, from which trade may vary only 2%. Yesterday, it said it was setting the midpoint based on market forces, which have been willing the yuan lower.

Beijing is determined to achieve its economic growth target of 7% for this year. Top leaders will chart the course for the next five years at a meeting in October, and they are likely to continue targeting annual growth of around 7%.

"They (top leaders) are determined to hit 7% target. The downward pressure is big (but) so is the determination," said an economist inside the cabinet's think-tank.

Beijing prefers a gradual devaluation because a single, big move could spark capital flight and undermine its goal of fostering global use of the yuan in trade and finance, sources said.

China has been lobbying the IMF to include the yuan in its basket of reserve currencies, known as Special Drawing Rights, which it uses to lend to sovereign borrowers. This would mark a major step in terms of international use of the yuan.

The IMF said today that the central bank's new way of managing the exchange rate appeared to be a welcome step.

"There is definitely downward pressure on the economy, but we cannot rely (alone) on currency depreciation," said Zhu Baoliang, chief economist at the State Information Centre, a top government think-tank. – Reuters, August 12, 2015.

- See more at: http://www.themalaysianinsider.com/business/article/chinese-central-bank-under-pressure-to-weaken-yuan-further#sthash.dx7bFam1.dpuf

Monday 10 August 2015

My Check Lists

Here is a Ben Graham Checklist for Finding Undervalued Stocks

Criterias

Valuation

Risk

1. Earnings to price (the inverse of P/E) is double the high-grade corporate bond yield. If the high-grade bond yields 7%, then earnings to price should be 14%.

2. P/E ratio that is 0.4 times the highest average P/E achieved in the last 5 years.

3. Dividend yield is 2/3 the high-grade bond yield.

4. Stock price of 2/3 the tangible book value per share.

5. Stock price of 2/3 the net current asset value.

Quality of Balance Sheet and Management

Financial strength

6. Total debt is lower than tangible book value.

7. Current ratio (current assets/current liabilities) is greater than 2.

8. Total debt is no more than liquidation value.

Quality of Growth

Earnings stability

9. Earnings have doubled in most recent 10 years.

10. Earnings have declined no more than 5% in 2 of the past 10 years.

If a stock meets 7 of the 10 criteria, it is probably a good value, according to Graham

Criterias

Valuation

Risk

1. Earnings to price (the inverse of P/E) is double the high-grade corporate bond yield. If the high-grade bond yields 7%, then earnings to price should be 14%.

2. P/E ratio that is 0.4 times the highest average P/E achieved in the last 5 years.

3. Dividend yield is 2/3 the high-grade bond yield.

4. Stock price of 2/3 the tangible book value per share.

5. Stock price of 2/3 the net current asset value.

Quality of Balance Sheet and Management

Financial strength

6. Total debt is lower than tangible book value.

7. Current ratio (current assets/current liabilities) is greater than 2.

8. Total debt is no more than liquidation value.

Quality of Growth

Earnings stability

9. Earnings have doubled in most recent 10 years.

10. Earnings have declined no more than 5% in 2 of the past 10 years.

If a stock meets 7 of the 10 criteria, it is probably a good value, according to Graham

If you're income oriented, Graham recommended paying special attention to items 1 through 7.

If you're concerned about growth and safety, items 1 through 5 and 9 and 10 are important.

If you're concerned with aggressive growth, ignore item 3, reduce the emphasis on 4 through 6, and weigh 9 and 10 heavily.

Again, these checklists are a guideline and example, not a cookbook recipe you should follow precisely. They are a way of thinking and an example of how you may construct your own value investing system.

The criteria mentioned above are probably more focussed on dividends and safety than even today's value investors choose to be. But today's value investing practice owes an immense debt to this type of financial and investment analysis.

Spreadsheet for finding Undervalue Stocks

http://spreadsheets.google.com/pub?key=tZGNWHLD2d2nTgCcxSKyoCA&output=html

If you're concerned about growth and safety, items 1 through 5 and 9 and 10 are important.

If you're concerned with aggressive growth, ignore item 3, reduce the emphasis on 4 through 6, and weigh 9 and 10 heavily.

Again, these checklists are a guideline and example, not a cookbook recipe you should follow precisely. They are a way of thinking and an example of how you may construct your own value investing system.

The criteria mentioned above are probably more focussed on dividends and safety than even today's value investors choose to be. But today's value investing practice owes an immense debt to this type of financial and investment analysis.

Spreadsheet for finding Undervalue Stocks

http://spreadsheets.google.com/pub?key=tZGNWHLD2d2nTgCcxSKyoCA&output=html

If you're income oriented, Graham recommended paying special attention to items 1 through 7.

--------------------------

If you're concerned about growth and safety, items 1 through 5 and 9 and 10 are important.

---------------------------

If you're concerned with aggressive growth, ignore item 3, reduce the emphasis on 4 through 6, and weigh 9 and 10 heavily.

Quote

Criterias

Valuation

Risk

1. Earnings to price (the inverse of P/E) is double the high-grade corporate bond yield. If the high-grade bond yields 7%, then earnings to price should be 14%.

2. P/E ratio that is 0.4 times the highest average P/E achieved in the last 5 years.

3. Dividend yield is 2/3 the high-grade bond yield.

4. Stock price of 2/3 the tangible book value per share.

5. Stock price of 2/3 the net current asset value.

Quality of Balance Sheet and Management

Financial strength

6. Total debt is lower than tangible book value.

7. Current ratio (current assets/current liabilities) is greater than 2.

8. Total debt is no more than liquidation value.

Quality of Growth

Earnings stability

9. Earnings have doubled in most recent 10 years.

10. Earnings have declined no more than 5% in 2 of the past 10 years.

--------------------------

If you're concerned about growth and safety, items 1 through 5 and 9 and 10 are important.

Quote

Criterias

Valuation

Risk

1. Earnings to price (the inverse of P/E) is double the high-grade corporate bond yield. If the high-grade bond yields 7%, then earnings to price should be 14%.

2. P/E ratio that is 0.4 times the highest average P/E achieved in the last 5 years.

3. Dividend yield is 2/3 the high-grade bond yield.

4. Stock price of 2/3 the tangible book value per share.

5. Stock price of 2/3 the net current asset value.

Quality of Balance Sheet and Management

Financial strength

6. Total debt is lower than tangible book value.

7. Current ratio (current assets/current liabilities) is greater than 2.

8. Total debt is no more than liquidation value.

Quality of Growth

Earnings stability

9. Earnings have doubled in most recent 10 years.

10. Earnings have declined no more than 5% in 2 of the past 10 years.

---------------------------

If you're concerned with aggressive growth, ignore item 3, reduce the emphasis on 4 through 6, and weigh 9 and 10 heavily.

Quote

Criterias

Valuation

Risk

1. Earnings to price (the inverse of P/E) is double the high-grade corporate bond yield. If the high-grade bond yields 7%, then earnings to price should be 14%.

2. P/E ratio that is 0.4 times the highest average P/E achieved in the last 5 years.

3. Dividend yield is 2/3 the high-grade bond yield.

4. Stock price of 2/3 the tangible book value per share.

5. Stock price of 2/3 the net current asset value.

Quality of Balance Sheet and Management

Financial strength

6. Total debt is lower than tangible book value.

7. Current ratio (current assets/current liabilities) is greater than 2.

8. Total debt is no more than liquidation value.

Quality of Growth

Earnings stability

9. Earnings have doubled in most recent 10 years.

10. Earnings have declined no more than 5% in 2 of the past 10 years.

Risk-reward Does Not Make Sense At The Moment

Stan Druckenmiller: Bloomberg Encore (04/24)

8:01 AM MYT

April 25, 2015

April 24 -- Legendary money manager Stan Druckenmiller speaks to Bloomberg's Stephanie Ruhle. The exclusive interview covers topics including Federal Reserve policy, oil prices, the Greek debt crisis and much more. The founder of Duquesne Capital Management shares insights, predictions and in-depth analysis of global markets and the U.S. economy in 2015.

http://www.bloomberg.com/news/videos/2015-04-25/stan-druckenmiller-bloomberg-encore-04-24-

8:01 AM MYT

April 25, 2015

April 24 -- Legendary money manager Stan Druckenmiller speaks to Bloomberg's Stephanie Ruhle. The exclusive interview covers topics including Federal Reserve policy, oil prices, the Greek debt crisis and much more. The founder of Duquesne Capital Management shares insights, predictions and in-depth analysis of global markets and the U.S. economy in 2015.

http://www.bloomberg.com/news/videos/2015-04-25/stan-druckenmiller-bloomberg-encore-04-24-

Subscribe to:

Posts (Atom)