Wednesday, 31 August 2011

Public belief about best long term investment

Public beliefs about long term investment returns from different asset classes

Staggering (to me anyway) study out from Gallup a couple of weeks ago about the public’s beliefs about which asset classes offer the best long term investing returns.

When asked “which of the following do you think is the best long term investment?” 34% of the 1000-odd telephone interviews picked savings accounts with 33% picking real estate. Stocks and mutual funds crept in at a lowly 15% (see below).

Long Term Investing by Uncle8888

http://createwealth8888.blogspot.com/2011/08/investing-made-simple-by-uncle8888-22.html

Tuesday, 9 August 2011

Investing Made Simple by Uncle8888 (22)

Read? Investing Made Simple by Uncle8888 (21)

ST, Tuesday, August 9, 2011

S'pore retail investors make flight to safety. Massive volumes of stocks traded as many prefer cash to equity.

Engineer Sun Weixin, 28, liquidated his entire portfolio of mainly bank and blue-chip shares yesterday, worth less than $40,000. He suffered a loss but did not want to disclose the amount - but said he felt there is too too much uncertainty to stay invested.

Read? investors flock to low-risk assets, with focus on cash

Read? Should I sell all my equities and stay sideline?

Should Uncle8888 also sell out all equities and stay sideline?

Since 2001 he has been thinking very hard each time a Bear market arrived whether he should sell out all his equities and stay sideline until certainty come back to the stock market before reinvesting. This time is no different and he is thinking very hard too.

So actually what has happened to him during the past Bear markets for being stubborn or stupid?

He has been holding the following stocks across several bear markets:

His initial DBS holding is also cheaper by 16% after the 2:1 right issue; and internally price adjusted for all unit shares based on theoretical fair value of right issue shares.

There was no corporate action on Semb Corp. :-(

TSR as on Monday closing, 8 Aug 2011

For the coming Bear market, he is even more stupid to slide with the Bear with more members on board.

http://wincrt.blogspot.com/2011/08/create-wealth-through-long-term_09.html

ST, Tuesday, August 9, 2011

S'pore retail investors make flight to safety. Massive volumes of stocks traded as many prefer cash to equity.

Engineer Sun Weixin, 28, liquidated his entire portfolio of mainly bank and blue-chip shares yesterday, worth less than $40,000. He suffered a loss but did not want to disclose the amount - but said he felt there is too too much uncertainty to stay invested.

Read? investors flock to low-risk assets, with focus on cash

Read? Should I sell all my equities and stay sideline?

Should Uncle8888 also sell out all equities and stay sideline?

Since 2001 he has been thinking very hard each time a Bear market arrived whether he should sell out all his equities and stay sideline until certainty come back to the stock market before reinvesting. This time is no different and he is thinking very hard too.

So actually what has happened to him during the past Bear markets for being stubborn or stupid?

He has been holding the following stocks across several bear markets:

- Kep Corp since 2001

- Semb Corp since 2002

- DBS since 2003

His initial DBS holding is also cheaper by 16% after the 2:1 right issue; and internally price adjusted for all unit shares based on theoretical fair value of right issue shares.

There was no corporate action on Semb Corp. :-(

TSR as on Monday closing, 8 Aug 2011

For the coming Bear market, he is even more stupid to slide with the Bear with more members on board.

Will Uncle8888 survive this Bear to write more stories on short-term trading and long-term investing using his Pillow stocks strategy and finding Touch Stones?

http://wincrt.blogspot.com/2011/08/create-wealth-through-long-term_09.html

Never Sell A Winner and you end up being a long term investor

I will regularly add to my winners (at ever higher prices), and I will cull the losers from the portfolio during market corrections. But most importantly, it is my intention to never sell my winners.

Warren Buffett didn’t get rich by selling 10% gains on his stocks and companies. He (and his investors) have gotten rich by making “permanent” investments. His timeframe is famously “forever.”

I expect my “forever” to be a very long time. If my investments are in companies that are consistently earning money and growing their businesses, and I stick with them through thick and thin, do you think I’ll be able to outperform the 1% APR I’m earning on my savings account these days? I think so.

http://www.chicagosean.com/2011/03/06/never-sell-a-winner/

Warren Buffett didn’t get rich by selling 10% gains on his stocks and companies. He (and his investors) have gotten rich by making “permanent” investments. His timeframe is famously “forever.”

I expect my “forever” to be a very long time. If my investments are in companies that are consistently earning money and growing their businesses, and I stick with them through thick and thin, do you think I’ll be able to outperform the 1% APR I’m earning on my savings account these days? I think so.

http://www.chicagosean.com/2011/03/06/never-sell-a-winner/

Tuesday, 30 August 2011

Long-term Investing: An Insight

http://www.marinisgroup.com.au/articles/long-term-investing.pdf

This is the first paper in an annually updated series that gives investors an

insight into longer-term returns from various asset classes. It is aimed at

helping investors think carefully about their portfolio decisions. Investors should

understand their personal time horizons for their various investment portfolios

so that sensible, wealth-enhancing decisions can be made. Simplistically, an

investor saving for a home deposit in one year’s time will be focused on capital

preservation, whereas an investor saving for retirement in 30 years’ time will

place greater importance on capital growth and long-term returns. This paper

should be read alongside another Perennial paper, The Wisdom of Great

Investors, which brings together the principles of investing from some of the

world’s greatest investors.

http://www.marinisgroup.com.au/articles/the-wisdom-of-great-investors.pdf

The Wisdom of Great Investors

“If you can keep your head when all about you are losing theirs . . . yours is the Earth and everything

that’s in it.” And what’s more, you’ll be a successful investor!

(Apologies to Rudyard Kipling

The Wisdom of Great Investors brings together the principles of investing from some of the world’s

greatest investors who have not only lived through but also prospered in diffi cult times.

Though each of these great investors offers a different perspective, the common theme is that

a disciplined, patient, emotionally detached investment approach can help you to reach your

long-term fi nancial goals.

At Perennial, we believe their collective thoughts are an invaluable insight into long-term investing

and may help you in preparing your own mindset to successfully build and preserve long-term

wealth.

http://www.marinisgroup.com.au/

This is the first paper in an annually updated series that gives investors an

insight into longer-term returns from various asset classes. It is aimed at

helping investors think carefully about their portfolio decisions. Investors should

understand their personal time horizons for their various investment portfolios

so that sensible, wealth-enhancing decisions can be made. Simplistically, an

investor saving for a home deposit in one year’s time will be focused on capital

preservation, whereas an investor saving for retirement in 30 years’ time will

place greater importance on capital growth and long-term returns. This paper

should be read alongside another Perennial paper, The Wisdom of Great

Investors, which brings together the principles of investing from some of the

world’s greatest investors.

http://www.marinisgroup.com.au/articles/the-wisdom-of-great-investors.pdf

The Wisdom of Great Investors

“If you can keep your head when all about you are losing theirs . . . yours is the Earth and everything

that’s in it.” And what’s more, you’ll be a successful investor!

(Apologies to Rudyard Kipling

The Wisdom of Great Investors brings together the principles of investing from some of the world’s

greatest investors who have not only lived through but also prospered in diffi cult times.

Though each of these great investors offers a different perspective, the common theme is that

a disciplined, patient, emotionally detached investment approach can help you to reach your

long-term fi nancial goals.

At Perennial, we believe their collective thoughts are an invaluable insight into long-term investing

and may help you in preparing your own mindset to successfully build and preserve long-term

wealth.

http://www.marinisgroup.com.au/

Are you a landlord?

“Landlording and long-term investing go hand-in hand. Being a landlord isn’t for everyone, but if you have the right personality and decision making skills then it’s a snap.”

Sunday, 28 August 2011

Market crash 'could hit within weeks', warn bankers

A more severe crash than the one triggered by the collapse of Lehman Brothers could be on the way, according to alarm signals in the credit markets.

9:50PM BST 24 Aug 2011

Insurance on the debt of several major European banks has now hit historic levels, higher even than those recorded during financial crisis caused by the US financial group's implosion nearly three years ago.

Credit default swaps on the bonds of Royal Bank of Scotland, BNP Paribas, Deutsche Bank and Intesa Sanpaolo, among others, flashed warning signals on Wednesday. Credit default swaps (CDS) on RBS were trading at 343.54 basis points, meaning the annual cost to insure £10m of the state-backed lender's bonds against default is now £343,540.

The cost of insuring RBS bonds is now higher than before the taxpayer was forced to step in and rescue the bank in October 2008, and shows the recent dramatic downturn in sentiment among credit investors towards banks.

"The problem is a shortage of liquidity – that is what is causing the problems with the banks. It feels exactly as it felt in 2008," said one senior London-based bank executive.

"I think we are heading for a market shock in September or October that will match anything we have ever seen before," said a senior credit banker at a major European bank.

Despite this, bank shares rebounded on Wednesday, showing the growing disconnect between equity and credit investors. RBS closed up 9pc at 21.87p, while Barclays put on 3pc to 149.6p despite credit default swaps on the bank hitting a 12-month high. This mirrored the US trend, with Bank of America shares up 10pc in late Wall Street trade after a hitting a 12-month low on Tuesday over fears that it might have to raise as much as $200bn (£121bn). As with the European banks, the rebound in the share price was not reflected in the credit markets, where its CDS reached a 12-month high of 384.42 basis points.

European stock markets joined in the rally. The FTSE closed up 1.5pc at 5,206 on hopes the chance of a global recession had diminished. European shares hit a one-week high, with Germany's DAX closing up 2.7pc and France's CAC 1.8pc higher. The Dow Jones index edged higher on strong durable goods orders data as markets began to accept that the US Federal Reserve is unlikely to signal fresh stimulus at Jackson Hole this Friday.

Even Moody's decision to downgrade Japan's sovereign credit rating by one notch to Aa3 did little to damage global sentiment, although Tokyo's Nikkei closed down just over 1pc.

As stock market nerves settled, gold - which has recorded steady gains recently as investors seek a safe haven - fell 5.3pc to $1,777 in London.

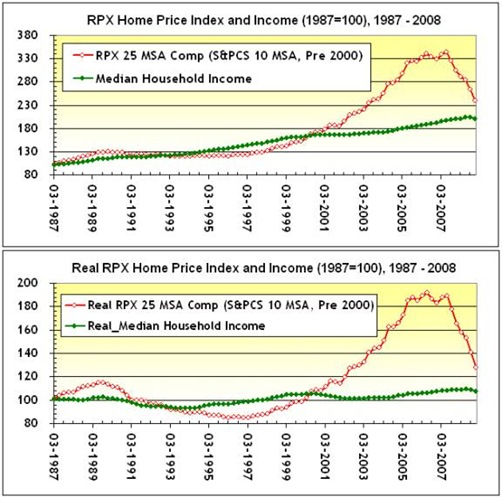

US Home Prices and Income, 1987 – 2008

Home Prices and Income, 1987 – 2008, Nominal [top] and Real [bottom]

As the bottom chart of inflation-adjusted home prices and income demonstrates, even as real household income meandered along a relatively flat path, home prices exploded after 2001. This was due, in part, to:

- A steep yield curve;

- The widespread use of ARMS;

- Flexible mortgage underwriting standards; and

- Mortgage product innovations (subprime, Alt-A, Option ARMs).

All of the above encouraged home ownership. By 2006, prices had peaked, and began to correct.

Benefiting from Investor Over-reaction in major market crisis

Many investors overreact during times of crises. Retail investors especially tend to panic and sell out at the bottom and then buy at the top when the market rebounds. The fear of losing out on a rally and recoup some of their losses forces them to act this way. This classic scenario occurred in the aftermath of the recent financial crisis.After seeing their portfolio values decline consistently for many months some investors threw in the towel and sold out right when the market was hitting the lows in March 2009. These investors couldn’t be more wrong. From the lows of March 10, 2009 the S&P 500 rallied a spectacular 80% by April of 2010. The moral of the story here is that investors should not panic and sell out when the market is already down significantly. The market rewards patient investors who hold investments for the long-term as opposed to trying to time the market in the short-term for a quick profit.

In general, how does the markets perform post major crises?

The chart below shows the 1-year and 2-year returns of Dow Jones Industrial Average(DJIA) after 12 major post-war crises:

The returns assume reinvestment of dividends and distributions. Similar to the S&P 500, the Dow Jones Index gained 65% and 95% in 1 year and 2 years respectively after the 2008-09 global financial crisis. Overall the index was up by double digits in the periods mentioned after each of the crises shown in the chart above.

http://topforeignstocks.com/2011/06/25/stock-market-performance-post-major-crises/

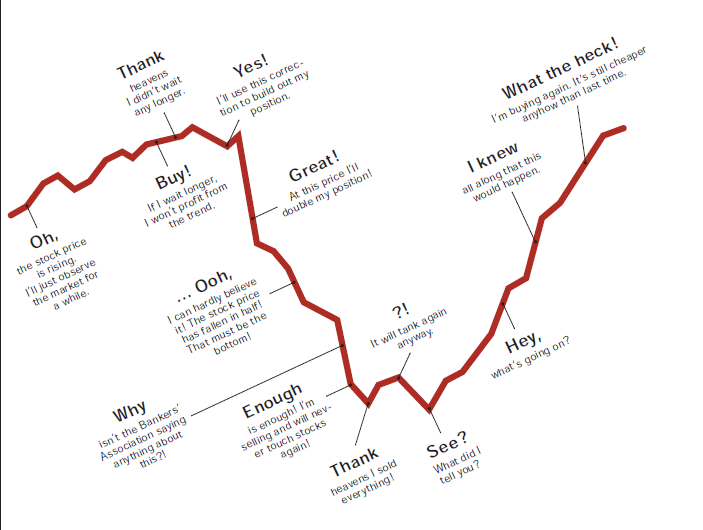

Phrases of Market Phases

Investing in the markets is not suitable for everyone.One should have a strong stomach when markets dive and not get carried away with greed when markets soar.The chart shows the various stages of emotions that most investors experience with investing in equities.

http://topforeignstocks.com/category/strategy/page/2/

Subscribe to:

Posts (Atom)