What are REITs?

REITs stand for Real Estate Investment Trusts. They are specialized companies that invest in commercial, industrial, residential and healthcare real estates. Examples on the Singapore Stock Exchange includes CapitaCommerical Trust (Commercial), Cambridge Industrial REIT (industrial), Saizen REIT (residential) and Parkway Life REIT (healthcare). These companies buy and manage properties including shopping malls, offices, hotels, hospitals.

REITs usually pay a generous dividend because they are required by law to distribute most of their earnings to shareholders. In exchange, they receive tax incentives.

Perhaps, we can view REITs as an instrument to buy and own a small portion of a property, while at the same time shared fundings with many other shareholders to employ someone to manage that piece of property. With REITs, we can invest in real estate with no leverage, no property and no need for any stress in finding tenants and collecting rent from them.

REITs investment generally focus on dividend yield. Also, like any stocks on the exchange, investing REITs can also result in capital gain. The same can be said of investing in real properties. However, because REITs are traded on the stock exchange, it's liquidity is much higher than the actual property itself.

So how do we choose what types of REITs to invest in? I'm not an expert in it, but I shall share some basics of what I think.

The factors that are important to me are:

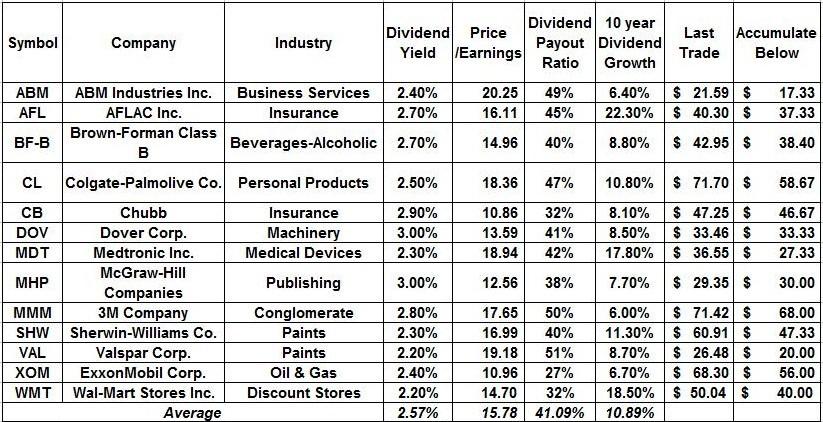

1) Dividend yield with regards to current stock price, as with how we choose most dividend stocks

2) Gearing

3) Growth potential

4) Sector

5) Sponsor/Backer

1) Dividend yield

Basically, I will be happy with any dividend yield from 6~8% considering that I do not need to actively monitor the stock price. Choosing and buying those with dividend yield of >6% will mean that should anything unforseen occurs, a reduction in DPU would perhaps still beat putting the money in the bank anytime. Of course, reduction in DPUs would likely bring about a drop in the share price as well till the dividend yield is back to the 'acceptable' range. This should not matter if we are taking a longer term investment view as the dividends would eventually pay itself off.

2) Gearing

With the recent credit crisis, there are companies who have to stop dividend payouts, do placement, issue rights, etc, in order to remain in business. If the gearing is low, refinancing of debts is usually a problemless affair. However, if the gearing is high, as in Saizen REIT and Rickmers Maritime, the ability to refinance debts at critical juncture is hampered. The ability to remain as a going concern would be cast in doubt, and this would make it even harder for refinancing.

3) Growth Potential

A REIT which is actively, but conservatively, acquiring properties would in the long run benefit the shareholders with increasing NAV and increasing dividend yield.

4) Sector

The different sectors mentioned earlier, commercial, industrial, residential and healthcare are different in nature. Industrial and healthcare related properties are usually more defensive in revenue, hence the dividend yield would be more consistent. For commercial and residential sectors, the rents could vary more as the tenants are much more mobile. Hence, the dividend yield could fluctuate. However, for the risk, the yield is usually higher.

At the moment, for REITs, I have only CapitaCommercial Trust and Starhill Global REIT, both in the commercial sector. I hope to eventually include the other 3 sectors so that there will be some diversification.

5) Sponsor/Backer

A strong sponsor like Temasek Holdings, Capitaland, or YTL Corporation would be key to the success of the REIT in refinancing its loans.

![[AztechDividends.gif]](https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEjuXvHz5aR0PCJ-ldWIUjWLqK-qKJdYngRmE2R5VBCMslLTIdOFDxH71ORZo6vAPdwkNiJefLBN0AMSAB71QUKDRAYf0vy92MYLM5fPKelWKegX3TKpoRdyMKb1qNpvktOxY5xXJ6ywXDzo/s640/AztechDividends.gif)

Make your child a millionaire Photo: GETTY

Parents could make their baby an adult millionaire by starting a pension pot when they are born. While it may be hard to imagine your children reaching retirement, by contributing just £88 per month to a child self invested pension plan (SIPP) until the age of 18, the fund should easily top £1 million by the time they reach 65.

For most parents, saving regularly is an integral part of securing their child's financial future and with the abolition of Child Trust Funds, parents could consider pensions as an alternative way to provide financial stability.

Making regular contributions to a child's pension may not seem like the obvious choice. However, given the flexible nature of SIPPs and the tax relief offered by the Government, they can provide a very simple way of securing children's financial future in retirement.

While they won't have the money until they are 55 at the earliest, knowing that there are pension plans in place will give them greater choice over what they spend their money on when they are younger.

Steve Latto, head of pensions at Alliance Trust Savings, said: "Financial planning for children is always a high priority for parents who wish to safeguard their children's financial future. We have a significant number of parents already using an Alliance Trust Savings SIPP for their children in order to take advantage of the tax relief and flexibility that SIPPs offer."

HOW DOES IT WORK?

You can put a maximum of £2,880 into a personal pension for a child each year. The Government will add £720 in tax relief, boosting the value to £3,600. Put another way, this equates to 25 per cent growth on your money on day one. The investments then grow free from income and capital gains tax.

Better still, the £2,880 yearly contribution falls below the £3,000 annual gift limit for inheritance tax (IHT). This removes the money from your estate for tax purposes even if you die before the normal seven-year threshold, potentially saving your heirs 40 per cent in tax.

This would take the effective cost of the £3,600 pension investment down to £1,728 a year, or a total of £31,104 over 18 years. This tax-efficient way to give money to your relatives while you are still alive is sometimes known as "giving with warm hands".

Tom McPhail, pensions expert at Hargreaves Lansdown, said: "Setting up a pension for a child is one of the most efficient financial gifts you can make. You get tax relief on the contribution and the child benefits from tax-free growth. Because the money is invested over such a long term – up to 55 years or more, you have the luxury of taking a unique long view on the investment strategy which presents the opportunity to really go for maximum returns."

BUT WHY IS IT SO IMPORTANT TO START AT AS SOON AS THE CHILD IS BORN?

This is largely thanks to the miracle of compound interest. If, instead of starting the pension at birth, your child starts contributing once he or she starts work and saves the same £3,600 every year from the ages of 25 to 65, they will end up with a pension pot worth only £590,600 before taking inflation into account, rather than £1.8 million. This is despite them saving for 40 years instead of 18.

Ian Naismith, head of pensions at Scottish Widows, said: "Setting up a pension plan for a child gives them a head-start in saving for retirement and allows plenty of time for their pension funds to grow.

"Money in a pension is also guaranteed to be available for retirement, with no temptation to fritter it away." Remember parents and grandparents can still pay into existing Child Trust Funds, but Mr Naismith says, contribution limits are lower (£1,200 a year compared with £3,600 into a pension, including tax relief) and CTF money is likely to be spent in early adulthood.

While anyone can pay into a pension for a child, the plan has to be arranged by their parent or legal guardian, who will be responsible for it until they reach 18. There is a special declaration to complete, but the application is straightforward and can be done through a financial adviser or direct with an insurance company.

Enlist the help of grandparents and other relatives to put as much as possible into the pension fund as well as in their CTF. You may have to coordinate the payments, but with a maximum CTF contribution of £1,200 a year and a maximum pension contribution of £2,880 a year there's plenty of scope for several people to make gifts that the child will be really grateful for in the future.

SO, DOES THIS MEAN THAT THE CHILD WOULD NOT NEED TO MAKE THEIR OWN PENSION CONTRIBUTIONS AS AN ADULT?

Unfortunately not, said Mr Naismith. "It's unlikely that contributions made for children will be enough for them to retire on, given that the maximum is currently £3,600 a year including tax relief," he said.

"It should be thought of more as a foundation for retirement planning, and one the child will hopefully build on when they start earning."

Mr McPhail said that the beauty of starting a pension for your children means that they will have more financial freedom when they reach adulthood, allowing them to concentrate on housing and education costs.

"At a time when we are all looking at having to work longer, starting a pension early for your children removes a financial burden, which will leave them free to concentrate on more immediate needs without having to work until they are 70 as a consequence."