Although there are several formulas you can use, there are no black-and-white answers on valuation techniques.

It’s important to conduct your own research, then get independent advice from a business valuer or broker. Here are four of the most commonly used valuation methods.

Method 1: Asset valuation

Method 2: Capitalised future earnings

Method 3: Earnings multiple

Method 4: Comparable sales

Method 1: Asset valuation

This approach determines the value of a business by adding up the value of its assets and subtracting liabilities. It tells you what the business would be worth if it were closed down today and its assets sold off, but it doesn’t take into account the ability of those assets to generate revenue in the future. For that reason, it may understate the true value of the business.

How it works

1.Add up the value of all the assets such as cash, stock, plant and equipment and receivables.

2.Add up liabilities, such as any bank debts and payments due.

3.Subtract the business’ liabilities from its assets to get the net asset value.

Example

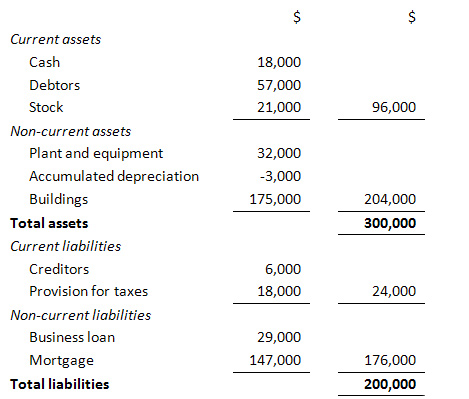

Richard wants to buy a manufacturing business. Here’s an extract from the business’ balance sheet.

With assets of $300,000 and liabilities of $200,000, the net asset value of the business is $100,000.

What about goodwill?

This method doesn’t include a value for goodwill or the right to earn future profits, so it may understate the true value of a business. Goodwill is the difference between the true value of a business and the value of its net assets. It can be crucial to the value of retail and service-based businesses.

For example, when you are valuing a business such as a hairdressing salon, where the standard of service, location and reputation are important, the value of any goodwill would have to be added to net assets to get a valuation.

You need to consider whether goodwill can be transferred when you buy the business. While goodwill can come from physical features such as location, it can also arise from personal factors, such as the owner’s reputation or their relationships with customers or suppliers, which may not be transferable.

And if the business is underperforming and there is no goodwill attached to it, then using the net assets valuation method could be an accurate way of determining its value.

Method 2: Capitalised future earnings

When you buy a business, you’re not only buying its assets. You’re also buying the right to all of the profits that business might generate. Different valuation methods try to capture that.

Capitalising future earnings is the most common method used to value small businesses. The method looks at the rate of return on investment (ROI) that you can expect to get from the business.

How it works

1.Work out the average net profit of the business over the last three years using its profit-and-loss statements. You’ll need to adjust the profit for any one-off expenses or other irregular items each year.

2.Decide the annual rate of return that you’re looking for as a business owner (for example, 20%). There are no hard and fast rules about what number you should choose, except that the higher the risk, the higher your return should be. A good starting point is to compare the business with other investment opportunities — everything from safe havens like term deposits, to riskier investments like shares. You can also look at the rate of return that similar businesses in the same industry achieve.

3.Divide net profits by the rate of return to determine the value of the business, then multiply by 100.

Example

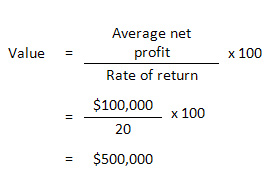

David is looking at buying a bakery business with average net profits of $100,000 per annum after adjustments. David wants an annual rate of return of 20%. The capitalised earnings valuation is:

Method 3: Earnings multiple

If you invest in shares, you might already be familiar with this method, since it’s often used to assess the value of companies whose shares are traded on a stock exchange and therefore reflect market expectations. But it can be used to value unlisted businesses.

Its big advantage is its simplicity. The difficulty lies in deciding which multiple to use.

How it works

Simply multiply the business’ earnings before interest and tax (EBIT) by your selected multiple. For example, you might value the business at twice its annual earnings — so a business with an EBIT of $200,000 might be valued at $400,000.

The multiple you choose will depend on the industry and the growth potential of the business. A service-based business might be valued at as little as one year’s earnings, while an established business with sustainable profits might sell for as much as six times earnings. (Listed companies trade at much higher multiples, because their size and liquidity makes them less risky investments.)

This method can be useful for valuing a business where there are regular sales of similar businesses to help you determine an objective earnings multiple. A business broker should be able to tell you this.

Method 4: Comparable sales

Whatever other valuation method you use, you should also look at prices for recent sales of similar businesses. Like buying a house, it makes sense to know what is happening in the market in which you’re interested.

Speak to a few business brokers and gauge their feeling about the business’ value. They might know what similar operations are selling for and how the market is placed at that particular time. Check business-for-sale listings in relevant industry magazines, newspapers or websites.

Tools and templates

Buying a business checklist

Important information

As this advice has been prepared without considering your objectives, financial situation or needs, you should, before acting on the advice, consider its appropriateness to your circumstances. All products mentioned on this web page are issued by the Commonwealth Bank of Australia; view our Financial Services Guide (PDF 59kb).

http://www.commbank.com.au/business/betterbusiness/buying-a-business/whats-it-worth/

Summary: