Inflation erodes your money systematically.

Inflation simply means that prices of goods and services go up, so the purchasing power of your money decreases and you have to pay more to maintain the lifestyle to which you have become accustomed.

For example, your pension may seem to be adequate now, while you are saving for it. However, after a number of years' retirement, you may suddenly realise that the amount you had set aside is not enough and you cannot maintain your standard of living. With life expectancy on the increase, people often outlive their money.

Even in the current relatively low-inflation environment, inflation can make a big difference in your retirement.

For example: if you hid $1,000 under your mattress today and left it there for 20 years, even at a fairly low inflation rate of 3%, it would have shrunk to the equivalent of $544 - almost half its original value.

So inflation eats away at your money. It has no regard for how hard you have worked, how many hours you have put in or even how efficient you are. Your money simply becomes worth less as time goes by.

Friday, 29 January 2010

Your money's job description and your principal financial goal: "Work to give a real rate of return."

Return is a very important concept in the investment world. It is simply the difference between the money you start off with and the money you end up with. In other words, how your money has grown.

The rate of return is the pace at which you achieve that growth, and is normally expressed as a percentage per year.

The nominal rate of return does not take inflation into account, while the real rate of return is the nominal rate of return less the inflation rate.

E.g.

Nominal rate of return for FD 4%

Inflation 3%

Real rate of return for FD 1% (4% - 3%)

You should learn how your money can work for you to increase over time and to beat inflation.

Your money should give you a real rate of return. This should be your money's job description and your principal financial goal.

The rate of return is the pace at which you achieve that growth, and is normally expressed as a percentage per year.

The nominal rate of return does not take inflation into account, while the real rate of return is the nominal rate of return less the inflation rate.

E.g.

Nominal rate of return for FD 4%

Inflation 3%

Real rate of return for FD 1% (4% - 3%)

You should learn how your money can work for you to increase over time and to beat inflation.

Your money should give you a real rate of return. This should be your money's job description and your principal financial goal.

A few sobering statistics. Only 6 out of 100 people achieve financial independence

It is estimated that out of every 100 people aged 25 today, in 40 years' time:

How many people of 60 and older do you know who are dependent on their family or still have to work? Scary, isn't it?

Many people do not realise that, despite their strong work ethic, their hard work alone is not enough to help them on their way to accumulating wealth and becoming financially independent.

To gain financial independence, your money must work for you. You need to be smart about money, and you need to know your money's enemies and friends.

The story of Rockefeller

As a teenager, John D. Rockefeller, one of the richest men in America in the 19th century, earned $1 hoeing potatoes for a neighbour for 30 hours. A week later, he collected interest of $3.50 on a loan he had made to another farmer a year earlier. Rockefeller learned early on that you do not necessarily need to work harder, but that you do need to work smart.

If you share Rockefeller's determination and want to end up being one of the 6 out of 100 people without financial worries when you retire, you should learn to invest early.

- only 6 will be financially independent

- 34 people will have passed away

- 10 will be drawing a government pension,

- 20 will still be working, and,

- 30 will be dependent on relatives.

How many people of 60 and older do you know who are dependent on their family or still have to work? Scary, isn't it?

Many people do not realise that, despite their strong work ethic, their hard work alone is not enough to help them on their way to accumulating wealth and becoming financially independent.

To gain financial independence, your money must work for you. You need to be smart about money, and you need to know your money's enemies and friends.

The story of Rockefeller

As a teenager, John D. Rockefeller, one of the richest men in America in the 19th century, earned $1 hoeing potatoes for a neighbour for 30 hours. A week later, he collected interest of $3.50 on a loan he had made to another farmer a year earlier. Rockefeller learned early on that you do not necessarily need to work harder, but that you do need to work smart.

If you share Rockefeller's determination and want to end up being one of the 6 out of 100 people without financial worries when you retire, you should learn to invest early.

Everyone wants to be financially independent

Acquiring investing knowledge is important. The earlier you acquire this knowledge of how your money can work for you, the better for you.

In order to gain financial independence you need to understand first and foremost that hard work is important, but not enough. You should also be clever about making the money you earn work hard for you.

You also need to know yourself before you make any investment decisions. Your objectives and the time you have in which to achieve them are the 2 most important factors when deciding on an investment programme.

Unfortunately, very few investors realise this when they start. You will need to find out how much risk you can tolerate, as well as what your relationship with money is.

Investment options are increasing dramatically in number and sophistication. Many people stumble along, buying a share here and a unit trust there. Only when they start learning about investments do they realise that they have made a mess of things. You have to make the most of this sophistication by adhering to simple principles and basic truths when compiling your investment portfolio.

The road may sometimes be bumpy, and at times you may wonder whether it would not have been more prudent to keep your hard-earned money under your mattress. But you will see that patience will be rewarded, and the ability to achieve long-term objectives depends on a long-term plan.

In order to gain financial independence you need to understand first and foremost that hard work is important, but not enough. You should also be clever about making the money you earn work hard for you.

You also need to know yourself before you make any investment decisions. Your objectives and the time you have in which to achieve them are the 2 most important factors when deciding on an investment programme.

Unfortunately, very few investors realise this when they start. You will need to find out how much risk you can tolerate, as well as what your relationship with money is.

Investment options are increasing dramatically in number and sophistication. Many people stumble along, buying a share here and a unit trust there. Only when they start learning about investments do they realise that they have made a mess of things. You have to make the most of this sophistication by adhering to simple principles and basic truths when compiling your investment portfolio.

The road may sometimes be bumpy, and at times you may wonder whether it would not have been more prudent to keep your hard-earned money under your mattress. But you will see that patience will be rewarded, and the ability to achieve long-term objectives depends on a long-term plan.

Very good advice for the younger investors contemplating stock investing

When is a good time (age) to invest in the stock market?

3:02 am on January 28, 2010

Hi, I am 20 years old and am looking to start investing into the stock market. I have been told that I am too young to invest and that I will end up broke. I am going to be an accountant, so I know how to handle my money. Also, I was curious if there is a minimum to invest at a time or if I can invest a small amount now and invest more once I have established myself? And finally am I too young to invest?

Donald F 3:02 am on January 28, 2010 Permalink

I am glad that you are asking this question at your age. Like in everything else in life, there’s nothing like starting early. You are studying to be an accountant, so you already know the power of Compounding, and what it can do. Consider this excellent article about the benefits of starting early and what Compounding can do for you, when you start early.

Power of Compounding

http://www.valueresearchonline.com/story/h2_storyView.asp?str=4007

Next, I would recommend you to first get solid grounding in Investing. 3 must read books. If you haven’t heard of these, buy them NOW, today. They will be your invaluable guides to safe & prosperous investing and future wealth creation.

1. Intelligent Investor -Benjamin Graham

Considered the bible of all investors, this will foremost teach you the basics and most importantly, how not to lose money. Thats the first lesson you need, believe me

2. One up on Wall Street -Peter Lynch

This is another classic. Tells you how to spot winners from what you see around you. successful products, companies. Practically shows you how you do not need to be a hot shot financial analyst to be able to spot good moneymaking opportunities in stocks

3. Common stocks Uncommon Profits- Phil Fisher

As you dabble for 1 or 2 years, make some money and also make some small (hopefully) mistakes, you will start itching to catch the multi-baggers, the ones that go up 4x-10x in a couple of years! This book show you how to sift out probable winners

As you start reading the books, start an online trading account like someone mentioned e-Trade, use the principles in the first book to buy a few good stock at a reasonable price. Start listening in on the financial channels, start reading a business daily, daily. Check out great investing basics websites like

http://beginnersinvest.about.com/

http://www.investopedia.com/articles/basics/

http://www.kiplinger.com/moneybasics/

And ask questions to the more experienced investors at popular forums, hang in lurk at some of the great investing forums for pearls of wisdom and when you have a query that you have to have answered post a quick one. Consider Chucks Angels -a nice yahoogroup for wannabe investors too http://finance.groups.yahoo.com/group/chucks_angels/

Good Luck. You are not too early by any standards. I would say just about right time. Get cracking, boy!

Eka A 3:02 am on January 28, 2010 Permalink

When the stock market have got into bullish.But it up to the economics,although perhaps economics slow down but you can get profit in bearish.it up to your skill.I will show you and example that present you about the US recession can’t effect to everyone,thus you can make progit on this situation. here this link

http://finance-fantasy.blogspot.com/2008/05/us-financial-crisis-has-not-had-bad.html

cashing 3:02 am on January 28, 2010 Permalink

Try <— http://earn-cash-today.com/stock

Good luck!

ha ha ha thats funny im 16 and i invest in stock options

Liz A 3:02 am on January 28, 2010 Permalink

You can invest at any point in your life and start with small amounts if you like. There are alot of different investment options out there so study up on it first and see what fits for you. If you go with stocks, remember the old saying "buy low – sell high"

To start, go to you local bank and talk to an advisor. They can give you some good option advise for free, that’s their job. Of course they would like you to invest through them, but you don’t have too.

andy 3:02 am on January 28, 2010 Permalink

When I was in the Navy, there were people your age investing in the stock market and making money. If you have spare money and can handle the risks go for it. I would start with an online stock trader such as e-trade to get your feet wet. It usually takes a few hundred dollars to get started. Good luck and happy investing.

Ray 3:02 am on January 28, 2010 Permalink

Anytime is good to invest. Your age is NOT a factor if you understand the marketplace and it’s ramifications.

There is no minimum – but you need to understand you pay commission per trade and buy the stock at it’s current market price.

And hope the price goes up. Then you sell it for profit.

However, there are also stock options you can trade as a tool to hedge your investments.

You should also look at futures trading as a tool for investment and hedging.

In the futures market (also called "commodities"), you can buy OR sell without ownership. You are "betting" or speculating the price of gold, or crude, or sugar, or wheat will go up OR go down. Much riskier than stocks, but you can make a lot of money in a short period. (you can also loose it just as fast!)

You can use a broker who will offer advise or trade yourself online- like schwab online.

However, it is the your responsibility to do the research.

What type of stock and the companies you invest in will determine your chances of success.

Dump it all on one stock or smaller amounts in a few different stocks? These are some things you will have to decide.

Also- DO NOT listen to people who give you TIPS. Chances are, by the time you hear the "hot tip", it’s too late. Someone else has already cashed in.

Watch the movie Boiler Room. IT will teach you a good lesson- how you can get scammed by what appear to be legitimate brokers.

DO YOUR HOMEWORK FIRST before you give anyone a cent.

Good Luck-

Sheri Dev 3:02 am on January 28, 2010 Permalink

Ziggy,

Investing in direct equity market without proper knowledge is risky. Till achieving the required knowledge, you can select mutual fund path by applying SIP (systematic Investment Plan) with best available funds today. that is recommended.

Still, you want to know about the time buy stocks, please read further.

There are two types of activities with share and stock. 1. Stock trading 2. Stock Investing.

Stock traders commonly buying stocks today and selling immediately the same day or next day to get small profits. This is dangerous for someone doesn’t have proper knowledge. The method most of the traders using to analyze a stock called Technical Analysis using trend and historical performance charts. It is a kind of speculation that can give you money or cost you money.

Stock Investing also same but, investors throughly analysis companies using various fundamental analysis tools and once they found a good one, the will invest on that. compare with the above, stock investing have long term investment perspective of 5 to 15 years. This will give them proper profits time to time from there in vestment.

Now about the time to invest:

There is a basic approach seeing that, buy stocks in low and sell at high. This is OK but you have to watch a lot and have skills to identify the stock moves.

The best time is to buy stocks is "Any Time" you want. But if you buy stocks at any time, you have to follow some criteria.

Best wishes and go ahead.

Here’s my stock answer to investing rookies. Two suggestions:

1. Get professional advice from a fee only financial planner. Someone who sells advice – NOT products on commission like a stockbroker does. Fee Only Planners have no reason to give you anything but their best advice, since they want you to be happy and refer friends. And their compensation isn’t tied to what you invest in, eliminating conflicts of interest as much as possible. I think this makes sense in the same way it makes sense to hire a mechanic to fix your car – you just don’t want to spend the time and effort to figure it out for yourself. This is the most expedient method, but is more expensive out of pocket, than DIY, much like a mechanic. It still should be much cheaper than a stockbroker’s loads, fees and commissions however.

Full disclosure, I am such an advisor.

-or-

brckr1 3:02 am on January 28, 2010 Permalink

best time was about 2 months ago, or when the market was low. your not too young to invest, just talk with a brokerage firm or your bank…do alot of research first…..then wait….you may not make money fast but if you invest in good companies and look to the future………look at alternative energy stock, wind, solar, fuel cells, companies thet reclaim waste and those that turn waste emissions into energy…GRGR.PK on the NYSE….TMG.V,APV.TO and SBX.V all on the TSX………read what T. Boone Pickens has announced………

http://investing.hirby.com/when-is-a-good-time-to-invest-in-the-stock-market/

3:02 am on January 28, 2010

Hi, I am 20 years old and am looking to start investing into the stock market. I have been told that I am too young to invest and that I will end up broke. I am going to be an accountant, so I know how to handle my money. Also, I was curious if there is a minimum to invest at a time or if I can invest a small amount now and invest more once I have established myself? And finally am I too young to invest?

Donald F 3:02 am on January 28, 2010 Permalink

I am glad that you are asking this question at your age. Like in everything else in life, there’s nothing like starting early. You are studying to be an accountant, so you already know the power of Compounding, and what it can do. Consider this excellent article about the benefits of starting early and what Compounding can do for you, when you start early.

Power of Compounding

http://www.valueresearchonline.com/story/h2_storyView.asp?str=4007

Next, I would recommend you to first get solid grounding in Investing. 3 must read books. If you haven’t heard of these, buy them NOW, today. They will be your invaluable guides to safe & prosperous investing and future wealth creation.

1. Intelligent Investor -Benjamin Graham

Considered the bible of all investors, this will foremost teach you the basics and most importantly, how not to lose money. Thats the first lesson you need, believe me

2. One up on Wall Street -Peter Lynch

This is another classic. Tells you how to spot winners from what you see around you. successful products, companies. Practically shows you how you do not need to be a hot shot financial analyst to be able to spot good moneymaking opportunities in stocks

3. Common stocks Uncommon Profits- Phil Fisher

As you dabble for 1 or 2 years, make some money and also make some small (hopefully) mistakes, you will start itching to catch the multi-baggers, the ones that go up 4x-10x in a couple of years! This book show you how to sift out probable winners

As you start reading the books, start an online trading account like someone mentioned e-Trade, use the principles in the first book to buy a few good stock at a reasonable price. Start listening in on the financial channels, start reading a business daily, daily. Check out great investing basics websites like

http://beginnersinvest.about.com/

http://www.investopedia.com/articles/basics/

http://www.kiplinger.com/moneybasics/

And ask questions to the more experienced investors at popular forums, hang in lurk at some of the great investing forums for pearls of wisdom and when you have a query that you have to have answered post a quick one. Consider Chucks Angels -a nice yahoogroup for wannabe investors too http://finance.groups.yahoo.com/group/chucks_angels/

Good Luck. You are not too early by any standards. I would say just about right time. Get cracking, boy!

Eka A 3:02 am on January 28, 2010 Permalink

When the stock market have got into bullish.But it up to the economics,although perhaps economics slow down but you can get profit in bearish.it up to your skill.I will show you and example that present you about the US recession can’t effect to everyone,thus you can make progit on this situation. here this link

http://finance-fantasy.blogspot.com/2008/05/us-financial-crisis-has-not-had-bad.html

cashing 3:02 am on January 28, 2010 Permalink

Try <— http://earn-cash-today.com/stock

Good luck!

jjunit 3:02 am on January 28, 2010 Permalink

"I have been told that I am too young to invest and that I will end up broke."ha ha ha thats funny im 16 and i invest in stock options

Liz A 3:02 am on January 28, 2010 Permalink

You can invest at any point in your life and start with small amounts if you like. There are alot of different investment options out there so study up on it first and see what fits for you. If you go with stocks, remember the old saying "buy low – sell high"

To start, go to you local bank and talk to an advisor. They can give you some good option advise for free, that’s their job. Of course they would like you to invest through them, but you don’t have too.

andy 3:02 am on January 28, 2010 Permalink

When I was in the Navy, there were people your age investing in the stock market and making money. If you have spare money and can handle the risks go for it. I would start with an online stock trader such as e-trade to get your feet wet. It usually takes a few hundred dollars to get started. Good luck and happy investing.

Ray 3:02 am on January 28, 2010 Permalink

Anytime is good to invest. Your age is NOT a factor if you understand the marketplace and it’s ramifications.

There is no minimum – but you need to understand you pay commission per trade and buy the stock at it’s current market price.

And hope the price goes up. Then you sell it for profit.

However, there are also stock options you can trade as a tool to hedge your investments.

You should also look at futures trading as a tool for investment and hedging.

In the futures market (also called "commodities"), you can buy OR sell without ownership. You are "betting" or speculating the price of gold, or crude, or sugar, or wheat will go up OR go down. Much riskier than stocks, but you can make a lot of money in a short period. (you can also loose it just as fast!)

You can use a broker who will offer advise or trade yourself online- like schwab online.

However, it is the your responsibility to do the research.

What type of stock and the companies you invest in will determine your chances of success.

Dump it all on one stock or smaller amounts in a few different stocks? These are some things you will have to decide.

Also- DO NOT listen to people who give you TIPS. Chances are, by the time you hear the "hot tip", it’s too late. Someone else has already cashed in.

Watch the movie Boiler Room. IT will teach you a good lesson- how you can get scammed by what appear to be legitimate brokers.

DO YOUR HOMEWORK FIRST before you give anyone a cent.

Good Luck-

Sheri Dev 3:02 am on January 28, 2010 Permalink

Ziggy,

Investing in direct equity market without proper knowledge is risky. Till achieving the required knowledge, you can select mutual fund path by applying SIP (systematic Investment Plan) with best available funds today. that is recommended.

Still, you want to know about the time buy stocks, please read further.

There are two types of activities with share and stock. 1. Stock trading 2. Stock Investing.

Stock traders commonly buying stocks today and selling immediately the same day or next day to get small profits. This is dangerous for someone doesn’t have proper knowledge. The method most of the traders using to analyze a stock called Technical Analysis using trend and historical performance charts. It is a kind of speculation that can give you money or cost you money.

Stock Investing also same but, investors throughly analysis companies using various fundamental analysis tools and once they found a good one, the will invest on that. compare with the above, stock investing have long term investment perspective of 5 to 15 years. This will give them proper profits time to time from there in vestment.

Now about the time to invest:

There is a basic approach seeing that, buy stocks in low and sell at high. This is OK but you have to watch a lot and have skills to identify the stock moves.

The best time is to buy stocks is "Any Time" you want. But if you buy stocks at any time, you have to follow some criteria.

- First, you should have a long term investment perspective of 5 to 10 years.

- Second, you should study and analysis companies to know whether the stock of this company is suitable to invest or not. to analyze a company, great investors like Benajamin graham and warren buffett provided some valuation methods. read the same here: http://uliponline.blogspot.com/2008/05/ten-points-ben-grahams-last-will-and.html if the company is suitable to this valuation methods and your investment horizon is long, buy the shares at any time not considering the market status and hold the shares. You will certainly get handsome profit.

Best wishes and go ahead.

gampublic 3:02 am on January 28, 2010 Permalink

Two things first: Generally, I’ve found accountants great with tax forms/laws, not so hot as investors, so beware of overconfidence. Second, you’re asking how to time the market, and history and study after study shows no one is worth a darn at it over time.

So the short answer is "A soon as possible *when* you know what you are doing". Here’s my stock answer to investing rookies. Two suggestions:

1. Get professional advice from a fee only financial planner. Someone who sells advice – NOT products on commission like a stockbroker does. Fee Only Planners have no reason to give you anything but their best advice, since they want you to be happy and refer friends. And their compensation isn’t tied to what you invest in, eliminating conflicts of interest as much as possible. I think this makes sense in the same way it makes sense to hire a mechanic to fix your car – you just don’t want to spend the time and effort to figure it out for yourself. This is the most expedient method, but is more expensive out of pocket, than DIY, much like a mechanic. It still should be much cheaper than a stockbroker’s loads, fees and commissions however.

Full disclosure, I am such an advisor.

-or-

2. Do It Yourself – Read Books – for investing, my favorite authors are Larry Swedroe, Rick Ferri, William Bernstein, and John Bogle. Basically, they skip over the “pop finance” garbage (most media) that’s simply a distraction, and get down to real professional quality investing while still being accessible to most reasonably intelligent people. You will find this has nearly nothing to do with accounting as you study it. If you don’t mind spending the time to figure it out right, and are interested in the topic, this is a perfectly good choice, and less money out of pocket.

Your Call. Good Luck.

brckr1 3:02 am on January 28, 2010 Permalink

best time was about 2 months ago, or when the market was low. your not too young to invest, just talk with a brokerage firm or your bank…do alot of research first…..then wait….you may not make money fast but if you invest in good companies and look to the future………look at alternative energy stock, wind, solar, fuel cells, companies thet reclaim waste and those that turn waste emissions into energy…GRGR.PK on the NYSE….TMG.V,APV.TO and SBX.V all on the TSX………read what T. Boone Pickens has announced………

http://investing.hirby.com/when-is-a-good-time-to-invest-in-the-stock-market/

Investing In A Bear Market

Investing In A Bear Market

We are in the 6th inning of the residential RE crisis and the 1st inning of the commercial RE crisis. Most of you are trapped in normalized bull market valuation methods (Income Statements and Cash Flow statements) which states "earnings growth and cashflow" are what you should follow. In a bear market you should be focused on the (Balance Sheets and Cash Flow Statements). Notice the switch from income statement to balance sheet. Read some of my first few blogs and you will see before the residential RE crisis started in mass I was focused only on balance sheet items (cash and debt). I was right and the worst balance sheet stocks got killed not the ones with the biggest losses.

If you actually look at how I ranked builder stocks using cash and debt and applied it to other industries you would see the same result. Why? When a bear economy is upon us credit markets tighten, loans do not get renewed, cash flow turns negative, borrowing costs go up, interest burden becomes magnified, asset prices drop, etc.....

Wall Street can't value stocks as easily when the future is uncertain and earnings go negative or are falling. Bear markets are about surviving and the companies that thrive DURING AND AFTER a bear market are the ones with the best balance sheets buying assets on the cheap. They are also the companies that have the cash to continue to invest in future product while their competitors are trying to stay alive vs. thinking and investing in future operational profit.

Be like the best companies. Stop listening to doom and gloomers, raise cash, invest in yourself, work twice as hard, stay focused and push forward doing whatever you have to in order to make money. Invest it wisely. You may not make as much today, but deflation pushed all your consumer good prices down too. Everything is on sale even at the Chicken Ranch.

http://kolkalamar.blogspot.com/2010/01/investing-in-bear-market.html

We are in the 6th inning of the residential RE crisis and the 1st inning of the commercial RE crisis. Most of you are trapped in normalized bull market valuation methods (Income Statements and Cash Flow statements) which states "earnings growth and cashflow" are what you should follow. In a bear market you should be focused on the (Balance Sheets and Cash Flow Statements). Notice the switch from income statement to balance sheet. Read some of my first few blogs and you will see before the residential RE crisis started in mass I was focused only on balance sheet items (cash and debt). I was right and the worst balance sheet stocks got killed not the ones with the biggest losses.

If you actually look at how I ranked builder stocks using cash and debt and applied it to other industries you would see the same result. Why? When a bear economy is upon us credit markets tighten, loans do not get renewed, cash flow turns negative, borrowing costs go up, interest burden becomes magnified, asset prices drop, etc.....

Wall Street can't value stocks as easily when the future is uncertain and earnings go negative or are falling. Bear markets are about surviving and the companies that thrive DURING AND AFTER a bear market are the ones with the best balance sheets buying assets on the cheap. They are also the companies that have the cash to continue to invest in future product while their competitors are trying to stay alive vs. thinking and investing in future operational profit.

Be like the best companies. Stop listening to doom and gloomers, raise cash, invest in yourself, work twice as hard, stay focused and push forward doing whatever you have to in order to make money. Invest it wisely. You may not make as much today, but deflation pushed all your consumer good prices down too. Everything is on sale even at the Chicken Ranch.

http://kolkalamar.blogspot.com/2010/01/investing-in-bear-market.html

Are You Paying Too Much For Stocks? Market Value is Not Equal to Actual Value

Are You Paying Too Much For Stocks?

Market Value Not Equal to Actual Value

A small loan can help you if you are short of cash until your next payday, but if you invest in the stock market and follow the crowd in their buying and selling habits, you may end up with many more liabilities than assets. Why? Have you noticed how much the stock market fluctuates in a day, and also the ups and downs of prices? Does that mean that the companies’ values goes up and down as much as the share price, or does that mean that there may be some other force at work here? As you can see, market value of a share doesn’t equal ACTUAL value of the same share, in terms of the value of a company.

Market Price Based on Emotions, Not Logic

One of the pioneers in value investing, Benjamin Graham, believed that many people rely too much on their emotions when investing rather than their logic. This explains the fluctuations of the market, and also why a lot of people think it’s risky to invest in it. What makes it risky is the constant buying and selling that goes on day after day, hour after hour. This constant buying and selling is what either drives the share price up or down, and it’s what creates the risk.

Ben Graham suggested in his book “The Intelligent Investor” that if you want to build your wealth from the stock market, you need to use a “dollar cost averaging” technique, meaning to consistently buy more shares at a lower price over time. As inflation and company values grow over time, your investments will be worth more in the long run. It’s also called “buy low and sell high” which you might have heard about. Unfortunately, most people tend to bring their emotions into their investing, and will panic and sell when the price is going down, because they are afraid to lose any more money on their investments, leaving them open to take out a small loan to survive.

Beyond the Smoke and Mirrors

The stock market is riddled with confusing terms, acronyms and policies, making it very difficult for the average investor to understand. All this is just smoke and mirrors designed to keep most people in the dark and dependent on high-priced brokers to navigate the investing maze for them. However, if you were to peek behind the curtain, you would see that all the confusion is just smoke and mirrors.

Inflated Price? Inflated Value!

In an effort to control the market prices, brokers and fund managers will either buy or sell enough shares to drive the price back up or down, depending on where the prices are going. Perhaps it’s due to a company that got good news or bad, and investors are trying to position themselves to not lose a lot of money, or make some. This tends to skew the value of a share price, and unbalances the market. Thus, a share price that has risen too quickly will have many shares sold off by fund managers or brokers to drive the price back down. Similarly, if a share price is dropping too fast, they’ll buy as many shares to even up. So if there are inflated prices, don’t go believing it’s actually worth that much. In fact, they may not be worth much at all!

P/E Ratio Tells it All

There is a very simple way to determine if a certain share price is on target or not—look at the Price per Earnings ratio. This is a valuation method that takes the company’s current share price on the market divided by the per-share earnings over a certain time frame, usually one year. If the price of shares in a company are $ 24 per share, and the earnings over the previous year were $ 2, the ratio of P/E is 12.

Buy Low, Sell High

When you can learn how to find the correct value of a company or share, you will know when the share price is at its lowest, and when you can buy. After share prices crest, you can sell your shares and pocket the rest without needing a small loan. If you do this, you will be able to make money on the stock market when everyone else is losing money.

http://www.401kinformationblog.com/are-you-paying-too-much-for-stocks/

Market Value Not Equal to Actual Value

A small loan can help you if you are short of cash until your next payday, but if you invest in the stock market and follow the crowd in their buying and selling habits, you may end up with many more liabilities than assets. Why? Have you noticed how much the stock market fluctuates in a day, and also the ups and downs of prices? Does that mean that the companies’ values goes up and down as much as the share price, or does that mean that there may be some other force at work here? As you can see, market value of a share doesn’t equal ACTUAL value of the same share, in terms of the value of a company.

Market Price Based on Emotions, Not Logic

One of the pioneers in value investing, Benjamin Graham, believed that many people rely too much on their emotions when investing rather than their logic. This explains the fluctuations of the market, and also why a lot of people think it’s risky to invest in it. What makes it risky is the constant buying and selling that goes on day after day, hour after hour. This constant buying and selling is what either drives the share price up or down, and it’s what creates the risk.

Ben Graham suggested in his book “The Intelligent Investor” that if you want to build your wealth from the stock market, you need to use a “dollar cost averaging” technique, meaning to consistently buy more shares at a lower price over time. As inflation and company values grow over time, your investments will be worth more in the long run. It’s also called “buy low and sell high” which you might have heard about. Unfortunately, most people tend to bring their emotions into their investing, and will panic and sell when the price is going down, because they are afraid to lose any more money on their investments, leaving them open to take out a small loan to survive.

Beyond the Smoke and Mirrors

The stock market is riddled with confusing terms, acronyms and policies, making it very difficult for the average investor to understand. All this is just smoke and mirrors designed to keep most people in the dark and dependent on high-priced brokers to navigate the investing maze for them. However, if you were to peek behind the curtain, you would see that all the confusion is just smoke and mirrors.

Inflated Price? Inflated Value!

In an effort to control the market prices, brokers and fund managers will either buy or sell enough shares to drive the price back up or down, depending on where the prices are going. Perhaps it’s due to a company that got good news or bad, and investors are trying to position themselves to not lose a lot of money, or make some. This tends to skew the value of a share price, and unbalances the market. Thus, a share price that has risen too quickly will have many shares sold off by fund managers or brokers to drive the price back down. Similarly, if a share price is dropping too fast, they’ll buy as many shares to even up. So if there are inflated prices, don’t go believing it’s actually worth that much. In fact, they may not be worth much at all!

P/E Ratio Tells it All

There is a very simple way to determine if a certain share price is on target or not—look at the Price per Earnings ratio. This is a valuation method that takes the company’s current share price on the market divided by the per-share earnings over a certain time frame, usually one year. If the price of shares in a company are $ 24 per share, and the earnings over the previous year were $ 2, the ratio of P/E is 12.

- Typically, the higher the P/E ratio is, the higher the expectations investors will have for company growth. This means that you will be able to see higher earnings within the next year with this company.

- However, the lower the ratio, the slower the growth regardless of what the market is doing.

Buy Low, Sell High

When you can learn how to find the correct value of a company or share, you will know when the share price is at its lowest, and when you can buy. After share prices crest, you can sell your shares and pocket the rest without needing a small loan. If you do this, you will be able to make money on the stock market when everyone else is losing money.

http://www.401kinformationblog.com/are-you-paying-too-much-for-stocks/

How to Value Stocks

The Stock Market

The stock market can be a great place to make money. However, the stock market can also be an incredibly frustrating place, where losing money becomes an everyday occurrence. Knowing what to buy and what to sell in the stock market can be very complicated. However, there is a method for estimating the true value of a stock that is both logical and often overlooked. Learning and implementing this method isn't easy, but once fully understood it is fairly easy to use and the results can be very rewarding

http://hubpages.com/hub/How-to-Value-Stocks

The stock market can be a great place to make money. However, the stock market can also be an incredibly frustrating place, where losing money becomes an everyday occurrence. Knowing what to buy and what to sell in the stock market can be very complicated. However, there is a method for estimating the true value of a stock that is both logical and often overlooked. Learning and implementing this method isn't easy, but once fully understood it is fairly easy to use and the results can be very rewarding

http://hubpages.com/hub/How-to-Value-Stocks

Active investing, look laterally in the same industry and trade up in quality

Value investing is never passive. Like other strategies, it is also an active process employing knowledge, skills and using various tools.

One approach to finding a cheap (value) stock starts with a bottom up approach.

Having discover and own a stock in a particular sector, one can also look laterally to analyse other firms in the same industry.

Are these also cheap, and for the same reasons?

You may decide that one of these other companies is a better investment than your initial purchase.

Perhaps, it is a higher quality company, with better profit margins or lower debt levels.

If so, you may trade up in quality, provided that you can still take advantage of the depressed status of the industry.

One approach to finding a cheap (value) stock starts with a bottom up approach.

Having discover and own a stock in a particular sector, one can also look laterally to analyse other firms in the same industry.

Are these also cheap, and for the same reasons?

You may decide that one of these other companies is a better investment than your initial purchase.

Perhaps, it is a higher quality company, with better profit margins or lower debt levels.

If so, you may trade up in quality, provided that you can still take advantage of the depressed status of the industry.

Judgement is required when selling a stock.

The decision to sell a stock requires judgement.

Judgement is required to sell a winner.

Judgement is required to sell a stock that has not recovered.

At some point, everyone throws in the towel.

Even the most tolerant investor's patience can ultimately be exhausted.

There are always other places to invest the money.

A realised loss has at least some tax benefits for some investors.

A depressed stock in the portfolio is just a reminder of a mistake.

What are the triggers?

Judgement is required to sell a winner.

Judgement is required to sell a stock that has not recovered.

At some point, everyone throws in the towel.

Even the most tolerant investor's patience can ultimately be exhausted.

There are always other places to invest the money.

A realised loss has at least some tax benefits for some investors.

A depressed stock in the portfolio is just a reminder of a mistake.

What are the triggers?

- A deterioration in the assets beyond what was initially anticipated.

- A deterioration in the earnings power beyond what was initially anticipated.

- The stock may still be cheap, but the prospects of recovery have now started to fade.

****Strategies for long term investment as markets correct

Strategies for long term investment as markets correct

By Manish Misra on January 29, 2010

The rally in the equity markets has finally taken a breather. A bout of profit-booking was seen last week and it may be early to predict whether this is the start of the much-anticipated downturn in the equity markets. So, what should be your long term strategy to invest in such a scenario?

Investors remain concerned over the pace of the global economic recovery and have turned cautious in their approach to the markets, leading to profit-booking at every rise.

Although the results season was largely positive with most companies reporting earnings in line with or exceeding market expectations, it was weak global sentiment and consistent sell-offs by foreign institutional investor (FII) in last few trading sessions acted as a catalyst for the market correction.

The current rally in the domestic markets was driven mainly by liquidity owing to heavy inflows from FIIs who found the Asian markets poised for a recovery much ahead of their Western peers. While the domestic economy did not disappoint in terms of earnings numbers in the last two quarters, the current prices had already factored in the growth, thereby not leaving much room for a further upside. The market will now look for global cues to decide on the future direction.

The Reserve Bank of India (RBI) in the monetory policy, scheduled to be announced today (29/01/2010) afternoon, is expected to hike the CRR and Reverse Repo rates.

Over the short term, the markets could display increased volatility and this in turn could throw up attractive opportunities for medium to long term investors. While the long term growth story of the domestic economy remains intact, the short term will always be marred with uncertainty. Long-term investors would do well to use this uncertainty to their advantage.

Here are some strategies investors can adopt to ensure their portfolios remain aligned towards growth:

1. Review asset allocation

Investors should stick to their asset allocation across equity, debt and money market instruments depending on their overall investment profile. Reviewing the asset allocation when the markets peak gives an indication of whether to book profits in equity. As the markets correct, an asset allocation review will help investors decide on the amount which should be shifted back to equity in order to balance the asset allocation.

2. Maintain liquidity

Falling markets often present attractive opportunities but it can be made use of only if investors have money to invest. Re-balancing asset allocation can provide some liquidity to the investor and this can be used effectively to pick up desired stocks when the markets correct.

3. Selection of stocks

Stocks, especially in the large-cap category, had a major run-up in the past few months. For investors, it was a risky proposition to enter these stocks at the levels at which they looked more than fairly-valued. A correction in the markets has brought these stocks back to prices which are attractive for medium to long term investors. Hence, investors can identify their target companies and slowly start accumulating these stocks as the markets offer opportunities.

4. Stagger purchases

While the markets have been in a correction mode for the past two weeks, it is difficult to predict whether this phase is temporary or will continue for a while. Hence, it is important to stagger the purchases over a period of time rather than buying in one go. The expected volatility in the markets may give investors many opportunities to pick stocks at desired prices.

Conclusion

Follow these time tested strategies to invest in stock market. Investors who did not get a chance to enter the markets in the last rally can now make use of the opportunity to invest in select stocks at attractive levels to build a robust long-term portfolio.

http://www.personalmoney.in/strategies-for-long-term-investment-as-markets-correct/1458

By Manish Misra on January 29, 2010

The rally in the equity markets has finally taken a breather. A bout of profit-booking was seen last week and it may be early to predict whether this is the start of the much-anticipated downturn in the equity markets. So, what should be your long term strategy to invest in such a scenario?

Investors remain concerned over the pace of the global economic recovery and have turned cautious in their approach to the markets, leading to profit-booking at every rise.

Although the results season was largely positive with most companies reporting earnings in line with or exceeding market expectations, it was weak global sentiment and consistent sell-offs by foreign institutional investor (FII) in last few trading sessions acted as a catalyst for the market correction.

The current rally in the domestic markets was driven mainly by liquidity owing to heavy inflows from FIIs who found the Asian markets poised for a recovery much ahead of their Western peers. While the domestic economy did not disappoint in terms of earnings numbers in the last two quarters, the current prices had already factored in the growth, thereby not leaving much room for a further upside. The market will now look for global cues to decide on the future direction.

The Reserve Bank of India (RBI) in the monetory policy, scheduled to be announced today (29/01/2010) afternoon, is expected to hike the CRR and Reverse Repo rates.

Over the short term, the markets could display increased volatility and this in turn could throw up attractive opportunities for medium to long term investors. While the long term growth story of the domestic economy remains intact, the short term will always be marred with uncertainty. Long-term investors would do well to use this uncertainty to their advantage.

Here are some strategies investors can adopt to ensure their portfolios remain aligned towards growth:

1. Review asset allocation

Investors should stick to their asset allocation across equity, debt and money market instruments depending on their overall investment profile. Reviewing the asset allocation when the markets peak gives an indication of whether to book profits in equity. As the markets correct, an asset allocation review will help investors decide on the amount which should be shifted back to equity in order to balance the asset allocation.

2. Maintain liquidity

Falling markets often present attractive opportunities but it can be made use of only if investors have money to invest. Re-balancing asset allocation can provide some liquidity to the investor and this can be used effectively to pick up desired stocks when the markets correct.

3. Selection of stocks

Stocks, especially in the large-cap category, had a major run-up in the past few months. For investors, it was a risky proposition to enter these stocks at the levels at which they looked more than fairly-valued. A correction in the markets has brought these stocks back to prices which are attractive for medium to long term investors. Hence, investors can identify their target companies and slowly start accumulating these stocks as the markets offer opportunities.

4. Stagger purchases

While the markets have been in a correction mode for the past two weeks, it is difficult to predict whether this phase is temporary or will continue for a while. Hence, it is important to stagger the purchases over a period of time rather than buying in one go. The expected volatility in the markets may give investors many opportunities to pick stocks at desired prices.

Conclusion

Follow these time tested strategies to invest in stock market. Investors who did not get a chance to enter the markets in the last rally can now make use of the opportunity to invest in select stocks at attractive levels to build a robust long-term portfolio.

http://www.personalmoney.in/strategies-for-long-term-investment-as-markets-correct/1458

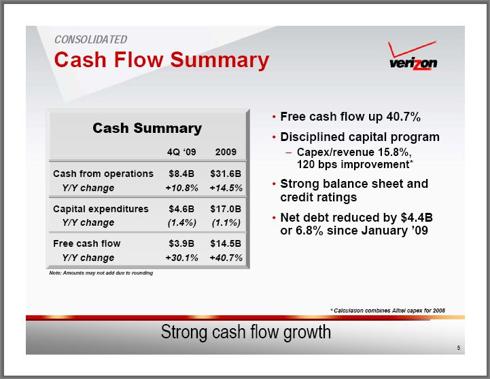

What management does with cash flow is key to long term performance.

Cash Deployment – After playing the stock-picking game for a while I notice that what management does with cash flow is key to long term performance. Sometimes they can't think of anything better to do than to load up with debt and then go on to spend the proceeds buying back shares at inflated prices. Of course when trouble hits it becomes necessary to raise capital by selling shares at fire sale prices. Readers who have avoided these types of problem during the downturn have done better than I and deserve to be congratulated.

Mr. Market does not like capex. It's a real turnoff, peeing away money that could support a nice special dividend or be used to pump up share prices. Actually risking it in an effort to make money from expanded or more efficient operations is less attractive than the alternatives, in terms of immediate price action.

http://seekingalpha.com/article/184987-why-i-m-staying-with-verizon

Mr. Market does not like capex. It's a real turnoff, peeing away money that could support a nice special dividend or be used to pump up share prices. Actually risking it in an effort to make money from expanded or more efficient operations is less attractive than the alternatives, in terms of immediate price action.

http://seekingalpha.com/article/184987-why-i-m-staying-with-verizon

Why I usually avoid IPOs

I browsed the local paper for those stocks priced closest to the year low. There were 35 stocks listed: 29 derivatives (warrant) and 6 non-derivatives (mother share). Stemlife was in this list.

====19/01/2010 Notice of Person Ceasing (29C) - The Goldman Sachs Group, Inc.

====19/01/2010 Changes in Sub. S-hldr's Int. (29B) - The Goldman Sachs International

Disposed 12/01/2010 5,706,000

====19/01/2010 Changes in Sub. S-hldr's Int. (29B) - The Goldman Sachs Group, Inc.

====18/01/2010 Changes in Sub. S-hldr's Int. (29B) - BERJAYA GROUP BERHAD

Disposed 14/01/2010 4,050,000

====18/01/2010 Changes in Sub. S-hldr's Int. (29B) - BERJAYA CORPORATION BERHAD

====18/01/2010 Changes in Sub. S-hldr's Int. (29B) - JUARA SEJATI SDN BHD

====18/01/2010 Changes in Sub. S-hldr's Int. (29B) - TAN SRI DATO' SERI VINCENT TAN CHEE YIOUN

====18/01/2010 Changes in Sub. S-hldr's Int. (29B) - HOTEL RESORT ENTERPRISE SDN BHD

====13/01/2010 Notice of Person Ceasing (29C) - HSC HEALTHCARE SDN BHD

====13/01/2010 Changes in Sub. S-hldr's Int. (29B) - HSC HEALTHCARE SDN BHD

Disposed 11/01/2010 10,000,000

Fundamentals

This company was listed with much hype in 2006. Its revenue grew quickly in this virgin medical sector. Those uninformed customers and investors saw "unlimited" potentials from this new medical technology. The business model was not one with durable competitiveness. With new competitors in the market, I can foresee this company's business will be challenging.

Listing in 2006 was the right timing as the stock was chased up to a high level during the bull market then. At the peak market price of more than MR 6 in 2007, its market cap was almost MR 900 million. It was not surprising that a significant large investor (insider) sold when the price was close to its peak; making a huge profit from the shares, locking in many years of future profits that the company can hope to generate through its business.

At 45 sen per share, its present market cap is MR 74.3 million. What is its intrinsic value? Interestingly, more major investors sold and exited the company recently.

This is a good company to study as it provides a lot of education on how to select the stocks you wish to invest into. In general, it is better to avoid IPOs. IPOs are never priced cheap. You can always let them build their business for a few years. Given the track record you can then assess the business fundamentals with more certainties, before you invest.

Some simple rules I follow:

A good company can be a good investment at fair price or bargain price.

A good company may be a bad investment if you overpay.

Avoid a lousy company at any price.

Insiders selling in huge volumes this January, desperate to unload

.

STEMLIFE BERHAD (ACE Market)

====19/01/2010 Notice of Person Ceasing (29C) - The Goldman Sachs International ====19/01/2010 Notice of Person Ceasing (29C) - The Goldman Sachs Group, Inc.

====19/01/2010 Changes in Sub. S-hldr's Int. (29B) - The Goldman Sachs International

Disposed 12/01/2010 5,706,000

====19/01/2010 Changes in Sub. S-hldr's Int. (29B) - The Goldman Sachs Group, Inc.

====18/01/2010 Changes in Sub. S-hldr's Int. (29B) - BERJAYA GROUP BERHAD

Disposed 14/01/2010 4,050,000

====18/01/2010 Changes in Sub. S-hldr's Int. (29B) - BERJAYA CORPORATION BERHAD

====18/01/2010 Changes in Sub. S-hldr's Int. (29B) - JUARA SEJATI SDN BHD

====18/01/2010 Changes in Sub. S-hldr's Int. (29B) - TAN SRI DATO' SERI VINCENT TAN CHEE YIOUN

====18/01/2010 Changes in Sub. S-hldr's Int. (29B) - HOTEL RESORT ENTERPRISE SDN BHD

====13/01/2010 Notice of Person Ceasing (29C) - HSC HEALTHCARE SDN BHD

====13/01/2010 Changes in Sub. S-hldr's Int. (29B) - HSC HEALTHCARE SDN BHD

Disposed 11/01/2010 10,000,000

Fundamentals

| INCOME STATEMENT 12/31/2006 2/31/2007 12/31/2008 | |||

| Net Turnover/Net Sales | 14,578 | 20,456 | 18,509 |

| EBITDA | 4,634 | 6,021 | 195 |

| EBIT | 3,719 | 5,112 | 327 |

| Net Profit | 3,772 | 5,515 | 1,317 |

| Ordinary Dividend | -1,650 | -1,650 | -1,650 |

Recent Financial Results

| Announcement Date | Financial Yr. End | Qtr | Period End | Revenue RM '000 | Profit/Lost RM'000 | EPS | Amended | ||||||

| 04-Mar-10 | 31-Dec-09 | 4 | 31-Dec-09 | 4,971 | -2,610 | -1.55 | - | ||||||

| 24-Feb-10 | 31-Dec-09 | 4 | 31-Dec-09 | 4,971 | -2,241 | -1.33 | - | ||||||

| 26-Nov-09 | 31-Dec-09 | 3 | 30-Sep-09 | 4,331 | 410 | 0.27 | - | ||||||

| 20-Aug-09 | 31-Dec-09 | 2 | 30-Jun-09 | 3,691 | 65 | 0.09 | - | ||||||

World Markets sentiments as reported in our local newspaper on 28.1.2010

HK stocks at 4-mth closing low, China at 3-mth low

Autralia shares drop 1.6%

Nikkei hits 5-wk closing low

Seoul at lowest close in 7-wks

Taiwan stocks down for 8th day

Vietnam stocks down 2.3%

Singapore stocks down 1.2%

Indonesia down for 5th day

Thai stocks down for 7th day

Indian shares drop for 6th day

FTSE 100 advances

US falls on concern Fed will withdraw more stimulus

Autralia shares drop 1.6%

Nikkei hits 5-wk closing low

Seoul at lowest close in 7-wks

Taiwan stocks down for 8th day

Vietnam stocks down 2.3%

Singapore stocks down 1.2%

Indonesia down for 5th day

Thai stocks down for 7th day

Indian shares drop for 6th day

FTSE 100 advances

US falls on concern Fed will withdraw more stimulus

Thursday, 28 January 2010

HDBSVR: Buy Parkson on share price weakness

HDBSVR: Buy Parkson on share price weakness

Tags: Hwang DBS Vickers Research | Parkson Holdings | Parkson Retail Group

Written by Hwang DBS Vickers Research

Thursday, 28 January 2010 09:17

KUALA LUMPUR: Hwang DBS Vickers Research says PARKSON HOLDINGS BHD []’s share price weakness is a buying opportunity. Its share price has fallen from its recent high of RM6.20 to RM5.51 currently.

“Maintain Buy and RM6.30 TP (RNAV -derived),” it said on Thursday, Jan 28.

Its said the sell-down – which might be due to China’s credit tightening initiatives – is excessive as there is still strong growth potential in China’s huge retail sector.

The December 2009 monthly data showed a 17.5% jump y-o-y (vs Nov 2009’s 15.8%) in retail sales.

Hwang DBS Vickers Research said an added positive is Parkson’s strong balance sheet (RM226 million net cash at end-September 2009) and healthy free cash flow (RM370 million in FY11F).

Foreign interest is returning with 25.4% foreign shareholding in Nov 2009 (versus a low of 20% in early 2009).

“Separately, the discount of Parkson’s market cap to its share of HK-listed Parkson Retail Group’s market cap has narrowed to 30% from a one-year high of 40.5%, but is still above its historical average of 25%. This suggests Parkson may continue to outperform Parkson Retail Group,” it said.

Tags: Hwang DBS Vickers Research | Parkson Holdings | Parkson Retail Group

Written by Hwang DBS Vickers Research

Thursday, 28 January 2010 09:17

KUALA LUMPUR: Hwang DBS Vickers Research says PARKSON HOLDINGS BHD []’s share price weakness is a buying opportunity. Its share price has fallen from its recent high of RM6.20 to RM5.51 currently.

“Maintain Buy and RM6.30 TP (RNAV -derived),” it said on Thursday, Jan 28.

Its said the sell-down – which might be due to China’s credit tightening initiatives – is excessive as there is still strong growth potential in China’s huge retail sector.

The December 2009 monthly data showed a 17.5% jump y-o-y (vs Nov 2009’s 15.8%) in retail sales.

Hwang DBS Vickers Research said an added positive is Parkson’s strong balance sheet (RM226 million net cash at end-September 2009) and healthy free cash flow (RM370 million in FY11F).

Foreign interest is returning with 25.4% foreign shareholding in Nov 2009 (versus a low of 20% in early 2009).

“Separately, the discount of Parkson’s market cap to its share of HK-listed Parkson Retail Group’s market cap has narrowed to 30% from a one-year high of 40.5%, but is still above its historical average of 25%. This suggests Parkson may continue to outperform Parkson Retail Group,” it said.

Maybank IB: Market should be 'fundamentals bullish' this year

Maybank IB: Market should be 'fundamentals bullish' this year

Tags: Maybank Investment Bank | Mohammed Rashdan Mohd Yusof

Written by Loong Tse Min

Thursday, 28 January 2010 16:37

KUALA LUMPUR: Maybank Investment Bank is positive on the outlook for the Malaysian equity market, which is underpinned by improving fundamentals including earnings growth and the FBM KLCI should be at about 1,400 by year-end.

Maybank IB chief executive officer Mohammed Rashdan Mohd Yusof said “we are fundamentals bullish".

"There is now clearly a earnings momentum, growth for quite a lot of our corporate sector and that in turn will reflect in a re-rating of the PEs (price-to-earnings) for the broader market area,” he told reporters on Thursday, Jan 28 at the pre-event for this year’s Invest Malaysia scheduled for March 30-31.

Mohammed Rashdan said Maybank IB’s house view was the FBM KLCI level to be about 1,400 at the year-end. The estimate is based on earnings momentum and a re-rating of the market on a broad level slightly higher to trade at about 16 times to 17 times PE.

As for the regional market selldown due led by the China government’s tightening liquidity to cool down its overheating economy, he said, “I also believe that Malaysia has shown its resilience in its fiscal and monetary policy management being shown that we were different in the previous round of tightening in 2007 when everybody else was increasing interest rates, we were not.

“We were proven right when there was a crash. Everybody else had interest rate volatility, we did not have interest rate volatility," he said.

Underscoring corporate earnings growth momentum in Malaysia this year, he said, was “a great deal of” domestic investment as well as foreign direct investment. “That is in essence, why we are fundamentals bullish,” he said.

The Edge

Tags: Maybank Investment Bank | Mohammed Rashdan Mohd Yusof

Written by Loong Tse Min

Thursday, 28 January 2010 16:37

KUALA LUMPUR: Maybank Investment Bank is positive on the outlook for the Malaysian equity market, which is underpinned by improving fundamentals including earnings growth and the FBM KLCI should be at about 1,400 by year-end.

Maybank IB chief executive officer Mohammed Rashdan Mohd Yusof said “we are fundamentals bullish".

"There is now clearly a earnings momentum, growth for quite a lot of our corporate sector and that in turn will reflect in a re-rating of the PEs (price-to-earnings) for the broader market area,” he told reporters on Thursday, Jan 28 at the pre-event for this year’s Invest Malaysia scheduled for March 30-31.

Mohammed Rashdan said Maybank IB’s house view was the FBM KLCI level to be about 1,400 at the year-end. The estimate is based on earnings momentum and a re-rating of the market on a broad level slightly higher to trade at about 16 times to 17 times PE.

As for the regional market selldown due led by the China government’s tightening liquidity to cool down its overheating economy, he said, “I also believe that Malaysia has shown its resilience in its fiscal and monetary policy management being shown that we were different in the previous round of tightening in 2007 when everybody else was increasing interest rates, we were not.

“We were proven right when there was a crash. Everybody else had interest rate volatility, we did not have interest rate volatility," he said.

Underscoring corporate earnings growth momentum in Malaysia this year, he said, was “a great deal of” domestic investment as well as foreign direct investment. “That is in essence, why we are fundamentals bullish,” he said.

The Edge

AmResearch: Cyclical bull rally has not prematurely ended

AmResearch: Cyclical bull rally has not prematurely ended

Tags: AmResearch | corporate earnings | cyclical bull rally

Written by AmResearch

Thursday, 28 January 2010 14:30

KUALA LUMPUR: AmResearch Sdn Bhd believes there is more upside for the local stock market and from a fundamental standpoint; it does not think the cyclical bull rally in the market has prematurely ended.

It said on Thursday, Jan 28 that for Malaysia, it expects gross domestic product to rebound by 5.7% in the first quarter 2010 (1Q10) and rise by a further 4.7% in 2Q10 before moderating to below 3% in the last two quarters of this year - as the low base effect tapers off.

“Historically, market performance has been strongest when GDP accelerates, underpinning a macro backdrop for corporate earnings - to expand at an even faster pace than our current estimate of 25% for 2010 (2009: -2%),” it said.

AmResearch retains its fair value of 1,450 for the FBM KLCI, based on 2010’s PE of 16.5 times or one standard deviation above its mean of 14.5 times.

Market should trade above its long-term average because corporate earnings growth of 25% set to rise this year is already more than three times the historical average growth rate of just 7% per annum.

“This market correction, therefore, presents an opportunity to accumulate quality stocks,” it said, adding several “high-beta” stocks on its Buy list that have been sold down in recent days are CIMB, IJM Land, Tenaga Nasional, Ann Joo Resources, AirAsia, Unisem, MPI and Genting Group.

To recap, it said that in recent days, the market rally has been somewhat destabilised by policy tightening surprises in China where it again moved in to curb banks from lending.

The FBM KLCI retraced 43 points (down 3%) on Wednesday from its recent peak of 1,308 on Jan 21 with risk aversion resurfacing.

It said the issue was whether this correction signaled the beginning of a valuation de-rating or a transitory mid-cycle pullback due to profit taking after a strong start since early this year.

AmResearch said it appears unlikely that China’s policy tightening will undermine its economic growth (4Q GDP: 10.7%) and by extension, de-rail the global economic recovery already gathering pace. Its baseline view is that the macro momentum remains robust.

“We continue to believe that the cyclical economic upswing will be most significant in 1H 2010, given a depressed base last year,” it said.

For Malaysia, its analysis of previous earnings-driven rally from trough to peak - in 1998/1999 and 2001/2002 - also indicates that an uptrend has never been shorter than 12 months.

The rallies in 1998/1999 and 2001/2002 sustained for 16 months and 12 months; respectively. Corporate earnings rebounded by a strong 36% in 1999 after contracting 20% in 1998. In 2002, corporate earnings accelerated by 24%, from just 3% in 2001.

“We are only just 10 months from lows seen in March 2009, and corporate earnings are still expanding with upside bias. To be sure, the previous earnings-driven rally from trough to peak - in 1998/1999a and 2001/2002 - was also punctuated by three mid-cycle corrections. Pullback was transitory, stretching no longer than two months. Dips were 15% to 22% off intermittent highs,” it said.

AmResearch said a 15% pullback from the market’s recent high of 1,308 means that it might form a base at 1,112 (or a 2010’s price-to-earnings of 12.8 times), implying a potential downside risk of 12% from the current 1,265.

However, the flipside is that the market will correct to 1,112, if it materialises. This would imply that an earnings-driven rebound to our fair value of 1,450 would also produce an attractive potential return of 30%, outweighing a downside risk of 12%.

“Thus, even though trading conditions might remain volatile at least until concern of policy risk dissipates, the upside potential is greater than downside risk,” it said.

It remained committed to its view that profit drivers - particularly for cyclicals - auto, banks, CONSTRUCTION [], property, transport and TECHNOLOGY [] and media are solidifying as end-demand and margin recovery kick-in to accentuate an earnings rebound.

Tags: AmResearch | corporate earnings | cyclical bull rally

Written by AmResearch

Thursday, 28 January 2010 14:30

KUALA LUMPUR: AmResearch Sdn Bhd believes there is more upside for the local stock market and from a fundamental standpoint; it does not think the cyclical bull rally in the market has prematurely ended.

It said on Thursday, Jan 28 that for Malaysia, it expects gross domestic product to rebound by 5.7% in the first quarter 2010 (1Q10) and rise by a further 4.7% in 2Q10 before moderating to below 3% in the last two quarters of this year - as the low base effect tapers off.

“Historically, market performance has been strongest when GDP accelerates, underpinning a macro backdrop for corporate earnings - to expand at an even faster pace than our current estimate of 25% for 2010 (2009: -2%),” it said.

AmResearch retains its fair value of 1,450 for the FBM KLCI, based on 2010’s PE of 16.5 times or one standard deviation above its mean of 14.5 times.

Market should trade above its long-term average because corporate earnings growth of 25% set to rise this year is already more than three times the historical average growth rate of just 7% per annum.

“This market correction, therefore, presents an opportunity to accumulate quality stocks,” it said, adding several “high-beta” stocks on its Buy list that have been sold down in recent days are CIMB, IJM Land, Tenaga Nasional, Ann Joo Resources, AirAsia, Unisem, MPI and Genting Group.

To recap, it said that in recent days, the market rally has been somewhat destabilised by policy tightening surprises in China where it again moved in to curb banks from lending.

The FBM KLCI retraced 43 points (down 3%) on Wednesday from its recent peak of 1,308 on Jan 21 with risk aversion resurfacing.

It said the issue was whether this correction signaled the beginning of a valuation de-rating or a transitory mid-cycle pullback due to profit taking after a strong start since early this year.

AmResearch said it appears unlikely that China’s policy tightening will undermine its economic growth (4Q GDP: 10.7%) and by extension, de-rail the global economic recovery already gathering pace. Its baseline view is that the macro momentum remains robust.

“We continue to believe that the cyclical economic upswing will be most significant in 1H 2010, given a depressed base last year,” it said.

For Malaysia, its analysis of previous earnings-driven rally from trough to peak - in 1998/1999 and 2001/2002 - also indicates that an uptrend has never been shorter than 12 months.

The rallies in 1998/1999 and 2001/2002 sustained for 16 months and 12 months; respectively. Corporate earnings rebounded by a strong 36% in 1999 after contracting 20% in 1998. In 2002, corporate earnings accelerated by 24%, from just 3% in 2001.

“We are only just 10 months from lows seen in March 2009, and corporate earnings are still expanding with upside bias. To be sure, the previous earnings-driven rally from trough to peak - in 1998/1999a and 2001/2002 - was also punctuated by three mid-cycle corrections. Pullback was transitory, stretching no longer than two months. Dips were 15% to 22% off intermittent highs,” it said.

AmResearch said a 15% pullback from the market’s recent high of 1,308 means that it might form a base at 1,112 (or a 2010’s price-to-earnings of 12.8 times), implying a potential downside risk of 12% from the current 1,265.

However, the flipside is that the market will correct to 1,112, if it materialises. This would imply that an earnings-driven rebound to our fair value of 1,450 would also produce an attractive potential return of 30%, outweighing a downside risk of 12%.

“Thus, even though trading conditions might remain volatile at least until concern of policy risk dissipates, the upside potential is greater than downside risk,” it said.

It remained committed to its view that profit drivers - particularly for cyclicals - auto, banks, CONSTRUCTION [], property, transport and TECHNOLOGY [] and media are solidifying as end-demand and margin recovery kick-in to accentuate an earnings rebound.

Hartalega 3Q net profit up 67% to RM37m

Hartalega 3Q net profit up 67% to RM37m

Written by Joseph Chin

Thursday, 28 January 2010 18:44

KUALA LUMPUR: HARTALEGA HOLDINGS BHD []'s earnings rose 67% to RM37.2 million in the third quarter ended Dec 31, 2009 from RM22.23 million a year ago, boosted by higher demand for its gloves.

It said on Thursday, Jan 28 that revenue rose 24.8% to RM148.59 million from RM119.05 million. Earnings per share were 15.35 sen compared with 9.17 sen. It declared five sen dividend per share.

"The significant achievement in revenue and profit before tax is in line with the group's continuous expansion in production capacity, increase in demand and more efficient production process, higher premium nitrile gloves, lower synthetic and natural latex price and favourable exchange rate," it said.

Hartalega said demand for gloves surged substantially due to the outbreak of H1N1, resulted in tight supply for both synthetic and natural latex gloves.

"We have started to build another plant with 10 new advanced high capacity glove production lines in June 2009 and targeted to commission two of the production lines by end of the financial year.

"With continuous growth in demand for gloves from the healthcare and food sector, the group has a positive outlook," it said.

The group's products are sold to the health care industry. It said glove consumption was inelastic in the medical environment because the usage of glove is mandatory for disease control.

It added its nitrile synthetic glove was well accepted by the end users due to it high quality and elastic PROPERTIES [] that mimic that of a natural rubber glove.

"Our protein free and competitive priced nitrile glove has made it more affordable for the acute health care industry to continue switching from the natural rubber to our synthetic nitrile glove to avoid the protein allergy problem," it said.

From The Edge

Written by Joseph Chin

Thursday, 28 January 2010 18:44

KUALA LUMPUR: HARTALEGA HOLDINGS BHD []'s earnings rose 67% to RM37.2 million in the third quarter ended Dec 31, 2009 from RM22.23 million a year ago, boosted by higher demand for its gloves.

It said on Thursday, Jan 28 that revenue rose 24.8% to RM148.59 million from RM119.05 million. Earnings per share were 15.35 sen compared with 9.17 sen. It declared five sen dividend per share.

"The significant achievement in revenue and profit before tax is in line with the group's continuous expansion in production capacity, increase in demand and more efficient production process, higher premium nitrile gloves, lower synthetic and natural latex price and favourable exchange rate," it said.

Hartalega said demand for gloves surged substantially due to the outbreak of H1N1, resulted in tight supply for both synthetic and natural latex gloves.

"We have started to build another plant with 10 new advanced high capacity glove production lines in June 2009 and targeted to commission two of the production lines by end of the financial year.

"With continuous growth in demand for gloves from the healthcare and food sector, the group has a positive outlook," it said.

The group's products are sold to the health care industry. It said glove consumption was inelastic in the medical environment because the usage of glove is mandatory for disease control.

It added its nitrile synthetic glove was well accepted by the end users due to it high quality and elastic PROPERTIES [] that mimic that of a natural rubber glove.

"Our protein free and competitive priced nitrile glove has made it more affordable for the acute health care industry to continue switching from the natural rubber to our synthetic nitrile glove to avoid the protein allergy problem," it said.

From The Edge

{kind=link}

This news is positive for Coastal

Company Name : COASTAL CONTRACTS BHD

Stock Name : COASTAL

Date Announced : 28/01/2010

Type : Announcement

Subject : Coastal Contracts Bhd (“Coastal” or “Company”) – Memorandum of Understanding (“MoU”) between Ramunia Fabricators Sdn Bhd (“RFSB”) and Pleasant Engineering Sdn Bhd (“PESB”)

Contents : The Board of Directors of Coastal is pleased to announce that its wholly-owned subsidiary, PESB, has on 28 January 2010 signed a MoU with RFSB for the proposed collaboration to undertake the tendering, bidding and fabrication in relation to any contract involving the engineering, procurement and construction of any topsides, jackets or any structures for the oil and gas industry.

RFSB is a wholly-owned subsidiary of Ramunia Holdings Bhd (“Ramunia”), and is involved in civil, structural and building maintenance, mechanical engineering and maintenance, as well as offshore facilities and tanks/tanks farm construction.