Warren Buffett's writings include his annual reports and various articles.

Buffett is recognized by communicators as a great story-teller, as evidenced by his annual letters to shareholders. He warned about the pernicious effects of inflation:

"The arithmetic makes it plain that inflation is a far more devastating tax than anything that has been enacted by our legislatures. The inflation tax has a fantastic ability to simply consume capital. It makes no difference to a widow with her savings in a 5 percent passbook account whether she pays 100 percent income tax on her interest income during a period of zero inflation, or pays no income taxes during years of 5 percent inflation."

— Buffett, Fortune (1977)

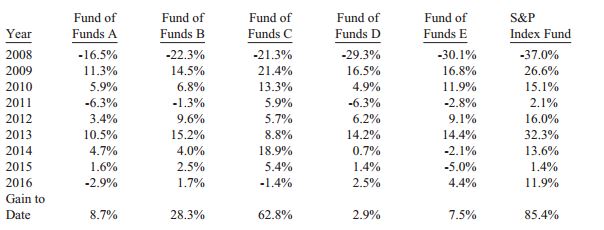

In his article "The Superinvestors of Graham-and-Doddsville", Buffett rebutted the academic efficient-market hypothesis, that beating the S&P 500 was "pure chance", by highlighting the results achieved by a number of students of the Graham and Dodd value investing school of thought. In addition to himself, Buffett named Walter J. Schloss, Tom Knapp, Ed Anderson (Tweedy, Browne LLC), William J. Ruane (Sequoia Fund, Inc.), Charles Munger (Buffett's own business partner at Berkshire), Rick Guerin (Pacific Partners, Ltd.), and Stan Perlmeter (Perlmeter Investments).

In his November 1999 Fortune article, he warned of investors' unrealistic expectations:

Let me summarize what I've been saying about the stock market: I think it's very hard to come up with a persuasive case that equities will over the next 17 years perform anything like—anything like—they've performed in the past 17. If I had to pick the most probable return, from appreciation and dividends combined, that investors in aggregate—repeat, aggregate—would earn in a world of constant interest rates, 2% inflation, and those ever hurtful frictional costs, it would be 6%!

— Buffett, Fortune (1999)