Whitney Tilson’s email to investors discussing the wild week

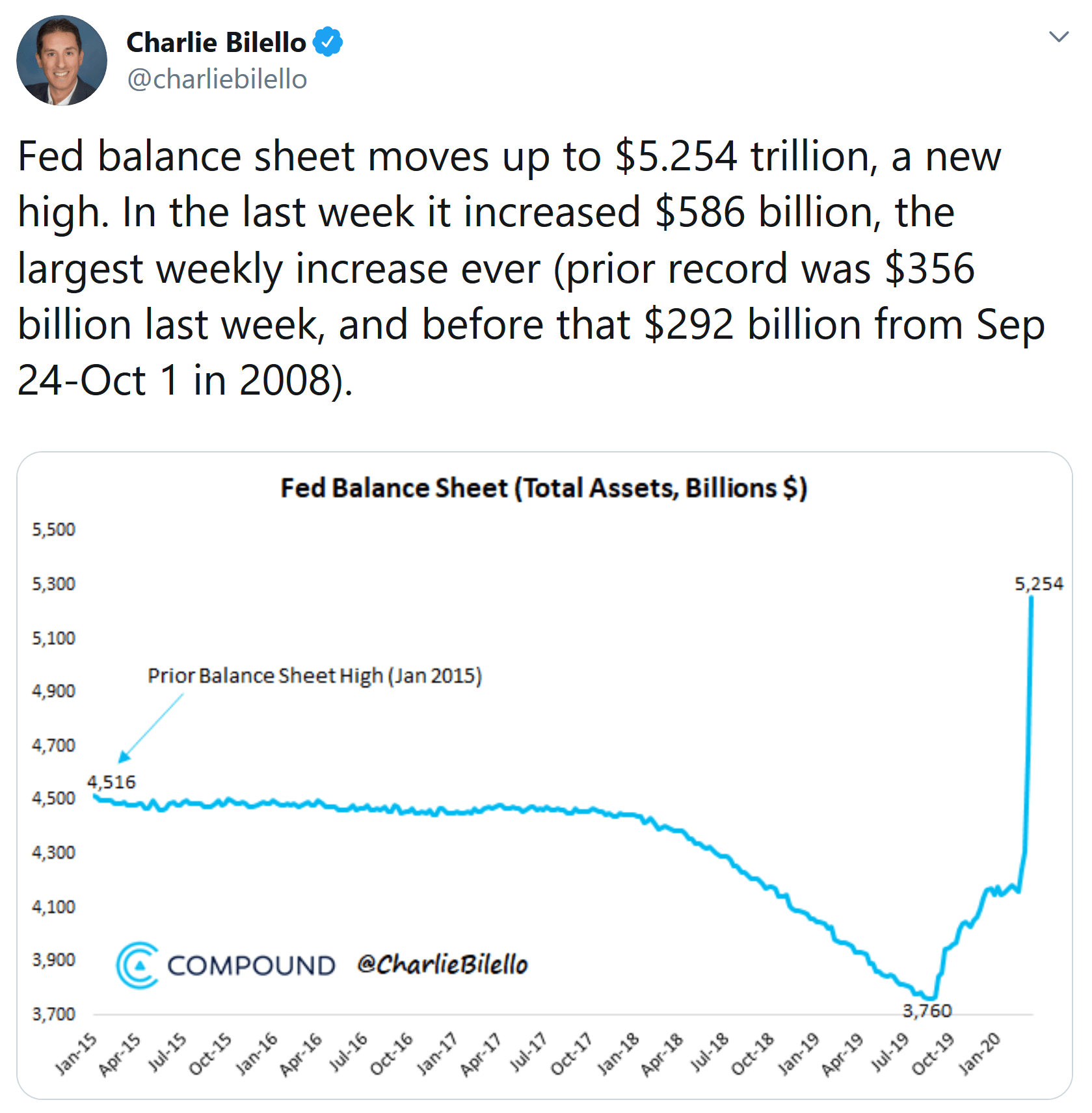

1) What a wild week! The sharpest, fastest bear market in history – the S&P 500 Index was down 35.2% from its closing high on February 19 to its intraday low on Monday – was followed by the sharpest, fastest move back into bull market territory in history, as the index rallied 20% from that point through yesterday's close. Both Tuesday and the past three days were the best for the Dow in 87 years.

I can't recall such a violent upward move in my entire career. I checked the bounces off the bottoms reached on October 10, 2002 and March 6, 2009 (the closing low was March 9, but the intraday low was on March 6) and, in the four days afterward, the S&P 500 rose by "only" 12.5% and 12.3%, respectively. And going back to the Dow's 22.6% plunge on Black Monday on October 19, 1987, while it rose 5.9% the next day, it then trickled downward for another month and a half – going well below its Black Monday close.

I rarely have opinions about where I think the market in general is going, especially in the short term, as this isn't my area of expertise. I find it a far better use of my time to study particular companies and industries to try to develop proprietary insights.

But Monday was one of those rare times. In my e-mail that day, I wrote:

..... why we've come to the firm conclusion that this is the absolute best time to be an investor in more than a decade. To borrow a phrase from one of my friends, "we're trembling with greed" right now.

................

If this doomsday scenario doesn't come to pass, stocks will likely go nuts.

So after the big move in the past three days, what's my thinking? Over the next few months, I no longer have a strong feeling. I think there's a bell curve of possible outcomes, and we're right in middle of it.

But if you ask me where we will be in a year (which is the absolute minimum time horizon I tend to consider) – I think odds are at least 75% that stocks will be higher.

2) In yesterday's e-mail, I wrote:

I just completed a report on [the coronavirus crisis] that I think is the best work I've ever done.

It's broken into three parts:

1. Why I'm Optimistic That We'll Soon Stop the Coronavirus

2. The Five Reasons We're Bullish on Stocks Right Now

3. 10 Stocks to Buy to Profit from the Coming Market Upturn

As it becomes clear that we've controlled the spread of the virus and know exactly where the outbreaks are – which could happen as soon as a couple of weeks from now – we can start bringing our economy back to life.

https://www.valuewalk.com/2020/03/ackmans-greatest-trade/

1) What a wild week! The sharpest, fastest bear market in history – the S&P 500 Index was down 35.2% from its closing high on February 19 to its intraday low on Monday – was followed by the sharpest, fastest move back into bull market territory in history, as the index rallied 20% from that point through yesterday's close. Both Tuesday and the past three days were the best for the Dow in 87 years.

I can't recall such a violent upward move in my entire career. I checked the bounces off the bottoms reached on October 10, 2002 and March 6, 2009 (the closing low was March 9, but the intraday low was on March 6) and, in the four days afterward, the S&P 500 rose by "only" 12.5% and 12.3%, respectively. And going back to the Dow's 22.6% plunge on Black Monday on October 19, 1987, while it rose 5.9% the next day, it then trickled downward for another month and a half – going well below its Black Monday close.

I rarely have opinions about where I think the market in general is going, especially in the short term, as this isn't my area of expertise. I find it a far better use of my time to study particular companies and industries to try to develop proprietary insights.

But Monday was one of those rare times. In my e-mail that day, I wrote:

..... why we've come to the firm conclusion that this is the absolute best time to be an investor in more than a decade. To borrow a phrase from one of my friends, "we're trembling with greed" right now.

................

If this doomsday scenario doesn't come to pass, stocks will likely go nuts.

So after the big move in the past three days, what's my thinking? Over the next few months, I no longer have a strong feeling. I think there's a bell curve of possible outcomes, and we're right in middle of it.

But if you ask me where we will be in a year (which is the absolute minimum time horizon I tend to consider) – I think odds are at least 75% that stocks will be higher.

2) In yesterday's e-mail, I wrote:

I just completed a report on [the coronavirus crisis] that I think is the best work I've ever done.

It's broken into three parts:

1. Why I'm Optimistic That We'll Soon Stop the Coronavirus

2. The Five Reasons We're Bullish on Stocks Right Now

3. 10 Stocks to Buy to Profit from the Coming Market Upturn

As it becomes clear that we've controlled the spread of the virus and know exactly where the outbreaks are – which could happen as soon as a couple of weeks from now – we can start bringing our economy back to life.

https://www.valuewalk.com/2020/03/ackmans-greatest-trade/