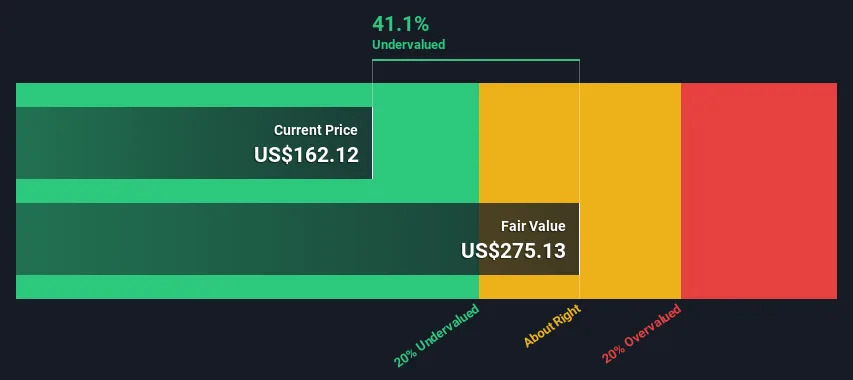

Stocks for the long run.

The power of compounding is truly remarkable, almost magical for those with the ability to identify these companies with earnings power over the long term.

Do you know that DLady was priced RM 1.60 per share, Nestle RM 6 to RM 8 per share and Petdag RM 2.00 per share in the 1990s?

Today, DLady is RM 23.00 per share, Nestle is RM 120.00 per share and Petdag is RM 22.00 per share.

The prices of these stocks have dropped from their highest. DLady has dropped from its historical high price of RM 75.00 per share. Nestle has dropped from its high of RM 160+ per share. Similarly, Petdag has dropped from its high price of RM 30+ per share a few years ago.

DLady has dropped a lot and there are various reasons for these.

How can you exploit any opportunities depend on how you approach your investing.

Enduring multi-baggers and Transitory multi-baggers.

ENDURING multi-baggers are those companies whose wealth creation is long-lasting and correction from the peak valuation is limited.

In fact, they continue to exist as multi-baggers even after the correction.

The enduring multi-bagging companies are typically few and difficult to be spotted, and most of the time they appear to be expensive at the time of buying because of the lack of faith in their longevity and size of growth.

TRANSITORY multi-baggers, on the contrary, are easier to be spotted but they always end up giving nasty end results.

Corrections are typically almost 100 per cent.

Cyclicals broadly come under this category.

The tragedy with this class of companies is that if you cannot sell in time, nothing is left in your hand.

But as correction is inevitable, market as a whole is left high and dry with a bad experience.

These companies are plenty and easy to be found, and they attract a lot of crowd.

Ten-baggers operate in growth industries.

Ten-baggers are shares where you make 10 times your money (I believe the phrase is derived from baseball). Such opportunities are rare, but I have been fortunate enough over the years to be involved in a few such situations: DLady, Nestle, Petdag and others.

There tend to be some common characteristics among these winners. The businesses all operate in growth industries and the company in question must be able to grow the top line. No one ever made a tenfold return on a pure margin improvement, or cost-cutting story with no sales growth.

Turnarounds are, however, a rich source of 10-baggers. For these to work, one's timing has to be immaculate, and the underlying business has to be sound - just desperately unloved by the stock market.

Patience is needed.

Such returns need patience. A hedge fund that churns its holdings every few months will never enjoy a 10-bagger. And therein lies the greatest danger: selling too early to enjoy the 1,000 per cent gain.

When you have doubled or trebled your money, it is so tempting to cash in profits. It must have been tempting in the early 1950s to take profits on Glaxo shares, just a few years after their 1947 flotation. Or to have done the same for Tesco which floated in the same year. Or sell Racal in the late 1960s after its 1961 market debut, decades before it spun off Vodafone. Yet each of those shares rewarded patient investors with epic performances over many decades, all 20-baggers at least, not even allowing for dividend.

One of the advantages that private equity enjoys is that it is forced to take a reasonably long-term view, and so is usually unable to rush for the exit at the first opportunity. Venture capital's other edge over quoted investors is debt: gearing in successful situations always amplifies the return to equity-holders. Typically, buy-outs have structures where 70 per cent of the capital is borrowed.

Quoted companies probably have the reverse capitalisation, with equity providing three-quarters of the funding. And as ever in investing, those who regularly find 10-baggers say you should stick to your own sphere of competence: buy what you understand.

Usual rules apply: Quality, Management & Valuation

But the usual rules apply: look for real companies with competent management and a proven business model.

You won't find a 10-bagger among much of the over-hyped, speculative froth. Search for the solid operation with strong fundamentals and a high quality of earnings.

Very few acquisitive vehicles are 10-baggers. Management in such firms focuses on doing deals rather than organically growing its core business. This can produce reasonable returns, but rarely delivers the stellar, long-run performance that can come from a strong business franchise in an attractive niche.

And balance sheets matter: 10-baggers must be able to fund expansion internally or through debt. Companies that are forever issuing equity dilute their stock performance.

So good luck in your search for the next blockbuster. It may well be an obscure, neglected company now, but with the potential for greatness. The secret is to spot that potential.