A Conversation With Benjamin Graham

Benjamin Graham, senior author of Security Analysis, needs no introduction to the readers of this magazine [Financial Analysts Journal.] The Journal thanks Charles D. Ellis, a member of its Editorial Board, for making available this presentation, in question-and-answer format, to a recent Donaldson, Lufkin & Jenrette seminar.

--------------------------------------------------------------------------------

In the light of your 60-odd years of experience in Wall Street what is your overall view of common stocks?

Common stocks have one important characteristics and one important speculative characteristic. Their investment value and average market price tend to increase irregularly but persistently over the decades, as their net worth builds up through the reinvestment of undistributed earnings--incidentally, with no clear-cut plus or minus response to inflation. However, most of the time common stocks are subject to irrational and excessive price fluctuations in both directions, as the consequence of the ingrained tendency of most people to speculate or gamble--i.e., to give way to hope, fear and greed.

What is your view of Wall Street as a financial institution?

A highly unfavorable--even a cynical--one. The Stock Exchanges appear to me chiefly as a John Bunyan type of Vanity Fair, or a Falstaffian joke, that frequently degenerates into a madhouse--"a tale full of sound and fury, signifying nothing." The stock market resembles a huge laundry in which institutions take in large blocks of each other's washing--nowadays to the tune of 30 million shares a day--without true rhyme or reason. But technologically it is remarkably well-organized.

What is your view of the financial community as a whole?

Most of the stockbrokers, financial analysts, investment advisers, etc., are above average in intelligence, business honesty and sincerity. But they lack adequate experience with all types of security markets and an overall understanding of common stocks--of what I call "the nature of the beast." They tend to take the market and themselves too seriously. They spend a large part of their time trying, valiantly and ineffectively, to do things they can't do well.

What sort of things, for example?

To forecast short- and long-term changes in the economy, and in the price level of common stocks, to select the most promising industry groups and individual issues--generally for the near-term future.

Can the average manager of institutional funds obtain better results than the Dow Jones Industrial Average or the Standard & Poor's Index over the years?

No. In effect, that would mean that the stock market experts as a whole could beat themselves--a logical contradiction.

Do you think, therefore, that the average institutional client should be content with the DJIA results or the equivalent?

Yes. Not only that, but I think they should require approximately such results over, say, a moving five-year average period as a condition for paying standard management fees to advisors and the like.

What about the objection made against so-called index funds that different investors have different requirements?

At bottom that is only a convenient cliche or alibi to justify the mediocre record of the past. All investors want good results from their investments, and are entitled to them to the extent that they are actually obtainable. I see no reason why they should be content with results inferior to those of an indexed fund or pay standard fees for such inferior results.

Turning now to individual investors, do you think that they are at a disadvantage compared with the institutions, because of the latter's huge resources, superior facilities for obtaining information, etc.?

On the contrary, the typical investor has a great advantage over the large institutions.

Why?

Chiefly because these institutions have a relatively small field of common stocks to choose from--say 300 to 400 huge corporations--and they are constrained more or less to concentrate their research and decisions on this much over-analyzed group. By contrast, most individuals can choose at any time among some 3000 issues listed in the Standard & Poor's Monthly Stock Guide. Following a wide variety of approaches and preferences, the individual investor should at all times be able to locate at least one per cent of the total list--say, 30 issues or more--that offer attractive buying opportunities.

What general rules would you offer the individual investor for his investment policy over the years?

Let me suggest three such rules: (1) The individual investor should act consistently as an investor and not as a speculator. This means, in sum, that he should be able to justify every purchase he makes and each price he pays by impersonal, objective reasoning that satisfies him that he is getting more than his money's worth for his purchase--in other words, that he has a margin of safety, in value terms, to protect his commitment. (2) The investor should have a definite selling policy for all his common stock commitments, corresponding to his buying techniques. Typically, he should set a reasonable profit objective on each purchase--say 50 to 100 per cent--and a maximum holding period for this objective to be realized--say, two to three years. Purchases not realizing the gain objective at the end of the holding period should be sold out at the market. (3) Finally, the investor should always have a minimum percentage of his total portfolio in common stocks and a minimum percentage in bond equivalents. I recommend at least 25 per cent of the total at all times in each category. A good case can be made for a consistent 50-50 division here, with adjustments for changes in the market level. This means the investor would switch some of his stocks into bonds on significant rises of the market level, and vice-versa when the market declines. I would suggest, in general, an average seven- or eight-year maturity for his bond holdings.

In selecting the common stock portfolio, do you advise careful study of and selectivity among different issues?

In general, no. I am no longer an advocate of elaborate techniques of security analysis in order to find superior value opportunities. This was a rewarding activity, say, 40 years ago, when our textbook "Graham and Dodd" was first published; but the situation has changed a great deal since then. In the old days any well-trained security analyst could do a good professional job of selecting undervalued issues through detailed studies; but in the light of the enormous amount of research now being carried on, I doubt whether in most cases such extensive efforts will generate sufficiently superior selections to justify their cost. To that very limited extent I'm on the side of the "efficient market" school of thought now generally accepted by the professors.

What general approach to portfolio formation do you advocate?

Essentially, a highly simplified one that applies a single criteria or perhaps two criteria to the price to assure that full value is present and that relies for its results on the performance of the portfolio as a whole--i.e., on the group results--rather than on the expectations for individual issues.

Can you indicate concretely how an individual investor should create and maintain his common stock portfolio?

I can give two examples of my suggested approach to this problem. One appears severely limited in its application, but we found it almost unfailingly dependable and satisfactory in 30-odd years of managing moderate-sized investment funds. The second represents a great deal of new thinking and research on our part in recent years. It is much wider in its application than the first one, but it combines the three virtues of sound logic, simplicity of application, and an extraordinarily good performance record, assuming--contrary to fact--that it had actually been followed as now formulated over the past 50 years--from 1925 to 1975.

Some details, please, on your two recommended approaches.

My first, more limited, technique confines itself to the purchase of common stocks at less than their working-capital value, or net-current-asset value, giving no weight to the plant and other fixed assets, and deducting all liabilities in full from the current assets. We used this approach extensively in managing investment funds, and over a 30-odd year period we must have earned an average of some 20 per cent per year from this source. For a while, however, after the mid-1950's, this brand of buying opportunity became very scarce because of the pervasive bull market. But it has returned in quantity since the 1973-74 decline. In January 1976 we counted over 300 such issues in the Standard & Poor's Stock Guide--about 10 per cent of the total. I consider it a foolproof method of systematic investment--once again, not on the basis of individual results but in terms of the expectable group outcome.

Finally, what is your other approach?

This is similar to the first in its underlying philosophy. It consists of buying groups of stocks at less than their current or intrinsic value as indicated by one or more simple criteria. The criterion I prefer is seven times the reported earnings for the past 12 months. You can use others--such as a current dividend return above seven per cent or book value more than 120 percent of price, etc. We are just finishing a performance study of these approaches over the past half-century--1925-1975. They consistently show results of 15 per cent or better per annum, or twice the record of the DJIA for this long period. I have every confidence in the threefold merit of this general method based on (a) sound logic, (b) simplicity of application, and (c) an excellent supporting record. At bottom it is a technique by which true investors can exploit the recurrent excessive optimism and excessive apprehension of the speculative public.

--------------------------------------------------------------------------------

"It is fortunate for Wall Street as an institution that a small minority of people can trade successfully and that many others think they can. The accepted view holds that stock trading is like anything else; i.e., with intelligence and application, or with good professional guidance, profits can be realized. Our own opinion is skeptical, perhaps jaundiced. We think that, regardless of preparation and method, success in trading is either accidental and impermanent or else due to a highly uncommon talent."

"...we must express some serious reservations and perhaps prejudices that we hold about the basic utility of industry analysis as it is practiced in Wall Street and as its results are exhibited in typical brokerage-house studies. Industry analysis relates to the past and the future. Insofar as it relates to the past, the elements dealt with have already influenced the results of the companies in the industry and the average market price of their shares. ...When industry analysis addresses itself to the future it generally assumes that past characteristics and trends will continue. We find these forward projections of the past to be misleading at least as often as they are useful."

"If we could assume that the price of each of the leading issues already reflects the expectable developments of the next year or two, then a random selection should work out as well as one confined to those with the best near-term outlook."

-- Security Analysis, Third Edition, 1951

http://www.bylo.org/bgraham76.html

Saturday, 17 January 2009

Benjamin Graham's strategy

Published January 14, 2009

Tags: Benjamin Graham, Investment Ideas, Value Investing

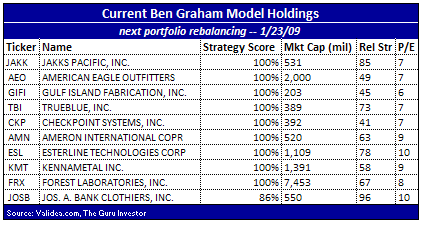

I always find it interesting to look at the guru portfolios I run on Validea, and ask the question “what is working” now? Over the last month, in a period where the S&P is up 0.4%, 11 out of Validea’s 13 portfolios have outperformed. The best performer is my Ben Graham strategy, up 9.4%. Incidentally, the Graham portfolio is also the best long term performer (up 89.3 percent vs. -12.9% for the S&P since July 15, 2003). The table below shows the performance of the 10-stock portfolios I run over the last 30 days.

In looking at the specifics, Graham’s approach limited risk in a number of ways, and my Graham-based model lays out several of those methods. For example, one key criterion is that a firm’s current ratio — that is, the ratio of its current assets to its current liabilities — is at least two, showing that the firm is in good financial shape. The approach also targets financially sound firms by requiring that long-term debt not exceed long-term assets.

I always find it interesting to look at the guru portfolios I run on Validea, and ask the question “what is working” now? Over the last month, in a period where the S&P is up 0.4%, 11 out of Validea’s 13 portfolios have outperformed. The best performer is my Ben Graham strategy, up 9.4%. Incidentally, the Graham portfolio is also the best long term performer (up 89.3 percent vs. -12.9% for the S&P since July 15, 2003). The table below shows the performance of the 10-stock portfolios I run over the last 30 days.

In looking at the specifics, Graham’s approach limited risk in a number of ways, and my Graham-based model lays out several of those methods. For example, one key criterion is that a firm’s current ratio — that is, the ratio of its current assets to its current liabilities — is at least two, showing that the firm is in good financial shape. The approach also targets financially sound firms by requiring that long-term debt not exceed long-term assets.

Two other criteria the Graham method uses to find low-risk plays: the price/earnings ratio and the price/book ratio. Graham wanted P/E ratios to be no greater than 15 (and, as another signal of his conservative style, he used three-year average earnings rather than trailing 12-month earnings, to ensure that one-year anomalies didn’t skew the ratio). For the price/book ratio, he used a more unusual standard: He believed that the P/E ratio multiplied by the P/B ratio should be no greater than 22.

By using these conservative, fundamental-focused measures, Graham earned himself the moniker “The Father of Value Investing”. And as the father of that school of thought, he inspired a number of famous “sons” — Mario Gabelli, John Neff, John Templeton, and, most famously, Buffett, are all Graham disciples who went on to their own stock market greatness.

Perhaps the most intriguing part of Graham’s strategy is that, while it was published almost 60 years ago, it still works today. Since I started tracking it more than five years ago, my 10-stock Graham-based portfolio has racked up an impressive gain while the overall market is down.

Here are the current holdings of the 10-stock Graham portfolio:

http://theguruinvestor.com/2009/01/14/ben-graham-portfolio-at-top-of-the-charts/

Friday, 16 January 2009

Students join the home-owning classes

Students join the home-owning classes

Nicola VenningLast Updated: 10:47AM BST 07 Sep 2006

One of the flats in Artillery House

Renting near universities can be expensive, but Nicola Venning says buying for your children can earn you top marks

Children are expensive. And they do not get cheaper when they go to university, especially at this time of year, when thousands of students face a scramble for decent, reasonably-priced digs in London before the start of the university term.

More than 173,000 students live in London, according to the Higher Educational Statistical Agency. And 42 per cent of them must live in private accommodation, so competition for flats can be fierce. "Flats go within two weeks, and by October, people are desperate," says Alex Koch de Gooryend, a lettings manager with Knight Frank.

Rather than run this gauntlet, some parents decide to buy a home to let to their student children.

"We are seeing more and more instances of parents buying for their student offspring," adds Nik Madan, lettings director with John D Wood. "I'd say it's doubled in the past five years, partly because rents, particularly in London, are creeping up higher and higher. Also, many parents buy directly in their children's names to avoid inheritance tax."

Drasco Vasiljevic, a 52-year-old meteorologist in London, has just paid £250,000 for a studio flat in Chelsea Wharf for his 19-year-old daughter Jelena, who will use it when she starts her second year at the London School of Economics this autumn.

"Prices to rent were about £250 per week in this central area, about the same as a mortgage, so I decided to buy," Vasiljevic says.

Jelena adds: "It's a good idea, particularly if I stay in the city after university."

But beware... every student loves to party. Madan recalls a three-bedroom home in Richmond. "The owners' son and his friends trashed it," Madan says. "They were unable to let it."

But avoiding party animals is only half the challenge. You need to think clearly. "You are making a long-term investment," cautions Tim Hyatt, lettings manager with Knight Frank. He suggests buying into a new build scheme offering a two-year rent guarantee that would cover any void periods.

Berkeley Homes, for example, is selling Loft Apartments in the former Ministry for Pensions Building in Acton, West London: two-bedroom flats start from £299,950. And in Woolwich, south-east London, you can pick up a one-bedroom apartment in the redeveloped 19th century Artillery House at the Royal Arsenal from £250,000.

Whatever you do, though, stick to the golden rules of buy to let: invest in an emerging area with decent public transport and reasonable amenities.

"Affordable areas east of the City, such as Newham, Limehouse, Stratford and the Royal Docks (where one-bed flats start around £200,000) are worthy of note," says Richard Davies, lettings director with Chesterton.

http://www.telegraph.co.uk/property/3352474/Students-join-the-home-owning-classes.html

Nicola VenningLast Updated: 10:47AM BST 07 Sep 2006

One of the flats in Artillery House

Renting near universities can be expensive, but Nicola Venning says buying for your children can earn you top marks

Children are expensive. And they do not get cheaper when they go to university, especially at this time of year, when thousands of students face a scramble for decent, reasonably-priced digs in London before the start of the university term.

More than 173,000 students live in London, according to the Higher Educational Statistical Agency. And 42 per cent of them must live in private accommodation, so competition for flats can be fierce. "Flats go within two weeks, and by October, people are desperate," says Alex Koch de Gooryend, a lettings manager with Knight Frank.

Rather than run this gauntlet, some parents decide to buy a home to let to their student children.

"We are seeing more and more instances of parents buying for their student offspring," adds Nik Madan, lettings director with John D Wood. "I'd say it's doubled in the past five years, partly because rents, particularly in London, are creeping up higher and higher. Also, many parents buy directly in their children's names to avoid inheritance tax."

Drasco Vasiljevic, a 52-year-old meteorologist in London, has just paid £250,000 for a studio flat in Chelsea Wharf for his 19-year-old daughter Jelena, who will use it when she starts her second year at the London School of Economics this autumn.

"Prices to rent were about £250 per week in this central area, about the same as a mortgage, so I decided to buy," Vasiljevic says.

Jelena adds: "It's a good idea, particularly if I stay in the city after university."

But beware... every student loves to party. Madan recalls a three-bedroom home in Richmond. "The owners' son and his friends trashed it," Madan says. "They were unable to let it."

But avoiding party animals is only half the challenge. You need to think clearly. "You are making a long-term investment," cautions Tim Hyatt, lettings manager with Knight Frank. He suggests buying into a new build scheme offering a two-year rent guarantee that would cover any void periods.

Berkeley Homes, for example, is selling Loft Apartments in the former Ministry for Pensions Building in Acton, West London: two-bedroom flats start from £299,950. And in Woolwich, south-east London, you can pick up a one-bedroom apartment in the redeveloped 19th century Artillery House at the Royal Arsenal from £250,000.

Whatever you do, though, stick to the golden rules of buy to let: invest in an emerging area with decent public transport and reasonable amenities.

"Affordable areas east of the City, such as Newham, Limehouse, Stratford and the Royal Docks (where one-bed flats start around £200,000) are worthy of note," says Richard Davies, lettings director with Chesterton.

http://www.telegraph.co.uk/property/3352474/Students-join-the-home-owning-classes.html

Buy-to-let: Warning for 'accidental' landlords

Buy-to-let: Warning for 'accidental' landlords

Home owners who think they can ride out the housing downturn by offering their properties to let, rather than for sale face a nasty shock.

By Paula Hawkins Last Updated: 11:53AM GMT 16 Jan 2009

Warning for 'accidental' landlords

It may sound like the easy option, but home owners who think they can ride out the housing downturn by offering their properties to let rather than for sale face a nasty shock. This is a difficult rental market in which only the best properties are letting easily, and those "accidental" landlords who take a less than professional approach to renting out their homes are facing long and expensive void periods.

"Contrary to what people might think, the lettings market is not busy across the board," says Tim Hyatt, head of residential lettings at Knight Frank. "As a landlord you have to be totally flexible and you need to treat the property as you would an investment property: it must be well-priced, neutrally decorated, and ready for someone to move into straight away."

Accidental landlords have always been a feature of the private rentals market, but their numbers have risen sharply over the past year.

"The stagnant housing market is making it virtually impossible for many people to sell – at least at prices they are happy with," says Melanie Bien, a director of Savills Private Finance, the mortgage broker.

According to Mr Hyatt, accidental landlords contributed around 25pc of the increase in Knight Frank's stock levels in 2008. Research published by the National Landlords Association (NLA) late last year showed that the number of new landlord instructions to let in the third quarter of 2008 rose at the fastest rate since records began. Booming supply has not been matched by an increase in demand for rental property, however, as the number of applicants is rising, but at a much slower pace.

This trend is set to continue in 2009. "It is likely that if property prices keep falling we will see more people choosing to hold on to their asset and let their property rather than sell it," says Richard Price, director of operations at the NLA.

Thanks in part to the influx of new landlords, the lettings market is now highly competitive. "Stock levels in many offices are up 100pc over the past 12 months, while in some offices levels are three times as high as they were at this time last year," Mr Hyatt says. Jane Ingram, head of lettings at Savills, says that its letting agencies are seeing similar increases in stock levels.

"They are significantly higher than a year ago, with the number of properties doubling, if not trebling – partly due to the rise in accidental landlords coming new to the market," she says.

The result has been a downward pressure on rents, which is particularly acute at the higher end of the rentals market.

"At the top end of the London market, there is a huge variety of stock for people to look at, so this is a highly competitive market," says Mr Hyatt. "In some areas, landlords are having to look at rent reductions of 20pc to 40pc per week."

Knight Frank's figures show that rents are now back to December 2006 levels – and in fact are just 4pc above where they were in September 2001.

Renting out a property in a tough market is not as straightforward as it may at first appear. Seasoned buy-to-let investors purchase the kind of properties that they know to be in demand in a certain area, but accidental landlords do not have the luxury of choice. According to advice from the search website PropertyFinder, "landlords who have not had the power to choose an appropriate property will find it difficult to cover their costs".

This does not mean that you should reject out of hand the option of letting out your property. The key thing is to research the market very carefully, and find out which properties are in demand and at what rates. "Take the advice of your local lettings agent," says Mr Hyatt. "I say this all the time but no one listens: ask your agent for some examples of properties that will let overnight and then compare them to your own. If your property does not match up, you should prepare for long void periods."

You may also need to spend some money up front to make your property appeal to renters. "Accidental landlords are people who are renting out private homes decorated to personal taste," Mr Hyatt says. "These properties may not be ideal for the rental market.

"You need to ask yourself if you are prepared to make the necessary investment in the property, and whether you are prepared to refinance in order to make that investment. If not, you may struggle."

Home owners who are highly geared should be very wary of entering the rentals market – research from the NLA shows that more than 70pc of landlords expect rental arrears to become a problem in 2009.

"For the highly geared landlord whose monthly mortgage payments rely heavily on monthly rental income, tenants not paying can quickly spell disaster," says Simon Gordon of the NLA. In fact, while some mortgage lenders offer buy-to-let loans to those with a 25pc deposit, experts say that in order to make money in the current rental market you need to own a larger share.

"The only landlords who are going to make lets work over the next couple of years are those with a decent slab of equity in their property – around 40pc," says Liam Bailey, Knight Frank's head of residential research.

If you decide to go ahead and rent out your property, your first step should be to inform your mortgage lender. "If you fail to do this, you are in breach of the mortgage contract," Ms Bien says. "Theoretically, if the lender finds out, it could insist that you repay the mortgage because you have broken that contract." Many corporate tenants will insist that you provide proof of your lender's consent before signing a contract.

Your lender may allow you to remain on your existing mortgage for a specified length of time before you switch to a buy-to-let deal, or you may be required to make the switch immediately. "If you have to switch to a buy-to-let deal straight away, this may be problematic," Ms Bien explains, "because there are few deals available, and both rates and fees are high."

According to Moneyfacts, the cheapest buy-to-let loan on the market at the moment comes from The Mortgage Works, with a rate of 4.99pc available up to a maximum loan-to-value of 70pc, with an arrangement fee of 2.5pc.

In addition to getting permission from your lender, you need to inform your household insurer, and if you are planning to let your property furnished it is worth getting specialist landlord's insurance.

It pays to know the rules

Landlords are required to comply with a wide variety of ever-changing rules and regulations. Joining a landlord's association is a good idea: these will keep you informed of the regulations and may also offer discounts on services such as landlord's insurance.

Membership costs vary, but you should expect to pay around £70 a year.

Landlords are required to produce an Energy Performance Certificate (EPC) for tenants' inspection (although EPCs do last for 10 years). They must also arrange for deposits to be held by the Deposit Protection Service, or covered by one of the two insurance-backed deposit protection schemes, Mydeposits or the Tenancy Deposit Scheme.

Those landlords who run houses in multiple occupation (HMOs) must also obtain licences and comply with rules set down by the local housing authority.

There is a host of health and safety regulations to follow, too. Landlords are responsible for the upkeep of the property as well as any supplied appliances, furniture and the gas and electricity systems. A landlords' association or lettings agent will be able to supply you with a full list of the checks that need to be carried out.

See our website, telegraph.co.uk/propertyclub, for much more detail on all aspects of being a landlord.

http://www.telegraph.co.uk/finance/personalfinance/investing/4269824/Buy-to-let-Warning-for-accidental-landlords.html

Related Content

More on Investing

Nine in 10 buy-to-let mortgage deals disappear

Buy-to-let 2009 Outlook

No let-up for buy-to-let

Apartment for sale - and the tenants come too

Students join the home-owning classes

Don't bet on buy-to-let If you fancy entering the housing market as a landlord, do your sums carefully, warns Jenny Knight, and don't over-extend yourself

Related partners

Telegraph Investor Services

Legal & General High Income ISA

Investing for your financial future

Home owners who think they can ride out the housing downturn by offering their properties to let, rather than for sale face a nasty shock.

By Paula Hawkins Last Updated: 11:53AM GMT 16 Jan 2009

Warning for 'accidental' landlords

It may sound like the easy option, but home owners who think they can ride out the housing downturn by offering their properties to let rather than for sale face a nasty shock. This is a difficult rental market in which only the best properties are letting easily, and those "accidental" landlords who take a less than professional approach to renting out their homes are facing long and expensive void periods.

"Contrary to what people might think, the lettings market is not busy across the board," says Tim Hyatt, head of residential lettings at Knight Frank. "As a landlord you have to be totally flexible and you need to treat the property as you would an investment property: it must be well-priced, neutrally decorated, and ready for someone to move into straight away."

Accidental landlords have always been a feature of the private rentals market, but their numbers have risen sharply over the past year.

"The stagnant housing market is making it virtually impossible for many people to sell – at least at prices they are happy with," says Melanie Bien, a director of Savills Private Finance, the mortgage broker.

According to Mr Hyatt, accidental landlords contributed around 25pc of the increase in Knight Frank's stock levels in 2008. Research published by the National Landlords Association (NLA) late last year showed that the number of new landlord instructions to let in the third quarter of 2008 rose at the fastest rate since records began. Booming supply has not been matched by an increase in demand for rental property, however, as the number of applicants is rising, but at a much slower pace.

This trend is set to continue in 2009. "It is likely that if property prices keep falling we will see more people choosing to hold on to their asset and let their property rather than sell it," says Richard Price, director of operations at the NLA.

Thanks in part to the influx of new landlords, the lettings market is now highly competitive. "Stock levels in many offices are up 100pc over the past 12 months, while in some offices levels are three times as high as they were at this time last year," Mr Hyatt says. Jane Ingram, head of lettings at Savills, says that its letting agencies are seeing similar increases in stock levels.

"They are significantly higher than a year ago, with the number of properties doubling, if not trebling – partly due to the rise in accidental landlords coming new to the market," she says.

The result has been a downward pressure on rents, which is particularly acute at the higher end of the rentals market.

"At the top end of the London market, there is a huge variety of stock for people to look at, so this is a highly competitive market," says Mr Hyatt. "In some areas, landlords are having to look at rent reductions of 20pc to 40pc per week."

Knight Frank's figures show that rents are now back to December 2006 levels – and in fact are just 4pc above where they were in September 2001.

Renting out a property in a tough market is not as straightforward as it may at first appear. Seasoned buy-to-let investors purchase the kind of properties that they know to be in demand in a certain area, but accidental landlords do not have the luxury of choice. According to advice from the search website PropertyFinder, "landlords who have not had the power to choose an appropriate property will find it difficult to cover their costs".

This does not mean that you should reject out of hand the option of letting out your property. The key thing is to research the market very carefully, and find out which properties are in demand and at what rates. "Take the advice of your local lettings agent," says Mr Hyatt. "I say this all the time but no one listens: ask your agent for some examples of properties that will let overnight and then compare them to your own. If your property does not match up, you should prepare for long void periods."

You may also need to spend some money up front to make your property appeal to renters. "Accidental landlords are people who are renting out private homes decorated to personal taste," Mr Hyatt says. "These properties may not be ideal for the rental market.

"You need to ask yourself if you are prepared to make the necessary investment in the property, and whether you are prepared to refinance in order to make that investment. If not, you may struggle."

Home owners who are highly geared should be very wary of entering the rentals market – research from the NLA shows that more than 70pc of landlords expect rental arrears to become a problem in 2009.

"For the highly geared landlord whose monthly mortgage payments rely heavily on monthly rental income, tenants not paying can quickly spell disaster," says Simon Gordon of the NLA. In fact, while some mortgage lenders offer buy-to-let loans to those with a 25pc deposit, experts say that in order to make money in the current rental market you need to own a larger share.

"The only landlords who are going to make lets work over the next couple of years are those with a decent slab of equity in their property – around 40pc," says Liam Bailey, Knight Frank's head of residential research.

If you decide to go ahead and rent out your property, your first step should be to inform your mortgage lender. "If you fail to do this, you are in breach of the mortgage contract," Ms Bien says. "Theoretically, if the lender finds out, it could insist that you repay the mortgage because you have broken that contract." Many corporate tenants will insist that you provide proof of your lender's consent before signing a contract.

Your lender may allow you to remain on your existing mortgage for a specified length of time before you switch to a buy-to-let deal, or you may be required to make the switch immediately. "If you have to switch to a buy-to-let deal straight away, this may be problematic," Ms Bien explains, "because there are few deals available, and both rates and fees are high."

According to Moneyfacts, the cheapest buy-to-let loan on the market at the moment comes from The Mortgage Works, with a rate of 4.99pc available up to a maximum loan-to-value of 70pc, with an arrangement fee of 2.5pc.

In addition to getting permission from your lender, you need to inform your household insurer, and if you are planning to let your property furnished it is worth getting specialist landlord's insurance.

It pays to know the rules

Landlords are required to comply with a wide variety of ever-changing rules and regulations. Joining a landlord's association is a good idea: these will keep you informed of the regulations and may also offer discounts on services such as landlord's insurance.

Membership costs vary, but you should expect to pay around £70 a year.

Landlords are required to produce an Energy Performance Certificate (EPC) for tenants' inspection (although EPCs do last for 10 years). They must also arrange for deposits to be held by the Deposit Protection Service, or covered by one of the two insurance-backed deposit protection schemes, Mydeposits or the Tenancy Deposit Scheme.

Those landlords who run houses in multiple occupation (HMOs) must also obtain licences and comply with rules set down by the local housing authority.

There is a host of health and safety regulations to follow, too. Landlords are responsible for the upkeep of the property as well as any supplied appliances, furniture and the gas and electricity systems. A landlords' association or lettings agent will be able to supply you with a full list of the checks that need to be carried out.

See our website, telegraph.co.uk/propertyclub, for much more detail on all aspects of being a landlord.

http://www.telegraph.co.uk/finance/personalfinance/investing/4269824/Buy-to-let-Warning-for-accidental-landlords.html

Related Content

More on Investing

Nine in 10 buy-to-let mortgage deals disappear

Buy-to-let 2009 Outlook

No let-up for buy-to-let

Apartment for sale - and the tenants come too

Students join the home-owning classes

Don't bet on buy-to-let If you fancy entering the housing market as a landlord, do your sums carefully, warns Jenny Knight, and don't over-extend yourself

Related partners

Telegraph Investor Services

Legal & General High Income ISA

Investing for your financial future

'Toxic bank’ to soak up bad debts in UK

Financial crisis: The banks are still sinking

Ministers plan a 'toxic bank’ to soak up bad debts and unfreeze the money markets. But will it work, asks Katherine Griffiths.

Last Updated: 12:08PM GMT 16 Jan 2009

Comments 9 Comment on this article

Hang on – didn’t we save Britain’s banks in October? That was when the Government gave £500 billion to inject capital into Royal Bank of Scotland (RBS), Lloyds and HBOS and pledged ongoing support to get high-street lenders back on their feet.

So, why are banks’ share prices still plummeting, while they refuse to lend to each other because they are suspicious about what hidden nasties are on their rivals’ balance sheets? Their chief executives privately warn the Government – they are reluctant to deliver this message in public – that they do not have the cash to provide mortgages and loans to individuals and businesses.

The reality is that, while the Prime Minister, the self-styled saviour of the world, rode high in public opinion in October and November for leading the charge to deal with the global banking crisis, in fact what the Government had done was to carry out emergency surgery to save the banks – and the entire financial system – from immediate collapse.

Now it is time for the more painful process of restoring the patient to health. For the banks the medicine is going to be unpleasant to swallow – it will mean shrunken salaries and no bonuses for many. For the rest of us it is going to be expensive and could take years to administer.

The Government is understandably unwilling to come out with this prognosis, but it needs to do so soon. The US has been ahead of Britain in preparing for a second round of emergency operations on its banks, with Citigroup set to be split into a “good” and “bad” bank so that investors can feel confident about owning its shares again.

Switzerland has also set up a special entity to swallow about £30 billion of toxic assets from its largest bank, UBS, so that it can begin the process of recovery.

In the UK, we have seen this week measures from Lord Mandelson’s department to help small businesses, but they will only have a marginal impact unless ministers can deal with the banking disease at the heart of the problem.

Now, the word out of Downing Street is that ministers are on the case and are preparing to announce the creation of a “toxic bank” to soak up more than £30 billion of British banks’ bad debts. The plan will form the centrepiece of a fresh bail-out designed to get them lending again, to each other and to their customers.

The difficulties the Government faces are immense.

The wholesale markets, which banks use for much of their funding so that they can lend to customers, remain frozen. This is because of a breakdown of trust between financial institutions: no one can be sure what problems banks are sitting on, so investors do not want to lend them money in case more difficulties emerge and they lose their cash.

What is needed most is clarity: what really is on the books of each bank? It is difficult to put a price on their troubled assets, many of which are based on the collapsed subprime loans sector in the US.

The Government is hoping that clarity is coming soon. In the next few weeks, the banks will report their results for 2008, and to do so they need to get their figures signed off by auditors. The auditing firms – such as PricewaterhouseCoopers, KPMG and Deloitte – will have to agree to the valuation of banks’ assets.

The accountants will want to get these values right because, if their banking clients should fail later, the first port of call for potential shareholders’ lawsuits will be the deep-pocketed auditors.

In anticipation, ministers are preparing the creation of that “toxic bank” to allow for a fresh start.

In theory, it will suck in all of the failing assets that have poisoned the banks’ balance sheets and destroyed confidence in the system. That would leave the remaining banks cleansed and able to attract both investors who want to put their capital in banks’ shares, and providers of funds so that the wholesale markets would be defrosted, and lending could be restarted.

Of course, if it was as simple as that, a bad bank would have been constituted months ago and Gordon Brown and Alistair Darling would be hailing it as part of their world-leading financial recovery plan.

As Sweden found when it had to take similar measures in the early Nineties, creating a bad bank is fraught with problems. As with this entire crisis, the main challenge is how to value the assets.

In order to take control of the toxic investments, the Government would have to give the banks some money in return.

If it sets the price too low, banks will either refuse to hand the assets over, thereby not solving the systemic problem of a lack of confidence, or will have to take new write-downs to recognise the lower value, further weakening their own books. If the price is too high, there will be an outcry that taxpayers’ money is being squandered to save bankers’ skins.

Ministers are keen to ensure that banks are not seen by the public as being let off the hook. Consequently, they are informing executives that we are entering a new world of lower bonuses, less risk-taking and smaller profits.

Rather than the “green shoots” of recovery suggested by business minister Baroness Vadera on Wednesday, the Government has to be prepared to come out with more bleak news.

RBS, until a year and a half ago Britain’s biggest banking success story, is now almost 60 per cent owned by the taxpayer and in its present state is essentially finished as a private institution. The problems at HBOS, comprised of Halifax and Bank of Scotland, are greater than anticipated, and its new owner – Lloyds TSB – will struggle to cope unless it receives more help from the public purse.

Northern Rock, which the Government had hoped to flip from its nationalised state back to the private sector for a quick profit, now looks like the most sensible home for the bad bank and so will have to spend many years in public hands.

And Barclays, the only major high street bank apart from HSBC to avoid participating in the October bail-out, looks increasingly as if it will have to accept government cash, either by using the bad bank or by being involved in a potential further round of cash injections into the banking sector.

It is not all doom and gloom. The Government can make a reasonable case that it is more sensible to create a bad bank than to inject more cash straight into banks, as the investments could simply be wiped out.

This would lead to complete nationalisation of the banking sector, which the Government is unwilling to do until it has tried other measures first.

But a bad bank alone will not kick-start the economy. The Government must get to work with other countries to rethink the “Basle II” banking rules that dictate how institutions lend. They contributed to the banks’ lending bubble, rather than preventing it, by enabling them to place large amounts of new types of debt off balance sheets and beyond the reach of regulators.

And it is clear that in Britain, the tweaks to VAT were inadequate: more tax cuts are required fast.

It is not difficult to see why ministers have taken their time: many, along with their advisers, have not lived through difficult economic times. While the Government had to react quickly last year to a succession of blow-ups, it says it now wants to get its policy right for the longer term.

To do otherwise will lead to lawsuits, such as the one going through the courts over Northern Rock’s nationalisation.

More importantly, spending billions of pounds more of taxpayers’ money on a policy that fails to hit the mark would be disastrous.

The Government has the critical next stage of its rescue of the banking system close to completion. An announcement is expected as early as next week.

All of us, consumers and bankers, had better hope it works.

http://www.telegraph.co.uk/finance/financetopics/recession/4250231/Financial-crisis-The-banks-are-still-sinking.html

Comment:

This is akin to Danaharta and Danamodal approach adopted by Malaysia in 1997-1998 Asian Financial Crisis.

Ministers plan a 'toxic bank’ to soak up bad debts and unfreeze the money markets. But will it work, asks Katherine Griffiths.

Last Updated: 12:08PM GMT 16 Jan 2009

Comments 9 Comment on this article

Hang on – didn’t we save Britain’s banks in October? That was when the Government gave £500 billion to inject capital into Royal Bank of Scotland (RBS), Lloyds and HBOS and pledged ongoing support to get high-street lenders back on their feet.

So, why are banks’ share prices still plummeting, while they refuse to lend to each other because they are suspicious about what hidden nasties are on their rivals’ balance sheets? Their chief executives privately warn the Government – they are reluctant to deliver this message in public – that they do not have the cash to provide mortgages and loans to individuals and businesses.

The reality is that, while the Prime Minister, the self-styled saviour of the world, rode high in public opinion in October and November for leading the charge to deal with the global banking crisis, in fact what the Government had done was to carry out emergency surgery to save the banks – and the entire financial system – from immediate collapse.

Now it is time for the more painful process of restoring the patient to health. For the banks the medicine is going to be unpleasant to swallow – it will mean shrunken salaries and no bonuses for many. For the rest of us it is going to be expensive and could take years to administer.

The Government is understandably unwilling to come out with this prognosis, but it needs to do so soon. The US has been ahead of Britain in preparing for a second round of emergency operations on its banks, with Citigroup set to be split into a “good” and “bad” bank so that investors can feel confident about owning its shares again.

Switzerland has also set up a special entity to swallow about £30 billion of toxic assets from its largest bank, UBS, so that it can begin the process of recovery.

In the UK, we have seen this week measures from Lord Mandelson’s department to help small businesses, but they will only have a marginal impact unless ministers can deal with the banking disease at the heart of the problem.

Now, the word out of Downing Street is that ministers are on the case and are preparing to announce the creation of a “toxic bank” to soak up more than £30 billion of British banks’ bad debts. The plan will form the centrepiece of a fresh bail-out designed to get them lending again, to each other and to their customers.

The difficulties the Government faces are immense.

The wholesale markets, which banks use for much of their funding so that they can lend to customers, remain frozen. This is because of a breakdown of trust between financial institutions: no one can be sure what problems banks are sitting on, so investors do not want to lend them money in case more difficulties emerge and they lose their cash.

What is needed most is clarity: what really is on the books of each bank? It is difficult to put a price on their troubled assets, many of which are based on the collapsed subprime loans sector in the US.

The Government is hoping that clarity is coming soon. In the next few weeks, the banks will report their results for 2008, and to do so they need to get their figures signed off by auditors. The auditing firms – such as PricewaterhouseCoopers, KPMG and Deloitte – will have to agree to the valuation of banks’ assets.

The accountants will want to get these values right because, if their banking clients should fail later, the first port of call for potential shareholders’ lawsuits will be the deep-pocketed auditors.

In anticipation, ministers are preparing the creation of that “toxic bank” to allow for a fresh start.

In theory, it will suck in all of the failing assets that have poisoned the banks’ balance sheets and destroyed confidence in the system. That would leave the remaining banks cleansed and able to attract both investors who want to put their capital in banks’ shares, and providers of funds so that the wholesale markets would be defrosted, and lending could be restarted.

Of course, if it was as simple as that, a bad bank would have been constituted months ago and Gordon Brown and Alistair Darling would be hailing it as part of their world-leading financial recovery plan.

As Sweden found when it had to take similar measures in the early Nineties, creating a bad bank is fraught with problems. As with this entire crisis, the main challenge is how to value the assets.

In order to take control of the toxic investments, the Government would have to give the banks some money in return.

If it sets the price too low, banks will either refuse to hand the assets over, thereby not solving the systemic problem of a lack of confidence, or will have to take new write-downs to recognise the lower value, further weakening their own books. If the price is too high, there will be an outcry that taxpayers’ money is being squandered to save bankers’ skins.

Ministers are keen to ensure that banks are not seen by the public as being let off the hook. Consequently, they are informing executives that we are entering a new world of lower bonuses, less risk-taking and smaller profits.

Rather than the “green shoots” of recovery suggested by business minister Baroness Vadera on Wednesday, the Government has to be prepared to come out with more bleak news.

RBS, until a year and a half ago Britain’s biggest banking success story, is now almost 60 per cent owned by the taxpayer and in its present state is essentially finished as a private institution. The problems at HBOS, comprised of Halifax and Bank of Scotland, are greater than anticipated, and its new owner – Lloyds TSB – will struggle to cope unless it receives more help from the public purse.

Northern Rock, which the Government had hoped to flip from its nationalised state back to the private sector for a quick profit, now looks like the most sensible home for the bad bank and so will have to spend many years in public hands.

And Barclays, the only major high street bank apart from HSBC to avoid participating in the October bail-out, looks increasingly as if it will have to accept government cash, either by using the bad bank or by being involved in a potential further round of cash injections into the banking sector.

It is not all doom and gloom. The Government can make a reasonable case that it is more sensible to create a bad bank than to inject more cash straight into banks, as the investments could simply be wiped out.

This would lead to complete nationalisation of the banking sector, which the Government is unwilling to do until it has tried other measures first.

But a bad bank alone will not kick-start the economy. The Government must get to work with other countries to rethink the “Basle II” banking rules that dictate how institutions lend. They contributed to the banks’ lending bubble, rather than preventing it, by enabling them to place large amounts of new types of debt off balance sheets and beyond the reach of regulators.

And it is clear that in Britain, the tweaks to VAT were inadequate: more tax cuts are required fast.

It is not difficult to see why ministers have taken their time: many, along with their advisers, have not lived through difficult economic times. While the Government had to react quickly last year to a succession of blow-ups, it says it now wants to get its policy right for the longer term.

To do otherwise will lead to lawsuits, such as the one going through the courts over Northern Rock’s nationalisation.

More importantly, spending billions of pounds more of taxpayers’ money on a policy that fails to hit the mark would be disastrous.

The Government has the critical next stage of its rescue of the banking system close to completion. An announcement is expected as early as next week.

All of us, consumers and bankers, had better hope it works.

http://www.telegraph.co.uk/finance/financetopics/recession/4250231/Financial-crisis-The-banks-are-still-sinking.html

Comment:

This is akin to Danaharta and Danamodal approach adopted by Malaysia in 1997-1998 Asian Financial Crisis.

Using PE as a Guide

http://samltt88.blogspot.com/2008/12/v-thats-y-d-chinese-said-d-length-of.html

Sam, I am a silent reader of seng's blog & also your blog , I found that they are confuse with which PE to use for shares picking, mind to teach us which one to be used?

thanks in advance

Read the below:

random: and which PE should we use bb? TTM PE? Last year's PE? Forward PE? 10 Dec 07, 10:46

sasuka: andy.. I doubt syndicate will play the market... so just look at good timing 2 enter... 10 Dec 07, 10:46

random: even the PE stated on my HLE screen is sometimes wrong.. 10 Dec 07, 10:45

bullbear: For example, the simple PE. PE of KNM is quoted at around 27 in the Star, in the Financial edge it is 47. The price is the same, so the calculation of PE was definitely based on different EPS used by these 2 sites. This can be confusing for the average investors.

***First of all, who is seng ? Which blog u r referring to?

From d above posting, I can see some of them don’t 100% understand what is PE?

That's y Chinese said: - d length of our fingers r not d same, means: - why some one can be Doctor, lawyer, successful investor n bizman...N why some cant???

Why some can be rich n some r so poor?

Why same effort n guidance given by u but not all of them can be graduate?

As known to u , everyone know who is Warren Buffet N Benjamin Graham, n most of them read their investment skill n method also, why some can be so successful n some r so broke ?

Bcos:-D Length of our fingers r not d same! Some r smart some r not!

U know d formula of PE doesn’t mean u know what is PE!

U know what is PE doesn’t mean u understand what is PE!

U understand what is PE doesn’t mean u know how to apply it on share investment!

Why should u follow d press n broking hse’s PE when they r not d same? (this show they r either don’t understand or may be don’t know how to calculate PE )

Do it yrself by calculate its PE based on its earning lah ! what so difficult ?

Why there r differences of PE ? simple ! Some broking hse calculate based on last year earning, some calculate based on 1 or 2 or 3 qtrs earning !

of course they r different lah !

So which one to use ?

Last year PE take it as a guide, use current earning to estimate its PE for d coming year !

Example :

Last year PE giving u 8

If I see its Qtr earning improving ( minus out d one off earning if there any ) n its future earning looks bright ( Steel sector n oil sector ) , I am quite sure d PE for d coming year will definitely better or lower than last year ^V^

Masteel at 1.51

Based on last year earning of 22.47

PE = 1.51/22.47 = 6.7

Based current earning (3 Qtrs only )= 23.32 cts

PE = 1.51/23.32 = 6.4

BUT dont forget, PE 6.4 is based on 3 QTRS only !!

there is one more to come , therefore , we can expect lower n better PE for Masteel in year ended 2007 !

What is so difficult to get its PE yrself ?D

Do u know how to define mkt crash like 1997 n 1998 ? Mkt crash is when u can buy d below blue chips at PE < 10 :-

PBB , PPB, Maybank, IOIcorp, YTL, Genting , Digi ,SD , IJM , KNM ,Resorts.....

Once u can get d above blue chips at below PE 10, then u will understand better what actually PE is !?

Is low PE guaranteed u sure gain ? refer to my previous posting at :-

http://samgang.blogspot.com/2007/12/v-portfolio-as-at-30-nov-07-v.html

Posted by Samgoss at 7:54 PM

Comment:

Copied an old posting from the above blog to illustrate how PE is being used by this blogger. It is good of Samgoss to share this.

PE is only one of many market metrics one look at as a guide to investing in shares.

Also read:

Market metrics P/E and Intrinsic value

Sam, I am a silent reader of seng's blog & also your blog , I found that they are confuse with which PE to use for shares picking, mind to teach us which one to be used?

thanks in advance

Read the below:

random: and which PE should we use bb? TTM PE? Last year's PE? Forward PE? 10 Dec 07, 10:46

sasuka: andy.. I doubt syndicate will play the market... so just look at good timing 2 enter... 10 Dec 07, 10:46

random: even the PE stated on my HLE screen is sometimes wrong.. 10 Dec 07, 10:45

bullbear: For example, the simple PE. PE of KNM is quoted at around 27 in the Star, in the Financial edge it is 47. The price is the same, so the calculation of PE was definitely based on different EPS used by these 2 sites. This can be confusing for the average investors.

***First of all, who is seng ? Which blog u r referring to?

From d above posting, I can see some of them don’t 100% understand what is PE?

That's y Chinese said: - d length of our fingers r not d same, means: - why some one can be Doctor, lawyer, successful investor n bizman...N why some cant???

Why some can be rich n some r so poor?

Why same effort n guidance given by u but not all of them can be graduate?

As known to u , everyone know who is Warren Buffet N Benjamin Graham, n most of them read their investment skill n method also, why some can be so successful n some r so broke ?

Bcos:-D Length of our fingers r not d same! Some r smart some r not!

U know d formula of PE doesn’t mean u know what is PE!

U know what is PE doesn’t mean u understand what is PE!

U understand what is PE doesn’t mean u know how to apply it on share investment!

Why should u follow d press n broking hse’s PE when they r not d same? (this show they r either don’t understand or may be don’t know how to calculate PE )

Do it yrself by calculate its PE based on its earning lah ! what so difficult ?

Why there r differences of PE ? simple ! Some broking hse calculate based on last year earning, some calculate based on 1 or 2 or 3 qtrs earning !

of course they r different lah !

So which one to use ?

Last year PE take it as a guide, use current earning to estimate its PE for d coming year !

Example :

Last year PE giving u 8

If I see its Qtr earning improving ( minus out d one off earning if there any ) n its future earning looks bright ( Steel sector n oil sector ) , I am quite sure d PE for d coming year will definitely better or lower than last year ^V^

Masteel at 1.51

Based on last year earning of 22.47

PE = 1.51/22.47 = 6.7

Based current earning (3 Qtrs only )= 23.32 cts

PE = 1.51/23.32 = 6.4

BUT dont forget, PE 6.4 is based on 3 QTRS only !!

there is one more to come , therefore , we can expect lower n better PE for Masteel in year ended 2007 !

What is so difficult to get its PE yrself ?D

Do u know how to define mkt crash like 1997 n 1998 ? Mkt crash is when u can buy d below blue chips at PE < 10 :-

PBB , PPB, Maybank, IOIcorp, YTL, Genting , Digi ,SD , IJM , KNM ,Resorts.....

Once u can get d above blue chips at below PE 10, then u will understand better what actually PE is !?

Is low PE guaranteed u sure gain ? refer to my previous posting at :-

http://samgang.blogspot.com/2007/12/v-portfolio-as-at-30-nov-07-v.html

Posted by Samgoss at 7:54 PM

Comment:

Copied an old posting from the above blog to illustrate how PE is being used by this blogger. It is good of Samgoss to share this.

PE is only one of many market metrics one look at as a guide to investing in shares.

Also read:

Market metrics P/E and Intrinsic value

Country risk - Emerging economies caught in the storm

Country risk - Emerging economies caught in the storm

<<

- The global crisis is affecting emerging country risk

- The crisis has revealed their vulnerabilities, but with contrasting situations

- Analysis of risk in Russia, Turkey and India >>

Some countries are in a better position than others to face the crisis. Some countries have resources and structures that offer more shelter from the global crisis: Singapore (rated AA), Chile (A), Czech Republic (A), HongKong (A), Malaysia (A), Slovenia (A), Taiwan (A), Bahrain (BB), Botswana (BB),Brazil (BB), Israel (BB), South Korea (BB), Kuwait (BB), Mexico (BB), Oman(BB), Poland (BB), Qatar (BB), Saudi Arabia (BB), Slovakia (BB), South Africa(BB), Thailand (BB) and Tunisia (BB).

PARIS, Jan. 15 /CNW Telbec/ -

Euler Hermes has published its analysis of country risk in a global economic crisis. Country risk takes on another dimension in a recessionary environment. Emerging countries are faced with dwindling sources of external financing, the recession of the major economies and falling commodities prices. These difficulties have been exacerbated by bank liquidity problems, volatile exchange rates and the withdrawal of foreign capital. These economies' weaknesses, less visible during growth periods, have resurfaced. Countries that seemed perfectly safe a short while ago now represent a risk for the companies that do business with them.

Against this backdrop, Euler Hermes Country Risk Analyst David Atkinson said: "The present economic crisis is affecting all countries, with no exception. Although some countries are in a better position to resist the crisis, many are experiencing a rapid deterioration in their situation. It is essential that trade partners and exporters keep a close watch on these countries, on the reforms implemented and on future trends".

Emerging economies are slowing

Euler Hermes is forecasting growth of less than 1% for the global economy in 2009 with the large developed economies experiencing their first recession since World War II. At the same time, emerging economies are being severely hurt by a world crisis that does not correspond to a normal economic cycle.

The decoupling theory, whereby emerging economies would continue to grow, has

been largely invalidated. These countries now face numerous problems:

<< - Wide-scale withdrawal of foreign investment

- Drop in exports

- Tumbling commodities prices (oil, etc.)

Against this difficult background, Euler Hermes expects economic growth to slow sharply in emerging countries.

-----------------------------------------------------

Regional real GDP 2003-2006/ 2007/ 2008/ 2009

(% change) annual Euler Hermes Euler Hermes

average projections projections

-------------------------------------------------------------------------

Emerging Europe 6.8/ 7.0/ 5.4/ 2.0

-------------------------------------------------------------------------

Russia 7.1/ 8.1/ 6.1/ 1.5

-------------------------------------------------------------------------

Turkey 7.5/ 4.5/ 2.3/ 1.0

-------------------------------------------------------------------------

Emerging Asia 8.4/ 9.2/ 7.1/ 5.0

-------------------------------------------------------------------------

China 10.5/ 11.9/ 9.2/ 7.0

-------------------------------------------------------------------------

India 8.7/ 9.0/ 7.0/ 5.0

-------------------------------------------------------------------------

Latin America 4.6/ 5.5/ 4.6/ 1.9

-------------------------------------------------------------------------

Brazil 3.4/ 5.1/ 5.5/ 2.3

-------------------------------------------------------------------------

Mexico 3.3/ 3.3/ 2.0/ 0.0

-------------------------------------------------------------------------

Middle East & Africa 5.8/ 5.7/ 5.9/ 4.6

-------------------------------------------------------------------------

A growing number of high-risk countries

The overall trend in the risk ratings assigned by Euler Hermes to each country (see methodology) reflects the general trend in risk of international trade. With the risk ratings of 16 countries downgraded in 2008, international trade has entered a more turbulent period.

---------------------------

Net Country Grade Changes

---------------------------

2000 -1

2001 -5

2002 -8

2003 +3

2004 +11

2005 +1

2006 -1

2007 +3

2008 -16

---------------------------

At the individual level, each country's rating reflects its sensitivity to a downturn in its environment and its capacity to stand firm. In the present conditions, individual country risk ratings can change rapidly and should therefore be monitored closely by exporters and their partners. Since the economic crisis worsened, Euler Hermes has downgraded the country risk ratings of eleven countries:

----------------------------------

Grade Change

----------------------------------

South Korea A to BB

----------------------------------

Hungary B to C

----------------------------------

Romania B to C

----------------------------------

Bulgaria B to C

----------------------------------

Lithuania B to C

----------------------------------

Guatemala B to C

----------------------------------

Jordan B to C

----------------------------------

Iceland A to D

----------------------------------

Argentina C to D

----------------------------------

Pakistan C to D

----------------------------------

Vietnam C to D

----------------------------------

Euler Hermes has identified a group of more vulnerable countries:

- With a C rating: Hungary, Romania, Russia, Turkey, Lithuania, Bulgaria, Latvia, Kazakhstan, Indonesia, Dominican Republic, Honduras and Jamaica

- With a D rating: Iceland, Ukraine, Serbia, Bosnia Herzegovina, Vietnam, Argentina, Venezuela, Ecuador, Kenya, Lebanon and Pakistan

>>

Some countries are in a better position than others to face the crisis:

Some countries have resources and structures that offer more shelter from the global crisis: Singapore (rated AA), Chile (A), Czech Republic (A), Hong Kong (A), Malaysia (A), Slovenia (A), Taiwan (A), Bahrain (BB), Botswana (BB), Brazil (BB), Israel (BB), South Korea (BB), Kuwait (BB), Mexico (BB), Oman (BB), Poland (BB), Qatar (BB), Saudi Arabia (BB), Slovakia (BB), South Africa (BB), Thailand (BB) and Tunisia (BB).

Russia: liquidity crunch and tumbling oil prices

Russia's economic growth is expected to slow significantly, from 6.1% in 2008 to 1.5% in 2009 according to Euler Hermes estimates, after several strong years (7.4% in 2006 and 8.1% in 2007).

The rapid slowdown was visible in the fourth quarter of 2008 with a very sharp fall in industrial production.

The business slowdown has been accompanied by a slump in the share prices of listed Russian companies (down 70% in six months) and the weakening of the rouble, down 13% against the dollar, despite heavy intervention.

Foreign exchange reserves have decreased by more than 25% since August 2008 and the fall in the price of oil will have a significant impact on the fiscal and external current account balances.

Euler Hermes has left its C rating unchanged but notes the risks from banking and corporate foreign exchange illiquidity and lower oil prices.

Turkey: strong inflation and low foreign exchange reserves

Turkey's economic growth has slowed significantly since 2007 (6.9% in 2006, 4.5% in 2007). Euler Hermes is expecting economic growth to stand at 2.3% in 2008 and fall to 1.0% in 2009.

Inflation remains relatively high. Euler Hermes estimates that the inflation rate will have risen to 10.1% in 2008 and remain at a similar level in 2009 (10%).

The large current account deficit and reliance on short time capital flows is a key vulnerability and the Turkish Lira has fallen sharply.

Foreign exchange reserves have also fallen but currently still cover 3.5 months of imports, though only 60% of external debt due in 2009.

Euler Hermes has left its C rating unchanged but is closely monitoring the situation, including developments with regards to the IMF programme currently under discussion.

India: substantial foreign exchange reserves but limited possibilities

India recorded a sharp downturn in industrial activity in the fourth quarter of 2008.

The banking sector has been relatively sheltered from the global financial crisis directly though credit conditions have tightened noticeably.

The Indian stock market and exchange rates have also been affected. Economic growth has slowed significantly but remains relatively high in the global context (7.0% in 2008 and 5.0% in 2009 according to Euler Hermes forecasts).

Government support for the currency have significantly decreased into foreign exchange reserves but these still cover seven months of imports and the total stock of external debt.

However, the size of the fiscal deficit considerably constraints government action to offset the slowdown in economic activity.

Euler Hermes has maintained its B rating. Regional and political uncertainties will also need to be monitored.

#################################

Technical details

Methodology

Euler Hermes assigns each country a risk rating that reflects thecountry's economic and political risk. The economic factors taken into accountare the macroeconomic indicators (indebtedness, fiscal deficit, etc) andinstitutional and structural factors. The political factors taken into accountare the efficiency and stability of the political system in place. Thecombination of these two types of indicators are reflected in a rating - AA,A, BB, B, C or D; AA is the strongest rating. This classification constitutesa first filter for any credit limit request and influences the terms andconditions of cover extended by Euler Hermes.

Euler Hermes country risk analysis

Euler Hermes country risk analysisThree Euler Hermes specialists, two in London and one in Hamburg, arededicated to country risk. A country risk committee, which also includesrepresentative of group subsidiaries, meets every two months. The country riskspecialists' work is published in a weekly bulletin. Any change in a country'srisk results in an immediate, ad hoc review.

David Atkinson is one of Euler Hermes' three country risk analysts. Hejoined the group in 1999 and and has established a Group-wide framework forcountry risk analysis. Previously, David spent twenty-five years ininternational banking as an emerging markets and country risk analyst,specialising in Latin America, Eastern and Southern Europe and East Asiaincluding China. David is based in the United Kingdom and holds a degree inEconomics from the University of Nottingham.

-------------------------------------------------------------------------

Euler Hermes is the worldwide leader in credit insurance and one of theleaders in the areas of bonding, guarantees and collections. With 6,000employees in over 50 countries, Euler Hermes offers a complete range ofservices for the management of B-to-B trade receivables and posted aconsolidated turnover of (euro) 2.1 billion in 2007.

Euler Hermes has developed a credit intelligence network that enables itto analyse the financial stability of 40 million businesses across theglobe. The group protectsworldwide business transactions totalling(euro) 800 billion.

Euler Hermes, subsidiary of AGF and a member of the Allianz group, islisted on Euronext Paris. The group and its principal credit insurancesubsidiaries are rated AA- by Standard & Poor's. http://www.eulerhermes.com/

-------------------------------------------------------------------------

These assessments are, as always, subject to the disclaimer provided below.

Cautionary Note Regarding Forward-Looking Statements: Certain of thestatements contained herein may be statements of future expectations and otherforward-looking statements that are based on management's current views andassumptions and involve known and unknown risks and uncertainties that couldcause actual results, performance or events to differ materially from thoseexpressed or implied in such statements. In addition to statements which areforward-looking by reason of context, the words "may, will, should, expects,plans, intends, anticipates, believes, estimates, predicts, potential, orcontinue" and similar expressions identify forward-looking statements. Actualresults, performance or events may differ materially from those in suchstatements due to, without limitation, (i) general economic conditions,including in particular economic conditions in the Allianz SE's core businessand core markets, (ii) performance of financial markets, including emergingmarkets, (iii) the frequency and severity of insured loss events, (iv)mortality and morbidity levels and trends, (v) persistency levels, (vi) theextent of credit defaults (vii) interest rate levels, (viii) currency exchangerates including the Euro-U.S. Dollar exchange rate, (ix) changing levels ofcompetition, (*) changes in laws and regulations, including monetary convergenceand the European Monetary Union, (xi) changes in the policies of central banksand/or foreign governments, (xii) the impact of acquisitions, includingrelated integration issues, (xiii) reorganization measures and (xiv) generalcompetitive factors, in each case on a local, regional, national and/or globalbasis. Many of these factors may be more likely to occur, or more pronounced,as a result of terrorist activities and their consequences. The mattersdiscussed herein may also involve risks and uncertainties described from timeto time in Allianz SE's filings with the U.S. Securities and ExchangeCommission. The Group assumes no obligation to update any forward-lookinginformation contained herein.

For further information: Press relations/Euler Hermes group: Raphaele Hamel, +33 (0)1 4070 8133, raphaele.hamel@eulerhermes.com; Agence Rumeur Publique: Salima Ait Meziane, +33 (0)1 5574 5223, salima@rumeurpublique.fr

EULER HERMES CANADA - More on this organization

http://www.newswire.ca/en/releases/archive/January2009/15/c8011.html

<<

- The global crisis is affecting emerging country risk

- The crisis has revealed their vulnerabilities, but with contrasting situations

- Analysis of risk in Russia, Turkey and India >>

Some countries are in a better position than others to face the crisis. Some countries have resources and structures that offer more shelter from the global crisis: Singapore (rated AA), Chile (A), Czech Republic (A), HongKong (A), Malaysia (A), Slovenia (A), Taiwan (A), Bahrain (BB), Botswana (BB),Brazil (BB), Israel (BB), South Korea (BB), Kuwait (BB), Mexico (BB), Oman(BB), Poland (BB), Qatar (BB), Saudi Arabia (BB), Slovakia (BB), South Africa(BB), Thailand (BB) and Tunisia (BB).

PARIS, Jan. 15 /CNW Telbec/ -

Euler Hermes has published its analysis of country risk in a global economic crisis. Country risk takes on another dimension in a recessionary environment. Emerging countries are faced with dwindling sources of external financing, the recession of the major economies and falling commodities prices. These difficulties have been exacerbated by bank liquidity problems, volatile exchange rates and the withdrawal of foreign capital. These economies' weaknesses, less visible during growth periods, have resurfaced. Countries that seemed perfectly safe a short while ago now represent a risk for the companies that do business with them.

Against this backdrop, Euler Hermes Country Risk Analyst David Atkinson said: "The present economic crisis is affecting all countries, with no exception. Although some countries are in a better position to resist the crisis, many are experiencing a rapid deterioration in their situation. It is essential that trade partners and exporters keep a close watch on these countries, on the reforms implemented and on future trends".

Emerging economies are slowing