| Dividend discussion, Dec. 6, 2002 |

GEOFF COLVIN: Today’s news from Washingtonhas got investors focusing on dividends like they haven’t in a very long time. To get us up to speed – fast – we’ve got a couple of experts on the subject. James Bianco is president of Bianco Research in Chicago. He’s done some fascinating research on when dividends are and are not good for investors. Gail Dudack is chief investment strategist at Sungard Institutional Brokerage in New York City, and she’s been arguing for months that dividend-paying stocks are the place to be. And so far this year she has been very right. Jim and Gail, thanks so much for being with us.

GAIL DUDACK: Great to be here.

COLVIN: Gail, forgetting about whether there’s a change in the tax on dividends, you’ve been arguing for a long time that stocks that pay dividends are the place to invest. How come?

DUDACK: There’s a lot of reasons, but there’s one simple one for the current environment, which is we’re going to be in a slower growth environment, in terms of GDP growth, because of all the debt load. And if that’s true, then earnings will be harder to come by, and if that’s true, they’ll probably grow maybe 5 to 7 percent. If you can get a 3 percent dividend yield in your portfolio, you’re halfway there. You’re likely to outperform.

DUDACK: There’s a lot of reasons, but there’s one simple one for the current environment, which is we’re going to be in a slower growth environment, in terms of GDP growth, because of all the debt load. And if that’s true, then earnings will be harder to come by, and if that’s true, they’ll probably grow maybe 5 to 7 percent. If you can get a 3 percent dividend yield in your portfolio, you’re halfway there. You’re likely to outperform.COLVIN: But you know the argument against dividends, which is that if the companies just kept the money, reinvested it, they could make the stock price go up more, and investors wouldn’t be taxed when they get the dividends. You don’t buy it?

DUDACK: I don’t buy that, because if you’re in a slow-growth environment, there are few places you can get that required rate of return. So companies are buying back their own shares. However, that’s been kind of the spin of the ‘90s, because what did all those share buy backs bring investors in the last few years? Very little. Wouldn’t they have rather had the check in the mail than those stock repurchases? I think so.

COLVIN: Especially over the past 2 ½ or 3 years, they would for sure. Jim, you’ve done some looking into when dividend-paying stocks have been a good investment and when they haven’t. And what did you find?

JAMES BIANCO: What we found is that dividend-paying stocks is an investment theme that seems to work well with the direction of the market.

COLVIN: Meaning?

BIANCO: Meaning that when the stock market goes up, non-dividend-paying stocks do better; when the stock market goes down, dividend-paying stocks do better. So one of the over-arching themes in whether or not you want to invest in dividends is your belief in which way the market’s going to go. If it’s going to go down, you want to invest in dividend stocks; if it’s going to go up, you don’t want to invest in dividend stocks.

BIANCO: Meaning that when the stock market goes up, non-dividend-paying stocks do better; when the stock market goes down, dividend-paying stocks do better. So one of the over-arching themes in whether or not you want to invest in dividends is your belief in which way the market’s going to go. If it’s going to go down, you want to invest in dividend stocks; if it’s going to go up, you don’t want to invest in dividend stocks.COLVIN: And what do you believe?

BIANCO: I think that after 2 ½ years, the market has found some kind of an important low in October. I think it’s going to rally for the next several months, maybe a year. Maybe it’s not going to make a new high. I doubt it’s even going to make halfway towards erasing the losses it had, maybe get to S&P 1200. And if that’s true and the market does do better for the next several months, I think that non-dividend-paying stocks are going to lead that charge.

COLVIN: Okay. Interesting, because it’s not quite the same as what Gail has been saying. Let’s take a step back and look at the longer term, the bigger picture. Dividends have really been going out of fashion for the past 20 years, right?

DUDACK: That’s true.

COLVIN: And I think we have some information on this showing that the number of companies paying dividends has decreased from almost all of them in 1980, 93.8%, paying a pretty fat yield at that time, 5.9, till today only 70% are paying dividends, and the yield is tiny, 1.6%

DUDACK: Historic low.

COLVIN: Historic low. Is that an opportunity?

DUDACK: It’s an opportunity for companies to start picking up their dividends and for investors to start looking for some. I think one of the most important points here is that investors understand that stocks are the best performing asset class, but they don’t understand why. It’s because they have capital gains and dividends. And so the aftermath of the ‘90s shows that stocks don’t always perform. In fact, in the bear market the high-yielding stocks are the best performers.

COLVIN: Well, and in fact we can see that in a graphic we have also which says that – I think this is year-to-date – so far companies that didn’t pay dividends declined much further than companies that did pay dividends. And, Jim, that’s consistent with your observation over a longer period of time.

BIANCO: That is true. And if you actually were to break down this year’s activity between dividend and non-dividend-paying stocks, you’d find that dividend-paying stocks outperformed non-dividend-paying stocks until about August of this year, and then they started to kind of perform in line. And since the October low, they’ve been really outperforming. So the non-dividend–paying stocks have been leading the charge for the last two months.

COLVIN: Well, now this really then gets to a bigger question of what you think the big picture of the market’s future is. Jim, you’ve told us. Gail, you were prescient on this fact a few years ago when you said, you turned bearish. You took heat for it. You were right. What do you think now?

DUDACK: Well, I think we’re in the final stages of the bear. The bull, the transition from a bear to a bull does not happen like that. It’s a transition. So I’ve been saying all year that 2002 is the transition from bear to bull. I now think the transition is going to be pushed out into 2003. The reason being earnings were a huge disappointment. And until the momentum improves, we’re still in this process. I think we may retest these lows, and that’s a contrarian view right now.

DUDACK: Well, I think we’re in the final stages of the bear. The bull, the transition from a bear to a bull does not happen like that. It’s a transition. So I’ve been saying all year that 2002 is the transition from bear to bull. I now think the transition is going to be pushed out into 2003. The reason being earnings were a huge disappointment. And until the momentum improves, we’re still in this process. I think we may retest these lows, and that’s a contrarian view right now.COLVIN: Yeah, it is indeed. And longer term, Jim, are you optimistic or pessimistic? You’ve spoken only so far about the next year or so.

BIANCO: Yeah, longer term, if you can look out three, four, five years, I’m not that optimistic. I do think that after, like I said, 2 ½ years of going down, we’ve got a period where the market could rally. I believe the rally started in October. But after we go up maybe 20 percent or so over the next year or year and a half, if that pans out, I think the market’s then ready to start back down again and may test the lows.

Is the big bear market that started in 2000 over? No. We’re ready for maybe a cyclical bull market or a cyclical correction that could last many months where the market’s going to rally, and (after) that is where I meant going (back) down again.

COLVIN: Gotcha. Gail, let’s think about finding stocks that pay dividends. There’s still an awful lot of them out there and you want to choose only particular ones. How do you choose them?

DUDACK: Well, I think it’s important to kind of look, to use some filters, to look for dividends that are greater than inflation, because right then you’re going to have, and inflation’s pretty low, let’s say 2 percent. And then to look for stocks that have pay-out ratios, they’re not paying out more than 70 percent of their earnings. And then you want to look for companies that still have improving profit margins. So you’re looking for good companies with above average dividends, the dividend in line with or above the inflation rate.

COLVIN: And when you run these screens, what kind of companies do you end up with?

DUDACK: Well, when I run the screens, at the top, the high-paying dividends are always the ones that you really have to check out very carefully. You get a pretty low number from the S&P really of companies. And then I look for other things that I like. I like to see companies that have increased their dividend every quarter or every year for the last 10 years. That shows to me that they have a very good business plan.

DUDACK: Well, when I run the screens, at the top, the high-paying dividends are always the ones that you really have to check out very carefully. You get a pretty low number from the S&P really of companies. And then I look for other things that I like. I like to see companies that have increased their dividend every quarter or every year for the last 10 years. That shows to me that they have a very good business plan.COLVIN: Like who?

DUDACK: Well, there are companies that have done that like Exxon Mobil has done that. They’ve increased their dividend more than the rate of inflation every year. Johnson & Johnson has done that. Kellogg has done that. (My comment: Interestingly, these are in Warren Buffett's portfolio.)

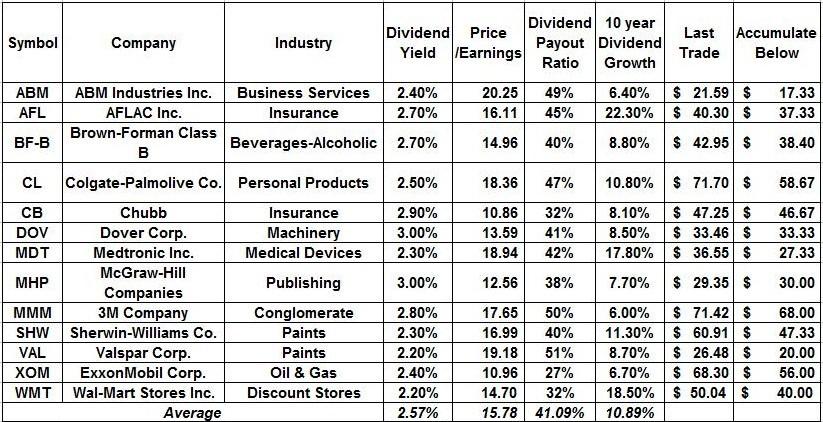

COLVIN: Interesting. Now you mentioned a minute ago those that have really high yields, and those may be more dangerous than they are attractive. What are some of those? I think we have some of them on a graphic also.

DUDACK: I think you have some on a graphic. The one thing I would say is that when you start to get very high dividend yields, it’s probably because the stock price has collapsed because of some event which needs to be checked into. And so you have to be very careful. And you also want to – this is where the screen is important – make sure that their dividend is not more than their earnings. So take a look at that payout ratio.

COLVIN: Interesting. We only have a few seconds left, but I wanted to get one other view, Jim, because I know you have a thought about bonds. We hear a lot of talk. What do you think investors should be doing?

BIANCO: Bonds are at this point in 2002 the opposite of the stock market. They bottomed in yield the same day the stock market bottomed. They should be the opposite of your view. I think the stock market’s going to rally, that means that yields are probably going to head higher.

Bonds should be avoided. If you have the view that the stock market’s going to go down, bonds will probably do very well. So they’re kind of an anti-stock is really what they are, and they should be viewed as that.

COLVIN: Jim and Gail, thanks so much for being with us.

![[AztechDividends.gif]](https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEjuXvHz5aR0PCJ-ldWIUjWLqK-qKJdYngRmE2R5VBCMslLTIdOFDxH71ORZo6vAPdwkNiJefLBN0AMSAB71QUKDRAYf0vy92MYLM5fPKelWKegX3TKpoRdyMKb1qNpvktOxY5xXJ6ywXDzo/s640/AztechDividends.gif)