Summary

- Ferragamo has a strong positioning on the Premium segment and a diversified profile.

- The Italian company is well positioned to benefit from all the major growth engines of the luxury industry in the upcoming years.

- Ferragamo announced increasing revenues and improving margins for 2013.

Overview and 2013 results

Salvatore Ferragamo Group (OTC:SFRGF)(OTCPK:SFRGY) is an Italian luxury goods company that was founded in 1928 by Salvatore Ferragamo in Florence focusing on ladies' footwear. The group operates now worldwide through more than 600 mono-brand stores and employs more than 3,000 collaborators. The company specializes in footwear, leather goods, ready-to-wear, accessories and perfumes. Ferragamo went public in June 2011 and is listed in the Milan stock exchange. The company has a premium positioning and a strong brand image, which makes it possible to target High net worth individuals, generate increasing revenues worldwide and resist to slower economies.

Ferragamo published strong 2013 results with improving revenues and margins:

€m

|

2013

|

2012

|

Variation (%)

|

Revenues

|

1,258

|

1,153

|

9.1

|

EBITDA

|

260

|

228

|

13.9

|

EBITDA margin (%)

|

20.7

|

19.8

|

n/a

|

EBIT

|

219

|

194

|

12.8

|

EBIT margin (%)

|

17.4

|

16.9

|

n/a

|

Net income

|

160

|

125

|

27.7

|

Source: Financial report

The debt profile also improved as net debt decreased by 43% from €57.8m to €32.6m ($45m), which accounts for a 0.1x net debt/ EBITDA ratio.

Summary of the luxury industry trends and upcoming growth engines

According to Bain, the luxury market was worth €217b in 2013 and is expected to grow by 5/6% over the next years. The number of consumers reached approximately 330m people in 2013 and should increase to 400m by 2020 and 500m by 2050.

- Customers

According to Bain, the top bracket of "true luxury" consumers (individuals with the highest incomes, buying the most expensive items), represented about 15m people who together spend €100b on luxury goods a year, almost half of the global luxury market.

HENRYs (High Earners, Not Rich Yet) are becoming a primary target for luxury goods companies. It refers to a segment of families earning between $250,000 and $500,000, but not having much left after taxes, schooling, housing and family costs.

The middle class in emerging markets should finally become one of the main growth drivers in the medium-term. Their consumption of accessories, perfumes and ready-to-wear products should increase in the next years.

- Main products

The report highlights that revenues will be driven by absolute luxury items (high level products, high quality materials, strong brand image etc.). Leather goods, accessories and shoes already became the biggest segment and should keep growing faster than other categories (4% growth in 2013 and 28% of total sales). Cosmetics and perfumes are slowing down in mature markets but are still strong in emerging countries (2% growth in 2013).

- Main markets

According to Bain, the main markets for luxury items are the Americas (4% growth), China (4% growth), South East Asia (11% growth) and the Middle East (5% growth). Europe is stable with a 2% growth and Japan should experience a 12% decline (mainly due to the depreciation of the currency). The study also underlines the fact that Africa is becoming a high-potential area with 11% growth.

In order to perform, I believe that luxury companies must be able to produce absolute luxury items in order target High Net Worth individuals. By doing so, they will strengthen their brand image and develop a competitive advantage. As a consequence, they will then be able to market and sell accessories, perfumes or ready-to-wear products to a broader category of customers worldwide.

Ferragamo is well positioned to benefit from the major growth engines of the luxury industry

The Italian company is well positioned to benefit from the major growth engines of the luxury industry thanks to a strong product and geographical diversification. Ferragamo offers all the products that should experience increasing sales in the upcoming years and is already well implemented in the growing areas.

First of all, Ferragamo is well diversified in terms of products. The Italian company's footwear and leather products can be considered as absolute luxury items and the Group can easily target High Net Worth individuals.

The Italian group is also present on other growing segments such as accessories, which should boost the revenues in the upcoming years. The ready-to-wear and accessories divisions developed by the company make it possible to target HENRYs and emerging markets middle classes, which is very positive.

The company can finally benefit from a growing perfume division (+13.7% yoy) that should provide long-term growth and resist to slower economies.

€m

|

2013

|

2012

|

Variation (%)

|

% 2013

|

% 2012

|

Footwear

|

544

|

506

|

7.5

|

43.2

|

43.9

|

leather goods

|

419

|

360

|

16.4

|

33.3

|

31.2

|

Ready to wear

|

103

|

108

|

-4.5

|

8.2

|

9.4

|

Accessories

|

91

|

90

|

1.2

|

7.2

|

7.8

|

Perfumes

|

80

|

70

|

13.7

|

6.3

|

6.1

|

Other

|

21

|

19

|

13.3

|

1.7

|

1.6

|

Source: Company

The Italian company also has a balanced geographical diversification with a good exposure to Asia (46.3%) and emerging markets in general (41.8%). The growing revenues from North America and the US are also very positive considering that the economy is improving. I finally like the fact that Ferragamo already operates in Latin America and progressively increases its exposure to Brazil and Mexico.

Be that as it may, the Italian company is present in all the markets where the luxury industry is growing.

€m

|

2013

|

2012

|

Variation (%)

|

% 2013

|

% 2012

|

Europe

|

326

|

289

|

12.8

|

25.9

|

25.1

|

North America

|

290

|

257

|

13.0

|

23.1

|

22.3

|

Japan

|

116

|

134

|

-13.5

|

9.2

|

11.6

|

Asia

|

467

|

420

|

11.0

|

37.1

|

36.5

|

Latin America

|

59

|

52

|

12.5

|

4.7

|

4.5

|

Source: Company

Ferragamo will generate a safe and long-term flow of increasing revenues

We have already seen that the Italian company should benefit from all the major growth engines of the luxury industry. I believe that Ferragamo is also one of the few luxury brands that can maintain a strong image, generate increasing revenues and last forever.

This is mainly due to the brand image, the focus on quality and the corporate governance.

- Ferragamo benefits from a brand heritage strongly linked with Italy and the Italian style. The company has been producing luxury items for more than 80 years and the brand is still associated to the founder: Salvatore Ferragamo.

- The Italian company offers superior quality products supported by the "Made in Italy" standard carried out by many carefully selected workshops. I believe that Ferragamo's products have the potential to become luxury icons and last forever. For instance, the company produces "extreme luxury shoes", made-to-order women's evening shoes that are real pieces of art.

- Ferragamo's corporate governance is strong, which is a key asset in order to generate long-term growth. The board of directors is made of people from different backgrounds that are able to manage the business adequately. Ferragamo is also still owned by the family through Ferragamo Finanziaria, which ensures a long-term commitment. I believe that the interests of the long-term investors and the family are aligned.

Source: Company

Ferragamo is finally one of the most powerful families in Florence and they maintain a good relationship with Matteo Renzi, former mayor of Florence and now Prime Minister, which is a key asset in Italy.

Investment thesis

Ferragamo is a strong investment for long-term investors who want to get a diversified exposure to the luxury industry.

The Italian company has a strong brand image and a Premium positioning, which guarantees a long-term growth and increasing revenues.

The Italian company is well positioned to benefit from all the major growth engines of the luxury industry in the upcoming years.

Valuation

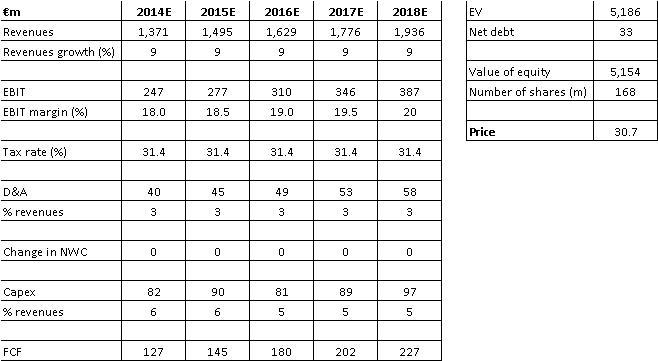

In order to get an indicative value of the share, I ran a DCF model based on the following assumptions:

- Long-term growth rate: 5%

- WACC: 10% (luxury industry)

- EBIT margin: 20%

- Tax rate: 31.4% (KPMG)

- Capex: 5% of revenues

(click to enlarge)

According to the model, the fair value of the share is about €30.7 ($42.4) compared with the current price of €22.7 ($31.3).

Risks

There are several risks to take into account:

- A slowdown of the Chinese economy would impact negatively the revenues as Ferragamo is mainly exposed to Asia.

- A switch of the demand from footwear & leather goods to more ready-to-wear products would be a real issue.

- Incapacity to increase the operating margins. Ferragamo still lags behind its peers in terms of operating margins.

2013

|

Ferragamo

|

Tod's

|

Prada (9M13)

|

Hermes (2012)

|

EBITDA margin (%)

|

20.7

|

24.4

|

31.9

|

35.5

|

EBIT margin (%)

|

17.4

|

20.0

|

26.3

|

32.1

|

Conclusion

Ferragamo is a strong investment to get exposure to the luxury industry. The Italian company has a great positioning on the Premium segment and a diversified profile. As a consequence, Ferragamo should be able to benefit from the major growth engines of the luxury industry and generate increasing revenues in the upcoming years.

However Ferragamo still needs to improve the operating margins in order to become more profitable and outperform its peers.

Finally, it might not be a good time to buy the stock as a downtrend appears to be going on. The stock price could be impacted negatively by the recent pullback of the main luxury goods companies including LVMH and Kering.

(click to enlarge)

Source: Yahoo finance

Source:

Editor's Note: This article covers a stock trading at less than $1 per share and/or has less than a $100 million market cap. Please be aware of the risks associated with these stocks.

http://seekingalpha.com/article/2087323-ferragamo-offers-a-diversified-and-long-term-exposure-to-the-luxury-industry?source=email_investing_ideas_lon_ide_13_17&ifp=0