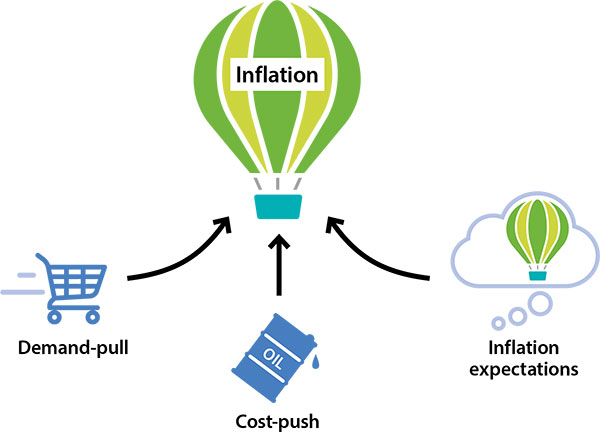

Cost-push inflation

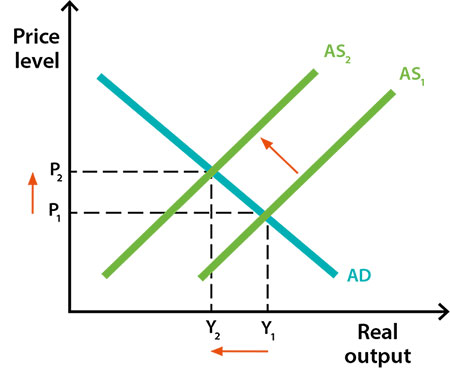

Cost-push inflation occurs when the total supply of goods and services in the economy which can be produced (aggregate supply) falls. A fall in aggregate supply is often caused by an increase in the cost of production. If aggregate supply falls but aggregate demand remains unchanged, there is upward pressure on prices and inflation – that is, inflation is ‘pushed’ higher.

An increase in the price of domestic or imported inputs (such as oil or raw materials) pushes up production costs. As firms are faced with higher costs of producing each unit of output they tend to produce a lower level of output and raise the prices of their goods and services. This can have flow-on effects by pushing up the prices of other goods and services. For example, an increase in the price of oil, which is a major input in many sectors of the economy, will initially lead to higher petrol prices. However, higher petrol prices will also make it more expensive to transport goods from one location to another which, in turn, will result in increased prices for items like groceries.

Cost-push inflation can also arise due to supply disruptions in specific industries – for example, due to unusual weather or natural disasters. Periodically, there are major cyclones and floods that damage large volumes of agricultural produce and result in significant increases in the price of processed food and both takeaway and restaurant meals, resulting in temporary periods of higher inflation.

Imported inflation and the exchange rate

Exchange rate movements can also affect prices and influence inflation outcomes. A decrease in the value of the domestic currency − that is, a depreciation − will increase inflation in two ways. First, the prices of goods and services produced overseas rise relative to those produced domestically. Consequently, consumers pay more to buy the same imported products and firms that rely on imported materials in their production processes pay more to buy these inputs. The price increases of imported goods and services contribute directly to inflation through the cost-push channel.

Second, a depreciation of the currency stimulates aggregate demand. This occurs because exports become relatively cheaper for foreigners to buy, leading to an increase in demand for exports and higher aggregate demand. At the same time, domestic consumers and firms reduce their consumption of relatively more expensive imports and shift their purchases towards domestically produced goods and services, again leading to an increase in aggregate demand. This increase in aggregate demand puts pressure on domestic production capacity, and increases the scope for domestic firms to raise their prices. These price increases contribute indirectly to inflation through the demand-pull channel.

In terms of imported inflation, the exchange rate has a greater influence on inflation through its effect on the prices of goods and services that are exported and imported (known as tradable goods and services), while prices of non-tradable goods and services depend more on domestic developments.