Concept of Financial Efficiency

A company's management may run the business well and yet not give the outside stockholders the right results for them, because its efficiency is confined to operations and does not extend to the best use of the capital.

The objective of efficient operation is to produce at low cost and to find the most profitable articles to sell.

Efficient finance requires that the stockholders' money be working in forms most suitable to their interest.

This is a question in which management, as such, has little interest.

$$$$$

Actually, it almost always wants as much capital from the owners as it can possibly get, in order to minimize its own financial problems.

Thus the typical management will operate with more capital than is necessary, if the stockholders permit it - which they often do.

It is not to be expected that public owners of a large business will strive as hard to get the maximum use and profit from their capital as will a young and energetic entrepreneur.

We are not offering any counsels of perfection or suggesting that stockholders should make exacting demands upon their superintendents.

We do suggest, however, that failure of the existing capital to earn enough to support its full value in the marketplace is sufficient justification for a critical spirit on the part of the stockholders.

Their inquiry should then extend to the question of whether the amount of capital used is suited to the results and to the reasonable needs of the business.

$$$$$

For the controlling stockholders, the retention of excessive capital is not a detriment, especially since they have the power to draw it out when they wish.

As pointed out above, this is one of the major factors that give insiders important and unwarranted benefits over outsiders.

If the ordinary public stockholders hold a majority of the stock, they have the power - buy use of their votes - to enforce appropriate standards of capital efficiency in their own interest.

To bring this about they will need more knowledge and gumption than they now exhibit.

Where the insiders have sufficient stock to constitute effective voting control, the outside stockholders have no power even if they do have the urge to protect themselves.

To meet this fairly frequent situations there is need, we believe, for a further development of the existing body of law defining the trusteeship responsibilities of those in control of a business toward those owners who are without an effective voice in its affairs.

Benjamin Graham

The Intelligent Investor

Friday, 30 January 2015

Tuesday, 27 January 2015

Portfolio Policy for the Enterprising Investor (Benjamin Graham)

The activities characteristics of the enterprising investor may be classified under four heads:

1. Buying in low market and selling in high markets

2. Buying carefully chosen "growth stocks"

3. Buying bargain issues of various types

4. Buying into "special situations"

Benjamin Graham

The Intelligent Investor

Related:

1. Buying in low market and selling in high markets

2. Buying carefully chosen "growth stocks"

3. Buying bargain issues of various types

4. Buying into "special situations"

Benjamin Graham

The Intelligent Investor

Quote

"The purpose of this book is to supply, in a form suitable for laymen, guidance in the adoption of an investment policy. Comparatively little will be said here about the technique of analysing securities; attention will be paid chiefly to investment principles and investors' attitudes."

"That risk cannot be avoided. But by bearing it clearly in mind we may succeed in reducing it."

Related:

### Attractive Buying Opportunities arise through a Variety of Causes

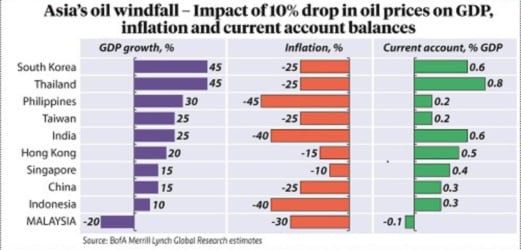

Lower oil prices and slowing global growth outside the US.

No changes in GDP growth upgrade following plunging oil prices: Merrill Lynch

BY - 23 JANUARY 2015 @ 11:25 PM

KUALA LUMPUR: Lower oil prices have yet to result in any sizeable goss domestic product (GDP) growth upgrade for emerging Asia, partly because of slowing global growth outside the US, said Bank of America Merrill Lynch.

“Lower oil prices have, however, improved the trade surplus significantly, supporting the current account balance and forex reserves positions.”

The research house said lower oil prices have also resulted in a sharp drop in inflation, particularly in Thailand, Philippines and India, which has allowed central banks to stay accommodative.

The Reserve Bank of India cut policy rates last week as inflation pressures and expectations fell sharply, while markets are starting to price in possible cuts in Thailand and South Korea.

“Emerging Asian countries will likely see a boost to GDP growth in the range of 10 basis points to 45 basis points with every 10 per cent fall in oil prices, if the oil price drop was purely a supply shock.”

Big beneficiaries are consumers as fuel prices at the pump fall, it said.

Savings from reduced fuel costs could be channeled to investments, which for example, is showing in Indonesia's government doubling of capital spending.

”Malaysia, is however an exception and will see overall GDP growth slow with lower oil, given its heavy reliance on oil & gas revenues.”

The government downgraded the growth outlook and raised its fiscal deficit projections this week.

“We remain cautious on the fiscal and current account outlook, given the heavy fiscal dependence on oil and downward trajectory of LNG prices in the coming months.”

The research house has downgraded the average oil price to US$52 for 2015, with oil prices likely to spiral to US$31 per barrel at the end of the first quarter before recovering.

“Asia’s oil windfall will likely see a significant shift in the relative positions of sovereign wealth funds. Oil and gas-related sovereign wealth funds (US$4.3 trillion) – which account for about 60 per cent of total sovereign wealth funds -- will likely see their size stagnate or erode on falling oil prices.”

Falling oil prices will likely dampen the overall growth of sovereign funds, as a large proportion is oil-related.

Norway's government pension fund (US$893 billion), Abu Dhabi Investment Authority (US$773 billion) and Saudi Arabia's SAMA (US$753 billion) are the three largest sovereign funds in the world, and are all oil-related.

“Recycling of Asia-dollars might partly replace the recycling of petrodollars.”

Asian sovereign wealth funds (US$2.8 trillion) account for about 39 per cent of total sovereign wealth funds, and will likely see their size increase at a faster clip.

Sovereign wealth funds of China (CIC & SAFE), Hong Kong (HKMA), Singapore (GIC & Temasek) and Korea (KIC) rank in the Top-15 globally.

http://www.nst.com.my/node/70742

Monday, 26 January 2015

Approach to Convertible Issues

An illustration on convertible issue

The fine balance between what is given and what is withheld in a standard-type convertible issue is well illustrated by the extensive use of this type of security in the financing of American Telephone & Telegraph Company.

Since 1913 the company has sold at least seven separate issues of convertible bonds, most of them through subscription rights to stockholders.

The convertible bonds had the important advantage to the company of bringing in a much wider class of buyers than would have been available for a stock offering, since the bonds are popular with many financial institutions which possess huge resources but some of which are not permitted to buy stocks.

The interest return on the bonds has generally been less than half the corresponding dividend yield on the stock - a factor which was calculated to offset the prior claim of the bondholders.

Since the company has been able to maintain its dividend without change for many years, the result has been the eventual conversion of all the older convertible issues into stock.

Thus the buyers of these convertibles have fared well through the years - but not quite so well as if they had bought the capital stock in the first place.

This example establishes the soundness of American Telephone & Telegraph, but not the intrinsic attractiveness of convertible bonds.

To prove them sound in practice we should need to have a number of instances in which the convertible worked out well even though the common stock proved disappointing.

Such instances are not easy to find.

$$$$$

Advice by Benjamin Graham on convertibles

Our general attitude toward new convertible issues is thus a mistrustful one.

We mean here, as in other similar observations, that the investor should look more than twice before he buys them.

After such hostile scrutiny he may find some exceptional offerings that are too good to refuse.

The ideal combination, of course, is a strongly secured convertible, exchangeable for a common stock which itself is attractive, and at a price only slightly higher than the current market.

Every now and then a new offering appears that meets these requirements.

By the nature of the securities markets, however, you are more likely to find such an opportunity in some older issue which has developed into a favorable position rather than in a new flotation.

(If a new issue is a really strong one, it is not likely to have a good conversion privilege.)

Benjamin Graham

The Intelligent Investor

The fine balance between what is given and what is withheld in a standard-type convertible issue is well illustrated by the extensive use of this type of security in the financing of American Telephone & Telegraph Company.

Since 1913 the company has sold at least seven separate issues of convertible bonds, most of them through subscription rights to stockholders.

The convertible bonds had the important advantage to the company of bringing in a much wider class of buyers than would have been available for a stock offering, since the bonds are popular with many financial institutions which possess huge resources but some of which are not permitted to buy stocks.

The interest return on the bonds has generally been less than half the corresponding dividend yield on the stock - a factor which was calculated to offset the prior claim of the bondholders.

Since the company has been able to maintain its dividend without change for many years, the result has been the eventual conversion of all the older convertible issues into stock.

Thus the buyers of these convertibles have fared well through the years - but not quite so well as if they had bought the capital stock in the first place.

This example establishes the soundness of American Telephone & Telegraph, but not the intrinsic attractiveness of convertible bonds.

To prove them sound in practice we should need to have a number of instances in which the convertible worked out well even though the common stock proved disappointing.

Such instances are not easy to find.

$$$$$

Advice by Benjamin Graham on convertibles

Our general attitude toward new convertible issues is thus a mistrustful one.

We mean here, as in other similar observations, that the investor should look more than twice before he buys them.

After such hostile scrutiny he may find some exceptional offerings that are too good to refuse.

The ideal combination, of course, is a strongly secured convertible, exchangeable for a common stock which itself is attractive, and at a price only slightly higher than the current market.

Every now and then a new offering appears that meets these requirements.

By the nature of the securities markets, however, you are more likely to find such an opportunity in some older issue which has developed into a favorable position rather than in a new flotation.

(If a new issue is a really strong one, it is not likely to have a good conversion privilege.)

Benjamin Graham

The Intelligent Investor

Sunday, 25 January 2015

Most security buyers obtain advice without paying for it specifically. You and your financial advisors..

Most security buyers obtain advice without paying for it specifically.

They should be wary of all persons, whether customers' brokers or security salesmen, who promise spectacular income or profits.

This applies both to the selection of securities and to guidance in the elusive art of trading in the market.

For defensive investors

Defensive investors, as we have defined them, will not ordinarily be equipped to pass independent judgement on the security recommendations made by their advisers.

But they can be explicit - and even repetitiously so - in stating the kind of securities they want to buy.

If they follow our prescription, they will confine themselves to US Savings Bonds and the common stocks of leading corporations purchased at levels that are not high in the light of experience and analysis.

The security analyst of any reputable stock exchange house can make up a suitable list of such common stocks and can certify to the investor whether or not the existing price level is a reasonably conservative one as judged by past experience.

For aggressive investors

The aggressive investor will ordinarily work in active co-operation with his advisers.

He will want their recommendations explained in detail and he will insist on passing his own judgment upon them.

This means that the investor will gear his expectations and the character of his security operations to the development of his own knowledge and experience in the field.

Only in the exceptional case, where the integrity and competence of the advisers have been thoroughly demonstrated, should the investor act upon the advice of others without understanding and approving the decision made.

They should be wary of all persons, whether customers' brokers or security salesmen, who promise spectacular income or profits.

This applies both to the selection of securities and to guidance in the elusive art of trading in the market.

For defensive investors

Defensive investors, as we have defined them, will not ordinarily be equipped to pass independent judgement on the security recommendations made by their advisers.

But they can be explicit - and even repetitiously so - in stating the kind of securities they want to buy.

If they follow our prescription, they will confine themselves to US Savings Bonds and the common stocks of leading corporations purchased at levels that are not high in the light of experience and analysis.

The security analyst of any reputable stock exchange house can make up a suitable list of such common stocks and can certify to the investor whether or not the existing price level is a reasonably conservative one as judged by past experience.

For aggressive investors

The aggressive investor will ordinarily work in active co-operation with his advisers.

He will want their recommendations explained in detail and he will insist on passing his own judgment upon them.

This means that the investor will gear his expectations and the character of his security operations to the development of his own knowledge and experience in the field.

Only in the exceptional case, where the integrity and competence of the advisers have been thoroughly demonstrated, should the investor act upon the advice of others without understanding and approving the decision made.

The relationship between the investment banker and the investor

Investment Bankers

The term "investment banker" is applied to a firm which engages to an important extent in originating, underwriting, and selling new issues of stocks and bonds. (To underwrite means to guarantee to the issuing corporation or other issuer, that the security will be fully sold.)

Much of the theoretical justification for maintaining active stock markets, notwithstanding their frequent speculative excesses, lies in the fact that organized security exchanges facilitate the sale of new issues of bonds and stocks.

The relationship between the investment banker and the investor is basically that of the salesman to the prospective buyer.

The investment banker and the financial institutions (banks and insurance companies)

For many years the great bulk of the new offerings has consisted of bond issues which were purchased in the main by financial institutions such as banks and insurance companies.

In this business the security salesmen have been dealing with shrewd and experienced buyers.

Hence any recommendations made by the investment bankers to these customers has had to pass careful and skeptical scrutiny.

Thus these transactions are almost always effected on a businesslike footing.

The investment banker and the individual security buyer

But a different situation obtains in the relationship between the individual security buyer and the investment banking firms, including the stockbrokers acting as underwriters.

Here the purchaser is frequently inexperienced and seldom shrewd.

He is easily influenced by what the salesman tells him, especially in the case of common-stock issues, since often his unconfessed desire in buying is chiefly to make a quick profit.

The effect of all this is that the public investor's protection lies less in his own critical faulty than in the scruples and ethics of the offering houses.

It is a tribute to the honesty and competence of the underwriting firms that they are able to combine fairly well the discordant roles of adviser and salesman.

But it is imprudent for the buyer to trust himself to the judgment of the seller.

The bad results of this unsound attitude show themselves recurrently in the underwriting field and with notable effect in the sale of new common-stock issues during periods of active speculation.

The intelligent investor will pay attention to the advice and recommendations received from investment banking houses, especially those known to him to have an excellent reputation; but he will be sure to bring sound and independent judgment to bear upon these suggestions - either his own, if he is competent, or that of some other type of adviser.

Benjamin Graham

Intelligent Investor

The term "investment banker" is applied to a firm which engages to an important extent in originating, underwriting, and selling new issues of stocks and bonds. (To underwrite means to guarantee to the issuing corporation or other issuer, that the security will be fully sold.)

Much of the theoretical justification for maintaining active stock markets, notwithstanding their frequent speculative excesses, lies in the fact that organized security exchanges facilitate the sale of new issues of bonds and stocks.

The relationship between the investment banker and the investor is basically that of the salesman to the prospective buyer.

The investment banker and the financial institutions (banks and insurance companies)

For many years the great bulk of the new offerings has consisted of bond issues which were purchased in the main by financial institutions such as banks and insurance companies.

In this business the security salesmen have been dealing with shrewd and experienced buyers.

Hence any recommendations made by the investment bankers to these customers has had to pass careful and skeptical scrutiny.

Thus these transactions are almost always effected on a businesslike footing.

The investment banker and the individual security buyer

But a different situation obtains in the relationship between the individual security buyer and the investment banking firms, including the stockbrokers acting as underwriters.

Here the purchaser is frequently inexperienced and seldom shrewd.

He is easily influenced by what the salesman tells him, especially in the case of common-stock issues, since often his unconfessed desire in buying is chiefly to make a quick profit.

The effect of all this is that the public investor's protection lies less in his own critical faulty than in the scruples and ethics of the offering houses.

It is a tribute to the honesty and competence of the underwriting firms that they are able to combine fairly well the discordant roles of adviser and salesman.

But it is imprudent for the buyer to trust himself to the judgment of the seller.

The bad results of this unsound attitude show themselves recurrently in the underwriting field and with notable effect in the sale of new common-stock issues during periods of active speculation.

The intelligent investor will pay attention to the advice and recommendations received from investment banking houses, especially those known to him to have an excellent reputation; but he will be sure to bring sound and independent judgment to bear upon these suggestions - either his own, if he is competent, or that of some other type of adviser.

Benjamin Graham

Intelligent Investor

Wednesday, 21 January 2015

The preferred stocks to own - Growth Stocks at suitable prices. Do not overpay to own them.

The stock of a growing company, if purchasable at a suitable price, is obviously preferable to others.

The choice between the attractive issue that turns out well and the one that does poorly is by no means easy to make in the growth-stock field.

However, superior results may be obtained in this field if the choices are competently made.

Even with careful selection, some of the individual issues may fare relatively poorly.

The choice between the attractive issue that turns out well and the one that does poorly is by no means easy to make in the growth-stock field.

However, superior results may be obtained in this field if the choices are competently made.

Even with careful selection, some of the individual issues may fare relatively poorly.

Tuesday, 20 January 2015

Formula Timing - Buying in low markets and selling in high markets. No simple and fool-proof formula. Select a ins and outs formula timing plan that is simple and convenient .

Let's look at the possibilities and limitations of a policy of entering the market when it is depressed and selling out in the advanced stages of a boom.

This bright idea appeared feasible from a first inspection of the market chart covering the gyrations of the past fifty years.

But closer study indicated that no simple and fool-proof formula could be counted upon to work out in the future.

For example, the history of the Dow-Jones Industrial Average suggests that it should be possible to buy at 140 during the next few years and sell out at 280 later.

But this is only an indication and not a true prediction.

Nor can we tell whether the probability of its working out is good enough to justify the basing of an investment policy upon it.

$$$$$

The various formula timing plans, which have come into prominence in recent years, all represent a compromise attempt to deal with this probability.

Instead of planning to do all the buying at 140 - or some similar price - and all the selling at 280, the formula user buys at various stages on the downside and sells in installments on the upside.

By this means he can obtain some benefit from market fluctuations, even if they do not fall precisely within the range suggested by the chart.

Thus his formula assures him at least some profit if the future performance of the market is only reasonably close to that of the past.

$$$$$

A simple application of this idea would be to sell 10 percent of your holdings when the market advances 10 per cent above a chosen base or central level; then to sell 20 per cent of the remainder when it advances another 10 per cent and so on.

Repurchases would be made after the market had declined to the central level, and on some similar schedule.

Following this plan, you would have sold all your stocks if and when the market level reached double the base figure, and you would then have realized a profit of 37 per cent above the base.

You can apply these ins and outs of formula timing plans, using various types of plans, to calculate their possible results, using the record of your own actual operations and also applied to hypothetical or imaginary funds.

$$$$$

There is some danger here for both writers and investors to lose themselves in a maze of alternative procedures.

It is well to bear certain basic facts in mind. No one plan has a priori or guaranteed advantage over any other.

The relative results of various plans will depend on how well each happens to fit the market fluctuations of the future.

$$$$$

1. The more certain the investor is that the range of future fluctuations will duplicate the past, the more justified he is in concentrating his buying close to the bottom line of the Dow-Jones performance chart and his selling not much below the top line.

2. But since we lack any proof that the past range must determine that of the future, most of us will prefer a compromise formula by which buying and selling is done in various stages below and above the indicated median level.

3. So too, there is no assured advantage as between a plan to sell 100 per cent of our stock holdings by the time a designated high point is reached and a plan that assures retention of some stocks under all circumstances. The latter in some measure protects against an inflationary breakout of a permanent character into a much higher band of fluctuation than we have experienced hitherto.

But like all the other choices in formula timing plans the wisdom of this one depends not on reasoning but on results.

$$$$$

The sovereign virtue of all formula plans lies in the compulsion they bring upon the investor to sell when the crowd is buying and to buy when the crowd lacks confidence.

If the reader adopts a formula plan today and it happens to turn out badly - because the market chances to soar upwards to unexpected heights and does not return - it will still prove to have been worth while.

For the principle and the psychology will remain sound and applicable to the markets of the future, however far removed their middle range may be from the line of the past.

$$$$$

Since all the rest is a matter of detail or of guesswork, we strongly advice to "formula investors" that they select a plan that is simple and convenient in their circumstance.

Benjamin Graham

Intelligent Investor

This bright idea appeared feasible from a first inspection of the market chart covering the gyrations of the past fifty years.

But closer study indicated that no simple and fool-proof formula could be counted upon to work out in the future.

For example, the history of the Dow-Jones Industrial Average suggests that it should be possible to buy at 140 during the next few years and sell out at 280 later.

But this is only an indication and not a true prediction.

Nor can we tell whether the probability of its working out is good enough to justify the basing of an investment policy upon it.

$$$$$

The various formula timing plans, which have come into prominence in recent years, all represent a compromise attempt to deal with this probability.

Instead of planning to do all the buying at 140 - or some similar price - and all the selling at 280, the formula user buys at various stages on the downside and sells in installments on the upside.

By this means he can obtain some benefit from market fluctuations, even if they do not fall precisely within the range suggested by the chart.

Thus his formula assures him at least some profit if the future performance of the market is only reasonably close to that of the past.

$$$$$

A simple application of this idea would be to sell 10 percent of your holdings when the market advances 10 per cent above a chosen base or central level; then to sell 20 per cent of the remainder when it advances another 10 per cent and so on.

Repurchases would be made after the market had declined to the central level, and on some similar schedule.

Following this plan, you would have sold all your stocks if and when the market level reached double the base figure, and you would then have realized a profit of 37 per cent above the base.

You can apply these ins and outs of formula timing plans, using various types of plans, to calculate their possible results, using the record of your own actual operations and also applied to hypothetical or imaginary funds.

$$$$$

There is some danger here for both writers and investors to lose themselves in a maze of alternative procedures.

It is well to bear certain basic facts in mind. No one plan has a priori or guaranteed advantage over any other.

The relative results of various plans will depend on how well each happens to fit the market fluctuations of the future.

$$$$$

1. The more certain the investor is that the range of future fluctuations will duplicate the past, the more justified he is in concentrating his buying close to the bottom line of the Dow-Jones performance chart and his selling not much below the top line.

2. But since we lack any proof that the past range must determine that of the future, most of us will prefer a compromise formula by which buying and selling is done in various stages below and above the indicated median level.

3. So too, there is no assured advantage as between a plan to sell 100 per cent of our stock holdings by the time a designated high point is reached and a plan that assures retention of some stocks under all circumstances. The latter in some measure protects against an inflationary breakout of a permanent character into a much higher band of fluctuation than we have experienced hitherto.

But like all the other choices in formula timing plans the wisdom of this one depends not on reasoning but on results.

$$$$$

The sovereign virtue of all formula plans lies in the compulsion they bring upon the investor to sell when the crowd is buying and to buy when the crowd lacks confidence.

If the reader adopts a formula plan today and it happens to turn out badly - because the market chances to soar upwards to unexpected heights and does not return - it will still prove to have been worth while.

For the principle and the psychology will remain sound and applicable to the markets of the future, however far removed their middle range may be from the line of the past.

$$$$$

Since all the rest is a matter of detail or of guesswork, we strongly advice to "formula investors" that they select a plan that is simple and convenient in their circumstance.

Benjamin Graham

Intelligent Investor

Monday, 19 January 2015

Timing is of no value, unless it coincides with pricing, enabling repurchase at substantially under previous selling price.

The investor can scarcely take seriously the innumerable predictions which appear almost daily and are his for the asking.

Yet in many cases he pays attention to them and even acts on them. Why?

Because he has been persuaded that it is important for him to form some opinion of the future course of the stock market, and because he feels that the brokerage or service forecast is at least more dependable than his own.

This attitude will bring the typical investor nothing but regrets.

Without realizing it, he is likely to find himself transformed into a market trader.

During a sustained bull movement, when it is easy to make money by simply swimming with the speculative tide, he will gradually lose interest in the quality and the value of the securities he is buying and become more and more engrossed in the fascinating game of beating the market.

But "beating the market" really means beating himself - for he and his fellows constitute the market.

Thus he begins by studying market movements as a "commonsense investment precaution" or a "desirable supplement to his study of security values"; he ends as a stock-market speculator, indistinguishable from all the rest.

A great deal of brain power goes into this field, and undoubtedly, some people can make money by being good stock-market analysts.

But it is absurd to think that the general public can ever make money out of market forecasts.

For who will buy when the general public, at a given signal, rushes to sell out at a profit?

If you, the reader, expect to get rich over the years by following some system or leadership in market forecasting, you must be expecting:

(a) to try to do what countless others are aiming at and

(b) to be able to do it better than your numerous competitors in the market.

There is no basis either in logic or in experience for assuming that any typical or average investor can anticipate market movements more successfully that the general public, of which he is himself a part.

$$$$$$$$$$

Timing is of great psychological importance to the speculator because he wants to make his profit in a hurry.

The idea of waiting a year before his stock moves up is repugnant to him.

But a waiting period, as such, is of no consequence to the investor.

What advantage is there to him in having his money un-invested until he receives some (presumably) trustworthy signal that the time has come to buy?

He enjoys an advantage only if by waiting he succeeds in buying later at a sufficiently lower price to offset his loss of dividend income.

What this means is that timing is of no real value to the investor unless it coincides with pricing - that is, unless it enables him to repurchase his shares at substantially under his previous selling price.

Benjamin Graham

Intelligent Investor

Yet in many cases he pays attention to them and even acts on them. Why?

Because he has been persuaded that it is important for him to form some opinion of the future course of the stock market, and because he feels that the brokerage or service forecast is at least more dependable than his own.

This attitude will bring the typical investor nothing but regrets.

Without realizing it, he is likely to find himself transformed into a market trader.

During a sustained bull movement, when it is easy to make money by simply swimming with the speculative tide, he will gradually lose interest in the quality and the value of the securities he is buying and become more and more engrossed in the fascinating game of beating the market.

But "beating the market" really means beating himself - for he and his fellows constitute the market.

Thus he begins by studying market movements as a "commonsense investment precaution" or a "desirable supplement to his study of security values"; he ends as a stock-market speculator, indistinguishable from all the rest.

A great deal of brain power goes into this field, and undoubtedly, some people can make money by being good stock-market analysts.

But it is absurd to think that the general public can ever make money out of market forecasts.

For who will buy when the general public, at a given signal, rushes to sell out at a profit?

If you, the reader, expect to get rich over the years by following some system or leadership in market forecasting, you must be expecting:

(a) to try to do what countless others are aiming at and

(b) to be able to do it better than your numerous competitors in the market.

There is no basis either in logic or in experience for assuming that any typical or average investor can anticipate market movements more successfully that the general public, of which he is himself a part.

$$$$$$$$$$

Timing is of great psychological importance to the speculator because he wants to make his profit in a hurry.

The idea of waiting a year before his stock moves up is repugnant to him.

But a waiting period, as such, is of no consequence to the investor.

What advantage is there to him in having his money un-invested until he receives some (presumably) trustworthy signal that the time has come to buy?

He enjoys an advantage only if by waiting he succeeds in buying later at a sufficiently lower price to offset his loss of dividend income.

What this means is that timing is of no real value to the investor unless it coincides with pricing - that is, unless it enables him to repurchase his shares at substantially under his previous selling price.

Benjamin Graham

Intelligent Investor

A creditable, if unspectacular, result can be achieved by the lay investor with a minimum of effort and capability.

One thing badly needed by investors - and a quality they rarely seem to have - is a sense of financial history. In nine companies out of ten the factor of fluctuation has been a more dominant and important consideration in the matter of investment than has the factor of long-term growth or decline.

Yet the market tends to greet each upsurge as if it were the beginning of an endless growth and each decline in earnings as if it presaged ultimate extinction.

Investments may be soundly made with either of two alternative intentions:

(a) to carry them determinedly through the fluctuations that are reasonably to be expected in the future, or

(b) to take advantage of such fluctuations by buying when confidence and prices are low and by selling when both are high.

Neither policy can be followed with intelligence unless the investor, or his adviser, has a broad comprehension of the effects of the economic alternations of the past, and unless he takes them fully into account in planning to meet the future.

The art of investment has one characteristic which is not generally appreciated. A creditable, if unspectacular, result can be achieved by the lay investor with a minimum of effort and capability, but to improve this easily attainable standard requires much application and more than a trace of wisdom. If you merely try to bring just a little extra knowledge and cleverness to bear upon your investment program, instead of realizing a little better than normal results, you may well find that you have done worse.

Since anyone - by just buying and holding a representative list - can equal the performance of the market averages, it would seem a comparatively simple matter to "beat the averages"' but as a matter of fact the proportion of smart people who try this and fail is surprisingly large.

Even many of the investment funds, with all their experienced personnel, have not performed as well over the years as has the general market.

Allied to the foregoing is the record of the published stock-market predictions of the brokerage houses, for there is strong evidence that their calculated forecasts have been somewhat less reliable than the simple tossing of a coin.

Benjamin Graham

Intelligent Investor

Yet the market tends to greet each upsurge as if it were the beginning of an endless growth and each decline in earnings as if it presaged ultimate extinction.

Investments may be soundly made with either of two alternative intentions:

(a) to carry them determinedly through the fluctuations that are reasonably to be expected in the future, or

(b) to take advantage of such fluctuations by buying when confidence and prices are low and by selling when both are high.

Neither policy can be followed with intelligence unless the investor, or his adviser, has a broad comprehension of the effects of the economic alternations of the past, and unless he takes them fully into account in planning to meet the future.

The art of investment has one characteristic which is not generally appreciated. A creditable, if unspectacular, result can be achieved by the lay investor with a minimum of effort and capability, but to improve this easily attainable standard requires much application and more than a trace of wisdom. If you merely try to bring just a little extra knowledge and cleverness to bear upon your investment program, instead of realizing a little better than normal results, you may well find that you have done worse.

Since anyone - by just buying and holding a representative list - can equal the performance of the market averages, it would seem a comparatively simple matter to "beat the averages"' but as a matter of fact the proportion of smart people who try this and fail is surprisingly large.

Even many of the investment funds, with all their experienced personnel, have not performed as well over the years as has the general market.

Allied to the foregoing is the record of the published stock-market predictions of the brokerage houses, for there is strong evidence that their calculated forecasts have been somewhat less reliable than the simple tossing of a coin.

Benjamin Graham

Intelligent Investor

Judged by past history, you always had a chance to buy them back at substantially lower levels at some time later.

Another encouraging element for the preceptor is found in the strong warp of continuity that seems to underlie the pattern of financial change.

Important developments affecting broad groups of security values do not come suddenly or in one piece.

An excellent example is found in the long term course of the stock market; this has never moved to permanently higher levels without retreating at least once to former territory.

Hence, investors who sold out representative stocks at what seemed a high price as judged by past history have always had a chance to buy them back at substantially lower levels at some later time.

This proved true in spite of the inflationary effects of the First World War and again of the Second World War, and it also was notoriously true after the extreme market advance of 1928 - 29.

Benjamin Graham

The Intelligent Investor

Comments:

Here are the charts of KLSE and the annual returns of KLSE.

Observe for yourself whether the statement by Benjamin Graham above holds true.

It generally is so but how can you hope to profit from this strategy?

Annual Stock Market Returns in KLSE

2005 -0.84%

2006 21.83%

2007 31.82%

2008 -39.33%

2009 45.17%

2010 19.34%

2011 0.78%

2012 10.34%

2013 10.54%

2014 -5.66%

MSCI Malaysia (price) index

2005 -1.52%

2006 33.11%

2007 41.54%

2008 -43.39%

2009 47.79%

2010 32.51%

2011 -2.92%

2012 10.76%

2013 4.17%

2014 -13.41%

Important developments affecting broad groups of security values do not come suddenly or in one piece.

An excellent example is found in the long term course of the stock market; this has never moved to permanently higher levels without retreating at least once to former territory.

Hence, investors who sold out representative stocks at what seemed a high price as judged by past history have always had a chance to buy them back at substantially lower levels at some later time.

This proved true in spite of the inflationary effects of the First World War and again of the Second World War, and it also was notoriously true after the extreme market advance of 1928 - 29.

Benjamin Graham

The Intelligent Investor

Comments:

Here are the charts of KLSE and the annual returns of KLSE.

Observe for yourself whether the statement by Benjamin Graham above holds true.

It generally is so but how can you hope to profit from this strategy?

Annual Stock Market Returns in KLSE

2005 -0.84%

2006 21.83%

2007 31.82%

2008 -39.33%

2009 45.17%

2010 19.34%

2011 0.78%

2012 10.34%

2013 10.54%

2014 -5.66%

MSCI Malaysia (price) index

2005 -1.52%

2006 33.11%

2007 41.54%

2008 -43.39%

2009 47.79%

2010 32.51%

2011 -2.92%

2012 10.76%

2013 4.17%

2014 -13.41%

Sunday, 18 January 2015

### Attractive Buying Opportunities arise through a Variety of Causes

Attractive buying opportunities for the enterprising investor arise through a variety of causes.

The standard or recurrent reasons are

(a) a low level of the general market and

(b) the carrying to an extreme of popular disfavor toward individual issues.

Sometimes, but much more rarely, we have the failure of the market to respond to an important improvement in the company's affairs and in the value of its stock.

Frequently, we find a discrepancy between price and value which arises from the public's failure to realise the true situation of a company - this in turn being due to some complicated aspects of accounting or corporate relationships.

It is the function of competent security analysis to unravel such complexities and to bring the true facts and values to light.

Benjamin Graham

Intelligent Investor

Summary:

Attractive buying opportunities (discrepancy between price and value) due to various causes:

1. low level of the general market

2. extreme of popular disfavour towards individual stocks

3. failure of market to respond to improvement in the company

4. failure to realise hidden value in the company due to some complicated aspects of accounting or corporate relationships

The standard or recurrent reasons are

(a) a low level of the general market and

(b) the carrying to an extreme of popular disfavor toward individual issues.

Sometimes, but much more rarely, we have the failure of the market to respond to an important improvement in the company's affairs and in the value of its stock.

Frequently, we find a discrepancy between price and value which arises from the public's failure to realise the true situation of a company - this in turn being due to some complicated aspects of accounting or corporate relationships.

It is the function of competent security analysis to unravel such complexities and to bring the true facts and values to light.

Benjamin Graham

Intelligent Investor

Summary:

Attractive buying opportunities (discrepancy between price and value) due to various causes:

1. low level of the general market

2. extreme of popular disfavour towards individual stocks

3. failure of market to respond to improvement in the company

4. failure to realise hidden value in the company due to some complicated aspects of accounting or corporate relationships

Special Situation is where a Definite Corporate Event creates undervalued security in which profits is expected to be realised.

A particular kind of undervalued security in which the profit is expected to be realized from a definite corporate event, rather than from a mere change in the market's attitude is known as a "special situation."

Such events include

A great deal of money has been made by shrewd investors in recent years through the purchase of bonds of railroads in bankruptcy - bonds which they knew would be worth much more than their cost when the railroads were finally reorganized.

Similar large profits have been made in the preferred and common stocks of public-utility holding companies which either were being broken up under the so-called death-sentence clause of the 1935 legislation or were subject to recapitalization plans.

The underlying factor here is the tendency of the security markets to undervalue issues which are involved in any sort of complicated legal proceedings.

An old Wall Street motto has been: "Never buy into a lawsuit."

This may be sound advice to the speculator seeking quick action on his holdings.

But the adoption of this attitude by the general public is bound to create bargain opportunities in the securities affected by it, since the prejudice against them holds their price down to unduly low levels.

"In general, the market undervalues a litigated claim as an asset and overvalues it as a liability. Hence students of these situations often have an opportunity to buy into them at less than their true value, and to realize attractive profits - on the average - when the litigation is disposed off."

The exploitation of special situations is a technical branch of investment which requires a somewhat unusual mentality and equipment. Probably only a small percentage of our enterprising investors are likely to engage in it.

Benjamin Graham

The Intelligent Investor

Such events include

- sale of the business,

- merger,

- recapitalization,

- reorganization, and

- liquidation.

A great deal of money has been made by shrewd investors in recent years through the purchase of bonds of railroads in bankruptcy - bonds which they knew would be worth much more than their cost when the railroads were finally reorganized.

Similar large profits have been made in the preferred and common stocks of public-utility holding companies which either were being broken up under the so-called death-sentence clause of the 1935 legislation or were subject to recapitalization plans.

The underlying factor here is the tendency of the security markets to undervalue issues which are involved in any sort of complicated legal proceedings.

An old Wall Street motto has been: "Never buy into a lawsuit."

This may be sound advice to the speculator seeking quick action on his holdings.

But the adoption of this attitude by the general public is bound to create bargain opportunities in the securities affected by it, since the prejudice against them holds their price down to unduly low levels.

"In general, the market undervalues a litigated claim as an asset and overvalues it as a liability. Hence students of these situations often have an opportunity to buy into them at less than their true value, and to realize attractive profits - on the average - when the litigation is disposed off."

The exploitation of special situations is a technical branch of investment which requires a somewhat unusual mentality and equipment. Probably only a small percentage of our enterprising investors are likely to engage in it.

Benjamin Graham

The Intelligent Investor

Saturday, 17 January 2015

Concept of "Risk." Market price fluctuation is NOT risk.

It is conventional to speak of good bonds as less risky than good preferred stocks and of the latter as less risky than good common stocks.

From this is derived the popular prejudice against common stocks because they are not "safe."

The words "risk" and "safety" are applied to securities in two different senses, with a resultant confusion in thought.

A bond is clearly proved unsafe when it defaults its interest or principal payments.

Similarly, if a preferred stock or even a common stock is bought with the expectation that a given rate of dividend will be continued, then a reduction or passing of the dividend means that it is unsafe.

It is also true that an investment contains a risk if there is a fair possibility that the holder may have to sell at a time when the price is well below cost.

Nevertheless, the idea of risk is often extended to apply to a possible decline in the price of a security, even though the decline may be of a cyclical and temporary nature and even though the holder is unlikely to be forced to sell at such times.

These chances are present in all securities, other than United States Savings Bonds, and to a greater extent in the general run of common stocks than in senior issues generally.

But we believe that what is here involved is not a true risk in the useful sense of the term.

$$$$

The man who holds a mortgage on a building might have to take a loss if he were forced to sell it at an unfavourable time. That element is not taken into account in judging the safety or risk of ordinary real-estate mortgages, the only criterion being the certainty of punctual payments.

In the same way the risk attached to an ordinary commercial business is measured by the chance of its losing money, not by what would happen if the owner, were forced to sell.

We would emphasize our conviction that the bona fide investor does not lose money merely because the market price of his holdings declines; the fact that a decline may occur does not mean that he is running a true risk of loss.

$$$$$

If a group of well-selected common-stock investments shows a satisfactory over-all return, as measured through a fair number of years, then this group investment has proved to be "safe".

During that period its market value is bound to fluctuate, and as likely as not it will sell for a while under the buyer's cost.

If that fact makes the investment "risky" it would then have to be called both risky and safe at the same time.

$$$$$

This confusion may be avoided if we apply the concept of risk solely to a loss of value which either:

(a) is realized through actual sale or

(b) is ascertained to be caused by a significant deterioration in the company's position.

Many common stocks do involve risks of such deterioration.

But it is our thesis that a properly executed group investment in common stocks does not carry any substantial risk of this sort and that therefore it should not be termed "risk" merely because of the element of price fluctuation.

Benjamin Graham

The Intelligent Investor

From this is derived the popular prejudice against common stocks because they are not "safe."

The words "risk" and "safety" are applied to securities in two different senses, with a resultant confusion in thought.

A bond is clearly proved unsafe when it defaults its interest or principal payments.

Similarly, if a preferred stock or even a common stock is bought with the expectation that a given rate of dividend will be continued, then a reduction or passing of the dividend means that it is unsafe.

It is also true that an investment contains a risk if there is a fair possibility that the holder may have to sell at a time when the price is well below cost.

Nevertheless, the idea of risk is often extended to apply to a possible decline in the price of a security, even though the decline may be of a cyclical and temporary nature and even though the holder is unlikely to be forced to sell at such times.

These chances are present in all securities, other than United States Savings Bonds, and to a greater extent in the general run of common stocks than in senior issues generally.

But we believe that what is here involved is not a true risk in the useful sense of the term.

$$$$

The man who holds a mortgage on a building might have to take a loss if he were forced to sell it at an unfavourable time. That element is not taken into account in judging the safety or risk of ordinary real-estate mortgages, the only criterion being the certainty of punctual payments.

In the same way the risk attached to an ordinary commercial business is measured by the chance of its losing money, not by what would happen if the owner, were forced to sell.

We would emphasize our conviction that the bona fide investor does not lose money merely because the market price of his holdings declines; the fact that a decline may occur does not mean that he is running a true risk of loss.

$$$$$

If a group of well-selected common-stock investments shows a satisfactory over-all return, as measured through a fair number of years, then this group investment has proved to be "safe".

During that period its market value is bound to fluctuate, and as likely as not it will sell for a while under the buyer's cost.

If that fact makes the investment "risky" it would then have to be called both risky and safe at the same time.

$$$$$

This confusion may be avoided if we apply the concept of risk solely to a loss of value which either:

(a) is realized through actual sale or

(b) is ascertained to be caused by a significant deterioration in the company's position.

Many common stocks do involve risks of such deterioration.

But it is our thesis that a properly executed group investment in common stocks does not carry any substantial risk of this sort and that therefore it should not be termed "risk" merely because of the element of price fluctuation.

Benjamin Graham

The Intelligent Investor

Substantial profits from the purchase of secondary companies at bargain prices arise in a variety of ways

If secondary issues tend normally to be undervalued, what reason has the investor to hope that he can profit by such a situation?

For if it persists indefinitely, will he not always be in the same position market wise as when he bought the issue?

The answer here is somewhat complicated.

Substantial profits from the purchase of secondary companies at bargain prices arise in a variety of ways:

1. The dividend return is high.

2. The reinvested earnings are substantial in relation to the price paid and will ultimately affect the price. In a five- to seven-year period these advantages can bulk quite large in a well-selected list.

3. When a bull market appears it is most generous to low-priced issues; thus it tends to raise the typical bargain issue to at least a reasonable level.

4. Even during relatively featureless market periods a continuous process of price adjustment goes on, under which secondary issues that were undervalued may rise at least to the normal level for their type of security.

Benjamin Graham

The Intelligent Investor

Related:

For if it persists indefinitely, will he not always be in the same position market wise as when he bought the issue?

The answer here is somewhat complicated.

Substantial profits from the purchase of secondary companies at bargain prices arise in a variety of ways:

1. The dividend return is high.

2. The reinvested earnings are substantial in relation to the price paid and will ultimately affect the price. In a five- to seven-year period these advantages can bulk quite large in a well-selected list.

3. When a bull market appears it is most generous to low-priced issues; thus it tends to raise the typical bargain issue to at least a reasonable level.

4. Even during relatively featureless market periods a continuous process of price adjustment goes on, under which secondary issues that were undervalued may rise at least to the normal level for their type of security.

Benjamin Graham

The Intelligent Investor

Related:

Bargain-issue pattern in Secondary Companies

Friday, 16 January 2015

Bargain-issue pattern in Secondary Companies

We have defined a secondary company as one which is not a leader in a fairly important industry.

Thus, it is usually one of the smaller concerns in its field, but it may equally well be the chief unit in an unimportant line.

By way of exception, any company that has established itself as a growth stock is not ordinarily considered as "secondary."

In the 1920's relatively little distinction was drawn between industry leaders and other listed issues, provided the latter were of respectable size.

The public felt that a middle-sized company was strong enough to weather storms and that it had a better chance for really spectacular expansion than one which was already of major dimensions.

The 1931-33 depression

The 1931-33 depression, however, had a particularly devastating impact on companies below the first rank either in size or in inherent stability.

As a result of that experience investors have since developed a pronounced preference for industry leaders and a corresponding lack of interest in the ordinary company of secondary importance.

This has meant that the latter group has usually sold at much lower prices in relation to earnings and assets than have the former.

It has also meant further that in many instances the price has fallen so low as to establish the issue in the bargain class.

When investors rejected the stocks of secondary companies, even though these sold at relatively low prices, they were expressing a belief or fear that such companies faced a dismal future.

In fact, at least subconsciously, they calculated that any price was too high for them because they were heading for extinction - just as in 1929 the companion theory for the "blue chips" was that no price was too high for them because their future possibilities were limitless.

Both of these views were exaggerations and were productive of serious investment errors.

Actually, the typical middle-sized listed company is a large one when compared with the average privately-owned business.

There is no sound reason why such companies should not continue indefinitely in operation, undergoing the vicissitudes characteristic of our economy but earnings on the whole a fair return on their invested capital.

This brief review indicates that the stock market's attitude toward secondary companies tends to be unrealistic and consequently to create in normal times innumerable instances of major undervaluation.

Benjamin Graham

The Intelligent Investor

Thus, it is usually one of the smaller concerns in its field, but it may equally well be the chief unit in an unimportant line.

By way of exception, any company that has established itself as a growth stock is not ordinarily considered as "secondary."

In the 1920's relatively little distinction was drawn between industry leaders and other listed issues, provided the latter were of respectable size.

The public felt that a middle-sized company was strong enough to weather storms and that it had a better chance for really spectacular expansion than one which was already of major dimensions.

The 1931-33 depression

The 1931-33 depression, however, had a particularly devastating impact on companies below the first rank either in size or in inherent stability.

As a result of that experience investors have since developed a pronounced preference for industry leaders and a corresponding lack of interest in the ordinary company of secondary importance.

This has meant that the latter group has usually sold at much lower prices in relation to earnings and assets than have the former.

It has also meant further that in many instances the price has fallen so low as to establish the issue in the bargain class.

When investors rejected the stocks of secondary companies, even though these sold at relatively low prices, they were expressing a belief or fear that such companies faced a dismal future.

In fact, at least subconsciously, they calculated that any price was too high for them because they were heading for extinction - just as in 1929 the companion theory for the "blue chips" was that no price was too high for them because their future possibilities were limitless.

Both of these views were exaggerations and were productive of serious investment errors.

Actually, the typical middle-sized listed company is a large one when compared with the average privately-owned business.

There is no sound reason why such companies should not continue indefinitely in operation, undergoing the vicissitudes characteristic of our economy but earnings on the whole a fair return on their invested capital.

This brief review indicates that the stock market's attitude toward secondary companies tends to be unrealistic and consequently to create in normal times innumerable instances of major undervaluation.

Benjamin Graham

The Intelligent Investor

Purchase of Bargain Issues

We define a bargain issue as one which, on the basis of facts established by analysis, appears to be worth considerably more than it is selling for.

The genus includes bonds and preferred stocks selling well under par, as well as common stocks.

To be concrete as possible, let us suggest that an issue is not a true "bargain" unless the indicated value is at least 50% more than the price.

What kind of facts would warrant the conclusion that so great a discrepancy exists?

How do bargains come into existence, and how does the investor profit from them?

There are two tests by which a bargain common stock is detected.

The first is by our method of appraisal. This relies largely on estimating future earnings and then multiplying these by a factor appropriate to the particular issue.

The second test is the value of the business to a private owner. This value also is often determined chiefly by expected future earnings - in which case the result may be identical with the first. But in the second test more attention is likely to be paid to the realizable value of the assets, with particular emphasis on the net current assets or working capital.

Courage in depressed markets

At low point in the general market a large proportion of common stocks are bargain issues, as measured by these standards.

It is true that current earnings and the immediate prospects may both be poor, but a level-headed appraisal of average future conditions would indicate values far above ruling prices.

Thus the wisdom of having courage in depressed markets is vindicated not only by the voice of experience but also by application of plausible techniques of value analysis.

The same vagaries of the marketplace which recurrently establish a bargain condition in the general list account for the existence of many individual bargains at almost all market levels.

The market is always making mountains out of molehills and exaggerating ordinary vicissitudes into major setbacks. Even a mere lack of interest or enthusiasm may impel a price decline to absurdly low levels.

Thus we have two major sources of undervaluation: (a) currently disappointing results, and (b) protracted neglect or unpopularity.

The private-owner test

The private-owner test would ordinarily start with the net worth as shown in the balance sheet. The question then arises as to whether the indicated earning power is sufficient to validate the net worth as a measure of what a private buyer would be justified in paying for the business as a whole.

If the answer is definitely yes, we suggest that an ordinary investor should find the common stock attractive at a price one-third or more below such a figure.

If instead of using all the net worth as a starting point the investor considered only the working capital and applied his test to that, he would have a more convincing demonstration of the existence of a bargain opportunity.

For it is something of an axiom that a business is worth to any private owner at least the amount of its working capital, since it could ordinarily be sold or liquidated for more than this figure.

Hence, if a common stock can be bought at no more than two-thirds of the working -capital value alone- disregarding all the other assets - and if the earnings record and prospects are reasonably satisfactory, there is strong reason to believe that the investor is getting substantially more than his money's worth.

Benjamin Graham

The Intelligent Investor

The genus includes bonds and preferred stocks selling well under par, as well as common stocks.

To be concrete as possible, let us suggest that an issue is not a true "bargain" unless the indicated value is at least 50% more than the price.

What kind of facts would warrant the conclusion that so great a discrepancy exists?

How do bargains come into existence, and how does the investor profit from them?

There are two tests by which a bargain common stock is detected.

The first is by our method of appraisal. This relies largely on estimating future earnings and then multiplying these by a factor appropriate to the particular issue.

The second test is the value of the business to a private owner. This value also is often determined chiefly by expected future earnings - in which case the result may be identical with the first. But in the second test more attention is likely to be paid to the realizable value of the assets, with particular emphasis on the net current assets or working capital.

Courage in depressed markets

At low point in the general market a large proportion of common stocks are bargain issues, as measured by these standards.

It is true that current earnings and the immediate prospects may both be poor, but a level-headed appraisal of average future conditions would indicate values far above ruling prices.

Thus the wisdom of having courage in depressed markets is vindicated not only by the voice of experience but also by application of plausible techniques of value analysis.

The same vagaries of the marketplace which recurrently establish a bargain condition in the general list account for the existence of many individual bargains at almost all market levels.

The market is always making mountains out of molehills and exaggerating ordinary vicissitudes into major setbacks. Even a mere lack of interest or enthusiasm may impel a price decline to absurdly low levels.

Thus we have two major sources of undervaluation: (a) currently disappointing results, and (b) protracted neglect or unpopularity.

The private-owner test

The private-owner test would ordinarily start with the net worth as shown in the balance sheet. The question then arises as to whether the indicated earning power is sufficient to validate the net worth as a measure of what a private buyer would be justified in paying for the business as a whole.

If the answer is definitely yes, we suggest that an ordinary investor should find the common stock attractive at a price one-third or more below such a figure.

If instead of using all the net worth as a starting point the investor considered only the working capital and applied his test to that, he would have a more convincing demonstration of the existence of a bargain opportunity.

For it is something of an axiom that a business is worth to any private owner at least the amount of its working capital, since it could ordinarily be sold or liquidated for more than this figure.

Hence, if a common stock can be bought at no more than two-thirds of the working -capital value alone- disregarding all the other assets - and if the earnings record and prospects are reasonably satisfactory, there is strong reason to believe that the investor is getting substantially more than his money's worth.

Benjamin Graham

The Intelligent Investor

Growth Stock Approach

Every investor would like to select a list of securities that will do better than the average over a period of years. A growth stock may be defined as one which has done this in the past and is expected to do so in the future.

(A company with an ordinary record cannot, without confusing the term, be called a growth company or a "growth stock" merely because its proponent expects it to do better than the average in the future. It is just a "promising company.")

Thus it seems only logical that the intelligent investor should concentrate upon the selection of growth stocks.

Actually the matter is more complicated.

The pursue of this aspect of investment policy require more ability and application than most investors can bring to bear on the problem.

The stock of a growing company, if purchasable at a suitable price, is obviously preferable to others.

No matter how enthusiastic the investor may feel about the prospects of a particular company, however, he should set a limit upon the price that he is willing to pay for such prospects.

In the case of a growth company, we should recommended payment of a premium for the growth potential not to exceed about 50% of the value determined without it.

Such a rule would result at times in the missing of an unusually good opportunity.

More often, it would mean the investor's saving himself from "going overboard" on an issue that looked especially good to him and everyone else and consequently was selling much too high.

The choice between the attractive issue that turns out well and the one that does poorly is by no means easy to make in the growth-stock field.

However, superior results may be obtained in this field if the choices are competently made. Even with careful selection, some of the individual issues may fare relatively poorly.

Thus for good results in the growth-stock field there is need not only for skillful analysis but for ample diversification as well.

Summary

The enterprising investor may properly buy growth stocks.

He should beware of paying excessively for them, and he might well limit the price by some practical rule.

A growth-stock program will not be automatically successful; its outcome will depend on the foresight and judgement of the investor or his advisers rather than on any clear-cut methods of analysis.

Benjamin Graham

Intelligent Investor

(A company with an ordinary record cannot, without confusing the term, be called a growth company or a "growth stock" merely because its proponent expects it to do better than the average in the future. It is just a "promising company.")

Thus it seems only logical that the intelligent investor should concentrate upon the selection of growth stocks.

Actually the matter is more complicated.

The pursue of this aspect of investment policy require more ability and application than most investors can bring to bear on the problem.

The stock of a growing company, if purchasable at a suitable price, is obviously preferable to others.

No matter how enthusiastic the investor may feel about the prospects of a particular company, however, he should set a limit upon the price that he is willing to pay for such prospects.

In the case of a growth company, we should recommended payment of a premium for the growth potential not to exceed about 50% of the value determined without it.

Such a rule would result at times in the missing of an unusually good opportunity.

More often, it would mean the investor's saving himself from "going overboard" on an issue that looked especially good to him and everyone else and consequently was selling much too high.

The choice between the attractive issue that turns out well and the one that does poorly is by no means easy to make in the growth-stock field.

However, superior results may be obtained in this field if the choices are competently made. Even with careful selection, some of the individual issues may fare relatively poorly.

Thus for good results in the growth-stock field there is need not only for skillful analysis but for ample diversification as well.

Summary

The enterprising investor may properly buy growth stocks.

He should beware of paying excessively for them, and he might well limit the price by some practical rule.

A growth-stock program will not be automatically successful; its outcome will depend on the foresight and judgement of the investor or his advisers rather than on any clear-cut methods of analysis.

Benjamin Graham

Intelligent Investor

Thursday, 15 January 2015

Broader implications of adopting a sound investment policy

Investment policy, as it has been developed and taught by Benjamin Graham, depends in the first place upon a choice by the investor of either the defensive (passive) or aggressive (enterprising) role.

The aggressive investor must have a considerable knowledge of security values - enough, in fact, to warrant viewing his security operations as equivalent to a business enterprise.

There is no room in this philosophy for a middle ground, or a series of gradations, between the passive and aggressive status.

Many, perhaps most, investors seek to place themselves in such an intermediate category; in our opinion that is a compromise that is more likely to produce disappointment than achievement.

It follows from this reasoning that the majority of security owners should elect the defensive classification.

The enterprising investor may properly embark upon any security operation for which his training and judgement are adequate and which appears sufficiently promising when measured by established business standards.

Benjamin Graham

The Intelligent Investor

The aggressive investor must have a considerable knowledge of security values - enough, in fact, to warrant viewing his security operations as equivalent to a business enterprise.

There is no room in this philosophy for a middle ground, or a series of gradations, between the passive and aggressive status.

Many, perhaps most, investors seek to place themselves in such an intermediate category; in our opinion that is a compromise that is more likely to produce disappointment than achievement.

It follows from this reasoning that the majority of security owners should elect the defensive classification.

- They do not have the time, or the determination, or the mental equipment to embark upon investing as a quasi business.

- They should therefore be satisfied with the reasonably good return obtainable from a defensive portfolio, and they should stoutly resist the recurrent temptation to increase this return by deviating into other paths.

The enterprising investor may properly embark upon any security operation for which his training and judgement are adequate and which appears sufficiently promising when measured by established business standards.

Benjamin Graham

The Intelligent Investor

Investment in Giant Enterprises. But how successful are they from the standpoint of the investor?

Let us take a look at the top listed companies in the stock market with either the highest assets or highest sales. All of these enterprises have achieved enormous size, and by that token they have presumably made a great success.

But how successful are they from the standpoint of the investor?

What do you mean by success in this context?

"A successful listed company is one which earns sufficient to justify an average valuation of its shares in excess of the invested capital behind them."

This means that to be really successful (or prosperous) the company must have an earning-power value which exceeds the amount invested by and for the stockholder.

$$$$$$

It is evident from an analysis that the biggest companies are not the best companies to invest in, based on the percentage earned on invested capital.