Banks have some discretion in terms of accounting for their bond holdings (which is part of financial assets and liabilities) and treatments for unrealised gains and losses.

- Under IFRS 9 (known as MFRS 9 in Malaysia and SFRS 109 in Singapore), bond investments can be measured at cost (if they are intended to be held to maturity) or at fair values (if they may be sold before maturity).

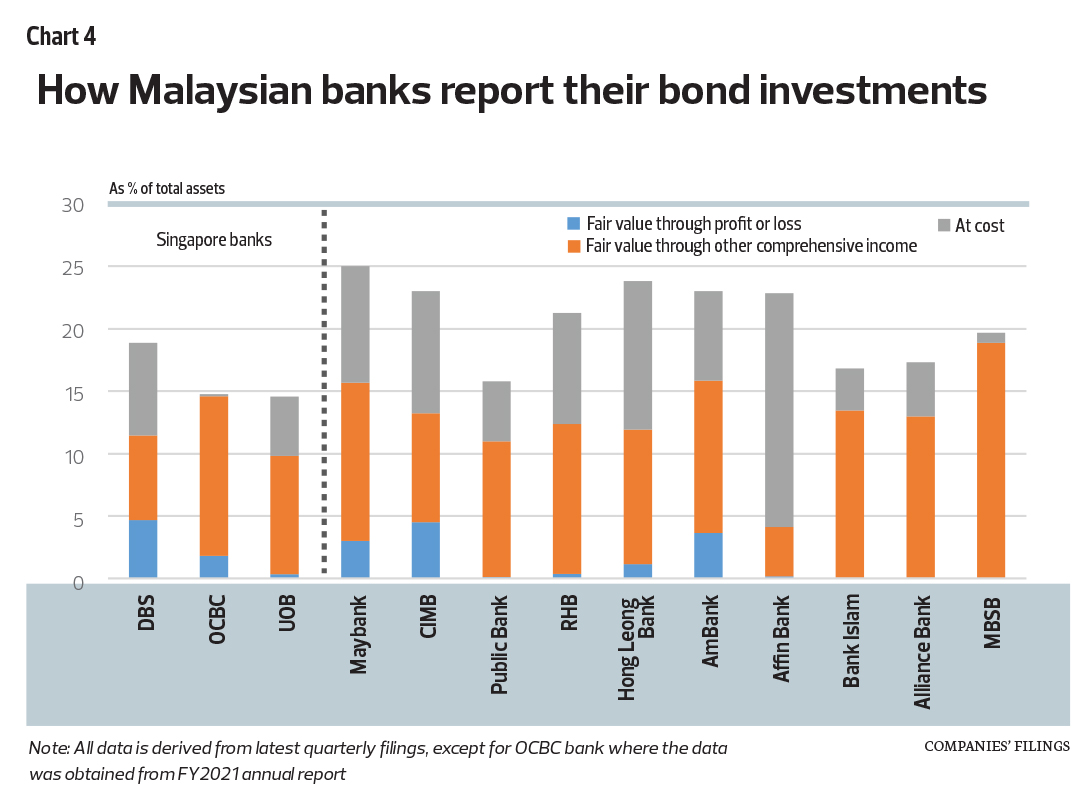

- And there are guidelines for treating changes in fair value measurements — they can be reflected through either the profit and loss (FVTPL) or other comprehensive income (FVOCI).

Under the first option, gains (losses) are recognised in the Income Statements, meaning reported net profit for the period is higher (lower).

Under the second option, gains (losses) are disclosed below the net profit line in the Statements of Comprehensive Income. In this case, the gains (losses) have no impact on reported net profit.

However, both the FVTPL and FVOCI options have balance sheet effects — unrealised gains (losses) will increase (decrease) retained earnings and shareholders’ equity (see Chart 4 for the different approaches in the accounting treatments for bond investments by Malaysian banks).

For instance, Affin Bank and, to a lesser extent, Hong Leong Bank have the highest proportions of bond investments measured at cost, which could indicate that, in the current environment, both their reported net profit and equity may be “overstated”. By comparison, the other seven local banks have, on average, mark-to-market some 63% of their bond holdings. In addition, Maybank, CIMB and Ambank would have adjusted their reported profit lower for a portion of these unrealised losses.

As mentioned above, bond holdings that are mark-to-market will affect balance sheets — unrealised losses or impairments will drag on the capital adequacy ratio of banks.

Herein lies the importance of Bank Negara’s more tempered path for interest rate hikes.

- The smaller interest rate hikes mean lower unrealised capital losses, thus limiting the negative impact on lending capacity and/or need to raise fresh capital.

- Smaller interest rate hikes also help keep a lid on the burden for debt servicing, for leveraged households, businesses as well as the government. Government debt and liabilities totalled RM1.5 trillion, or 83% of GDP.

No comments:

Post a Comment