Mon, 23 Mar 2020

KUALA LUMPUR: The double whammy of the Covid-19 outbreak and the oil price crash has dampened investor sentiments around the globe, especially on net export oil-producing economies like Malaysia.

The FBM KLCI has plunged nearly

18% year to date (YTD). Valuation wise,

KLCI’s current price-to-earnings ratio (PER) stood at 14.56 times, representing a 15.1% discount to its 10-year average of 17.15 times.

Simply put, it is the market in which investors, with cash in pockets, could cherry-pick the good bargains.

Since investor sentiment is transient in nature — they come and go like dark clouds, as such we look into how many Malaysian-listed companies lie in the affordable range, to a business-centric and well thought out billionaire investor that has US$1 billion (RM4.43 billion) cash on hand.

According to Bloomberg data, there are about 868 companies which market capitalisation (cap) is at or below US$1 billion.

Big caps at discount on valuation

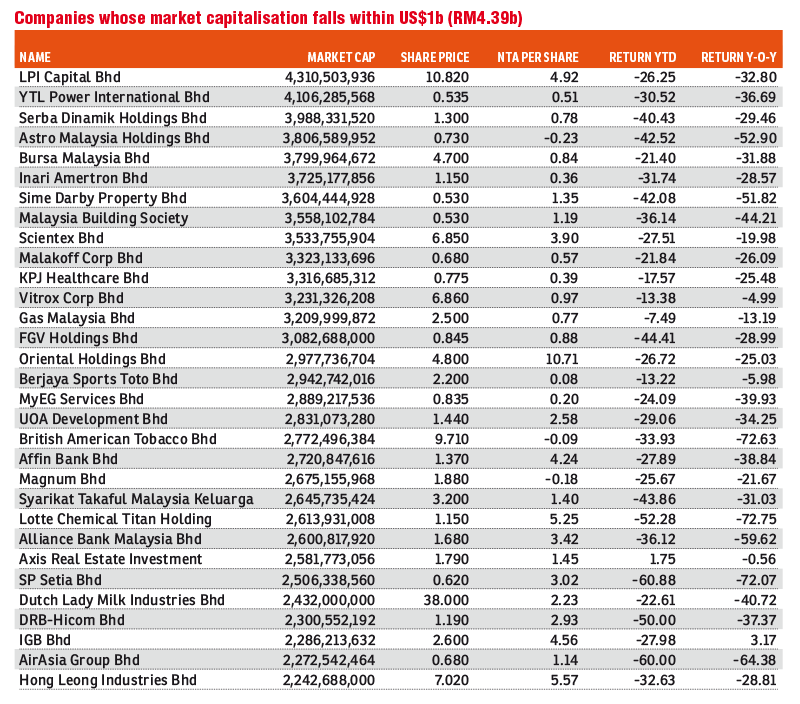

There are 31 big-cap companies, which market cap is in between the US$500 million to US$1 billion categories.

The stock exchange, Bursa Malaysia Bhd, is among the 31 listed entities.

Bursa Malaysia closed at RM4.70 last Friday after it rebounded 28 sen or 6.33%, giving it a market cap of RM3.79 billion, less than US$1 billion. The stock exchange is trading at PER at 20.45 times compared with its 10-year average of 23 times

LPI Capital Bhd, which sits on top of the list, came in at a total market cap of RM4.31 billion. The home-grown insurer last closed at RM10.82 as of last Friday — indicating its current

PER valuation stood at 13.37 times, representing a 23% discount to its five-year average PER of 17.38.

With US$1 billion in hand, the billionaire investor can even afford to buy out utility companies, namely

YTL Power International Bhd (RM4.1 billion),

Malakoff Corp Bhd (RM3.32 billion) and

Gas Malaysia Bhd (RM3.21 billion).

The three utility giants’ stock price fell in the range of

7% to 30% YTD, to close at 53.5 sen, 68 sen and RM2.50 last Friday.

Shares in

Astro Malaysia Holdings Bhd saw its price dropped by more than half year-on-year (y-o-y) to 73 sen, valuing it with a total market capitalisation of RM3.81 billion. The stock is currently trading at a PER valuation of 5.98 times, according to Bloomberg. The media stock’s PER valuation is indeed at a

73% discount to its five-year average PER of 22.3 times.

It is worth noting that many of these companies are

trading substantially lower than their net asset values. The list of companies includes

Malaysia Building Society Bhd, FGV Holdings Bhd, Oriental Holdings Bhd, Affin Bank Bhd, Lotte Chemical Titan Holding Bhd, Alliance Bank Malaysia Bhd, DRB-Hicom Bhd and AirAsia Group Bhd.

A random check on all the stocks’ valuation, in comparison to end-October 2008 period (the heights of the global financial crisis),

four out five of the stocks have suffered lower PER valuation during the 2008 selldown period.

Mid-large cap choices

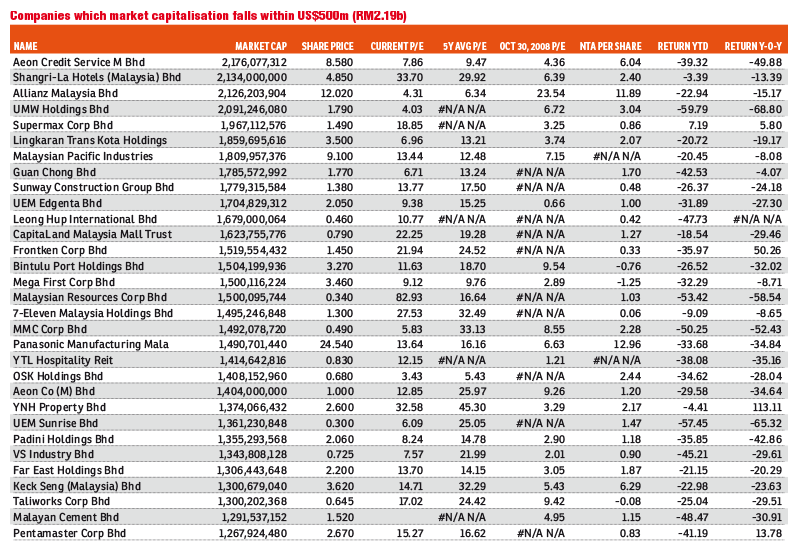

There are 124 companies that are valued between US$100 million and US$500 million.

A billionaire investor, who has US$1 billion in hand, could afford a buyout of some oil and gas giants,

Bumi Armada Bhd, Velesto Energy Bhd and Sapura Energy Bhd, which have been succumbed to irrational selldown after the meltdown on the crude oil prices.

Remarkably, shares in

Supermax Corp Bhd was the only one yielded positive among the top-31 companies within the category. Supermax which

gained 7% YTD, closed at RM1.49 last Friday — valuing the rubber glove maker at RM1.96 billion. Valuation of Supermax which was widely viewed as one of the beneficiaries for the pandemic containment efforts stood at 18.85 times PER, 33% higher than its 10-year average of 14.18 times.

Companies that sit

above the RM2 billion mark within this category include

Aeon Credit Service (M) Bhd, Shangri-La Hotels (Malaysia) Bhd, Allianz Malaysia Bhd and UMW Holdings Bhd — which saw their

share price slid between 13% to 68% y-o-y.

In particular,

Aeon Credit is trading at a single PER of 7.86 times based on last Friday’s closing of RM8.58. The valuation is at a

17% discount to its five-year average of 9.47 times.

While

Shangri-La Hotels’ stock price was holding up strong at RM4.85 despite the concern on the Covid-19 outbreak that will affect occupancy rate. The five-star hotel group is trading at

PER of 33.7 times, which is a 12% premium to its five-year average of 29.92 times.

Meanwhile,

Allianz Malaysia, which used to trade above six times average PER in the past five years, is currently trading at a

32% discount at 4.31 times PER at RM12.02. Interestingly, Allianz’s net tangible assets

(NTA) currently worth about RM11.89 per share — indicating that the investor gets to own 98% of the tangible assets for every ringgit invested into the insurance company.

Some of the notable

consumer-related companies within

US$100 million-US$500 million market cap range, includes

Guan Chong Bhd (RM1.78 billion), Leong Hup International Bhd at RM1.68 billion, 7-Eleven Malaysia Holdings Bhd (RM1.49 billion), Aeon Co (M) Bhd (RM1.40 billion) and Padini Holdings Bhd (RM1.35 billion), which saw their

share price tumbled 9% to 47% YTD. This group of companies, except for Leong Hup which was newly listed last year, were trading below their five-year average PERs.

Among the semiconductor companies that are within

US$100 million and US$500 million range, Malaysian Pacific Industries Bhd (RM1.81 billion) was the only one traded at a premium to its historical values, which stood at 13.44 times PER, representing a 7% premium relative to its five-year average of 12.48 times.

Meanwhile,

Frontken Corp Bhd, VS Industry Bhd and Pentamaster Corp Bhd are all traded at a discount to their historical values. Their share prices had plummeted 20% to 45% YTD.

Cheaper companies but cheaper quality

With US$1 billion in hand, billionaire investors will be

spoilt for choice at bargain prices for stocks with a market cap of US$100 million or less.

There are

713 companies valued at below US$100 million, based on last Friday’s closings, according to Bloomberg.

Out of the top 31 market cap companies within this category, there are

five loss-making companies.

Interestingly, companies in which NTA is significantly higher than their respective share prices include

MNRB Holdings Bhd, MPHB Capital Bhd, Sunsuria Bhd, Muhibbah Engineering (M) Bhd, Malayan Flour Mills Bhd, Can-One Bhd. Share prices in these companies have

tumbled 25% to 66% YTD.

MNRB’s NTA at RM2.97 per share is about close to five times higher than Friday’s closing price of 52 sen. While

Can-One’s NTA stood at RM9.01 per share, close to four times higher than its share price of RM1.93, and

MPHB’s NTA of RM1.88 per share is more than two times higher than its last trading price of 56.5 sen.

In terms of price valuation, all of the companies were

traded below their five-year average PER, except for

Amverton Bhd and Ayer Holdings Bhd which are both involved in property development.

Amverton, which has a valuation of RM438 million, saw its share price closed at RM1.20 — implies

current PER of 85 times, three times higher than its five-year average of 28 times.

Ayer Holdings current

PER stood at 29 times, representing 22% higher than its five-year average of 23 times, as of last closing price of RM5.20, valuing the company at RM389 million total market capitalisation.

https://www.theedgemarkets.com/article/more-700-companies-valued-below-us100-million-bursa