For a quick recap, Silicon Valley Bank (SVB) became the second-largest bank to fail in US history, the biggest being Washington Mutual Bank in 2008, following a run on the bank.

What happened?

SVB had an abnormally high percentage of bond holdings (56% of total assets) on its balance sheet and as unrealised losses mounted, worried depositors — mostly Silicon Valley start-ups and venture-capital firms with large, uninsured deposits (of more than US$250,000 per account) — rushed to withdraw their money.

The sudden huge outflow of deposits forced SVB to liquidate its bonds at current market values (losses), which then tipped it into insolvency (where the values of liabilities exceeded assets).

The bank had to be taken over by FDIC on March 10 to stem contagion fears.

Another regional bank, Signature Bank, suffered the same fate and went into FDIC receivership just days later.

Despite the quick actions, worries continued to spread to other smaller banks, all of which continue to suffer substantially higher-than-normal deposit withdrawals.

https://www.theedgemarkets.com/node/662043

The issues for SVB are, to a certain extent, idiosyncratic —

- an exceptionally narrow customer base and

- high uninsured deposits (according to various reports, they ranged from 88% to 96% of total deposits),

- abnormally high long-dated bond holdings relative to traditional loans and,

- critically, failure to hedge interest rate risks.

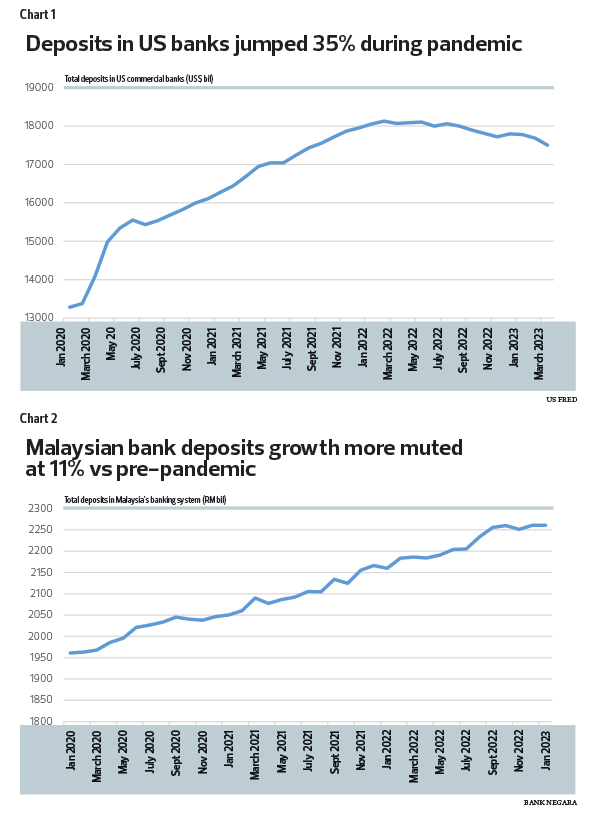

The overall US banking system is, no doubt, suffering from withdrawal symptoms — from excessive government stimulus, near-zero interest rates and massive quantitative easing over the past few years. At the outset of the pandemic, banks were inundated with large deposit inflows — excess savings surged from generous government handout, coupled with little avenue to spend during lockdowns.

Bank deposits increased by nearly US$5 trillion, or 35%, from about US$13.4 trillion in March 2020 to US$18.1 trillion in March 2022 (see Chart 1). Meanwhile, loans to businesses were limited during the pandemic. Banks had to put all these excess cash to work, and many ended up buying Treasuries and especially MBS (new mortgages and refinancing activities saw a huge jump as the housing sector boomed). Then the Fed started hiking interest rates aggressively.

Situation in Malaysia is quite different

Clearly, the situation is quite different in Malaysia.

For starters, pandemic cash handouts were far smaller and, while deposits also rose during the pandemic — owing to loan moratoriums and lower spending — it was nowhere near the scale of that in the US.

Total deposits increased from RM1.968 trillion to RM2.186 trillion between March 2020 and March 2022, or equivalent to just about 11% growth (see Chart 2).

No comments:

Post a Comment