Know what you are buying – investment products, insurance and mutual funds.

Elaboration of Section 30

This section serves as a crucial consumer protection and due diligence guide. It warns investors to look beyond the marketing name of a financial product and understand its underlying mechanics, costs, and true purpose. The core message is that complexity and opacity are often used to hide poor value.

1. Scrutinizing Investment Products: The "Capital Guaranteed" Trap

The section uses the example of "Capital Guaranteed Funds" to illustrate a common pitfall.

The Alluring Name: The name suggests absolute safety of your principal.

The Ugly Reality: Upon investigation, the product structure often reveals that 90% of your capital is invested in safe, low-return government bonds (which actually provide the guarantee), and only 10% is invested in equities.

The Problem: After accounting for high sales charges and management fees, the potential upside from the tiny equity portion is so minimal that the investor would likely have been better off simply putting their money in a fixed deposit. The lesson is to always look under the hood and understand the asset allocation and fee structure.

2. The Right Role for Insurance: Protection, Not Investment

This part delivers a clear, rule-based distinction:

Buy Insurance for PROTECTION: The primary purpose of insurance is to cover catastrophic, unforeseen financial losses (e.g., death, critical illness). For this, term insurance is the most efficient and affordable product because it offers pure protection with no investment component.

Do NOT Buy Insurance for INVESTMENT: Insurance products that combine protection with investment (e.g., endowment, whole life, investment-linked policies) are generally poor investment vehicles. They come with high costs, and the investment returns are often low because the funds are managed ultra-conservatively to meet regulatory and liability requirements. The smart strategy is to "buy term and invest the rest" separately.

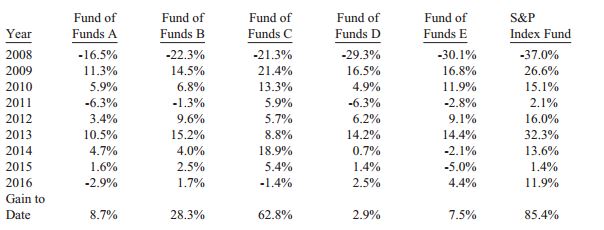

3. Selecting Mutual Funds: Philosophy Over Past Performance

When choosing a mutual fund, the section advises looking beyond recent returns and focusing on the manager's core philosophy.

The Example of Magellan Funds: The section holds up this fund as a model because its stated investment philosophy is a mirror of this entire guide. It explicitly aims to:

Minimize the risk of permanent capital loss.

Find outstanding companies with wide "economic moats."

Buy these companies at a discount to intrinsic value (a Margin of Safety).

The Due Diligence: This means an intelligent investor should read a fund's prospectus and understand its stated philosophy, ensuring it aligns with sound, business-like investing principles rather than short-term speculation.

4. The Critical Factor of Integrity

The section ends by circling back to a theme from Section 23: the paramount importance of integrity. Judging the integrity of a product provider or fund manager is difficult but essential. A lack of integrity means the seller's interests (to earn fees) are not aligned with your interests (to grow wealth). This is why understanding the product structure and philosophy yourself is a non-negotiable form of self-defense.

Summary of Section 30

Section 30 is a practical guide to financial self-defense, warning investors to thoroughly understand any financial product before buying it and to use different products for their intended purposes.

Investment Products: Look beyond the name. Analyze the underlying structure and fees. Often, "safe" products are structured in a way that offers minimal real return after costs.

Insurance: Use it for protection only. Buy affordable term insurance for pure financial protection. Avoid using insurance as an investment vehicle, as it is a costly and inefficient way to build wealth.

Mutual Funds: Judge the philosophy, not just the performance. Select funds whose stated investment philosophy aligns with value investing principles—seeking quality businesses with a margin of safety.

The Overarching Principle: The biggest risk is often buying something you don't understand. Complexity is frequently used to obscure poor value and high costs. The intelligent investor's duty is to perform this due diligence to ensure their capital is deployed efficiently and in alignment with their goals.

Comment

Comment