On February 28, 2026, the EPF declared a dividend rate of 6.15% for both its Conventional and Shariah schemes for the financial year ended December 2025. This resulted in a record total payout of RM79.6 billion.

Key Drivers of Performance

Income Growth: Total distributable income rose by 9.5% to RM82.7 billion, driven by resilient equity markets and a diversified portfolio strategy.

Equities Lead: Equities were the primary income generator, contributing RM50.7 billion (64% of total investment income).

Stability from Fixed Income: Fixed income instruments (mainly Malaysian Government Securities) provided a stable anchor, contributing RM26.3 billion.

Strategic Asset Allocation The fund's ability to navigate market volatility was attributed to its diversified approach:

Equities: 46.1%

Fixed Income: 44.7%

Real Estate & Infrastructure: 6.0%

Money Market: 3.2%

Global vs. Domestic Performance

Domestic Investments: Represented 61.7% of total assets, generating RM39.3 billion in income.

Global Investments: Made up 38.3% of the portfolio but outperformed slightly, contributing RM39.9 billion (50.4% of total investment income). Returns were moderated by the strengthening Ringgit.

Top Portfolio Holdings & Strategic Shift A review of the EPF's top equity holdings revealed a strategic realignment:

New Entry:Hong Leong Bank ($HLBANK (5819.MY)$) replaced Gamuda ($GAMUDA (5398.MY)$) in the top ten, signaling continued confidence in the financial sector.

Top Holding:Tenaga Nasional ($TENAGA (5347.MY)$) retained its position as the single largest equity holding, reflecting a preference for stable, defensive counters.

Banking Dominance: Banking stocks (Maybank, Public Bank, CIMB, and the newly added Hong Leong Bank) continue to dominate, suggesting the EPF is positioning for resilient dividend income and upside from Malaysia's economic growth.

This section is a curated collection of external articles and insights that provide practical, real-world guidance for managing EPF savings at retirement. It moves from general principles to specific considerations, helping an individual make an informed decision about whether to withdraw their EPF as a lump sum or leave it in the fund.

The section synthesizes several key themes from the provided articles:

1. The Lump-Sum vs. Flexible Withdrawal Dilemma The first article presents the core decision and outlines five critical questions to ask oneself, directly applying the concept of "Knowing Yourself" from Section 2:

Your Behavior with Money: Are you an emotional spender? If so, a large lump sum could lead to impulsive, big-ticket purchases. A flexible (partial or monthly) withdrawal is safer.

Your Ability to Generate Higher Returns: This is the fundamental financial question. Can you or your fund manager consistently beat EPF's ~5-6% dividend? If not, leaving the money in EPF is the smarter choice. One must also factor in the fees of financial advisors.

Your Debt Situation: If you have high-interest debt (credit cards, personal loans), it may be wise to withdraw a lump sum to pay it off, as the interest saved is a guaranteed, high return.

Your Desire for Control: Do you want full control over your retirement funds to invest as you see fit, or are you comfortable with EPF's management? Withdrawal offers control but also demands more personal responsibility and financial knowledge.

Your Draw-Down Plan: If you take a lump sum, how will you access the money to fund your retirement? You need a structured plan (e.g., quarterly redemptions, an annuity) to avoid outliving your savings.

2. The Challenge of Sustaining High EPF Dividends The second article provides a crucial reality check from an economist's perspective. It explains that EPF's ability to pay high dividends is not guaranteed and is tied to macro-economic factors:

External Vulnerabilities: As a large, open economy, Malaysia's financial market is influenced by global events (e.g., struggles in Europe or the US). This can make "paying consistently high dividends challenging."

Economic Link: EPF dividends correlate with the country's GDP growth. In a moderate growth environment, dividends may ease to a long-term average of around 4-5%.

Investment Challenge: EPF faces the immense task of profitably investing the RM10-12 billion in net new contributions it receives each year.

3. The Critical Need for a Retirement Income Strategy The final linked article delivers a powerful message about the shifting landscape of retirement planning:

The "Retirement Risk Zone": The years immediately before and after retirement are the most critical. Making a mistake here (like taking excessive risk or having no income plan) can force people to delay retirement or return to work.

Shift in Mindset: Investing in retirement is different from investing for retirement. The focus must shift from growth and accumulation to income, preservation, and controlled spending.

The New Rule: The old rule of relying on "safe" cash and bonds no longer works because their returns are often below inflation. Retirees must now accept "rather more risk" and invest differently to ensure their money lasts for a potentially 30-year retirement.

Summary of Section 14

Section 14 provides a practical decision-making framework for managing EPF savings at retirement, emphasizing that the "safe" choice of leaving funds in EPF is often the most intelligent one for the majority of retirees.

Core Decision: The choice between a lump-sum or flexible EPF withdrawal hinges on personal factors: financial discipline, investment skill, debt levels, and desire for control.

The Default Recommendation: For most people, especially those without advanced investment knowledge, leaving savings in EPF is the superior and safest strategy. It offers a strong, relatively safe return that is difficult for the average investor or even many professionals to beat consistently after fees.

A Reality Check: EPF's high dividends are subject to economic cycles, and a long-term average of 4-5% is a more realistic expectation than consistently high payouts.

The Bigger Picture: Retirement planning requires a shift from accumulation to a sustainable draw-down strategy. The old rules of relying solely on cash and bonds are broken due to inflation, requiring retirees to adopt more nuanced, income-focused investment approaches to prevent outliving their savings.

In essence, this section reinforces the conservative, safety-first principle of intelligent investing. It strongly suggests that for the defensive investor, the EPF is not just a savings vehicle but a premier, low-cost, professionally-managed "fund" that should form the bedrock of their retirement income plan.

Section 12: Discussions on retirement investing & EPF.

Elaboration of Section 12

This section presents a practical, real-world discussion among the group members, centered on a crucial question for Malaysian retirees: What should I do with my EPF (Employees Provident Fund) savings upon reaching the withdrawal age? The conversation moves from a simple question to a nuanced analysis, applying the principles discussed in earlier sections.

1. The Core Dilemma: To Withdraw or Not to Withdraw? The discussion is triggered by a member asking whether it's wise to leave his EPF savings in the fund to continue earning its historically higher dividends (5-6%) compared to the "paltry interest" from Fixed Deposits (FDs).

2. The Key Factors in the Decision The responses highlight that there is no one-size-fits-all answer. The decision must be based on a personal assessment, echoing the themes of Section 2 (Knowing Yourself):

Financial Situation & Objectives: The first response correctly states that the answer depends entirely on the individual's financial picture, including other assets, debts, and income needs.

Risk and Return Analysis:

EPF's Allure: EPF is presented as a virtually risk-free investment that has consistently delivered returns (~5-6%) significantly higher than FDs (~3.5%). The power of compounding this small percentage difference over many years is substantial.

The Justification for Withdrawal: The key insight is that if you withdraw from EPF to invest in riskier assets like stocks, you should have a compelling reason. Specifically, you should aim for a potential return that is at least twice what EPF offers (e.g., 10-12%+) to justify taking on the additional risk. If you cannot confidently achieve this, leaving the money in EPF is the wiser choice.

Alternative Uses for the Money: Withdrawing makes sense if the capital can be used for other high-impact financial goals, such as:

Paying down high-interest debt (e.g., credit cards).

Making a down payment on a property to avoid a large mortgage.

3. Advice for the Less Knowledgeable Investor A clear and cautious path is outlined for those who admit they are not financially astute:

Default Option: For the risk-averse or financially inexperienced, the safest and most recommended option is to leave the money in EPF. It offers a superior return to FDs with a similar level of safety.

The Buffett Endorsement: One member reinforces this by pointing out that even Warren Buffett advises his wife's inheritance to be put into a low-cost index fund. This is because most active fund managers fail to beat the market, and for a non-expert, trying to pick stocks is likely to result in losses.

The Importance of Diversification: The warning is given against putting "all your eggs in one basket," even if that basket is cash. A balanced asset allocation is still necessary.

4. "OPM" Strategy A member shares a behavioral and risk-management strategy:

Concept: Use a small portion of capital (e.g., RM100,000) to invest. Once a profit (e.g., RM10,000-RM20,000) is made, return the original capital to a safe FD.

Psychological Benefit: The investor then continues trading only with the "Other People's Money" (OPM)—the profits. This eliminates the stress of losing one's original capital, as any subsequent losses are only from the gains, not the principal.

5. The Power of Compounding and Starting Early The discussion concludes with a powerful reminder of Section 5 and 28, emphasizing that the real secret to the success stories (like Uncle Chua) is regular investing and long-term compounding. This strategy is best started young, but the principles of patience and discipline are valuable at any age.

Summary of Section 12

Section 12 is a practical discussion analyzing whether to withdraw EPF savings at retirement, concluding that for most, leaving funds in EPF is the best default option unless they have the skill to generate significantly higher returns elsewhere.

The Safe Bet: For the majority, especially those who are not investment experts, leaving savings in EPF is the most prudent choice. It offers an excellent balance of high safety and returns that outpace inflation and fixed deposits.

The Bar for Withdrawal: You should only withdraw EPF funds to invest in the stock market if you are confident you can achieve returns at least twice that of EPF (e.g., >10-12% annually) to justify the extra risk.

A Behavioral Strategy: The "OPM" (Other People's Money) method is suggested as a way to de-risk speculative investing by only risking profits, not original capital.

The Ultimate Lesson: The conversation underscores that successful wealth-building is not about brilliant, one-time decisions but about the disciplined, long-term compounding of savings in a safe and productive vehicle, with EPF serving as a prime example for defensive investors.

In essence, this section applies the theoretical framework of intelligent investing to a critical real-life decision for Malaysian retirees, providing a clear, reasoned flowchart for action: When in doubt, trust the proven, low-risk compound growth of EPF.

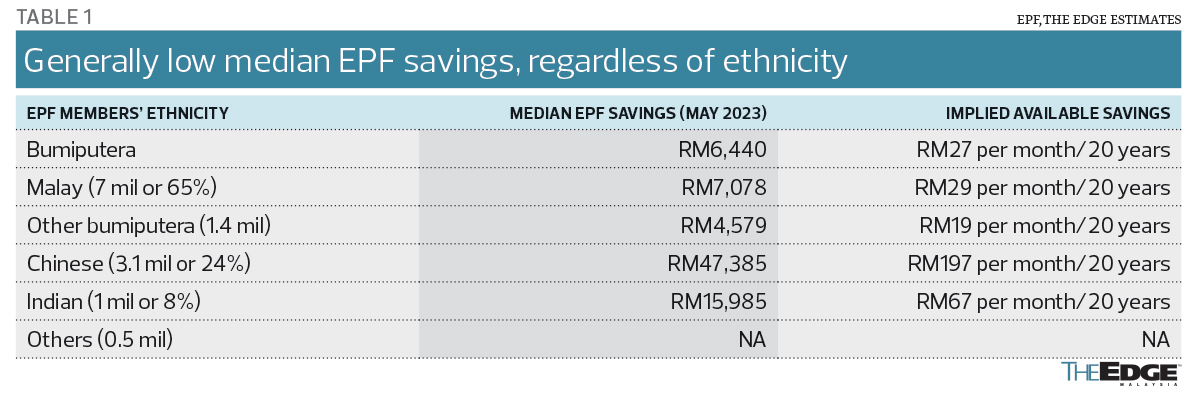

THE low level of retirement savings among Malay and other bumiputera private sector wage earners compared with their fellow Malaysians of Chinese and Indian ethnicity recently made headlines when lawmakers provided such numbers in parliament when arguing against more premature withdrawals of statutory retirement savings from the Employees Provident Fund (EPF).

While the median savings among EPF members of Chinese and Indian ethnicity in May 2023 were higher than that of Malays and other bumiputera, the reality is that the median EPF savings is low even among the Chinese, who make up about 24% of the provident fund’s membership.

According to EPF data, the median savings among the 3.1 million Chinese EPF members was RM47,385 as at May 2023, which works out to only RM197 per month for 20 years. That is just under one-fifth of the prevailing minimum civil service pension of RM1,000 a month — hardly enough to get by, even though the figure looks high when stacked against the median savings of RM7,078 (RM29 a month for 20 years) among the seven million Malay EPF members.

Savings adequacy is also a concern among the one million EPF members who are of Indian ethnicity, even though their median savings of RM15,985 (RM67 a month for 20 years) is above that of the median savings of RM4,579 (RM19 per month over 20 years) among the 1.4 million non-Malay bumiputera EPF members (see Table 1).

That median EPF savings of Malay members are higher than that of non-Malay bumiputera should not cloud the fact that the median savings of all ethnicities point to a serious need to shore up savings adequacy.

With only 19%, or 2.5 million, of the 13.3 million EPF members meeting the EPF’s basic savings by age, not all 3.1 million Chinese EPF members automatically have enough to retire. In short, ethnicity has scant meaning on one’s adequacy of retirement savings relative to more useful details like age, trajectory of wages, education, skills and the industries the EPF members are in.

Experts generally agree that the low level of EPF savings has much to do with low income. Rather than dwelling on ethnicity, policy action that focuses on upskilling and creating higher-income jobs and raising economic complexity should result in greater productivity and higher wages for all Malaysians.

Summary of EPF’s 2022 Investment Performance; EPF’s Dividend Chart from 2010 until 2022; and EPF’s Investment Assets as at 31 December 2022.

Tables of EPF Year-To-Date December 2022 Members/Employers Registration; Savings of EPF Members by Age Group (as at 31 Dec 2022); Savings of EPF Members by Race Group (as at 31 Dec 2022).

Savings of EPF Members by Savings Level Group (as at 31 Dec 2022).

There are many people who believe that stock investing can generate double-digit returns, which is higher than the 10-Year Dividend Yield Average of 6.17% per annum EPF return from 2010 to 2019.

So, is stock investing really better?

Firstly, in stock investing, the 10+% returns are not cash-based as delivered by the EPF and often, it refers to trading gains that are derived from buying stocks at low prices to selling them at higher prices later.

Thus, this 10+% returns are not guaranteed, predictable, or even recurring in nature.

Secondly, if you do not study a stock’s business model, financial results, and future plans before investing in it, and instead buy stocks because you anticipate they will rise in the future, then you are not investing but betting.

Lastly, it is one thing to make 10+% in returns in one year but a different feat if you can replicate this success and make 10+% in returns consistently every single year.

The keyword here is “consistency”.

So how does EPF invest your money to continue declaring future dividends?

This article sheds light, along with pointers on how you can build a stock portfolio for consistently attaininghigher returns than the EPF.

1: EPF’s Strategic Asset Allocation (SAA)

The EPF employs its SAA as a framework to optimise its long-term investment returns. The EPF allocates:

51% of its total investments into Fixed Income Instruments for capital preservation,

36% into Equities to grow its returns,

10% into Real Estate to hedge against inflation and

the remaining 3% is into Money-Market Instruments to fund its day-to-day operations.

In essence, it is likened to a person who has RM100,000 in capital to invest and parks

RM51,000 into FDs,

RM36,000 into stocks,

RM10,000 into REITs and

the final RM3,000 is left in his savings account for living expenses.

2: EPF invests primarily for income (cash flow)

The EPF has multiple recurring sources of income from its investment assets. They include

interest income from fixed income instruments,

dividend income from equities, and

rental income from real estate.

Combined, the amount of its recurring income has increased from RM16.2 billion in 2009 to RM32.6 billion in 2018.

They have contributed about 65% of EPF’s gross investment income for the past 10 years, which is key to its investment success and consistent delivery of the 6+% in annual dividends to its contributors.

EPF’s income flow from its investments.

3: EPF’s stock portfolio

The EPF built itself a global portfolio worth RM300 billion in 2018 where its key markets were in Malaysia, Hong Kong, USA and Singapore.

The following can be concluded by just focusing on the EPF’s top 30 equity holdings in Bursa Malaysia.

• Sector selection

The EPF places great emphasis on stocks that are cash cows. This is evident as it is the largest investor in Malaysia’s finance sector with 9/30 finance stock such as RHB, MBB, PBB and CIMB.

It also has a focus on the palm oil sector and telecommunication stocks, which are basically income and cash flow orientated.

• Holding period

The EPF has held onto 28 of these stocks for more than 10 years. It intends to earn dividend income from these stocks, which is a vital source of income for allowing EPF to pay recurring dividends to its contributors.

• Financial results

However, out of its 30 stocks invested, only 12 have generated a consistent increase in earnings for the long-term (five-10 years). The other 18 stocks have experienced a fall in earnings during the period. This leads to the next point:

• Stock price movements

The 12 that had consistent growth in earnings have enjoyed sustainable capital appreciation in the 10-year period, except for MBB for it has DRIP which requires a different way of assessing one’s total investment returns.

Stock prices of KL Kepong, Sime Darby Plantation and IOI Corporation had been flat.

The chart shows how the stocks have fared over the last 10 years.

How EPF’s stocks have fared over 10 years.

4: What works for EPF’s stock investments?

If you look at the 12 stocks that have appreciated in 10 years, the common ground is that these stocks have achieved consistent growth in profits.

Consistent growth in profits lead to a stock’s consistent growth in its stock prices. That is, in essence, value investing 101.

5: Should you keep your money in the EPF?

Based on financial reports, EPF has built a diversified portfolio of assets that are cash-flow orientated.

With continuous contributions from existing contributors and its dividends reinvested into the fund, EPF’s ability to continue making consistent dividends to contributors is intact.

Hence, if you don’t know how to invest, it would be better to just leave the money in EPF and enjoy the annual dividends.

What you can do is diversify a portion of savings into unit trust funds via i-Invest and collect not only 6+% in net dividend yields from the EPF, but also capital gains.

With that said, capital gains are not guaranteed, and you might incur capital losses instead if the funds fail to do well.

So, whether you can invest in the stock market and beat EPF’s returns depends on how good you are as a stock investor.

Most treat stocks like lottery tickets and invest in the hope that they will magically increase in price. It is, of course, flawed thinking.

KUALA LUMPUR (Bernama): The Employees Provident Fund (EPF) has declared a dividend rate of 6.15% for Conventional Savings 2018, with payout amounting to RM43bil and 5.9% for Shariah Savings 2018, with a payout amounting to RM4.32bil.

In total, the payout for 2018 amounts to RM47.32bil, a marginal decrease of 1.7 per cent from 2017.

"With a real dividend of 3.93 per cent for Simpanan Konvensional and 3.68% for Simpanan Shariah on a rolling three-year basis respectively, the EPF has exceeded its mandate of delivering a dividend of at least 2.5% on a yearly basis and at least 2.0% real dividend on a rolling three-year basis," the EPF said in a statement on Saturday (Feb 16).

"We are very grateful and pleased that we have been able to consistently meet our two strategic investment targets. Beyond the anticipated nominal dividends, more importantly is that we consistently deliver above-inflation returns so that we are able to preserve and enhance the value of our members' savings over the long term and help them achieve a better retirement future," its chairman, Tan Sri Samsudin Osman said.

"Nonetheless, we remained focused on our long-term strategy and our portfolio diversification has provided resiliency and delivered commendable returns to our members," he said.

Gross investment income for 2018 was RM50.88bil, out of which a total of RM4.62 billion was attributed to Shariah Savings, proportionate to its share of total Shariah assets, while RM46.26bil was attributed to Conventional Savings.

The lower income for EPF's Shariah portfolio in 2018 was due to the underperformance of the telecommunications, construction and oil and gas sectors in the domestic portfolio.

The dividend payout for each account was derived from total gross realised income for the year after deducting the net impairment on financial assets, unrealised gains or losses from intercompany transactions, investment expenses, operating expenditures, statutory charges, as well as dividend on withdrawals.

The payout amount required for each 1.0% of the dividend in 2018 was RM7.72bil, which is higher compared with RM7.02bil in 2017.

In accordance with the implementation of the Malaysian Financial Reporting Standards 9 (MFRS 9), which came into effect beginning Jan 1, 2018, capital gains on disposal of equity amounting to RM18.21bil for 2018 will flow directly to Retained Earnings from the Statement of Other Comprehensive Income, instead of the Statement of Profit and Loss as under the previous MFRS 139.

In addition, under MFRS 9, the EPF will no longer recognise any impairment on its listed equity holdings, he added. - Bernama

EPF proven to be successful retirement funds globally — CIMB

February 12, 2018, Monday

KUALA LUMPUR: The Employees Provident Fund (EPF) has proven to be one of the most successful retirement funds globally, said CIMB Group.

Its Group chief executive, Tengku Datuk Seri Zafrul Aziz said the commendable dividend rate is truly reflective of a well-diversified investment strategy.

On Saturday, EPF declared a dividend rate of 6.9 per cent for conventional accounts for 2017, with a payout amounting to RM44.15 billion and 6.4 per cent for Simpanan Shariah for 2017, with payout amounting to RM3.98 billion. Zafrul said CIMB also strongly supports EPF’s cause to make retirement a mainstream topic so that more youths could plan for it, whether through the EPF or Private Retirement Scheme, as soon as they start working. — Bernama

==

EPF eyes Latin America as new investment destination

February 13, 2018, Tuesday

KUALA LUMPUR: The Employees Provident Fund (EPF) is eyeing expansion into the Latin American market as part of its efforts at boosting its global assets portfolio to 32 per cent this year from 28 per cent in 2017.

Chief executive officer, Datuk Shahril Ridza Ridzuan, said an increase in the overseas asset portfolio would provide the fund with the necessary diversification and returns to meet contributors’ expectations.

“Like many global pension funds, we need to have a balanced portfolio and increase its exposure as much as possible to growth around the world,” he told reporters at the fund’s 2017 dividend briefing yesterday.

He said overseas investments also provided high returns, contributing 41.4 per cent of the total income, despite only making up of only 28 per cent of total investments last year.

“Our historical chart has shown that global assets give us the necessary diversification and exposure to growth, which is vital for the fund to continue to perform and provide the kind of return that our members expect,” he said.

He said diversification into overseas markets also helped the fund compensate for any downturn in any of its investment market and continue to grow.

As of last year, EPF has presence in 30 markets, primarily in the developed market, North Asia and Asean.

On Shariah Savings, Shahril said, they had, as of last year, attracted about 700,000 contributors with a total size of RM68 billion from RM100 billion allocated for the savings.

The total Conventional Savings and Shariah Savings have about 14 million contributors and total fund size of RM768.51 million, he said. He said Shariah assets made up 47.5 per cent of the fund’s total asset exposure and contributed 42.9 per cent of total income last year.

“Shariah investments’ underperformance was attributed to oil and gas and mobile telecommunication sectors,” he said.

Nevertheless, he said, Shariah investments contributed 36 per cent to conventional savings dividend distributions on top of 100 per cent contributions to Shariah savings.

On Saturday, EPF announced 6.9 per cent dividend for conventional savings with a payout amounting to RM44.15 billion and 6.4 per cent dividend to Shariah savings, with payout amounting to RM3.98 billion. — Bernama

Amongst the millions of questions regarding financial matters, the most popular one is undoubtedly “How do I save my money?”. Here are 3 common ways that could help you save a sizable amount for when it’s time to retire.

1) Contribute to EPF, do NOT withdraw

For Malaysians, EPF is undoubtedly the easiest way to save your money. Your personal contribution of 11% aside, your employer’s mandatory contribution of 13% (for employees earning less than RM5,000 monthly salaries) makes it a total of 24% of your monthly wages saved under your name each and every month.

To top it off, EPF’s average return of 5% per year is significantly higher than any fixed deposit interests in the market right now.

Tips: Firstly, get employed at a company that contributes to EPF. Try to keep your money in your EPF account for as long as possible because there simply aren’t any other bank deposits with higher interest rates in the market. If you can help it, DO NOT use any of your EPF sub accounts to pay for your home or buy a computer, so you can take full advantage of EPF’s high interest rate to maximize your returns.

2) Put your money aside the good old fashion way

Saving your money requires determination and discipline. If you aren’t already doing so, try putting aside a small percentage of your salary every month-end and save it in a separate bank account, preferably one without any easy withdrawal facilities (eg. ATM).

When you have a moderate amount, transfer the money to a high-interest fixed deposit account so it can generate greater interests whilst stopping you from accessing the funds every time you feel like getting a new handphone or a new pair of shoes.

Tips: Like many other things in life, saving is an endeavour that many find hard to adopt especially in the beginning. To ease yourself into your money-saving journey, you may wish to start off with a moderate amount (say 5-10% of your wages) so that it does not affect your cash flow to the extend of making you give up altogether. Over time, you can try to increase the amount as the act of saving becomes a habit. Also, when it comes to saving, it helps to start as young as possible so you can reap the benefits of compound interest over the long run.

3) Use your money to invest in something

If you have moderate tolerance to risk, are not close to retirement age and have a sizable amount in your savings or fixed deposit account, you’ll probably want to consider using some of the monies you have for investment purposes.

Be it in shares, gold or real estate; investment is a great way to save even MORE money because the potential returns are usually much greater than, say, putting your money into a bank. The downside, however, is that investment involves RISKS – the risk of non-performance from your investments, or in certain cases, the risk of total evaporation of value for your investments caused by adverse market conditions.

Tips: Not all categories of investments are born equal, so you are advised to do your homework well before you engage with any kind of investment. For example: properties are considered medium-risk investments; they generally enjoy consistent growth but they also have low liquidity (i.e. not easily turned to cash). Shares, on the other hand, are considered high-risk investments; they are prone to fluctuations in value caused by volatile market, which basically means you could potentially GAIN a lot or LOSE a lot. Whichever form of investment you choose, it is best to make a genuine effort to learn about it before you commit.

EPF: Lump-sum or partial withdrawals at 55?

Written by Celine Tan of theedgemalaysia.com

Wednesday, 31 August 2011 00:12

KUALA LUMPUR: Upon reaching 55, most people prefer to withdraw all their savings in the Employees Provident Fund (EPF) but more and more people are opting for flexible withdrawals (partial or monthly payments).

According to the EPF, last year, 235,931 employees made withdrawals at age 55 and 70% of the withdrawals were full withdrawals. The number of flexible withdrawals increased by 41.67% to 82,690, compared with 2009.

Choosing between withdrawing a lump sum and making a partial withdrawal depends on many factors. Financial planners say you can ask five questions when crunching the numbers for your retirement plan, not at 55.

1) What is your behaviour towards money?

Your EPF savings can be the single largest disbursement of money you will see in your lifetime. “It is something that most individuals look forward to throughout their working life. It gives them a sense of fulfilment when they receive it since they believe that it is then possible to achieve their life goals,” says K Gunasegaran, founder and licensed financial planner of Wealth Street Sdn Bhd.

If you are quick to spend money without a plan, think twice before withdrawing the whole. “Those who are not used to having large sums of money tend to get emotionally charged. It can lead to splurges on big-ticket items such as luxury cars. While the money is rightfully yours and it is not entirely wrong to benefit from your retirement savings, be aware of the consequences. If you know that you are an emotional spender, it is best to drop the idea of a lump-sum withdrawal because you have to make smart choices with the money,” says Gunasegaran.

2) Can you generate higher returns at a higher risk?

The primary concern of retirees is whether their retirement savings can sustain them throughout their golden years and generate sufficient returns to outpace inflation.

Headline inflation, as measured by the Consumer Price Index (CPI), increased to 3.3% on an annual basis in May, according to Bank Negara Malaysia (BNM). From 2005 to 2010, the average inflation rate in the country was 2.77%, reaching a historical high of 8.5% in July 2008 and a record low of –2.4% in July 2009.

For the past 59 years, from 1952 to 2010, the EPF has declared annual dividend rates of between 2.5% and 8.5%.In the past 10 years, the highest dividend payout from the EPF was 6% in 2000 and the lowest dividend payout was 4.25% in 2002. “If you are conservative and expect the EPF to continue providing decent annual dividends, opt for flexible withdrawals,” says Wong Keng Leong, practice manager and licensed financial adviser representative at Standard Financial Planner Sdn Bhd.

Headline inflation, however, is not necessarily a reflection of the rise in a household’s real cost of living. This means that the returns on your retirement savings should far exceed the reported CPI figures.

“Also, the EPF promises a minimum dividend of 2.5% per annum. If you think that you or your financial adviser or fund manager can surpass the average returns made by the EPF, consider a lump-sump withdrawal to boost your retirement nest egg,” says Gunasegaran.

When doing so, observe the associated costs such as sales charges or management fees levied by the financial professionals and financial institutions. If you decide to retain your retirement savings with the EPF, there will be a small charge that differs from year to year.

3) Would you still be paying debts at age 55?

If you will still be servicing high-interest debts at age 55, consider using your EPF savings to pare down or settle the loans. This is especially so if the interest levied is higher than the returns generated by your savings.

“High-interest debt includes credit cards [interest rate ranges from 13.5% to 17.5% a year] and personal loans [interest rate ranges from 8% to 12%]. Holding any of these debts negates any investment gains unless you are able to get superior returns on your investment over the years. Withdrawing your retirement savings, be it in a lump sum or partially, to settle your high-interest debt is a smart option but ensure that there is still some money left for your retirement, says Wong.

There is no fixed rule on how much debt you should settle. “How much you should pay off depends on the quantum of your savings. Also, it is good to check whether your debt can be restructured to reduce the interest you have to pay. If so, evaluate the financial benefit of settling this debt with a lump sum withdrawal of your EPF savings,” says Gunasegaran.

4) Do you want to control your retirement funds?

Contributors have little control over how their savings are managed and invested by the EPF, which has sole discretion on how to invest the money that they receive and the dividend (over the minimum amount guaranteed) to declare.

“If you want to take full charge of your retirement savings [either on your own or with professional help], you can do so at 55. When you take a lump-sum payment, you are able to invest in investments that may not be available to you if you were to retain your savings in the EPF [withdrawals can be made to EPF-approved local equity funds],” says Wong, who observes that most of his retired clients withdrew all their EPF monies at 55 as they were comfortable with managing their own money.

A key benefit of withdrawing your retirement savings in a lump sum is that it allows you to expose your loved ones to managing money with a long-term perspective.“At the point of death, most of us will not want to leave a large sum of money to loved ones who cannot manage it. In all likelihood, the money will be spent sooner than planned. Withdrawing your retirement savings in a lump sum at the point of retirement allows you to slowly educate your young-adult children on how to manage a big sum of money. Let them know where you keep your savings and what you are doing with it. This is an alternative to receiving a lump sum from the EPF when you are no longer around,” says Gunasegaran.

5) Do you have a plan to access your money?

If you are 55, under the EPF’s monthly payment withdrawal scheme, the board will transfer the total amount into a special account and put monthly payments into your bank account.

If you opt for a lump-sum withdrawal, how will you draw down your money to fund your lifestyle? There are two options to evaluate. Wong suggests that you should plan a draw-down strategy that includes either a quarterly or half-yearly redemption. “Note that some instruments allow you to make periodical withdrawals but may impose charges.”

On the other hand, Gunasegaran thinks that it is more advisable for retirees to put their retirement savings into annuity-like insurance plans, under which they will receive annual payments after a certain number of years.