Federal Reserve chairman Ben Bernanke is waging an epochal battle behind the scenes for control of US monetary policy, struggling to overcome resistance from regional Fed hawks for further possible stimulus to prevent a deflationary spiral.

Ben Bernanke needs fresh monetary blitz as US recovery falters Photo: GETTY IMAGES

Fed watchers say Mr Bernanke and his close allies at the Board in Washington are worried by signs that the US recovery is running out of steam. The ECRI leading indicator published by the Economic Cycle Research Institute has collapsed to a 45-week low of -5.7 in the most precipitous slide for half a century. Such a reading typically portends contraction within three months or so.

Key members of the five-man Board are quietly mulling a fresh burst of asset purchases, if necessary by pushing the Fed's balance sheet from $2.4 trillion (£1.6 trillion) to uncharted levels of $5 trillion. But they are certain to face intense scepticism from regional hardliners. The dispute has echoes of the early 1930s when the Chicago Fed stymied rescue efforts.

"We're heading towards a double-dip recession," said Chris Whalen, a former Fed official and now head of Institutional Risk Analystics. "The party is over from fiscal support. These hard-money men are fighting the last war: they don't recognise that money velocity has slowed and we are going into deflation. The only default option left is to crank up the printing presses again."

Mr Bernanke is so worried about the chemistry of the Fed's voting body – the Federal Open Market Committee (FOMC) – that he has persuaded vice-chairman Don Kohn to delay retirement until Janet Yellen has been confirmed by the Senate to take over his post. Mr Kohn has been a key architect of the Fed's emergency policies. He was due to step down this week after 40 years at the institution, depriving Mr Bernanke of a formidable ally in policy circles.

The Fed's statement this week shows growing doubts about the health of the recovery. Growth is no longer "strengthening": it is "proceeding". Financial conditions are now "less supportive" due to Europe's debt crisis.

The subtle tweaks in language have been enough to set bond markets alight. The yield on 10-year Treasuries has fallen to 3.08pc, the lowest since the gloom of April 2009. Futures contracts have ruled out tightening until well into next year.

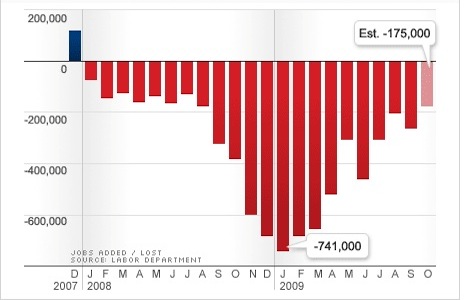

Yet the statement may understate the level of angst at the Board. New home sales crashed 33pc in May to an all-time low of 300,000 after the homebuyer tax-credit expired, confirming fears that the housing market has been propped up by subsidies. Unemployment is stuck at 9.7pc. Manufacturing capacity use is at 71.9pc. The Fed's "trimmed mean" index of core inflation is 0.6pc on a six-month basis, a record low.

"The US recovery is in imminent danger of stalling," said Stephen Lewis, from Monument Securities. "Growth could be negative again as soon as the fourth quarter. There is no easy way out since fiscal stimulus has already been pushed as far as it can credibly go without endangering US credit-worthiness."

Rob Carnell, global strategist at ING, said the Obama fiscal boost peaked in the first few months of this year. It will swing from a net stimulus of 2pc of GDP in 2010 to a net withdrawal of 2pc in 2011. "This is very substantial fiscal drag. On top of this the US Treasury is talking of a 'Just War' against the banks, which will further crimp lending. It is absolutely the wrong moment to do this."

Kansas Fed chief Thomas Hoenig dissented from Fed calls for ultra-low rates to stay for an "extended period", arguing that loose money risks asset bubbles and fresh imbalances. He recently called for interest rates to be raised to 1pc by the autumn.

While he has been the loudest critic, he is not alone. Philadelphia chief Charles Plosser says the Fed has blurred the lines of monetary and fiscal policy by purchasing bonds, acting as a Treasury without a legal mandate. Together with Richmond chief Jeffrey Lacker they represent a powerful block of opinion in the media and Congress.

Mr Bernanke has fought off calls from FOMC hawks for moves to drain stimulus by selling some of the Fed's $1.75 trillion of Treasuries, mortgage securities and agency bonds bought during the crisis. But there is little chance that he can secure their backing for further purchases at this point. "He just has to wait until everybody can see the economy is nearing the abyss," said one Fed watcher.

Gabriel Stein, from Lombard Street Research, said the US is still stuck in a quagmire because Mr Bernanke has mismanaged the quantitative easing policy, purchasing the bonds from banks rather than from the non-bank private sector.

"This does nothing to expand the broad money supply. The trouble is that the Fed does not understand broad money and ascribes no importance to it," he said. The result is a collapse of M3, which has contracted at an annual rate of 7.6pc over the last three months.

Mr Bernanke focuses instead on loan growth but this has failed to gain full traction in a cultural climate of debt repayment. The Fed is pushing on the proverbial string. The jury is out on whether or not his untested doctrine of "creditism" will work.

"We are now walking on deflationary quicksand," said Albert Edwards from Societe Generale.

-2.gif)