Friday, November 5, 2010

Mini Super bull run in the making before Chinese New Year ?

Comparing the circumstances back in 1993 against the current situation.

In the early 1990s, despite slowdown in the global economy, as the third largest economy in South-East Asia, after Indonesia and Thailand, Malaysia was supported by relatively strong macroeconomic fundamentals and resilient financial system. With the real GDP growing at 9.9%, ringgit appreciation, strong export growth and the Government’s measures to hold inflation low at 3.6%, the local stock market became an attractive alternative to foreign investors.

In 1991, Tun Dr Mahathir Mohamad unveiled the philosophy of “Malaysia Incorporated” which was a development strategy for Malaysia to achieve a developed nation by 2020.

Before 1993

Foreign investment in Malaysia was - long-term direct investment in manufacturing sector.

However, massive influx of foreign capital inflow helped fuel the super bull-run in 1993.

Within the year, the market increased by 98% to reach an all-time high of 1,275.3 points and foreign investors’ participation accounted for 15% of total trading value of our local bourse. Lured many retailers into the market

1993

Government planned several mega projects, such as

KL International Airport (RM8bil), Johor-Singapore Second Link (RM1.6bil) and Kuala Lumpur Light Rail Transit (RM1.1bil).

Government planning on privatising its own corporations, such as Petronas, KTM and Pos Malaysia had also driven these counters into prime trading targets.

Besides, the ease of accessing bank credit by investors also contributed to the market rally.

High percentage of loans was channelled to broad property sector as well as the purchase of securities.

1994.

Bank Negara introduced a number of selective capital controls in early 1994 to stabilise the financial system,

2010

Economic Transformation Programme (ETP) with the aim to boost our gross national income (GNI) to US$523bil in 2020 from US$188bil in 2009. GDP growth is anticipated to increase by 6% this year.

September 2010 saw net inflow of foreign funds again in our equity market. Over the past few weeks, the average stock market daily volume had been hovering above one billion shares per day.

According to Andrew Sheng in his book titled From Asian To Global Financial Crisis, there were two main indicators to irrational exuberance during the super bull run in 1993. The first was the amah (domestic maid) syndrome. We need to be careful when amahs got excited about the stock market. This was because they did not know what they were buying and would always be the last to sell. The second indicator was when businessmen began to speculate stocks in the stock market. This was because they might neglect their businesses and use some of their cash for speculation.

Comparing our current market situation with the 1993 bull run, there are certain similarities that we see, such as strong economic growth, ringgit appreciation, inflow of foreign capital and ease of credit.

Local retailer participation may be the last push factor towards the bull run.

( source : The star )

http://acnews101.blogspot.com/2010/11/mini-super-bull-run-in-making-before.html

----

Is there a super bull run in 2010?

Personal Investing – By Ooi Kok Hwa

Although the economic situation now compares with that of 1993, the last push must come from local retail investors

THE recent rally in our local bourse has prompted many seasoned investors, especially those who experienced the super bull run in 1993, to wonder whether the current rally is about to turn into a real bull run. Of course, nobody can tell for sure what will happen next, but we certainly can do some homework, comparing the circumstances back in 1993 against the current situation.

In 1991, Tun Dr Mahathir Mohamad unveiled the philosophy of “Malaysia Incorporated” which was a development strategy for Malaysia to achieve a developed nation by 2020. In the early 1990s, despite slowdown in the global economy, as the third largest economy in South-East Asia, after Indonesia and Thailand, Malaysia was supported by relatively strong macroeconomic fundamentals and resilient financial system. With the real GDP growing at 9.9%, ringgit appreciation, strong export growth and the Government’s measures to hold inflation low at 3.6%, the local stock market became an attractive alternative to foreign investors.

Before 1993, foreign investment in Malaysia was mainly dominated by long-term direct investment in the manufacturing sector. However, as a result of measures taken to develop our domestic equity market, coupled with the strong economic backdrop, we saw a massive influx of foreign capital inflow, which helped fuel the super bull-run in 1993. Within the year, the market increased by 98% to reach an all-time high of 1,275.3 points and foreign investors’ participation accounted for 15% of total trading value of our local bourse. This had also driven the market into a highly speculative one, which lured many retailers into the market, thinking of making fast and easy money.

With the presence of new and unfamiliar players, the market became a huge “casino”. Retail investors bought into stocks based on rumours rather than company fundamentals. Among the hottest topics during that time were the awards of government mega projects, privatisation candidates, sector play and regular news on upward revision of corporate earnings. Examples for the highly speculative stocks were Ekran, Ayer Molek Rubber Co, Berjuntai Tin Dredging and Kramat Tin Dredging.

In 1993, with the economy booming, the Government planned several mega projects, including the KL International Airport (RM8bil), Johor-Singapore Second Link (RM1.6bil) and Kuala Lumpur Light Rail Transit (RM1.1bil). The news of contract awarding immediately sent the market into speculative mood on those potential candidates. Similarly, the news of the Government planning on privatising some of the its own corporations, such as Petronas, KTM and Pos Malaysia had also driven these counters into prime trading targets.

Besides, the ease of accessing bank credit by investors also contributed to the market rally. We noticed that a high percentage of loans was channelled to broad property sector as well as the purchase of securities.

As a result of massive inflow of foreign funds and the super bull run in stock market, Bank Negara introduced a number of selective capital controls in early 1994 to stabilise the financial system,

Recently, our Prime Minister Datuk Seri Najib Tun Razak unveiled the Economic Transformation Programme (ETP) with the aim to boost our gross national income (GNI) to US$523bil in 2020 from US$188bil in 2009. The programme is to attract investment not only from the Government, but also (more importantly) from domestic direct investment as well as foreign direct investment. In view of strong economic growth, our GDP growth is anticipated to increase by 6% this year.

In September, we notice that there was a net inflow of foreign funds again in our equity market. Over the past few weeks, the average stock market daily volume had been hovering above one billion shares per day. Almost every day, the top 10 highly traded stocks were those speculative stocks with poor fundamentals. In addition, we noticed that some retail investors had started to get excited again in the stock market.

According to Andrew Sheng in his book titled From Asian To Global Financial Crisis, there were two main indicators to irrational exuberance during the super bull run in 1993. The first was the amah (domestic maid) syndrome. We need to be careful when amahs got excited about the stock market. This was because they did not know what they were buying and would always be the last to sell. The second indicator was when businessmen began to speculate stocks in the stock market. This was because they might neglect their businesses and use some of their cash for speculation.

Comparing our current market situation with the 1993 bull run, there are certain similarities that we see, such as strong economic growth, ringgit appreciation, inflow of foreign capital and ease of credit. However, our local retailer participation is yet to get boiling, which may be the last push factor towards the bull run. Hence, once the participation of the local investors starts to get heated up, together with more inflow of foreign fund, that may be the signs of the market heading for a ‘mini’ super bull run.

● Ooi Kok Hwa is an investment adviser and managing partner of MRR Consulting.

fr:biz.thestar.com.my/news/story.asp?file=/2010/11/3/business/7348793&sec=business

Sunday, 9 January 2011

Saturday, 8 January 2011

Ajinomoto (Malaysia) Berhad

Market Watch

Recent Financial Results

Announcement

Date Financial Yr. End Qtr Period End Revenue Profit/Lost EPS Amended

RM '000

23-Nov-10 31-Mar-11 2 30-Sep-10 77,686 5,378 8.85 -

27-Aug-10 31-Mar-11 1 30-Jun-10 82,127 8,630 14.19 -

25-May-10 31-Mar-10 4 31-Mar-10 71,877 1,482 2.44 -

10-Feb-10 31-Mar-10 3 31-Dec-09 72,661 9,525 15.67 -

Pr 4.08 (7.1.2011)

Outstanding shares 60.80m

Market cap 248.064m

ttm-EPS 41.15 sen

ttm-PE 9.91

DY % 4.41

Past Years Data

FYE

March 04 Revenue 164.126m Earnings 12.059m EPS 19.83 sen Div 9.0 sen

March 05 Revenue 166.869m Earnings 12.519m EPS 20.59 sen Div 9.00 sen

March 06 Revenue 170.59m Earnings 6.31m EPS 9.9 sen Div 7.9 sen

March 07 Revenue 190.63m Earnings 14.99m EPS 24.7 sen Div 8.9 sen

March 08 Revenue 215.46m Earnings 20.94 EPS 34.4 sen Div 12.9 sen

March 09 Revenue 243.84m Earnings 19.07m EPS 31.2 sen Div 15.0 sen

March 10 Revenue 284.62m Earnings 23.94m EPS 36.6 sen Div 18 sen

H1 2011 Revenue 159.813 Earnings 14.008m EPS 23.04 sen

Ajinomoto (Malaysia) Berhad

Business Description:

Ajinomoto (Malaysia) Berhad is engaged in the manufacturing and selling of monosodium glutamate and other related products.

Its retail products include AJI-NO-MOTO MSG, TUMIX stock seasoning powder, VONO cup soup, SERI-AJI ready to cook seasoning powder, AJI-SHIO flavored pepper, black pepper and iodized salt, PAL SWEET low calorie sweetener, Slim Up and AJI MIX seasoning.

Its other industrial products include HVP, AJI-AROMA, AJI-PLUS and AJIMATE.

The Company markets its products in Malaysia, the Middle East and in other Asian countries.

Recent Financial Results

Announcement

Date Financial Yr. End Qtr Period End Revenue Profit/Lost EPS Amended

RM '000

23-Nov-10 31-Mar-11 2 30-Sep-10 77,686 5,378 8.85 -

27-Aug-10 31-Mar-11 1 30-Jun-10 82,127 8,630 14.19 -

25-May-10 31-Mar-10 4 31-Mar-10 71,877 1,482 2.44 -

10-Feb-10 31-Mar-10 3 31-Dec-09 72,661 9,525 15.67 -

Pr 4.08 (7.1.2011)

Outstanding shares 60.80m

Market cap 248.064m

ttm-EPS 41.15 sen

ttm-PE 9.91

DY % 4.41

Past Years Data

FYE

March 04 Revenue 164.126m Earnings 12.059m EPS 19.83 sen Div 9.0 sen

March 05 Revenue 166.869m Earnings 12.519m EPS 20.59 sen Div 9.00 sen

March 06 Revenue 170.59m Earnings 6.31m EPS 9.9 sen Div 7.9 sen

March 07 Revenue 190.63m Earnings 14.99m EPS 24.7 sen Div 8.9 sen

March 08 Revenue 215.46m Earnings 20.94 EPS 34.4 sen Div 12.9 sen

March 09 Revenue 243.84m Earnings 19.07m EPS 31.2 sen Div 15.0 sen

March 10 Revenue 284.62m Earnings 23.94m EPS 36.6 sen Div 18 sen

H1 2011 Revenue 159.813 Earnings 14.008m EPS 23.04 sen

A look at the historical ttm-EPS and ttm-PE of Ajinomoto:

https://spreadsheets.google.com/pub?key=0AuRRzs61sKqRdFlaMjJCbnFlZUZETUc5YmQzRDdRbUE&hl=en&output=html

https://spreadsheets.google.com/pub?key=0AuRRzs61sKqRdFlaMjJCbnFlZUZETUc5YmQzRDdRbUE&hl=en&output=html

Business Description:

Ajinomoto (Malaysia) Berhad is engaged in the manufacturing and selling of monosodium glutamate and other related products.

Its retail products include AJI-NO-MOTO MSG, TUMIX stock seasoning powder, VONO cup soup, SERI-AJI ready to cook seasoning powder, AJI-SHIO flavored pepper, black pepper and iodized salt, PAL SWEET low calorie sweetener, Slim Up and AJI MIX seasoning.

Its other industrial products include HVP, AJI-AROMA, AJI-PLUS and AJIMATE.

The Company markets its products in Malaysia, the Middle East and in other Asian countries.

Fair Valuation of Berkshire Hathaway

http://www.tilsonfunds.com/BRK.pdf

- Cheap stock: 75-cent dollar, giving no value to recent investments and immense optionality

- Extremely safe: huge cash and other assets provide downside protection

- Strong earnings report should act as a near-term catalys

Guan Chong expects to raise RM120mil

Saturday January 8, 2011

Guan Chong expects to raise RM120mil

KUALA LUMPUR: Guan Chong Bhd (GCB) expects to raise up to RM120mil from through its corporate exercise of issuing RM2 for 60 million free warrants.

“Based on the exercise price of the warrants of RM2 per new GCB share, the company stands to potentially raise up to RM120mil during the tenure of the warrants upon full exercise of the warrants by the holders of the warrants.

“Such proceeds will be utilised for the day-to-day working capital requirements of the GCB group,” it told Bursa Malaysia yesterday.

The company said that it had fixed the exercise price for the warrants at RM2, which was 9.29% or 17 sen over the theoretical ex-price after the proposed bonus issue of RM1.83 per share, based on the five-day volume weighted average price of RM2.44.

The 60 million warrants were issued on the basis of one free warrant for every four existing shares held on the same entitlement date for the proposed bonus issue.

The corporate exercise also involved the proposed bonus issue of 80 million new shares of 25 sen on a one-for-three basis.

http://biz.thestar.com.my/news/story.asp?file=/2011/1/8/business/7758406&sec=business

Guan Chong expects to raise RM120mil

KUALA LUMPUR: Guan Chong Bhd (GCB) expects to raise up to RM120mil from through its corporate exercise of issuing RM2 for 60 million free warrants.

“Based on the exercise price of the warrants of RM2 per new GCB share, the company stands to potentially raise up to RM120mil during the tenure of the warrants upon full exercise of the warrants by the holders of the warrants.

“Such proceeds will be utilised for the day-to-day working capital requirements of the GCB group,” it told Bursa Malaysia yesterday.

The company said that it had fixed the exercise price for the warrants at RM2, which was 9.29% or 17 sen over the theoretical ex-price after the proposed bonus issue of RM1.83 per share, based on the five-day volume weighted average price of RM2.44.

The 60 million warrants were issued on the basis of one free warrant for every four existing shares held on the same entitlement date for the proposed bonus issue.

The corporate exercise also involved the proposed bonus issue of 80 million new shares of 25 sen on a one-for-three basis.

http://biz.thestar.com.my/news/story.asp?file=/2011/1/8/business/7758406&sec=business

Friday, 7 January 2011

Variety of market-shaking bubbles might inflate in 2011

7 JAN, 2011, 12.27PM IST,BLOOMBERG

Variety of market-shaking bubbles might inflate in 2011

TOKYO: Welcome to the year of the bubble. It may seem an odd assertion at a time when many key economies are in, or on the verge of, recession. Yet near-zero interest rates in Washington, Tokyo and Frankfurt have a way of wreaking havoc with markets and human psychology. It's not a reach to say we have a bubble in bubbles. A variety of market-shaking bubbles might inflate before our eyes - some in asset markets, others in flawed perceptions. Here are eight.

Hot money: It's terrific the MSCI AC Asia Pacific Index jumped 14% last year, outpacing MSCI's broader indexes. It would be better, though, if the gains had more to do with fundamentals and less with ultra-low rates. The Bank of Japan's largess has long seeped overseas to boost stock, bond and property prices near and far. The yen-carry trade - borrowing cheaply in yen and using the funds for riskier bets overseas - was the forerunner of a similar dollar trade. Federal Reserve policies sent tidal waves of liquidity toward Asia in 2010. It could reach disastrous proportions, leaving a trail of ruin in its wake.

Decoupling theory: The bubble here is the unsustainable belief that Asia can grow rapidly no matter what happens among the biggest economies. Don't bet on it. It's great China is growing 9.6% and India at 8.9%. But, nothing would serve Asia better than a rebound in growth in the US , euro zone, Japan and the UK, which combined make up $34 trillion in annual output. Developing economies may live for a couple of years without the majors. Good luck keeping up that performance in the years ahead.

Food prices: A January 3 Times of India headline raised a question in many minds: "Can government do nothing legally to check prices?" The answer is: not much. The UN Food and Agriculture Organization predicts the global cost of importing foodstuffs totalled $1.026 trillion in 2010, compared with $893 billion in 2009. Imbalances in supply and demand and regional trade rigidities will accelerate the trend, swamping developing nations with the most basic of problems: Filling the bellies of those powering their economic rise.

Income inequality: The trajectory of everyday prices is a fast-developing setback to Asia's efforts to narrow its gaping rich-poor divide. Rising costs for cooking-oil and rice may mean little to a Goldman Sachs Group Inc staffer. To a family living on $3 a day and already spending two-thirds of income on food, they are devastating. Rising wealth disparities could foreshadow a year of tensions, as failed harvests and inflation cause famines, riots, hoarding and trade wars worldwide. The bubble here would be one in human suffering.

Wacky weather: A few months ago, drought was imperiling Australia's economic outlook. Today floods that some characterise as "biblical" have economists calculating the implications for commodity prices. Forget temperatures and focus on the increasing frequency of freaky weather patterns from Miami to Mumbai.

Currency reserves: Why any economy needs $2.7 trillion of them is beyond me. It's not just China that is trapped into adding to its currency stockpile to keep its existing holdings from losing value. Japan has more than $1 trillion, while Taiwan, South Korea, Hong Kong, Singapore and Thailand have a combined $1.3 trillion. Talk about an unproductive use of wealth - and a risk that's growing by the day with no easy fix in sight.

Geopolitical risks: Leave it to Kim Jong-Il to remind investors that the biggest surprises won't be from economic or corporate reports, but rogue regimes. Expect a bull market in territorial disputes. Faced with growing uncertainty, governments are desperate to placate the masses. The desire to unify the home population may lead to rifts between neighbours. Those seeking shelter from these brewing storms explains why gold is almost $1,400 an ounce.

Group of 20: Any optimism that European officials can avert disaster might be seen as irrational. The same goes for the belief that China can grow 10% annually forever or that Japan's leaders can defeat deflation. The real perceptions bubble is that a disparate grouping of 20 nations can tame out-of-whack markets and imbalances that were decades in the making. The year ahead might turn any, or all, of these accepted wisdoms on their head.

http://economictimes.indiatimes.com/markets/analysis/variety-of-market-shaking-bubbles-might-inflate-in-2011/articleshow/7232817.cms

Variety of market-shaking bubbles might inflate in 2011

TOKYO: Welcome to the year of the bubble. It may seem an odd assertion at a time when many key economies are in, or on the verge of, recession. Yet near-zero interest rates in Washington, Tokyo and Frankfurt have a way of wreaking havoc with markets and human psychology. It's not a reach to say we have a bubble in bubbles. A variety of market-shaking bubbles might inflate before our eyes - some in asset markets, others in flawed perceptions. Here are eight.

Hot money: It's terrific the MSCI AC Asia Pacific Index jumped 14% last year, outpacing MSCI's broader indexes. It would be better, though, if the gains had more to do with fundamentals and less with ultra-low rates. The Bank of Japan's largess has long seeped overseas to boost stock, bond and property prices near and far. The yen-carry trade - borrowing cheaply in yen and using the funds for riskier bets overseas - was the forerunner of a similar dollar trade. Federal Reserve policies sent tidal waves of liquidity toward Asia in 2010. It could reach disastrous proportions, leaving a trail of ruin in its wake.

Decoupling theory: The bubble here is the unsustainable belief that Asia can grow rapidly no matter what happens among the biggest economies. Don't bet on it. It's great China is growing 9.6% and India at 8.9%. But, nothing would serve Asia better than a rebound in growth in the US , euro zone, Japan and the UK, which combined make up $34 trillion in annual output. Developing economies may live for a couple of years without the majors. Good luck keeping up that performance in the years ahead.

Food prices: A January 3 Times of India headline raised a question in many minds: "Can government do nothing legally to check prices?" The answer is: not much. The UN Food and Agriculture Organization predicts the global cost of importing foodstuffs totalled $1.026 trillion in 2010, compared with $893 billion in 2009. Imbalances in supply and demand and regional trade rigidities will accelerate the trend, swamping developing nations with the most basic of problems: Filling the bellies of those powering their economic rise.

Income inequality: The trajectory of everyday prices is a fast-developing setback to Asia's efforts to narrow its gaping rich-poor divide. Rising costs for cooking-oil and rice may mean little to a Goldman Sachs Group Inc staffer. To a family living on $3 a day and already spending two-thirds of income on food, they are devastating. Rising wealth disparities could foreshadow a year of tensions, as failed harvests and inflation cause famines, riots, hoarding and trade wars worldwide. The bubble here would be one in human suffering.

Wacky weather: A few months ago, drought was imperiling Australia's economic outlook. Today floods that some characterise as "biblical" have economists calculating the implications for commodity prices. Forget temperatures and focus on the increasing frequency of freaky weather patterns from Miami to Mumbai.

Currency reserves: Why any economy needs $2.7 trillion of them is beyond me. It's not just China that is trapped into adding to its currency stockpile to keep its existing holdings from losing value. Japan has more than $1 trillion, while Taiwan, South Korea, Hong Kong, Singapore and Thailand have a combined $1.3 trillion. Talk about an unproductive use of wealth - and a risk that's growing by the day with no easy fix in sight.

Geopolitical risks: Leave it to Kim Jong-Il to remind investors that the biggest surprises won't be from economic or corporate reports, but rogue regimes. Expect a bull market in territorial disputes. Faced with growing uncertainty, governments are desperate to placate the masses. The desire to unify the home population may lead to rifts between neighbours. Those seeking shelter from these brewing storms explains why gold is almost $1,400 an ounce.

Group of 20: Any optimism that European officials can avert disaster might be seen as irrational. The same goes for the belief that China can grow 10% annually forever or that Japan's leaders can defeat deflation. The real perceptions bubble is that a disparate grouping of 20 nations can tame out-of-whack markets and imbalances that were decades in the making. The year ahead might turn any, or all, of these accepted wisdoms on their head.

http://economictimes.indiatimes.com/markets/analysis/variety-of-market-shaking-bubbles-might-inflate-in-2011/articleshow/7232817.cms

Thursday, 6 January 2011

Reasonableness and Unreasonableness

An indictment against the Christian community

2011-01-04 21:46

My friend Jackson Ng has raised a very rational and legitimate point in his comment in the Malaysia Chronicle on the matter of the Najib aides asking the organisers of the Christmas Eve gathering at the St John’s Cathedral in Kuala Lumpur to remove the crucifixes, and the banning of singing hymns.

Jackson asked why didn't the church organizers object to such unreasonable instructions?

Although he is not a Christian, Jackson said he decided to write on the issue because it is a matter concerned with the universal acceptance of basic principles and the rights of mankind.

He has rightly pointed out that the removal of crucifixes and the banning of hymn-singing at St John’s Cathedral constitute a violation of religious freedom guaranteed under Article 3(1) of the Federal Constitution.

According to news reports, Datuk Seri Najib Razak’s aides had ordered the removal, claiming that the crucifixes would be offensive to the prime minister.

Jackson said he was not only upset with the instruction given by the Najib aides, but more angry with the church leaders for their failure to stand up and speak out on the matter.

"Are they not God-fearing Christians, just like Muslims are also God-fearing? Why then did the organisers remove the sacred crucifixes? Isn’t it logical to deduce that they are not God-fearing beings but Satan-fearing arse-licking politicians who claim to be Christians? God-fearing Christians would have defended the crucifixes, Jesus Christ and God. Do they value the presence of the PM more than God?" Jackson asked.

"As it was, the organisers, for reasons best known to them, felt the presence of the PM was more important than their Jesus Christ and God. To them, it was more important for the PM to grace the function and, therefore, abandon Jesus Christ and their God. Disgraceful and shameful are two words best to describe the organisers," he said.

"God-fearing Christians must therefore start defending Jesus Christ and their God by throwing out the organisers from their holy house of worship. If not, they too are condoning what they did," Jackson said.

Strong words, indeed, but Jackson certainly is right to lambast the church leaders for being spineless cowards in the face of such violation of human, civil and constitutional rights.

Jackson's denunciation of the action or lack of it of the Christian leaders is perhaps the first public indictment against the Christian community in Malaysia, as far as I know. And it is not without justification, and surely, appropriate too.

One of the major reasons that the fundamental human, civil and constitutional rights are slowly being eroded is the failure of so-called community and religious leaders to stand firm and steadfast to preserve, protect and promote these rights.

I am very familiar with the Malaysian Christian community, having been a Christian for nearly 45 years and actively involved in teaching and preaching for nearly 40. Hence, I think I am well-qualified to make observation and comment on the Church in Malaysia.

There are basically three types of Christians in Malaysia.

The first common type is the introvert conservatives, who are generally shy, reticent, and typically individualistic self-centered persons, predominantly concerned with their own thoughts and feelings, with nary a care for things outside the walls of their church.

These traditionally orthodox Christians are always concerned about their own "spiritual growth", and are generally timid and harmless. They live their lives in the familiar safe comfort zone of their church community, and speak a sort of churchy language, often convicing themselves that they will be okay if they go to church regularly, give often to the church and their pastor, pray always in whatever situation they are in, and shun, evade and eschew controversial matters, especially political ones. They dress decently and avoid elaborate and spectacular extravagant and lavish display of wealth and luxury. They made good church members and citizens as they never ask questions or challenge any rule, precept or instruction, no matter how excessive, unreasonable or even oppressive the rules and instructions are. They are generally afraid of anything official, especially the government and its enforcement agencies. Mention the ISA or May 13, and they will secrete cold sweat and clinched in fear.

Their pastors and church leaders love these church members, because they are literally under their complete control, and want them to remain in their innocent gullible situation. Hence, there is no real teaching of doctrines, biblical and theological matters, and on issues concerned with life, thoughts and faith in relation to the world outside the church. Actually, the pastors and church leaders themselves are as biblically and theologically disabled as their church members. Hence, they play church happily, and never growing beyond their religious pubescence. The church is their safe abode, and anything outside the church is none of their business.

The pastors and leaders of such churches generally avoid speaking up on issues, even if the issues affect their churches or their rights to religious freedom. They will not sign petitions to seek release of political and religious freedom fighters, and will not want to be part of the movement to struggle for the right to use the word "Allah" in the worship, teaching, preaching and publications of the Church. We have many of such Christians in the Malaysian Christian community.

The second type of Christians are the so-called Health and Wealth charismatics, whose main focus in their life, thoughts and faith is material wealth and luxurious living. Their church worship services are no difference from that of an entertainment disco joint, with whirling colourful psychedelic lights, with an intense, vivid and swirling abstract loud music and repeated chantings masquerading as worship songs that produce religious hallucinations and apparent expansion of spiritual consciousness.

Most of the worshippers jump, wave, swing, sway and undulated to the thumping rhythm of the deafening music, and wail loudly, with some making animal sounds. There is no solid biblical exposition, only entertaining motivation talks masquerading as sermons. A good preacher is one who tells a lot of stories and joke, and make the congregation laugh. No Bible message, just a feel good prosperity gospel.

Such churches are usually housed in mega complex with attractive facilities like gyms and swimming pools to attract members of other churches to their fold. There is no growth by evangelism or conversion, only the seduction of church members from other churches.

My personal observation is that most of these people are no different from those under the influence of psychedelic drugs, with their mental intuitive capability almost unilaterally being under the complete control of an irrational runaway emotion. These people are certainly brain-washed into giving large sums of money to their churches and pastors. Most of the pastors of such churches receive big fat pay packets, driving top brand cars, and live in luxury houses in upmarket residential areas. They go on church-sponsored overseas holiday masquerading as "mission trip" two or three times a year.

Obviously, the pastors, leaders and members from such churches couldn't care about what is happening in the real world outside their churches. They are in a world of their own. For the members, the churches are where they can find escape from their frustration, misery, griefs, mental suffering, and get release and relief for themselves. For the pastor, the church is a bigh income generator, giving him undreamt of wealth and luxury. The recent news reports of a mega church in Singapore, where the pastor is a multi-millionare is one example of such a church.

Such churches will not hestitate to remove any religious artifacts, like the Cross, and stop singing hymns and praying in order to receive a non-Christian VIP. To the pastors and church leaders, the Lord Jesus Christ is irrelevant so long as they receive material benefits such as government grants for their mega church building and facilities. After all, Christ is just a brandname of their religious commercial enterprise.

Finally, there are the radical non-comformist Christians, who will stick out their necks to stand up for their faith and principles. There is no organised body of such Christians, but they are found in various churches, especially the traditional denomination churches. These are Christians who are well-educated in their faith, know what it means to be "salt of the Earth" and "lights of the World", are professionals in the various fields in the secular marketplace, are outspoken and articulate in issues, especially on matters concerning the truth, righteous, justice, fairness, racial and gender equality, freedom of religious practices, freedom or speech and press, and accountability and transparency in the church and in government.

These are the Christians that the pastors and church leaders generally ignore and avoid, and will distance themselves from, for fear of getting into the bad book of the authorities. We don't find them holding leadership positions in the churches, but we see them active in the secular marketplace, spearheading the struggle for the advancement of God's kingdom among the people of the world, standing up and sacrificing career prospects for the sake of the Way, the Truth, and the Life.

These radical non-conformist Christians will never allow their faith and ethics to be compromised for the sake of acceptance by any unreasonable and oppressive regime.

My friend Jackson Ng is right. It's time the Christians who are truly God's people stand up and be counted in the face of the increasingly exessively unloving and tyrannical repressive regime.

Nazri speaks on 1Malaysia and various issues

Nazri: political leaders thrust crutches upon Malays who are already self-reliant (UPDATED)

2011-01-06 15:11

- Nazri: "Many Malay students already have the ability in their own right to gain entry into famous foreign universities for studies, but unfortunately, many leaders are still repeatedly reminding the Malays that they need government support." Photo courtesy: Sin Chew Daily

KUALA LUMPUR, Thursday 6 January 2011 -- Minister in the Prime Minister's Department Datuk Sri Nazri said that it was not that the Malays lacked confidence, but it was rather that some political leaders had yet to wake up and were still continuing to remind the Malays not to be too capable!

He said that, in fact, many Malays were now self-reliant.

He told Sin Chew Daily in an interview that there were many Malays who were confident of themselves now; and did not really want to rely on the Government's bumiputra policies, and they desired to show their abilities.

"Many Malay students already have the ability in their own right to gain entry into famous foreign universities for studies, but unfortunately, many leaders are still repeatedly reminding the Malays that they need government support."

Nazri used his own family as an example and said that more and more Malays could sustain themselves without government support.

"My grandparents came from Hulu Perak; they were not rich. Although there was no bumiputra policy at that time, my father managed to go overseas to study law and became a lawyer. I later followed in his footsteps and went to UK to study law at my own expense."

"PAS which was very conservative has already become open. Everyone should change; I hope Umno will not revert to its old ways."

Malaysian society going backwards

He said that the more advanced our times had become, the more backwards Malaysia seemed to be going. In an era without borders, many people continued to emphasize their ethnic race, advocate a singular point of view and were increasingly fanatical.

When on the topic of how a lot of people were afraid of becoming less Malay, Chinese or Indian, Nazri’s first response was: "I never worry about becoming less Malay, even though among leaders, I am one of the few who have this kind of thinking!"

He was also not worried that because he "is less of a Malay", he would be unpopular with people of his ethnic race, and said that that many in the Malay middle class agreed with him.

Nazri stressed that education was important as it allowed the Malays to become confident.

He also encouraged all races to interact with each other, and not to limit themselves to those of their own ethnic group.

Nazri: history textbooks will be honest and not cover up Yap Ah Loy’s contributions

Nazri pointed out that Kapitan Yap Ah Loy was a major founder of Kuala Lumpur. This is the truth, why should we cover up this fact?

He stressed that the history books must be based on facts and must be inclusive, so that history could be a tool for nation-building.

He told Sin Chew Daily that an in-depth study of Malaysia’s history would reveal that the ancestors of the various ethnic races have fought for national independence, and their contributions should not be concealed.

He said that the government wanted the people to feel proud of the nation’s independence, and wanted young people to wave the national flag on National Day to express their patriotism, but on the other hand told them: "Your race did not make any contribution." "How can we then convince the people?"

Therefore, Nazri suggested that before the compiling of history textbooks, the government should organize seminars, so that we could reach a consensus and accept these history textbooks.

Chinese are also Malaysians; it is understandable for them to want fairness

Nazri felt that it was reasonable that the Chinese had their demands for fairer opportunities in education and business, since Chinese were also Malaysian citizens, and the Chinese were living in this country.

Nazri felt that it was a very stupid action to question the patriotism of non-bumiputras from time to time, and described those who tell Chinese "to return to China" as having no common sense.

He regretted that the patriotic spirit of non-bumiputras was questioned, and in the matter of "non-bumiputras being accused of not joining the army because they are not loyal", he felt a strong sense of injustice.

"A lot of Malays, including myself, do not send their children to the army. Does it mean that the Malays, including me, are not patriotic?"

"If it is said that it is not patriotic of the Chinese to not send their children into the army, then are the Malays not the same?"

No need for racial remarks

Nazri said that he understood the deep disappointment and anger felt by the Chinese community over calls to Chinese to go back to China and remarks that the Chinese were disloyal and stressed that such racial remarks were totally unnecessary.

"They should not have casually called on the Chinese to go back to China... These people have something wrong with their brains."

"When China opened her doors in 1978, the Malaysian Chinese did not return to China in bulk. Malaysian Chinese only travelled to China for sightseeing; and returned to Malaysia. They did not return to China."

Nazri, who is the Member of Parliament for Padang Rengas, Perak said that the ancestors of many Malays were also from other places, and they also had a habit of returning to visit their ancestral homes. So why can the Malays do it and why can the Chinese not do it? Why have two sets of standards?

"So what if we call this piece of land Tanah Melayu? Thailand have 6 million Malays living there even though it is known as Thailand, and the United Kingdom is called England (English land), but there are many black people staying there. How do you explain it?"

People in Umno playing political games cause resistance to Najib’s reforms

Nazri did not deny that there were too many people in Umno who were playing political games, and causing great resistance to Najib's reforms.

"For example, I recently met with Wong Meng Chee. And some Umno members wanted Najib to dismiss me. I just ignored them, and I also could not care less."

Nazri said that as the first cabinet minister to announce himself as "Malaysian first, Malay secondarily," it did not pose any problem for him.

He agreed that many people did not dare to make such a declaration, and it might be due to self-preservation.

"I do not care what others think of me. I only want to service the people. I do not regard the official position as a personal honor. I have no worries. I have been a minister for 11 years; it would not be a problem for me if I were to retire. For me, being a public servant means I have to serve the people. This is not personal glory, but service. As long as the government still needs me, I will continue to serve."

A lone ranger in Cabinet

Nazri admitted that he was "one of the very few" in the Cabinet as he acted and talked rather differently from other ministers. He said probably due to political considerations some Cabinet ministers had not put the 1Malaysia concept into action even though they agreed to it.

He said he believed Perkasa was against 1Malaysia, but did not understand why some ministers still lent their support to the organisation.

"We should oppose Perkasa if we say we support 1Malaysia. Unfortunately I do not see any minister voice up against Perkasa. Yes, they say they support 1Malaysia, but I am not sure whether they have any practical action to support their claims."

When asked whether he belonged to the "one of the very few" in the Cabinet, Nazri said, "It seems to be this way. I don't know. We are not much different when it comes to talking. They know what I ask for, but are not doing anything."

"Probably there are some viruses inside my brain that make it hard to operate in a normal way. Since I belong to that minority group, the majority would do things in a way very different from me."

He also said he would just say it out directly if necessary, regardless of how senior a minister was, because he supported the prime minister and cared about the rakyat.

Nazri reiterated that the prime minister had not entrusted him with any particular mission, and all that he had done or was doing was from the bottom of his heart.

Need for continued existence of ISA

Nazri felt that it was necessary for the continued existence of the ISA, citing the reason that there were simply too many self-proclaimed heroes who would manipulate racial issues to protrude themselves.

Without ISA, he said, it would be very tough for the government to deal with these people.

Nazri admitted that racial relations remained fragile and tense even after the country had been independent for 53 years.

He nevertheless believed that Prime Minister Datuk Seri Najib Tun Razak was capable of handling the issue through the wealth of experiences he had accumulated over his past 23 years in politics.

Support from Malays still high

Nazri said he was not worried that his moderate talks would cost him the votes of the Malays, adding that he had the support of some 72% of Malays.

"You say leaders playing up racial issues will have good market demands, but in a democratic country, I only need 51% to get elected. I think I can get 51% if I do the right things. So, I don't worry about the market. Sure enough there are people supporting narrow-minded remarks, but they are not the majority.

"When talking about pluralism, I believe I am not one of the very few. While newspaper reports and blogs will draw the attention of many, the majority of Malays living in kampungs will not give them a heed. Newspaper reports and blogs do not represent the majority."

Nazri said direct BN membership was one way of diluting the ethnic tone of a political party. He said Umno, MCA and MIC would probably be no longer in existence if direct members of BN were to outnumber members of all component parties one day. However, he admitted that this could take a very long time to come through.

Quota system should go on

Nazri said unreservedly that he supported the country's existing quota system, and that this system should be based on the racial make-up of the country, i.e. 51% for bumiputra and 49% for non-bumiputra.

When asked whether the bumiputra policy would hinder national unity, Nazri said the quota system would ensure that national wealth was fairly distributed to all ethnic groups.

But does that mean meritocracy is no longer required in this country?

"When we talk about 51% and 49%, it should be distributed based on the lowest requirements. This is what I call meritocracy.

"For example the government wants to give away 100 scholarships to students scoring 5A's. While all the 45 non-bumiputra students score 5A's, only 30 out of 55 bumiputra students score 5A's. If we offer scholarships to the 25 bumi students not meeting the criteria, then it will be unfair and is against the principles of meritocracy."

"To me, quota system is required, as we are a multiracial society. We do not want any particular ethnic group to fall far behind and get unhappy. That said, the quota system must be fair and implemented based on meritocracy."

Religious conversion is not the way to avoid responsibility

Solve all the family and marital problems first before the conversion. Religious conversion is not the way to avoid responsibility. This is the advice of Minister in the Prime Minister’s Department Datuk Seri Nazri Aziz to those who wish to embrace Islam.

Nazri urged those who want to become Muslims to settle all their problems with their non-Muslim family members, including their former wives or husbands, as Islam should not be used as a tool to avoid responsibility.

Religious belief for those under 18 years old

According to Nazri, it is wrong to say that when one of the parents converts to Islam after their divorcement, he or she has the right to convert their children.

Nazri said that he sincerely believes that there is a constructive contract between every couple and their children have to be raised under their religious belief.

"Many Hindus have converted to Islam recently and the children were converted when the husband converted to Islam. According to them, children under 18 years old have no independent personal religious belief and their parents can raise them based on their own preferred religion,” he said.

"However, it is wrong to say that there is no religious belief for those under 18 years old as when their parents got married, they were both Hindus and the children, regardless whether they are eight or nine years old, know what is their religion as their parents had bought them to Batu Caves and Hindu temple. They also celebrate Deepavali. This shows that they have a religious belief," Nazri said.

As for the S. Shamala case, involving the unilateral conversion of children to Islam by one parent, Nazri said that any dispute before the conversion to Islam must be resolved in a civil court as the jurisdiction of the syariah court is only applicable from the date of conversion.

"Shamala's husband converted to Islam after their marriage and therefore, the case should be settled in a civil court,” he said.

Federal Court has no right to make judgment on religious belief

Nazri said he does not agree with the claim that the Federal Court has missed a golden opportunity to identify and clarify vital issues in the Shamala case.

He pointed out that as no amendment had been made to the relevant laws, the Federal Court has no right to rule on a person's religious belief, and the people must respect the existing legal provisions.

"The failure to amend the law means the problems still exist and the civil court will not and cannot hear cases related to Islam, which are rightfully under the jurisdiction of the syariah court," Nazri said.

On whether the civil court or the syariah court is the more appropriate court to rule on a person’s status as a Muslim, Nazri said: "The court should not be the forum to decide whether or not a person is Muslim. It is very controversial, and I do not know which is the most appropriate forum. If we amend the law, the civil court would be the best forum."

Translated by Adeline Lee, Dominic Loh and Soong Phui Jee

Sin Chew Daily

Wednesday, 5 January 2011

Temperament of an investor: Timing or Pricing

Stock prices rise and fall, so it is human nature to look for a way to profit from such volatility.

There are two possible ways to do so:

1. Timing: To anticipate the rise and fall of the market and of the prices of individual stocks. To buy or hold when they are expected to rise, and to sell or refrain from buying when they appear to be heading down.

2. Pricing: To buy stocks that are priced by the market below their fair value of the underlying business and to sell, or refrain from buying when they are priced above fair value.

Benjamin Graham was convinced that an intelligent investor could profit from focusing on pricing. He was equally convinced that anyone with their emphasis on timing, in the sense of believing their own (or others') forecasts, would end up as a speculator and be doomed to poor financial results over time.

Despite the wisdom of such convictions, Graham also understood most would not listen. "As a matter of business practice, or perhaps of thoroughgoing conviction, the stock brokers and the investment services seem wedded to the principle that both investors and speculators in common stocks should devote careful attention to market forecasts."

There are two possible ways to do so:

1. Timing: To anticipate the rise and fall of the market and of the prices of individual stocks. To buy or hold when they are expected to rise, and to sell or refrain from buying when they appear to be heading down.

Benjamin Graham was convinced that an intelligent investor could profit from focusing on pricing. He was equally convinced that anyone with their emphasis on timing, in the sense of believing their own (or others') forecasts, would end up as a speculator and be doomed to poor financial results over time.

Despite the wisdom of such convictions, Graham also understood most would not listen. "As a matter of business practice, or perhaps of thoroughgoing conviction, the stock brokers and the investment services seem wedded to the principle that both investors and speculators in common stocks should devote careful attention to market forecasts."

Malaysian stocks on bullish sentiment

Wednesday January 5, 2011

Malaysian stocks on bullish sentiment boosted by US data

By LEE KIAN SEONG

lks@thestar.com.my

PETALING JAYA: The FTSE Bursa Malaysia KLCI hit a new high yesterday, closing 18.47 points higher at 1,551.89, on high volume and positive investor sentiment.

Trading volume swelled to over two billion shares as investors were cheered by encouraging data from the United States and regional markets buoyed by rising liquidity.

After a long absence, Malaysia is also back on the radar screen of many international houses.

HwangDBS Investment Management Bhd head of equities Gan Eng Peng noted that last month, manufacturing in the United States grew at its fastest clip in seven months, sending US stocks to two-year highs.

“Investors' reaction was supported by encouraging data from the United States that suggested the economy is improving. Stocks in the United States did well on the first day of trading for the year, and investors call it the January barometer',” he told StarBiz.

Data released in the US on Monday indicated that the manufacturing sector grew in December at its fastest pace in seven months, reinforcing recovery signs.

Gan said foreign investors were increasingly confident about investing in countries like Malaysia.

“For the first time in many years, international research houses have recommended Malaysia as a stock market investment destination over and above many other markets in Asia Pacific .

“If you take this in the context where foreign ownership of stocks remains near historic lows, there could be a lot more buying activity, going forward,” Gan said.

Among the top gainers yesterday were British American Tobacco (M) Bhd which rose 60 sen to RM46.40; Sime Darby Bhd (+ 51 sen to RM9.46); Nestle (M) Bhd (+42 sen to RM43.84) and Ekovest Bhd (+ 37 sen to RM2.74).

Among regional bourses, the Nikkei 225 rose 169.18 points to 10398.10; Hang Seng Index (+232.43 points to 23668.48) and Straits Times (+14.52 points to 3250.29).

Gan said the multiple catalysts announced under the Economic Transformation Plan (ETP) and Budget 2011 would essentially benefit key stock market sectors like construction, building materials and property.

The ETP, if successfully implemented, would help to sustain the momentum.

An analyst from a local investment bank said the gains yesterday on the local bourse was in line with performance of the regional markets with positive news flow from the expected elections in Malaysia.

He said the current resistance level was between 1,560 and 1,570 points while support is between 1,505 and 1,500 points.

Fortress Capital Asset Management chief executive officer Thomas Yong said the rally in the stock market was not only in Malaysia but across regional markets where there was a lot of liquidity.

“Bond yields are currently very low and it is also expensive to invest in bonds. Thus, equities continue to be the preferred instrument at this point of time.

“It is not surprising that the market is going up but it has to do with more than just the expected elections this year,” Yong said.

Investors are moving back into their positions in the market after easing off in the last one month and they are accumulating stocks again.

“Foreign money has been coming in since middle of last year but it is not really huge in terms of large inflows. Certainly, there has been foreign buying but it is more from local investors,” Yong said, adding that commodities-related stocks were favoured by these funds.

It is not easy to judge whether the stock market momentum is sustainable but Yong believes it will sustain in the short term. However, the market is expected to be fairly volatile this year.

On the market risks, Yong pointed out that interest rates were expected to rise later this year and this could affect sentiment.

“Investors expect to see between 15% and 20% growth in corporate earnings in Asia this year. If the growth is not seen in the coming months, market confidence may be affected,” Yong said.

http://biz.thestar.com.my/news/story.asp?file=/2011/1/5/business/7735611&sec=business

Malaysian stocks on bullish sentiment boosted by US data

By LEE KIAN SEONG

lks@thestar.com.my

PETALING JAYA: The FTSE Bursa Malaysia KLCI hit a new high yesterday, closing 18.47 points higher at 1,551.89, on high volume and positive investor sentiment.

Trading volume swelled to over two billion shares as investors were cheered by encouraging data from the United States and regional markets buoyed by rising liquidity.

After a long absence, Malaysia is also back on the radar screen of many international houses.

HwangDBS Investment Management Bhd head of equities Gan Eng Peng noted that last month, manufacturing in the United States grew at its fastest clip in seven months, sending US stocks to two-year highs.

“Investors' reaction was supported by encouraging data from the United States that suggested the economy is improving. Stocks in the United States did well on the first day of trading for the year, and investors call it the January barometer',” he told StarBiz.

Data released in the US on Monday indicated that the manufacturing sector grew in December at its fastest pace in seven months, reinforcing recovery signs.

Gan said foreign investors were increasingly confident about investing in countries like Malaysia.

“For the first time in many years, international research houses have recommended Malaysia as a stock market investment destination over and above many other markets in Asia Pacific .

“If you take this in the context where foreign ownership of stocks remains near historic lows, there could be a lot more buying activity, going forward,” Gan said.

Among the top gainers yesterday were British American Tobacco (M) Bhd which rose 60 sen to RM46.40; Sime Darby Bhd (+ 51 sen to RM9.46); Nestle (M) Bhd (+42 sen to RM43.84) and Ekovest Bhd (+ 37 sen to RM2.74).

Among regional bourses, the Nikkei 225 rose 169.18 points to 10398.10; Hang Seng Index (+232.43 points to 23668.48) and Straits Times (+14.52 points to 3250.29).

Gan said the multiple catalysts announced under the Economic Transformation Plan (ETP) and Budget 2011 would essentially benefit key stock market sectors like construction, building materials and property.

The ETP, if successfully implemented, would help to sustain the momentum.

An analyst from a local investment bank said the gains yesterday on the local bourse was in line with performance of the regional markets with positive news flow from the expected elections in Malaysia.

He said the current resistance level was between 1,560 and 1,570 points while support is between 1,505 and 1,500 points.

Fortress Capital Asset Management chief executive officer Thomas Yong said the rally in the stock market was not only in Malaysia but across regional markets where there was a lot of liquidity.

“Bond yields are currently very low and it is also expensive to invest in bonds. Thus, equities continue to be the preferred instrument at this point of time.

“It is not surprising that the market is going up but it has to do with more than just the expected elections this year,” Yong said.

Investors are moving back into their positions in the market after easing off in the last one month and they are accumulating stocks again.

“Foreign money has been coming in since middle of last year but it is not really huge in terms of large inflows. Certainly, there has been foreign buying but it is more from local investors,” Yong said, adding that commodities-related stocks were favoured by these funds.

It is not easy to judge whether the stock market momentum is sustainable but Yong believes it will sustain in the short term. However, the market is expected to be fairly volatile this year.

On the market risks, Yong pointed out that interest rates were expected to rise later this year and this could affect sentiment.

“Investors expect to see between 15% and 20% growth in corporate earnings in Asia this year. If the growth is not seen in the coming months, market confidence may be affected,” Yong said.

http://biz.thestar.com.my/news/story.asp?file=/2011/1/5/business/7735611&sec=business

Tuesday, 4 January 2011

Is the Stock Market Cheap?

Is the Stock Market Cheap?

The Valuation Thesis

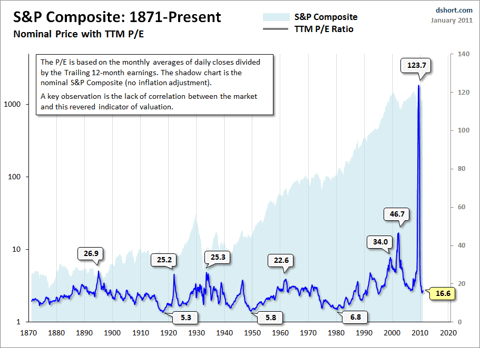

A standard way to investigate market valuation is to study the historic Price-to-Earnings (P/E) ratio using reported earnings for the trailing twelve months (TTM). Proponents of this approach ignore forward estimates because they are often based on wishful thinking, erroneous assumptions, and analyst bias.

The average P/E ratio since the 1870's has been about 15. But the disconnect between price and TTM earnings during much of 2009 was so extreme that the P/E ratio was in triple digits — as high as the 120s — in the Spring of 2009. In 1999, a few months before the top of the Tech Bubble, the conventional P/E ratio hit 34. It peaked close to 47 two years after the market topped out.

As these examples illustrate, in times of critical importance, the conventional P/E ratio often lags the index to the point of being useless as a value indicator. "Why the lag?" you may wonder. "How can the P/E be at a record high after the price has fallen so far?" The explanation is simple. Earnings fell faster than price. In fact, thenegative earnings of 2008 Q4 (-$23.25) is something that has never happened before in the history of the S&P 500.

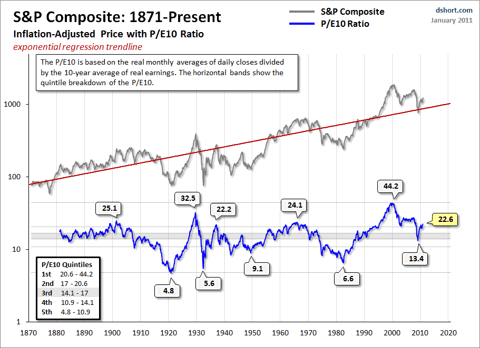

The P/E10 Ratio

Legendary economist and value investor Benjamin Graham noticed the same bizarre P/E behavior during the Roaring Twenties and subsequent market crash. Graham collaborated with David Dodd to devise a more accurate way to calculate the market's value, which they discussed in their 1934 classic book, Security Analysis. They attributed the illogical P/E ratios to temporary and sometimes extreme fluctuations in the business cycle. Their solution was to divide the price by a multi-year average of earnings and suggested 5, 7 or 10-years. In recent years, Yale professor Robert Shiller, the author of Irrational Exuberance, has reintroduced the concept to a wider audience of investors and has selected 10 years as the earnings denominator. As the accompanying chart illustrates, this ratio closely tracks the real (inflation-adjusted) price of the S&P Composite. The historic average is 16.35. Shiller refers to this ratio as the Cyclically Adjusted Price Earnings Ratio, abbreviated as CAPE, or the more precise P/E10, which is my preferred abbreviation.

The Current P/E10

After dropping to 13.4 in March 2009, the P/E10 rebounded above 20. The chart below gives us a historical context for these numbers. The ratio in this chart is doubly smoothed (10-year average of earnings and monthly averages of daily closing prices). Thus the fluctuations during the month aren't especially relevant (e.g., the difference between the monthly average and monthly close P/E10).

Of course, the historic P/E10 has never flat-lined on the average. On the contrary, over the long haul it swings dramatically between the over- and under-valued ranges. If we look at the major peaks and troughs in the P/E10, we see that the high during the Tech Bubble was the all-time high of 44 in December 1999. The 1929 high of 32 comes in at a distant second. The secular bottoms in 1921, 1932, 1942 and 1982 saw P/E10 ratios in the single digits.

Where does the current valuation put us?

For a more precise view of how today's P/E10 relates to the past, our chart includes horizontal bands to divide the monthly valuations into quintiles — five groups, each with 20% of the total. Ratios in the top 20% suggest a highly overvalued market, the bottom 20% a highly undervalued market. What can we learn from this analysis? The Financial Crisis of 2008 triggered an accelerated decline toward value territory, with the ratio dropping to the upper 4th quintile in March 2009. The price rebound since the 2009 low pushed the ratio back into the 1st quintile. By this historic measure, the market is expensive.

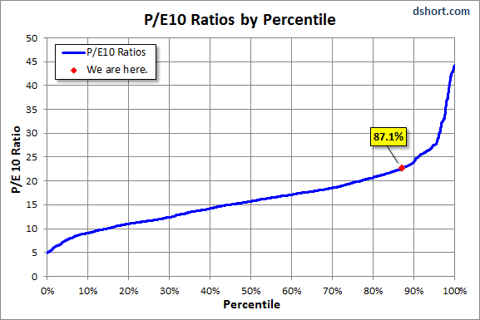

We can also use a percentile analysis to put today's market valuation in the historical context. As the chart below illustrates, latest P/E10 ratio is around the 87th percentile.

A more cautionary observation is that every time the P/E10 has fallen from the first to the fourth quintile, it has ultimately declined to the fifth quintile and bottomed in single digits. Based on the latest 10-year earnings average, to reach a P/E10 in the high single digits would require an S&P 500 price decline below 540. Of course, a happier alternative would be for corporate earnings to make a strong and prolonged surge. When might we see the P/E10 bottom? These secular declines have ranged in length from over 19 years to as few as three. The current decline is now in its tenth year.

Or was March 2009 the beginning of a secular bull market? Perhaps, but the history of market valuations suggests a caution perspective.

(Above graph: real P/E10 based on the ShadowStats Alternate CPI for the inflation adjustment, which suggests that the current market is fairly priced.)

http://seekingalpha.com/article/244408-is-the-stock-market-cheap

Related:

A rally from extreme cheapness to excellent value

Subscribe to:

Posts (Atom)