Benchmarking performance and watching key metrics are essential to evaluating whether your retirement holdings are doing their job.

Adam Zoll23/02/15

Whether your retirement portfolio consists of dozens of holdings or just a few, from time to time, it is a good idea to assess how each is performing and to take a look under the bonnet.

That's why it is important to know which performance benchmarks and key metrics to use when sizing up each holding individually. In doing so, you should look at both past performance and forward-looking measures designed to provide guidance as to how the investment will perform moving forward. That way, you can determine whether things in your portfolio are ticking along just fine, a few upgrades are in order, or whether changes need to be made.

Take the Long View on Past Performance

The metric that investors tend to focus on most, of course, is total return, a backward-looking measure. But reviewing a holding's total return versus its benchmark and peer group requires a dose of perspective. For one thing, it's important not to place too much emphasis on near-term results. If a fund you own has performed poorly of late, try to understand why.

Perhaps the fund's manager has placed an outsized bet on a particular sector that has underperformed in the near term but is poised to rebound soon. Likewise, don't be lulled into overconfidence by near-term outperformance – today’s outperforming investment often becomes tomorrow's underperformer.

Remember that you're investing for a retirement that may be years – if not decades – away, depending on your age. If you're more than 10 years from retirement, you have time to ride out the market's ups and downs. If you're closer to retirement, you may want to ratchet down the risk; but you'll still need to have a good sense of how your holdings may perform once you stop working. Whatever your retirement time frame, focus on your holdings' performance over the trailing five- and 10-year periods, but also pay attention to how they've reacted in different market environments.

You could begin your analysis by focusing on 2008, when the financial meltdown sent stock prices plummeting and bond prices higher. But also look at 2013, when stocks posted strong gains while bonds languished.

Using Appropriate Metrics

Of course, your portfolio probably contains at least a few different asset types, meaning you'll need to pay attention to benchmarks and metrics that are most relevant to each type. For example, volatility and risk measures may be more important to you when it comes to your stock holdings, whereas interest-rate sensitivity probably matters more to you with regard to your bond holdings.

The following guide is designed to point you in the right direction when it comes to benchmarking the performance of various asset types and identifying other important metrics to watch. It's by no means a comprehensive list, but it's a good place to start.

Key forward-looking metrics

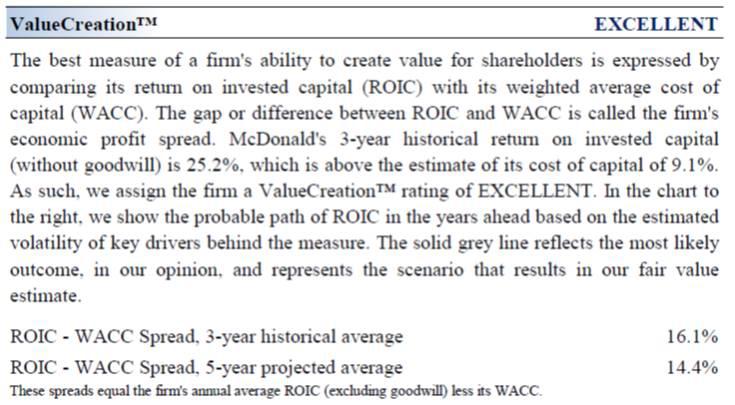

Morningstar Rating for stocks: Represents a stock's current trading price relative to our analyst team's assessment of its fair value price.

Stocks rated at 4 or 5 stars are trading meaningfully below their fair value estimates, meaning they appear to be undervalued, while those rated at 3 stars are fairly priced and those rated at 1 or 2 stars are trading above their fair value, meaning they appear to be overvalued.

Morningstar Economic Moat Rating: Analyst assessment of whether the company has one or more sustainable competitive advantages, with ratings ranging from wide to narrow to none.

Companies with economic moats tend to be better at sustaining profitability over time than those without them.

Key backward-looking metrics

Revenue growth: The amount of money the company brings in year over year, and a good indication of whether it is growing and to what degree.

Operating Margin: A measure of company profitability. The wider the operating margin, the more the company makes on sales of its products or services.

Free Cash Flow: Another measure of company profitability, based on the firm's cash flow from operations minus its capital spending.